|

市場調查報告書

商品編碼

2065775

網路功能虛擬化(NFV):市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Network Function Virtualization (NFV) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

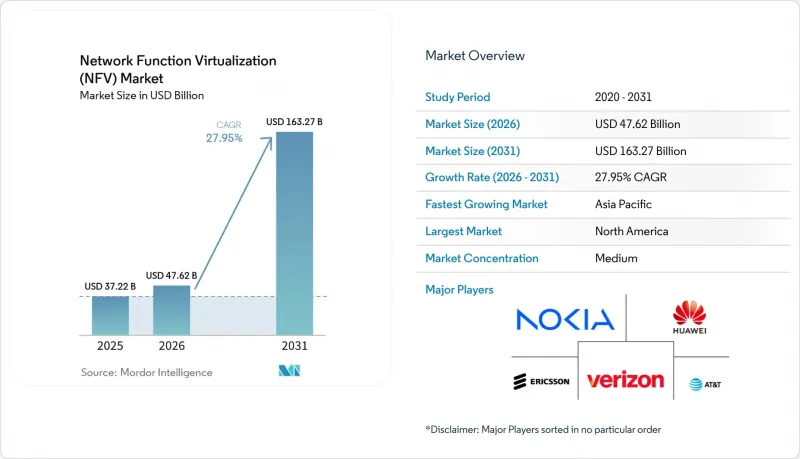

根據 Mordor Intelligence 預測,網路功能虛擬化 (NFV) 市場規模將從 2025 年的 372.2 億美元成長到 2026 年的 476.2 億美元,然後在 2031 年達到 1632.7 億美元,2026 年至 2031 年的複合年成長率為 27.95%。

本報告按元件(硬體、軟體等)、應用(虛擬設備、核心網路虛擬化等)、最終用戶(電信服務供應商、企業等)、部署模式(本地部署、公共雲端等)、虛擬化網路功能(運算等)和地區進行細分。市場預測以美元計價。

全球網路功能虛擬化 (NFV) 市場趨勢與洞察

對 5G 和網路切片的需求日益成長

網路切片技術允許通訊業者在通用基礎設施上建立多個獨立的虛擬網路,每個網路都針對特定的效能目標進行最佳化。透過結合軟體定義網路 (SDN) 和網路功能虛擬化 (NFV) 技術,通訊業者可以動態分配運算、儲存和傳輸資源,從而在幾分鐘內而非幾個月內推出新服務。早期商業切片應用包括自動駕駛汽車遙測、機器人流程自動化 (RPA) 以及智慧城市的感測器回程傳輸。該模型支援基於延遲和可靠性的差異化定價,使通訊業者從單純的頻寬轉售商轉變為服務提供者。

利用雲端原生NFV基礎設施,幫助通訊業者從資本支出(CAPEX)模式轉型為營運支出(OPEX)模式。

容器化網路功能和微服務使通訊業者能夠將單體網路元素拆分並快速部署,從而實現按需付費,僅需為實際使用的資源付費。 Dish 公開宣布投資 100 億美元建造全雲 5G 網路,充分展現了從固定硬體生命週期轉向彈性軟體生命週期的經濟優勢。成本節約不僅來自更低的硬體價格,還來自零接觸配置和自動化生命週期管理,這減少了對現場技術人員的需求,並最大限度地減少了手動配置造成的錯誤。

開放原始碼生態系統可以緩解廠商鎖定問題

O-RAN規範將無線接取網路分解為可互通的元件,而ONAP則提供了一個用於端對端服務編配的開放原始碼平台。透過採用開放介面,通訊業者可以減少對單一供應商的依賴,並加速多供應商創新週期。歐洲監管政策正在積極推廣開放架構,以加強數位主權並降低市場集中風險。

細分市場分析

到2025年,硬體仍將佔網路功能虛擬化(NFV)市場規模的64.30%,因為營運商級的運算和加速卡能夠確保即使在5G流量初期激增的情況下也能實現可預測的吞吐量。然而,在容器化網路功能和人工智慧編配套件的推動下,軟體收入預計將在2031年之前以29.2%的複合年成長率成長。超融合邊緣平台的激增表明,通訊業者正在將運算、儲存和交換功能整合到針對雲端原生封包處理最佳化的單一裝置中。

開放原始碼生態系統進一步推動了軟體的發展勢頭,縮短了開發週期,並促進了社區主導的創新。隨著通訊業者採用 GitOps 和 CI/CD 管線,發布頻率與雲端實務而非硬體更新計畫保持一致。這種轉變正在用可在幾分鐘內部署的可程式設計服務取代客製化設備,重塑整個網路功能虛擬化市場供應商的收入結構。

至2025年,虛擬設備(防火牆、vCPE、vRAN)將佔網路功能虛擬化(NFV)市場規模的44.65%。然而,由於服務敏捷性依賴協調數千個分散式虛擬網路功能(VNF)的意圖驅動型配置引擎,因此編配和自動化預計將以28.2%的複合年成長率成長,超過所有其他類別。通訊業者認為,在流量呈指數級成長的情況下,自動化封閉回路型控制對於實現網路切片貨幣化和維持服務品質至關重要。

容器化正在推動應用多樣化。邊緣 Kubernetes叢集現在承載著輕量級 UPF 和用戶平面加速器,從而支援工業IoT和身臨其境型媒體工作負載。供應商正在將分析和策略執行直接整合到編排器中,模糊了保障和控制之間的傳統界限。這些創新確保網路功能虛擬化市場繼續保持其「軟體優先」的發展軌跡。

區域分析

預計到2025年,北美將佔據網路功能虛擬化市場37.60%的佔有率,這主要得益於AT&T等通訊業者早期在虛擬化領域的投入,以及美國致力於在安全、本土主導的5G基礎設施領域確立領先地位的戰略舉措。聯邦政府對開放式無線接取網路(RAN)研究的激勵措施,加上穩健的資金籌措支持,正在加速商業部署。加拿大通訊業者也遵循類似的路徑,透過封包核心網路現代化來提升網路敏捷性,以滿足嚴格的服務品質要求。

在歐洲,隨著監管機構將數位主權、永續性和競爭置於優先地位,相關技術正穩步普及。歐洲電信監管委員會(BEREC)的雲端邊緣框架正在推廣開放介面和聯邦雲端模型,這些模型與網路功能虛擬化(NFV)自然契合。德國電信和西班牙電信等通訊業者正在試行人工智慧原生編配和GitOps流水線,展示了透過整合動態工作負載減少5%溫室氣體排放的潛力。然而,由於各國法規存在差異,跨境監管協調仍需時日。

亞太地區正以29.3%的複合年成長率成長,成為未來成長的主要驅動力。在中國,隨著5G大規模部署的推進,虛擬化技術正從無線網路逐步應用於核心網路;而在印度,為滿足爆炸性成長的行動數據需求,軟體定義架構的採用正在推動現代化進程。在日本和韓國,5G賦能的私人工廠已運作,充分展現了低延遲邊緣雲端的有效性。東協新興經濟體不受傳統網路的限制,正迅速向雲端原生部署轉型,為整個網路功能虛擬化(NFV)市場的供應商拓展了商機。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對 5G 和網路切片的需求不斷成長

- 利用雲端原生NFV基礎設施,幫助通訊業者從資本支出(CAPEX)模式轉型為營運支出(OPEX)模式。

- 邊緣雲端部署

- AI賦能的MANO及服務保障

- 開放原始碼生態系統(O-RAN、ONAP)可緩解廠商鎖定問題

- 工業 4.0 中私有 5G 的部署正在推動本地 NFV 的發展。

- 市場限制因素

- 與傳統OSS/BSS堆疊整合

- 多廠商虛擬網路功能互通性面臨的挑戰

- 通訊業者缺乏雲端原生營運的技能

- 分散式供應鏈中的安全和合規風險

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 產業生態系和夥伴關係

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 服務

- 透過使用

- 虛擬設備(vCPE、vFW、vRAN)

- 核心網路虛擬化(vEPC、vIMS、vSR)

- 編配與自動化

- 最終用戶

- 電信服務供應商

- 雲端服務供應商

- 公司

- 銀行、金融服務和保險(BFSI)

- 零售與電子商務

- 醫療保健和生命科學

- 製造業和工業

- 政府/國防

- 部署模式

- 現場

- 公共雲端

- 混合/多重雲端

- 按功能分類的虛擬化網路功能

- 計算(虛擬路由器、虛擬交換器)

- 貯存

- 網路(vLoad Balancer、vSR)

- 按地區

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd.

- Ericsson AB

- Nokia Corp.

- VMware Inc.

- Juniper Networks Inc.

- Hewlett Packard Enterprise(HPE)

- Dell Technologies Inc.

- Intel Corp.

- ATandT Inc.

- Verizon Communications Inc.

- ZTE Corp.

- Ribbon Communications

- NEC Corp.

- IBM Corp.

- Samsung Electronics

- Radisys Corp.

- Affirmed Networks(Microsoft)

- Mavenir Systems

- F5 Networks

第7章 市場機會與未來展望

According to Mordor Intelligence, the network function virtualization market size is expected to grow from USD 37.22 billion in 2025 to USD 47.62 billion in 2026 and is forecast to reach USD 163.27 billion by 2031 at 27.95% CAGR over 2026-2031.

This report is Segmented by Component (Hardware, Software, and More), Application (Virtual Appliances, Core Network Virtualization, and More), End User (Telecom Service Providers, Enterprise, and More), Deployment Mode (On-Premise, Public Cloud, and More), Virtualized Network Function (Compute, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Network Function Virtualization (NFV) Market Trends and Insights

Rising demand for 5G and network slicing

Network slicing lets operators create multiple isolated virtual networks on common infrastructure, each optimized for specific performance targets. By pairing software-defined networking with NFV, carriers dynamically allocate compute, storage, and transport resources to run new services in minutes rather than months. Early commercial slices span autonomous vehicle telemetry, robotic process automation, and smart-city sensor backhaul. The model supports differentiated pricing linked to latency or reliability, repositioning operators from bandwidth resellers to service enablers.

Telco CAPEX-to-OPEX shift via cloud-native NFV infrastructure

Containerized network functions and microservices allow operators to decompose monolithic network elements, spin them up rapidly, and pay only for the resources consumed. Dish's public commitment to spend USD 10 billion on an all-cloud 5G network showcases the financial appeal of shifting fixed hardware cycles toward elastic software lifecycles. Cost savings emerge not merely from cheaper hardware but from zero-touch provisioning and automated life-cycle management that cut field-engineering visits and manual configuration errors.

Open-Source ecosystems lowering vendor lock-in

The O-RAN specification disaggregates radio access networks into interoperable components, while ONAP delivers an open-source platform for end-to-end service orchestration. Carriers using open interfaces reduce single-vendor dependence and accelerate multivendor innovation cycles. Europe's regulatory agenda actively promotes open architectures to strengthen digital sovereignty and curb concentration risk.

Other drivers and restraints analyzed in the detailed report include:

- Edge-cloud deployments for URLLC and mMTC use-cases

- AI-Driven MANO and service assurance

- Private-5G adoption in Industry 4.0 driving on-prem NFV

- Integration with legacy OSS/BSS stacks

- Multi-vendor VNF interoperability gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware still underpins 64.30% of the 2025 network function virtualization market size because carrier-grade compute and acceleration cards guarantee predictable throughput during early 5G traffic spikes. Yet software revenues, propelled by container network functions and AI orchestration suites, are set to grow at 29.2% CAGR through 2031. A surge in hyper-converged edge platforms illustrates how operators bundle compute, storage, and switching in a single appliance optimized for cloud-native packets.

Software's momentum is reinforced by open-source ecosystems that shorten development cycles and encourage community-driven innovation. As operators adopt GitOps and CI/CD pipelines, release cadences mirror cloud disciplines rather than hardware refresh timelines. This transition displaces bespoke appliances with programmable services deployable in minutes, reshaping vendor economics across the network function virtualization market.

In 2025 virtual appliances-firewalls, vCPE, and vRAN-occupied 44.65% share of the network function virtualization market size. Orchestration and automation, however, will outpace all other categories at a 28.2% CAGR because service agility depends on intent-driven provisioning engines that coordinate thousands of distributed VNFs. Operators view automated closed-loop control as indispensable to monetizing network slices and maintaining quality of service amid exponential traffic growth.

Containerization is catalyzing application diversity. Edge Kubernetes clusters now host lightweight UPFs and user plane accelerators, enabling industrial IoT and immersive media workloads. Vendors integrate analytics and policy enforcement directly inside orchestrators, collapsing traditional boundaries between assurance and control domains. These innovations keep the network function virtualization market firmly on a software-first trajectory.

Geography Analysis

North America's 37.60% network function virtualization market share in 2025 stems from early virtualization initiatives by operators such as AT&T and the United States' strategic push for secure, domestic 5G infrastructure leadership. Federal incentives for open-RAN research, coupled with ample capital access, accelerate commercial deployments. Canadian carriers follow similar trajectories, modernizing packet cores to increase agility and satisfy aggressive service-quality mandates.

Europe registers steady adoption as regulators prioritize digital sovereignty, sustainability, and competition. BEREC's cloud-edge framework encourages open interfaces and federated cloud models that align naturally with NFV. Operators like Deutsche Telekom and Telefonica pilot AI-native orchestration and GitOps pipelines, demonstrating potential 5% greenhouse-gas reductions from dynamic workload consolidation. Fragmented national rules, however, prolong cross-border harmonization.

Asia-Pacific's 29.3% CAGR makes it the powerhouse of future growth. China's sweeping 5G rollout embeds virtualization from the radio to the core, while India's modernization drive embraces software-defined architectures to meet exploding mobile-data demand. Japan and South Korea already run private 5G-enabled factories, validating low-latency edge clouds. Emerging ASEAN economies, unencumbered by legacy networks, jump straight to cloud-native deployments, broadening supplier opportunities across the network function virtualization market.

- Cisco Systems Inc.

- Huawei Technologies Co. Ltd.

- Ericsson AB

- Nokia Corp.

- VMware Inc.

- Juniper Networks Inc.

- Hewlett Packard Enterprise (HPE)

- Dell Technologies Inc.

- Intel Corp.

- ATandT Inc.

- Verizon Communications Inc.

- ZTE Corp.

- Ribbon Communications

- NEC Corp.

- IBM Corp.

- Samsung Electronics

- Radisys Corp.

- Affirmed Networks (Microsoft)

- Mavenir Systems

- F5 Networks

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for 5G and network slicing

- 4.2.2 Telco CAPEX-to-OPEX shift via cloud-native NFV Infrastructure

- 4.2.3 Edge-cloud deployments for URLLC and mMTC use-cases

- 4.2.4 AI-driven MANO and service assurance

- 4.2.5 Open-source ecosystems (O-RAN, ONAP) lowering vendor lock-in

- 4.2.6 Private-5G adoption in Industry 4.0 driving on-prem NFV

- 4.3 Market Restraints

- 4.3.1 Integration with legacy OSS/BSS stacks

- 4.3.2 Multi-vendor VNF interoperability gaps

- 4.3.3 Telco skill-set shortage for cloud-native operations

- 4.3.4 Security and compliance risks in disaggregated supply chain

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Industry Ecosystem and Partnerships

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Application

- 5.2.1 Virtual Appliances (vCPE, vFW, vRAN)

- 5.2.2 Core Network Virtualization (vEPC, vIMS, vSR)

- 5.2.3 Orchestration and Automation

- 5.3 By End User

- 5.3.1 Telecom Service Providers

- 5.3.2 Cloud Service Providers

- 5.3.3 Enterprises

- 5.3.3.1 Banking, Financial Services, and Insurance (BFSI)

- 5.3.3.2 Retail and e-Commerce

- 5.3.3.3 Healthcare and Life Sciences

- 5.3.3.4 Manufacturing and Industrial

- 5.3.3.5 Government and Defense

- 5.4 By Deployment Mode

- 5.4.1 On-premise

- 5.4.2 Public Cloud

- 5.4.3 Hybrid / Multi-cloud

- 5.5 By Virtualized Network Function

- 5.5.1 Compute (vRouter, vSwitch)

- 5.5.2 Storage

- 5.5.3 Network (vLoad Balancer, vSR)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems Inc.

- 6.4.2 Huawei Technologies Co. Ltd.

- 6.4.3 Ericsson AB

- 6.4.4 Nokia Corp.

- 6.4.5 VMware Inc.

- 6.4.6 Juniper Networks Inc.

- 6.4.7 Hewlett Packard Enterprise (HPE)

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Intel Corp.

- 6.4.10 ATandT Inc.

- 6.4.11 Verizon Communications Inc.

- 6.4.12 ZTE Corp.

- 6.4.13 Ribbon Communications

- 6.4.14 NEC Corp.

- 6.4.15 IBM Corp.

- 6.4.16 Samsung Electronics

- 6.4.17 Radisys Corp.

- 6.4.18 Affirmed Networks (Microsoft)

- 6.4.19 Mavenir Systems

- 6.4.20 F5 Networks

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet Need Analysis

網路功能虛擬化 (NFV) 市場報告:按產品/服務、部署方式、企業規模、應用領域、最終用戶和地區分類 (2026–2034)

網路功能虛擬化 (NFV) 市場報告:按產品/服務、部署方式、企業規模、應用領域、最終用戶和地區分類 (2026–2034) 網路功能虛擬化 (NFV) 市場:按組件、功能、最終用戶和部署模式分類——2026 年至 2032 年全球市場預測

網路功能虛擬化 (NFV) 市場:按組件、功能、最終用戶和部署模式分類——2026 年至 2032 年全球市場預測 2026年全球網路功能虛擬化市場報告

2026年全球網路功能虛擬化市場報告 網路功能虛擬化 (NFV) 市場,全球預測至 2032 年:按組件、部署模型、主要用例、組織類型、技術、最終用戶和地區分類

網路功能虛擬化 (NFV) 市場,全球預測至 2032 年:按組件、部署模型、主要用例、組織類型、技術、最終用戶和地區分類 網路功能虛擬化市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、公司規模、最終用戶、地區和競爭格局分類,2021-2031年)

網路功能虛擬化市場 - 全球產業規模、佔有率、趨勢、機會及預測(按組件、公司規模、最終用戶、地區和競爭格局分類,2021-2031年) 網路功能虛擬化 (NFV) 市場規模、佔有率和成長分析(按組件、部署類型、組織規模、應用、最終用戶和地區分類)—2026-2033 年產業預測

網路功能虛擬化 (NFV) 市場規模、佔有率和成長分析(按組件、部署類型、組織規模、應用、最終用戶和地區分類)—2026-2033 年產業預測 SDN 和 NFV - 全球市場佔有率和排名、總收入和需求預測(2025-2031 年)

SDN 和 NFV - 全球市場佔有率和排名、總收入和需求預測(2025-2031 年) 5G核心網路進展及部署模式:調查結果與分析

5G核心網路進展及部署模式:調查結果與分析 雲端原生自動化和ETSI NFV MANO:演進,轉移,共存策略

雲端原生自動化和ETSI NFV MANO:演進,轉移,共存策略