|

市場調查報告書

商品編碼

2065753

家用服務機器人:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Domestic Service Robots - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

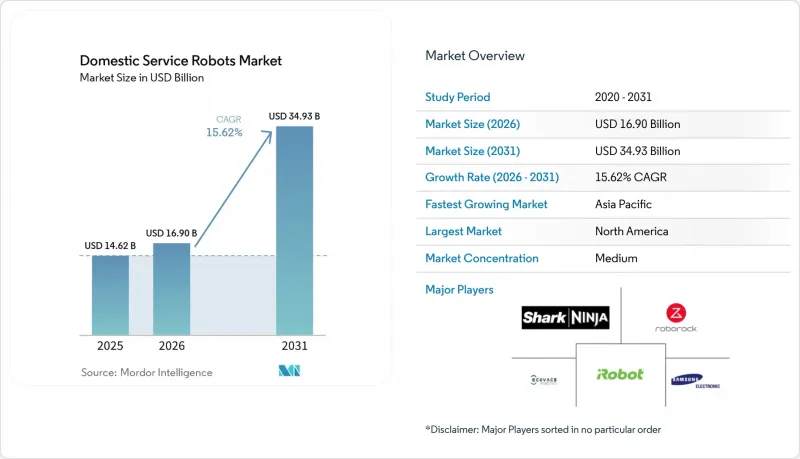

根據 Mordor Intelligence 預測,家庭服務機器人市場規模將從 2025 年的 146.2 億美元成長到 2026 年的 169 億美元,然後在 2031 年達到 349.3 億美元,2026 年至 2031 年的複合年成長率為 15.62%。

本報告按機器人類型(例如,地板清潔機器人、割草機器人)、應用(例如,吸塵/拖地功能、割草、泳池清潔)、連接性和智慧水平(例如,獨立式、Wi-Fi 連接)、銷售管道(例如,線上零售、線下零售)和地區(北美、南美、歐洲、亞太、中東和非洲)進行分類。

全球家庭服務機器人市場趨勢及洞察

智慧家庭生態系統的普及應用不斷擴大

製造商已重新定義家用機器人,不再將其視為孤立的設備,而是移動控制中心。透過與行動平台上的語音助理(例如 Alexa)整合,可以集中控制每個房間的照明、溫度和娛樂系統,使機器人成為家庭自動化系統的核心。供應商優先考慮開放 API,以確保與現有感測器和攝影機無縫整合。這種轉變吸引了生態系統投資者,他們將定期軟體更新視為維持價值的手段。

人口老化與維生的需求

日本超老齡化社會促使開展社會支持機器人試點項目,以減輕護理人員的負擔。臨床研究表明,機器人輔助療法在自閉症和失智症治療方面具有中等至較高的接受度,這加快了對陪伴平台的津貼。政府對家庭監控解決方案的激勵措施促使供應商將跌倒偵測和服藥提醒功能整合到產品中,進一步鞏固了家庭服務機器人市場的成長動能。

資料隱私與網路安全風險

2024 年發生的一起備受矚目的漏洞利用事件動搖了消費者的信任,表明攻擊者可以劫持掃地機器人、傳輸影像串流並傳播仇恨言論。 2025 年 9 月生效的歐盟資料保護法明確規定,設備製造商必須僅在獲得用戶同意的情況下共用數據,並確保數據可攜性。隨著企業採用零信任架構、安全啟動和端對端加密等技術,合規方面的投入也隨之增加。那些展現「隱私設計」概念的供應商獲得了市場優勢。

細分市場分析

到2025年,由於早期商業化和導航感測器成本的下降,地面清潔機器人將佔據家用服務機器人市場64.70%的佔有率。同時,受人口結構變化和對話式人工智慧進步的推動,陪伴機器人預計到2031年將以17.60%的複合年成長率成長。隨著健康保險公司試行居家監測的保險報銷方案,陪伴型家用服務機器人的市場規模預計將迅速擴大。石科技(Roborock)全球市佔率躍升至16%,清楚展現了敏捷的韌體更新和在地化零件的優勢。廚房自動化原型,包括能夠攪拌、翻炒和裝盤食物的機械臂,拓展了創新管道,從餐廳試點項目走向了高階住宅展示室。

在擁有大片土地的郊區,機器人割草機細分市場實現了兩位數的成長,這主要得益於不受邊界限制的視覺SLAM技術的進步。泳池清潔機器人則在重視水質持續監測的富裕住宅群體中保持著一定的市場佔有率。寵物護理機器人雖然絕對數量不多,但由於寵物日益“擬人化”,吸引了大量創業投資資金投資。跨領域的功能轉變也屢見不鮮,例如割草機中出現了自動垃圾處理功能,這反映了技術協同效應,縮短了產品開發週期。

到2025年,吸塵器和拖把將維持家用服務機器人市場65.60%的佔有率,鞏固其作為將自主機器人操作整合到家庭中的「入門級」設備的地位。隨著老齡化社會對跌倒檢測、認知刺激和遠距生命徵象記錄的需求不斷成長,預計到2031年,老年護理和陪伴應用將以17.70%的複合年成長率成長。隨著保險公司開始在保費計算中反映再入院率的降低,護理應用在家用服務機器人市場的佔有率預計將會擴大。在當地法規允許使用行動攝影機的地區,監控功能已逐漸受到關注,但由於隱私問題,其廣泛應用受到阻礙。將清潔、安防和娛樂功能整合於機殼的多模態機器人的普及,無需投資新硬體即可創造提升銷售機會。

在人手不足且時薪高的地區,對機器人割草服務的需求迅速成長。開發商利用基於攝影機的地理圍欄技術解決了諸如邊界標記等初期部署難題。改良的過濾技術縮短了維護週期,從而帶動了泳池清潔機器人的穩定更換需求。功能的多樣化使得機器人能夠同時執行多項家務,即使單一機器人處於非運作狀態,也能最大限度地提高電池容量的投資回報率,這一趨勢尤其顯著。

區域分析

預計2025年,北美將佔據國內服務機器人市場38.30%的佔有率。這主要得益於較高的可支配收入、智慧家庭的廣泛普及以及清晰的問責機制。零售商已推出延長保固服務,以消除消費者對接受度的擔憂。該地區訂閱服務的蓬勃發展也進一步增強了持續獲利的前景。

預計到2031年,亞太地區的複合年成長率將達到19.70%,主要得益於韓國全球領先的機器人普及率以及日本面臨的人口結構挑戰。中國品牌憑藉大規模生產和本地零件生態系統,實現了具有競爭力的成本績效,即使在國內需求趨於平穩的情況下,也依然推動了出口成長。

隨著監管機構最終確定「數據法」和人工智慧責任法規,歐洲家用服務機器人市場迅速擴張。這創造了一個既和諧又嚴格的合規環境,使那些在隱私保護方面享有良好聲譽的公司獲得了優勢。在斯堪地那維亞,節能充電站試點計畫與可再生能源網路結合,將家用機器人與永續性目標連結起來。西方消費者對道德規範的審查日益嚴格,並要求資料處理更加透明。

初期成長主要集中在南美洲、中東和非洲。儘管外匯波動和進口關稅阻礙了初期銷售,但訂閱服務的推出降低了高價的猶豫。當地經銷商與全球品牌合作,簡化了清關和售後服務物流流程,同時城市管理部門在封閉式社區試行推行機器人輔助垃圾分類。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大智慧家庭生態系統的應用

- 人口老化和對輔助住宅的需求

- 國內勞動力短缺

- 住宅保險風險緩解計劃

- 基於訂閱的RaaS模式可以降低資本支出。

- 強調室內空氣品質的衛生標籤

- 市場限制因素

- 資料隱私與網路安全風險

- 多功能機器人的初始成本高

- 國內物聯網標準碎片化

- 兒童與機器人之間關係的倫理問題

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素的影響

- 投資分析

第5章 市場規模與成長預測

- 按機器人類型

- 地板清潔機器人

- 割草機器人

- 泳池清潔機器人

- 陪伴機器人、社交互動機器人

- 廚房和烹飪機器人

- 寵物護理機器人

- 其他類型的機器人

- 透過使用

- 吸塵和拖地

- 割草

- 泳池清潔

- 監控與家庭安全

- 陪伴/老年護理

- 寵物娛樂和餵養

- 其他用途

- 連接性和智慧水平

- 獨立型(無連接性)

- 已連線 Wi-Fi

- AI輔助(例如,視覺SLAM)

- 多機器人協作系統

- 透過分銷管道

- 線上零售

- 線下零售

- 直接訂閱/RaaS

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- ASEAN

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- UAE

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- iRobot Corporation

- Ecovacs Robotics Co. Ltd.

- Roborock Technology Co. Ltd.

- Samsung Electronics Co. Ltd.

- Neato Robotics LLC

- SharkNinja Operating LLC

- Xiaomi Corp.(Dreame & Mijia)

- Dyson Technology Ltd.

- LG Electronics Inc.

- Panasonic Holdings Corp.

- Cecotec Innovaciones SL

- Husqvarna Group(Gardena)

- Maytronics Ltd.

- Segway-Ninebot Group

- Ubtech Robotics Inc.

- ZMP Inc.

- F&P Robotics AG

- Bobsweep Inc.

- ILIFE Innovation Ltd.

- Tertill Corporation

- Eufy(Anker Innovations)

- Karcher GmbH & Co. KG

- Midea Group(Cozii & Eureka)

- Matic Robotics

- Trifo Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the domestic service robots market size is expected to grow from USD 14.62 billion in 2025 to USD 16.9 billion in 2026 and is forecast to reach USD 34.93 billion by 2031 at 15.62% CAGR over 2026-2031.

This report is Segmented by Robot Type (Floor-Cleaning Robots, Lawn-Mowing Robots, and More), Application (Vacuuming and Mopping, Lawn Mowing, Pool Cleaning, and More), Connectivity and Intelligence Level (Stand-Alone, Wi-Fi Connected, and More), Distribution Channel (Online Retail, Offline Retail, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Global Domestic Service Robots Market Trends and Insights

Growing adoption in smart-home ecosystems

Manufacturers repositioned domestic robots as roaming control hubs rather than isolated gadgets. Voice-assistant tie-ins, such as Alexa integration with mobile platforms, enabled room-to-room orchestration of lighting, climate, and entertainment, elevating robots to the centre of home automation. Hardware vendors prioritised open APIs to ensure frictionless onboarding with existing sensors and cameras. The shift attracted ecosystem investors who view recurring software updates as value retention levers.

Aging population and assisted-living demand

Japan's super-aged society catalysed social-assistive robot pilots that supplemented overstretched caregiving staff. Clinical studies recorded moderate to high acceptance of robot-mediated therapy for autism and dementia, accelerating grant funding for companion platforms. Government incentives for in-home monitoring solutions encouraged vendors to embed fall-detection and medication-reminder modules, fortifying the domestic service robots market growth narrative.

Data privacy and cybersecurity risks

High-profile exploits in 2024 allowed attackers to commandeer robot vacuums, stream video feeds, and broadcast hate speech, shaking consumer confidence. The EU Data Act, effective September 2025, placed explicit obligations on device makers to share data only with user consent and to enable data porting. Compliance investments rose as firms adopted zero-trust architectures, secure boot, and end-to-end encryption. Vendors able to validate privacy-by-design gained a marketing edge.

Other drivers and restraints analyzed in the detailed report include:

- Labour shortages for domestic chores

- Subscription-based RaaS lowers CAPEX

- Ethical worries over child-robot bonding

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Floor-cleaning models controlled a 64.70% domestic service robots market share in 2025, benefiting from early commercialisation and falling navigation sensor costs. Companion robots, however, are projected to mark an 17.60% CAGR through 2031, powered by demographic shifts and improved conversational AI. The domestic service robots market size for companion units is expected to rise sharply as healthcare insurers test reimbursement schemes for in-home monitoring. Roborock's leap to 16% global share illustrated the advantage of agile firmware updates and regionally sourced components. Kitchen-automation prototypes, including robotic arms that stir, flip, and plate meals, moved from restaurant pilots to premium residential showrooms, widening the innovation funnel.

The lawn-mowing subcategory recorded double-digit growth in large-lot suburbs, boosted by improvements in boundary-free visual SLAM. Pool-cleaning robots preserved a niche among luxury homeowners who prioritise continuous water-quality monitoring. Pet-care robots, though small in absolute numbers, saw a venture funding influx due to rising pet humanisation. Cross-segment feature migration, such as self-emptying dustbins appearing in lawn mowers, signalled engineering synergies that compress product-development cycles.

Vacuuming and mopping retained 65.60% share of the domestic service robots market size in 2025, cementing their role as gateway purchases that familiarised households with robotic autonomy. Elder-care and companionship applications are forecast to deliver an 17.70% CAGR to 2031 as ageing societies demand fall alerts, cognitive stimulation, and remote vitals logging. The domestic service robots market share of care applications is set to expand when insurers factor reduced hospital readmissions into premium calculations. Surveillance functions gained traction where local regulations allowed mobile cameras, although privacy sensitivities limited blanket adoption. Multi-modal units that blend cleaning, security, and entertainment within one chassis proliferated, enabling upsell paths without new hardware investment.

Demand for robotic lawn services accelerated in regions with labour shortages and high hourly wage rates. Developers addressed early adoption hurdles-such as boundary wire placement-through camera-based geofencing. Pool-cleaning robots achieved steady replacement demand as filter technology improvements reduced maintenance intervals. Functional diversification underscored a trend where single robots tackle multiple chores during idle cycles, maximising return on battery capacity.

Geography Analysis

North America commanded 38.30% of the domestic service robots market share in 2025, buoyed by high disposable income, established smart-home penetration, and clear liability frameworks. Retailers integrated extended warranties that eased adoption anxiety. The region's subscription uptake amplified recurring revenue visibility.

Asia-Pacific is projected to post a 19.70% CAGR to 2031, driven by South Korea's world-leading robot density and Japan's demographic urgency. Chinese brands leveraged scale manufacturing and local component ecosystems to offer competitive price-performance ratios, facilitating export surges once domestic demand plateaued.

Europe's domestic service robots market size expanded as regulators finalised the Data Act and AI liability rules, creating a harmonised yet strict compliance landscape that favoured firms with strong privacy credentials. Scandinavian countries piloted energy-efficient charging stations tied to renewable power grids, tying domestic robots to sustainability targets. Western European consumers displayed heightened ethical scrutiny, prompting transparent data-handling disclosures.

South America and the Middle East and Africa recorded early-stage growth. Currency volatility and import duties weighed on upfront sales, but subscription offerings reduced sticker shock. Local distributors partnered with global brands to navigate customs and after-sales logistics, while city authorities tested robot-assisted waste sorting in gated communities.

- iRobot Corporation

- Ecovacs Robotics Co. Ltd.

- Roborock Technology Co. Ltd.

- Samsung Electronics Co. Ltd.

- Neato Robotics LLC

- SharkNinja Operating LLC

- Xiaomi Corp. (Dreame & Mijia)

- Dyson Technology Ltd.

- LG Electronics Inc.

- Panasonic Holdings Corp.

- Cecotec Innovaciones S.L.

- Husqvarna Group (Gardena)

- Maytronics Ltd.

- Segway-Ninebot Group

- Ubtech Robotics Inc.

- ZMP Inc.

- F&P Robotics AG

- Bobsweep Inc.

- ILIFE Innovation Ltd.

- Tertill Corporation

- Eufy (Anker Innovations)

- Karcher GmbH & Co. KG

- Midea Group (Cozii & Eureka)

- Matic Robotics

- Trifo Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing adoption in smart-home ecosystems

- 4.2.2 Aging population and assisted-living demand

- 4.2.3 Labour shortages for domestic chores

- 4.2.4 Home-insurance risk-mitigation programs

- 4.2.5 Subscription-based RaaS lowers CAPEX

- 4.2.6 Indoor-air-quality driven hygiene labels

- 4.3 Market Restraints

- 4.3.1 Data-privacy and cyber-security risks

- 4.3.2 High upfront cost of multi-function robots

- 4.3.3 Fragmented domestic-IoT standards

- 4.3.4 Ethical worries over child-robot bonding

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of Substitute Products

- 4.7.4 Intensity of Competitive Rivalry

- 4.7.5 Threat of New Entrants

- 4.8 Impact of Macroeconomic Factors

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Robot Type

- 5.1.1 Floor-Cleaning Robots

- 5.1.2 Lawn-Mowing Robots

- 5.1.3 Pool-Cleaning Robots

- 5.1.4 Companion and Social-Interaction Robots

- 5.1.5 Kitchen and Food-Preparation Robots

- 5.1.6 Pet-Care Robots

- 5.1.7 Other Robot Types

- 5.2 By Application

- 5.2.1 Vacuuming and Mopping

- 5.2.2 Lawn Mowing

- 5.2.3 Pool Cleaning

- 5.2.4 Surveillance and Home Security

- 5.2.5 Companionship and Elderly Care

- 5.2.6 Pet Entertainment and Feeding

- 5.2.7 Other Applications

- 5.3 By Connectivity and Intelligence Level

- 5.3.1 Stand-alone (No Connectivity)

- 5.3.2 Wi-Fi Connected

- 5.3.3 AI-Assisted (Visual-SLAM etc.)

- 5.3.4 Multi-Robot Coordinated Systems

- 5.4 By Distribution Channel

- 5.4.1 Online Retail

- 5.4.2 Offline Retail

- 5.4.3 Direct Subscription / RaaS

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 UAE

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 iRobot Corporation

- 6.4.2 Ecovacs Robotics Co. Ltd.

- 6.4.3 Roborock Technology Co. Ltd.

- 6.4.4 Samsung Electronics Co. Ltd.

- 6.4.5 Neato Robotics LLC

- 6.4.6 SharkNinja Operating LLC

- 6.4.7 Xiaomi Corp. (Dreame & Mijia)

- 6.4.8 Dyson Technology Ltd.

- 6.4.9 LG Electronics Inc.

- 6.4.10 Panasonic Holdings Corp.

- 6.4.11 Cecotec Innovaciones S.L.

- 6.4.12 Husqvarna Group (Gardena)

- 6.4.13 Maytronics Ltd.

- 6.4.14 Segway-Ninebot Group

- 6.4.15 Ubtech Robotics Inc.

- 6.4.16 ZMP Inc.

- 6.4.17 F&P Robotics AG

- 6.4.18 Bobsweep Inc.

- 6.4.19 ILIFE Innovation Ltd.

- 6.4.20 Tertill Corporation

- 6.4.21 Eufy (Anker Innovations)

- 6.4.22 Karcher GmbH & Co. KG

- 6.4.23 Midea Group (Cozii & Eureka)

- 6.4.24 Matic Robotics

- 6.4.25 Trifo Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

家用服務機器人市場預測至2034年—按產品類型、組件、技術、應用、最終用戶和地區分類的全球分析

家用服務機器人市場預測至2034年—按產品類型、組件、技術、應用、最終用戶和地區分類的全球分析 服務機器人市場-全球產業規模、佔有率、趨勢、機會和預測:按運行環境、應用、最終用戶、地區和競爭對手分類,2021-2031年

服務機器人市場-全球產業規模、佔有率、趨勢、機會和預測:按運行環境、應用、最終用戶、地區和競爭對手分類,2021-2031年 服務機器人市場:按產品類型、組件類型、運輸方式和最終用戶分類 - 全球市場預測 2026–2032

服務機器人市場:按產品類型、組件類型、運輸方式和最終用戶分類 - 全球市場預測 2026–2032 2026-2034年全球家用機器人市場規模、佔有率、趨勢和成長分析報告

2026-2034年全球家用機器人市場規模、佔有率、趨勢和成長分析報告 2026年航太服務機器人市場報告全球服務機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

2026年航太服務機器人市場報告全球服務機器人市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 服務機器人市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、形式、部署形式、最終用戶、功能2026年全球服務機器人市場報告購物指南機器人市場:依產品類型、支付方式、經營模式、通路和最終用戶分類-2026-2032年全球預測公共間機器人市場:按機器人類型、清潔技術、運作模式、通路、應用程式和終端用戶產業分類,全球預測(2026-2032年)

服務機器人市場分析及預測(至2035年):類型、產品類型、服務、技術、組件、應用、形式、部署形式、最終用戶、功能2026年全球服務機器人市場報告購物指南機器人市場:依產品類型、支付方式、經營模式、通路和最終用戶分類-2026-2032年全球預測公共間機器人市場:按機器人類型、清潔技術、運作模式、通路、應用程式和終端用戶產業分類,全球預測(2026-2032年)