|

市場調查報告書

商品編碼

2065612

無線電力傳輸:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Wireless Power Transmission - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

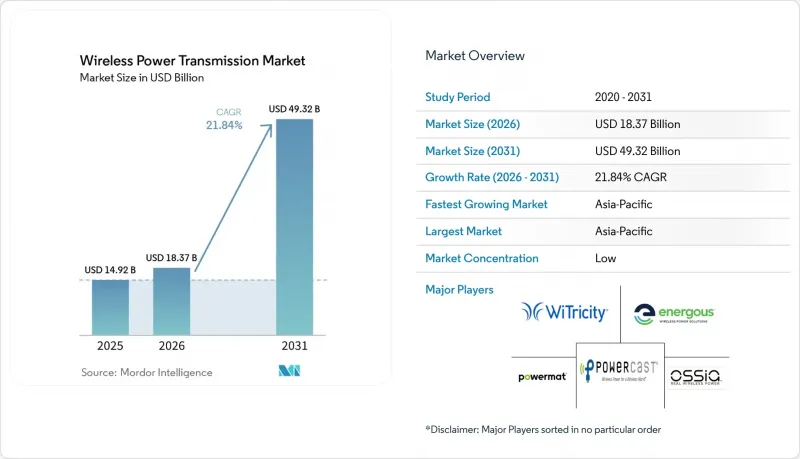

據 Mordor Intelligence 稱,2025 年無線電力傳輸市場價值為 149.2 億美元,預計到 2031 年將達到 493.2 億美元,而 2026 年為 183.7 億美元,預測期(2026-2031 年)的複合年成長率為 21.84%。

本報告按技術(例如,感應耦合)、傳輸範圍(短、中、長)、應用(例如,智慧型手機和平板電腦、穿戴式電子設備)、組件(例如,發送器、接收器、電源管理和控制整合電路、磁性材料和屏蔽層)以及地區進行細分。市場預測以美元計價。

全球無線電力傳輸市場趨勢與洞察

智慧型手機和穿戴式裝置廣泛採用無線充電技術

主流智慧型手機和穿戴式裝置對無線快充的廣泛應用,直接推動了無線電力傳輸市場的發展。 2025年7月推出的Qi2 v2.2.1標準,將充電功率提升至25W,縮小了與有線快充的差距,並消除了許多消費者的購買障礙。此次更新透過提升效能並著重增強消費者充電層的互通性,進一步推動了磁吸式充電技術的普及。此外,根據無線充電聯盟(Wireless Power Consortium)統計,Qi2標準推出一年內,已有15億台支援該標準的裝置進入市場,展現了其快速的部署速度。無線電力傳輸市場也受益於“配件效應”,因為購買了磁吸式充電器、錢包、支架和行動電源的消費者,在升級設備時往往會繼續使用相同的兼容產品。

電動汽車無線充電技術的加速發展與車輛電氣化進程

電動車試點計畫向商業化部署的轉變也推動了無線電力傳輸市場的發展。 2025年10月,Electreon在法國啟動了“A10計畫”,在實際交通條件下演示了300千瓦的感應式電力傳輸。這為道路營運商和汽車製造商提供了實際基礎設施的具體案例,而不僅僅是實驗室結果。 2026年3月,Electreon完成了對InductEV的收購,將動態和固定式充電相關的智慧財產權整合到一家公司旗下。此次總合使Electreon獲得了約400項專利。同樣在2025年12月,普渡大學在美國一條公共道路測試路段上成功演示了以65英里/小時的速度為一輛8級卡車進行190千瓦的充電,這表明大型車輛的應用案例正在進入全面檢驗階段。即使不考慮能量傳輸成本,無線電力傳輸市場的發展勢頭也更加強勁,因為在高頻物流環境中,充電站營運商可以減少插頭操作、操作時間和連接器磨損。

線圈錯位或熱負荷導致的效率降低

當實際應用環境與理想測試條件差異時,無線電力傳輸市場仍面臨實際效率的挑戰。根據IEEE ISSCC於2025年2月發布的研究,小型化無線電力傳輸中增強型頻分複用架構的端對端效率為60.2%。雖然這代表著顯著的進步,但與同等功率等級的最佳化有線充電相比,仍然相差甚遠。接收端的熱集中帶來了進一步的挑戰,尤其是在功率超過15W的消費性電子設備中,熱限制會降低輸出功率。在汽車應用中,高功率系統還需要冷卻和控制基礎設施,這抵消了無線充電通常被認為是其優勢的「便利性」。 2025年12月,Electreon和Infineon在示範使用碳化矽元件實現300kW感應式充電時,強調了這些高功率挑戰,因為溫度控管對於實現如此高的功率密度仍然至關重要。

細分市場分析

到2025年,感應耦合將佔無線電力傳輸市場銷售額的42.61%,成為該市場最大的技術板塊。這主要得益於Qi認證消費性硬體已建立的全球供應鏈。其主導地位的驅動力在於相容性、生產規模以及充電器和接收器設備的大規模部署經驗。目前,無線電力傳輸產業在行動電話、平板電腦和許多日常配件中仍然高度依賴感應耦合,因為該技術成熟且易於理解。然而,由於傳輸距離短且對準要求嚴格,感應耦合在使用者無法精確定位設備的應用場景中適用性有限。目前,諧振感應耦合正憑藉其對線圈偏移的更高接受度以及即使在較大間距下也能支持高功率功率傳輸的能力,在無線電力傳輸市場嶄露頭角。預計到2031年,諧振感應耦合的複合年成長率將達到22.84%,成為無線電力傳輸市場成長最快的技術方向。 Electreon於2025年10月在A10高速公路上進行的現場測試顯示,在實際交通條件下,該架構的峰值輸出功率達到了300千瓦,為該架構的商業化應用提供了示範案例。此外,在產品認證方面,那些在IEC 63028和SAE J2954標準框架下擁有更清晰合規記錄的解決方案仍然更受青睞。

在封閉的非鐵金屬和特殊環境中,電容耦合仍然是一種有限的選擇,因為在這些環境中,磁場的影響比單純的功率傳輸更為重要。無線電力傳輸市場還包括無電池感測和環境物聯網應用場景中的高頻和微波傳輸,在這些場景中,遠距離能源採集比充電板的對準更為重要。 Powercast憑藉其廣泛的專利組合和感測器部署記錄,證明了該領域存在利基商業需求,並且仍然是無線電力傳輸市場這一細分領域中值得關注的案例。雷射和紅外線傳輸仍然是最早實現商業化的類別之一,其重點在於遠距離或視距環境,而不是廣泛的部署應用。 IEEE ISSCC對小型諧振系統的研究也意義重大,因為它為設備製造商提供了緊湊型、嵌入式和穿戴式設計的基準。因此,儘管電感和諧振系統仍然是主要的收入來源,但無線電力傳輸市場正在經歷日益成長的技術多元化。這種多元化意義重大,因為它在同一無線電力傳輸市場中催生了不同的供應鏈、設計規則和認證流程。雖然預計到2025年電感式平台仍將是最大的市場,但在高功率環境和對精確對準要求不高的環境中,成長曲線正轉向諧振式架構。

到2025年,短距離系統將佔無線電力傳輸市場規模的55.39%,反映出基於Qi和Qi2標準的智慧型手機和穿戴式裝置充電生態系統已趨於成熟。由於數百萬用戶已在家中、職場和公共場所使用短距離充電板,因此該距離範圍仍佔據主導地位。無線電力傳輸市場在銷售量、組件尺寸和供應商學習效應方面仍然依賴現有的部署基礎。然而,預計到2031年,這種短期市場佔有率集中度將有所下降,因為面向汽車、工廠設備以及更分散的無線能源應用場景的系統正在推動市場更快成長。預計到2031年,長距離頻寬將以22.39%的複合年成長率成長,成為無線電力傳輸市場中成長最快的傳輸類別。這種成長與動態車輛充電、環境射頻能量收集以及傳統鐵氧體磁墊生態系統以外的定向能量傳輸等概念密切相關。中距離系統(通常涵蓋10公分至1公尺的範圍)在工業機器人和家具充電應用領域也越來越受歡迎,因為它們無需完整的遠端架構即可提供較高的接受度。像GuRu Wireless和Ossia這樣的公司正在推廣房間級供電的概念,這表明傳輸範圍的前景正在超越簡單的基於充電板的充電方式。

隨著傳輸距離的增加,價值鏈格局發生了顯著變化。短距離產品採用鐵氧體磁芯、線圈、屏蔽罩和接收積體電路,而長距離系統則需要不同的配置,包括天線陣列、波束控制和高價值的射頻電子元件。因此,無線電力傳輸市場正在為那些先前在行動電話充電組件領域中實力較弱的專業公司創造新的市場機會。這種差異意味著,短距離硬體的成本優勢並不能自動轉化為長距離無線電力傳輸領域的優勢。此外,買家群體也在發生變化,基礎設施規劃者、物流業者和企業物聯網整合商在評估這些系統時,所採用的投資報酬率標準與消費性電子設備製造商有所不同。隨著道路和環境電力專案現場數據的不斷積累,無線電力傳輸市場中,短距離領域的成熟企業和長距離領域的專業公司之間的界限將更加清晰。這種區分至關重要,因為它降低了單一產品架構壟斷所有應用情境的風險。無線電力傳輸產業的細分化程度日益加劇,不僅體現在終端用戶領域,也體現在傳輸距離的邏輯上。雖然短距離領域仍是核心,但長距離領域的機會正在塑造無線電力傳輸市場未來競爭格局的很大一部分。

區域分析

預計到2025年,亞太地區將佔據無線電力傳輸市場36.78%的佔有率,並在2031年之前以22.81%的複合年成長率持續成長。該地區之所以能夠推動無線電力傳輸市場的發展,得益於其高密度的智慧型手機需求、強大的電子製造業以及自動化投資的不斷增加,而這些因素都集中在同一地理區域內。中國在區域供應鏈中繼續發揮核心作用,為無線電力傳輸市場提供鐵氧體、利茲線、接收積體電路和裝置組裝的大規模生產。韓國也透過擴大商用和工業機器人的無線電力認證以及Qi v2.2.1認證活動,鞏固了其在2025年的地位,並強化了其作為消費性電子設備合規中心的地位。

北美和歐洲構成無線電力傳輸市場第二大地理叢集,並且仍然是電動車動態充電專案最活躍的地區。美國引領北美市場,這得益於智慧型手機無線充電的高普及率,以及人們對電動車隊日益成長的興趣和可見的基礎設施測試。普渡大學於2025年12月進行的一項重型卡車演示,為該地區高速公路行駛中充電樹立了強力的公共標竿。此外,美國聯邦通訊委員會(FCC)於2026年1月制定的關於基於地理圍籬的6GHz頻段可變功率設備的法規,有助於明確高功率、環保型無線設備更可行的發展路徑,這對無線電力傳輸市場的企業和工業應用案例具有重要意義。歐洲仍然是無線電力傳輸市場道路電氣化領域最先進的地區,其中法國和義大利處於領先地位。 2025年10月,Electreon在法國A10高速公路的部署,在實際交通條件下實現了尖峰300kW的動態充電。接下來,依維柯於2026年3月宣布將在義大利A35高速公路上推出「eDaily」服務,顯示車輛端整合技術距離商業化應用又更近了一步。這些進展共同表明,歐洲道路營運商和汽車製造商並未將動態無線充電視為遙遠的未來概念,而是將其視為短期基礎設施。

2026年全年,南美洲及中東及非洲的無線電力傳輸市場仍處於起步階段。巴西和阿根廷在南美洲仍展現出最清晰的機遇,但其應用仍主要集中在消費性電子設備充電領域,而非先進的電動車或工業系統。中東正逐漸成為無線電力傳輸市場的重要投資目的地,尤其是在移動出行計畫與更廣泛的脫碳和智慧城市目標相結合的地區。 2026年2月,Beam Global和HEVO分別在美國和阿拉伯聯合大公國為營運商推出了自主無線電動汽車充電平台,這表明沿岸地區在吸引先進移動出行解決方案方面比許多其他新興地區更快。非洲仍處於無線電力傳輸應用的早期階段,家用電子電器是主要的切入點,但仍面臨基礎設施短缺和進口壓力,難以在電動車和工業領域進行更廣泛的部署。儘管如此,隨著低功率消費應用的日益普及,以及隨後高價值汽車和自動化項目的湧現,預計2026年至2031年間,無線電力傳輸市場的地域覆蓋範圍將進一步擴大。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 智慧型手機和穿戴式裝置廣泛採用無線充電技術

- 加速採用無線電動汽車充電和車輛電氣化技術

- 擴大無線電力在工廠自動化和移動機器人領域的應用。

- 無線電力傳輸在密封式和植入式醫療設備的應用日益廣泛

- Qi2生態系標準化及磁性配件整合進展

- 零售和物流領域無電池物聯網網路的擴展

- 市場限制因素

- 由於線圈錯位和熱負荷導致效率降低。

- 與有線充電相比,更高的系統和基礎設施成本導致更高的整體成本。

- 不同的射頻輻射暴露和電磁相容性法規

- 鐵氧體和利茲線元件的供應集中。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過技術

- 感應耦合

- 諧振感應耦合

- 電容耦合

- 射頻和微波功率傳輸

- 雷射和紅外線功率傳輸

- 按傳輸範圍

- 短距離

- 中距離

- 長途

- 透過使用

- 智慧型手機和平板電腦

- 穿戴式電子產品

- 電動車充電

- 工業設備和機器人

- 醫療器材

- 公共基礎設施和家具

- 按組件

- 發送器

- 接收器

- 電源管理和控制積體電路

- 磁性材料和屏蔽

- 軟體和系統控制器

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- WiTricity Corporation

- Energous Corporation

- Ossia Inc.

- Powercast Corporation

- Powermat Technologies Ltd.

- Wi-Charge Ltd.

- NuCurrent, Inc.

- ConvenientPower HK Limited

- Mojo Mobility, Inc.

- GuRu Wireless, Inc.

- Electreon Wireless Ltd.

- HEVO Inc.

- Evatran, LLC

- Resonant Link Medical, LLC

- PowerLight Technologies, Inc.

- Emrod Limited

- Aeterlink Corporation

- Solace Power Inc.

- Reach Power Inc.

- Etherdyne Technologies, Inc.

- Yank Technologies, Inc.

- Aira, Inc.

- Aircharge Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the wireless power transmission market size was valued at USD 14.92 billion in 2025 and estimated to grow from USD 18.37 billion in 2026 to reach USD 49.32 billion by 2031, at a CAGR of 21.84% during the forecast period (2026-2031).

This report is Segmented by Technology (Inductive Coupling, and More), Transmission Range (Short Range, Medium Range, and Long Range), Application (Smartphones and Tablets, Wearable Electronics, and More), Component (Transmitters, Receivers, Power Management and Control ICs, Magnetic Materials and Shielding, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Wireless Power Transmission Market Trends and Insights

Expanding Wireless Charging Adoption in Smartphones and Wearables

The wireless power transmission market is gaining direct support from faster wireless charging in mainstream smartphones and wearables. Qi2 v2.2.1 raised charging capability to 25 W in July 2025, narrowing the gap with wired fast charging and removing a major purchase barrier for many buyers. The same update strengthened the case for magnetic alignment by improving performance while keeping interoperability at the center of the consumer charging tier. The Wireless Power Consortium also said 1.5 billion Qi2-capable devices entered circulation within the standard's first year, which shows how quickly the installed base expanded. The wireless power transmission market also benefits from the accessory effect, because consumers who buy magnetic chargers, wallets, stands, and battery packs are more likely to stay inside the same compatibility path when replacing handsets.

Accelerating Wireless EV Charging Deployment and Fleet Electrification

The wireless power transmission market is also being boosted by the transition from EV pilots to visible commercial deployment. Electreon activated the A10 project in France in October 2025 and demonstrated 300 kW of inductive power under live traffic conditions, providing road operators and vehicle makers with a real infrastructure reference point rather than a laboratory result. In March 2026, Electreon completed its acquisition of InductEV and brought together dynamic and stationary charging intellectual property under a single company, with roughly 400 combined patents. Purdue University also demonstrated 190 kW charging of a Class 8 truck at 65 mph in December 2025 on a public U.S. test segment, which showed that heavy-duty use cases are moving into serious validation. The wireless power transmission market gains further momentum because depot operators can reduce plug handling, labor time, and connector wear in high-cycle logistics environments even before comparing energy transfer costs.

Efficiency Losses from Coil Misalignment and Thermal Load

The wireless power transmission market still faces a practical efficiency problem when real-world alignment differs from ideal test conditions. IEEE ISSCC research published in February 2025 showed 60.2% end-to-end efficiency for an enhanced frequency-splitting architecture in miniaturized wireless power delivery, which is meaningful progress but still well below optimized wired charging performance at similar power levels. Heat concentration at the receiver side adds another layer of difficulty, especially in consumer devices above 15 W, where thermal limits can trigger power reduction. In automotive deployments, higher-power systems also need cooling and control infrastructure that offsets part of the simplicity argument usually made for wireless charging. Electreon and Infineon highlighted this high-power challenge in December 2025 when they demonstrated 300 kW inductive charging using silicon carbide devices, because thermal management remained central to achieving that power density.

Other drivers and restraints analyzed in the detailed report include:

- Growing Wireless Power Use In Factory Automation and Mobile Robotics

- Rising Qi2 Ecosystem Standardization and Magnetic Accessory Integration

- High System and Infrastructure Cost Premiums Versus Wired Charging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inductive coupling accounted for 42.61% of revenue in 2025, making it the largest technology block in the wireless power transmission market, as Qi-certified consumer hardware already had a deep global supply chain. That leadership came from compatibility, production scale, and a large installed base of chargers and receiving devices. The wireless power transmission industry still relies heavily on inductive coupling in phones, tablets, and many everyday accessories because it is well established and understood. Even so, the short transfer distance and tighter alignment requirements limit its suitability for applications where users cannot position equipment with high precision. The wireless power transmission market is now seeing resonant inductive coupling gain ground because it tolerates greater coil offset and supports higher power transfer across wider gaps. Resonant inductive coupling is projected to grow at a 22.84% CAGR through 2031, making it the fastest-growing technology path in the wireless power transmission market. Electreon's October 2025 A10 motorway deployment provided a commercial proof point for this architecture at 300 kW peak power under live traffic conditions. Product qualification also continues to favor solutions with clearer compliance history under IEC 63028 and SAE J2954 frameworks.

Capacitive coupling remains a narrower option in sealed, non-ferrous, and specialized environments where magnetic field considerations matter more than raw power throughput. The wireless power transmission market includes radio frequency and microwave transmission in battery-free sensing and ambient IoT use cases, where far-field harvesting matters more than charger-pad alignment. Powercast remains a visible reference in this part of the wireless power transmission market because its patent depth and sensor deployments show that niche commercial demand already exists. Laser and infrared transmission is still the earliest commercial category, focused on long-distance or line-of-sight settings rather than broad installed-base adoption. IEEE ISSCC work on miniaturized resonant systems also matters because it gives device makers a benchmark for compact implantable and wearable designs. As a result, the technology mix in the wireless power transmission market is widening even while inductive and resonant systems remain the main revenue engines. That spread matters because it creates separate supply chains, design rules, and qualification paths inside the same wireless power transmission market. The wireless power transmission market size for inductive platforms remained the largest in 2025, but the growth curve is shifting toward resonant architectures in higher-power and less precisely aligned environments.

Short-range systems accounted for 55.39% of the wireless power transmission market size in 2025, reflecting the maturity of smartphone and wearable charging ecosystems built around Qi and Qi2. This range remained dominant because millions of users already use short-distance charging pads at home, at work, and in public settings. The wireless power transmission market still depends on this installed base for volume, component scale, and supplier learning effects. Even so, short-term share concentration is expected to ease through 2031 as faster growth now comes from systems serving vehicles, factory equipment, and more distributed wireless energy use cases. Long-range is projected to expand at a 22.39% CAGR through 2031, making it the fastest-growing transmission category in the wireless power transmission market. That growth is tied to dynamic vehicle charging, ambient RF harvesting, and directed energy concepts that sit outside the traditional ferrite-pad ecosystem. Medium-range systems, usually spanning 10 cm to 1 m, are also finding space in industrial robotics and furniture charging because they offer greater tolerance without requiring fully long-range architectures. Companies such as GuRu Wireless and Ossia are pushing room-scale delivery concepts, which show how the transmission-range landscape is broadening beyond simple pad-based charging.

The supply chain picture changes meaningfully as transmission distance increases. Short-range products draw on ferrites, coils, shielding, and receiver ICs, while long-range systems require a different stack that includes antenna arrays, beam steering, and higher-value RF electronics. The wireless power transmission market, therefore, creates white space for specialists who were never strong in phone charging components. This difference means cost leadership in short-range hardware does not automatically translate into leadership in long-range wireless power. It also changes the buyer set, because infrastructure planners, logistics operators, and enterprise IoT integrators evaluate these systems with different return thresholds than consumer device makers. The wireless power transmission market will likely see clearer separation between short-range incumbents and long-range specialists as road and ambient power projects produce more field data. That separation matters because it reduces the risk that a single product architecture dominates every use case. The wireless power transmission industry is increasingly split by range logic, not just by end-use sector. Short range remains the anchor, but long-range opportunity is where much of the next competitive repositioning in the wireless power transmission market is taking shape.

Geography Analysis

Asia-Pacific held 36.78% of the wireless power transmission market share in 2025 and is projected to expand at a 22.81% CAGR through 2031. The region led the wireless power transmission market because it combined dense smartphone demand, deep electronics manufacturing, and rising automation investment within the same geographic base. China remained central to the regional supply chain because it supports large-scale production of ferrites, Litz wire, receiver ICs, and device assembly for the wireless power transmission market. South Korea also strengthened its position in 2025 through expanded wireless power certification for commercial and industrial robots and through Qi v2.2.1 certification activity that reinforced its role as a compliance hub for consumer devices.

North America and Europe formed the second-largest geographic cluster in the wireless power transmission market and remained the most active regions for dynamic EV charging projects. The United States was the leading North American market because it combined high smartphone wireless charging penetration with rising interest in EV fleets and visible infrastructure testing. Purdue University's December 2025 heavy-duty truck demonstration gave the region a strong public benchmark for in-motion charging at highway speeds. The FCC's January 2026 geofenced 6 GHz variable-power device rules also helped define a more workable path for higher-power ambient wireless devices, which matters for enterprise and industrial use cases in the wireless power transmission market. Europe remained the most advanced region for road electrification in the wireless power transmission market, led by France and Italy. Electreon's A10 motorway deployment in France validated 300 kW peak dynamic charging under real traffic conditions in October 2025. Iveco's March 2026 announcement of the eDaily on Italy's A35 motorway then showed that vehicle-side integration was moving closer to commercial use. Together, these developments showed that European road operators and OEMs are treating dynamic wireless charging as near-term infrastructure rather than a distant concept.

South America, the Middle East, and Africa remained early-stage markets for wireless power transmission through 2026. Brazil and Argentina continued to present the clearest South American opportunities, though adoption still leaned toward consumer device charging rather than advanced EV or industrial systems. The Middle East is emerging as a selective investment destination in the wireless power transmission market, especially where mobility programs are linked to wider decarbonization and smart-city targets. Beam Global and HEVO launched an autonomous, wireless EV charging platform in February 2026 for operators in the United States and the UAE, demonstrating that the Gulf is attracting advanced mobility solutions earlier than many other emerging regions. Africa remained at an early adoption stage, with consumer electronics as the main entry point, while broader EV and industrial deployment still face infrastructure gaps and import pressures. Even so, the wireless power transmission market is likely to expand its geographic reach over 2026-2031 as lower-power consumer applications gain familiarity before higher-value automotive and automation projects follow.

- WiTricity Corporation

- Energous Corporation

- Ossia Inc.

- Powercast Corporation

- Powermat Technologies Ltd.

- Wi-Charge Ltd.

- NuCurrent, Inc.

- ConvenientPower HK Limited

- Mojo Mobility, Inc.

- GuRu Wireless, Inc.

- Electreon Wireless Ltd.

- HEVO Inc.

- Evatran, LLC

- Resonant Link Medical, LLC

- PowerLight Technologies, Inc.

- Emrod Limited

- Aeterlink Corporation

- Solace Power Inc.

- Reach Power Inc.

- Etherdyne Technologies, Inc.

- Yank Technologies, Inc.

- Aira, Inc.

- Aircharge Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Wireless Charging Adoption in Smartphones and Wearables

- 4.2.2 Accelerating Wireless EV Charging Deployment and Fleet Electrification

- 4.2.3 Growing Wireless Power Use in Factory Automation and Mobile Robotics

- 4.2.4 Increasing Adoption of Wireless Power in Sealed and Implantable Medical Devices

- 4.2.5 Rising Qi2 Ecosystem Standardization and Magnetic Accessory Integration

- 4.2.6 Scaling Battery-Free Retail and Logistics IoT Networks

- 4.3 Market Restraints

- 4.3.1 Efficiency Losses From Coil Misalignment and Thermal Load

- 4.3.2 High System and Infrastructure Cost Premiums Versus Wired Charging

- 4.3.3 Fragmented RF Exposure and EMC Compliance Regimes

- 4.3.4 Concentrated Supply of Ferrites and Litz Wire Components

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Inductive Coupling

- 5.1.2 Resonant Inductive Coupling

- 5.1.3 Capacitive Coupling

- 5.1.4 Radio Frequency and Microwave Power Transmission

- 5.1.5 Laser and Infrared Power Transmission

- 5.2 By Transmission Range

- 5.2.1 Short Range

- 5.2.2 Medium Range

- 5.2.3 Long Range

- 5.3 By Application

- 5.3.1 Smartphones and Tablets

- 5.3.2 Wearable Electronics

- 5.3.3 Electric Vehicle Charging

- 5.3.4 Industrial Equipment and Robotics

- 5.3.5 Medical Devices

- 5.3.6 Public Infrastructure and Furniture

- 5.4 By Component

- 5.4.1 Transmitters

- 5.4.2 Receivers

- 5.4.3 Power Management and Control ICs

- 5.4.4 Magnetic Materials and Shielding

- 5.4.5 Software and System Controllers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 WiTricity Corporation

- 6.4.2 Energous Corporation

- 6.4.3 Ossia Inc.

- 6.4.4 Powercast Corporation

- 6.4.5 Powermat Technologies Ltd.

- 6.4.6 Wi-Charge Ltd.

- 6.4.7 NuCurrent, Inc.

- 6.4.8 ConvenientPower HK Limited

- 6.4.9 Mojo Mobility, Inc.

- 6.4.10 GuRu Wireless, Inc.

- 6.4.11 Electreon Wireless Ltd.

- 6.4.12 HEVO Inc.

- 6.4.13 Evatran, LLC

- 6.4.14 Resonant Link Medical, LLC

- 6.4.15 PowerLight Technologies, Inc.

- 6.4.16 Emrod Limited

- 6.4.17 Aeterlink Corporation

- 6.4.18 Solace Power Inc.

- 6.4.19 Reach Power Inc.

- 6.4.20 Etherdyne Technologies, Inc.

- 6.4.21 Yank Technologies, Inc.

- 6.4.22 Aira, Inc.

- 6.4.23 Aircharge Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

無線電力傳輸市場:依技術、組件、頻率和應用分類-2026-2032年全球市場預測

無線電力傳輸市場:依技術、組件、頻率和應用分類-2026-2032年全球市場預測 無線電力傳輸市場報告:按類型、技術、部署模式、接收器應用、終端用戶產業和地區分類(2026-2034 年)

無線電力傳輸市場報告:按類型、技術、部署模式、接收器應用、終端用戶產業和地區分類(2026-2034 年) 無線電力傳輸市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

無線電力傳輸市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 無線電力傳輸市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、最終用戶、設備、安裝類型及解決方案分類

無線電力傳輸市場分析及預測(至2035年):依類型、產品類型、技術、組件、應用、最終用戶、設備、安裝類型及解決方案分類 無線電力傳輸市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、類型、地區和競爭格局分類,2021-2031年日本無線電力傳輸市場規模、佔有率、趨勢及預測(按類型、技術、部署方式、接收器應用、最終用戶產業及地區分類),2026-2034年

無線電力傳輸市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、應用、類型、地區和競爭格局分類,2021-2031年日本無線電力傳輸市場規模、佔有率、趨勢及預測(按類型、技術、部署方式、接收器應用、最終用戶產業及地區分類),2026-2034年 無線電力傳輸市場規模、佔有率和成長分析(按技術、最終用戶、部署類型和地區分類)—產業預測(2026-2033 年)

無線電力傳輸市場規模、佔有率和成長分析(按技術、最終用戶、部署類型和地區分類)—產業預測(2026-2033 年) 無線供電市場:按技術、應用和地區分類無線電力傳輸系統市場(按技術、應用和地區)

無線供電市場:按技術、應用和地區分類無線電力傳輸系統市場(按技術、應用和地區) 全球無線傳輸市場

全球無線傳輸市場