|

市場調查報告書

商品編碼

2065547

ERP系統安全與合規:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)ERP Security And Compliance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

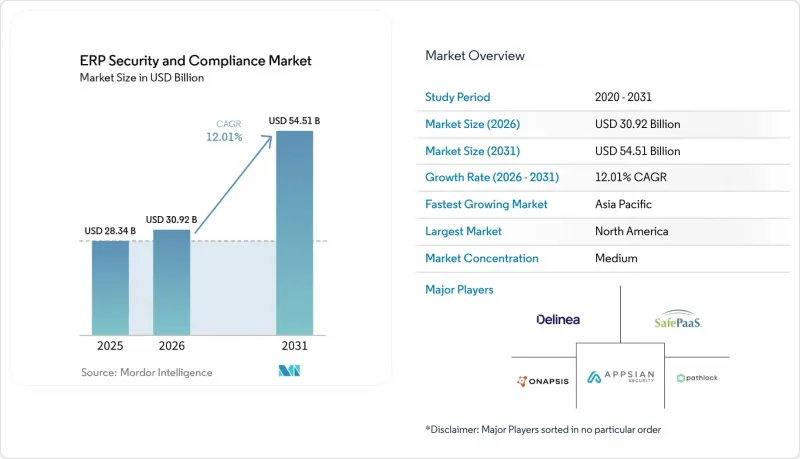

根據 Mordor Intelligence 預測,ERP 安全和合規市場規模預計將從 2025 年的 283.4 億美元和 2026 年的 309.2 億美元成長到 2031 年的 545.1 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 12.01%。

本報告按組件(軟體、服務)、部署方式(本地部署、雲端部署、混合部署)、組織規模(大型企業、中小企業)、最終用戶行業(製造業、銀行、金融服務和保險業、醫療保健業、零售/電子商務業、政府/公共部門、IT/電信業及其他行業)和地區進行細分。市場預測以美元計價。

全球ERP安全與合規市場趨勢與洞察。

雲端ERP採用率的擴大

到2025年,四分之三的公司將至少運行一個雲端ERP實例,但責任分類模式模糊了供應商和客戶在存取管治方面的責任界線。多租戶架構暴露了應用程式介面(API),攻擊者可以利用這些介面,到2025年,語音釣魚攻擊將佔雲端資料外洩事件的23%。美國證券交易委員會(SEC)現在要求上市公司在四個工作天內揭露重大網路安全事件,迫使董事會審查ERP角色設計和職責分離(SoD)的合理性。持續監控能夠擷取使用者行為遙測資料並即時偵測權限提升,逐漸成為董事會層面的要求。能夠自動將角色對應到業務流程風險情境的供應商正成為優先考慮的對象,因為它們可以將稽核準備時間從數週縮短到數小時。

各行各業的監理合規要求都在不斷提高。

PCI DSS v4.0 將於 2025 年 3 月強制實施,新增 64 項要求以加強認證,並強制要求對與 ERP 系統整合的持卡人環境進行季度滲透測試。歐洲企業永續性報告指令 (CSRD) 已擴大監管範圍,涵蓋非財務數據,要求財務部門將 ESG 指標與總分類帳進行核對。銀行正面臨巴塞爾協議 III 營運彈性認證,將關鍵業務服務映射到 ERP 模組,從而持續推動對自動化證據產生的需求。北美審計師越來越拒絕人工進行職責分離 (SoD) 認證,並轉向持續的數位化支援。這些多方面的監管要求,加上企業努力統一財務和永續發展揭露中的控制措施,共同推動了 ERP 安全合規市場的持續需求。

人工智慧驅動的行為分析的整合

以人工智慧為基礎的異常偵測引擎目前每小時可分析數百萬筆ERP交易,透過關聯異常的日記帳分錄時間、位置異常以及與競爭對手的偏差,產生即時風險評分。北美和歐洲的早期採用者報告稱,與基於規則的系統相比,誤報率降低了60%,使分析師能夠專注於更精準的威脅調查。 Onapsis的「代理閘道器」利用大規模語言模型實現了摘要功能,將取證訊號轉化為簡單易懂的事件報告。這使得財務和負責人無需依賴網路安全術語即可檢驗警報。人工智慧的可解釋性也正成為監管重點,歐洲監管機構正在考慮制定指導方針,要求對機器生成的存取決策提供清晰的審計追蹤。預計這將進一步刺激對透明行為分析引擎的投資。

細分市場分析

儘管軟體在2025年仍主導ERP安全和合規市場,但這一格局正在改變。企業已經部署了核心的職責分離(SoD)引擎和持續控制儀錶板,現在他們正在尋求維運方面的專業知識。反映出這項轉變,業務收益(諮詢、實施和託管檢測)正以16.80%的複合年成長率成長。諮詢服務擴大將業務流程重組納入其中,以確保SoD的實施符合ISO 27001:2022基於風險的原則,而託管服務訂閱則包含全天候警報分類和季度存取認證。

同時,軟體供應商正競相透過低程式碼 API編配來降低整體擁有成本 (TCO)。 Pathlock 於 2025 年 8 月與 Microsoft Sentinel 的整合,展示瞭如何將 ERP 驅動的異常情況直接整合到現有的保全行動工作流程中,從而無需單獨的 SIEM 儀表板。在整個預測期內,平台供應商將透過整合 AI 輔助配置功能來進一步彌合技能差距,這些功能可以引導客戶完成上下文感知的角色定義,同時保持 ERP 安全和合規市場軟體更新的勢頭。

預計到2025年,雲端部署將佔總營收的58.50%,隨著財務管理、供應鏈和人力資本管理套件遷移到Oracle Fusion Cloud、SAP S/4HANA Cloud和Microsoft Dynamics 365,雲端部署將繼續超越其他選擇。隨著基於SaaS的ERP成為新部署的預設選擇,與雲端實例相關的ERP安全合規市場規模預計將以18.30%的複合年成長率成長至2031年。 FedRAMP的「中等」基準包含325個控制項,其標準遠超美國聯邦政府機構,如今私人企業也要求達到類似的合規水準。持續的API日誌擷取、無伺服器代理程式和記憶體內分析技術可在幾分鐘內實現異常檢測,將平均偵測時間(MTD)從幾天縮短到幾分鐘。

在國防和關鍵基礎設施領域,由於資料主權規則和空氣間隙網路的要求,本地部署環境仍然十分普遍。隨著供應商將研發重點轉向雲端原生功能集,維護成本也隨之飆漲。將本地財務模組與雲端人力資源系統結合的混合部署方式引入了身分識別管理的複雜性,迫使安全團隊至少管理兩個目錄的提案權限。如今,能夠整合不同模式下風險態勢的整合儀錶板已成為招標書評估的必備條件。

區域分析

在符合薩班斯-奧克斯利法案的審計、強大的網路安全供應商陣容以及財富500強企業積極採用雲ERP的支持下,北美仍將保持最大的區域市場佔有率,預計到2025年將達到34.10%。人工智慧(AI)驅動的異常檢測引擎率先在該地區獲得應用,並催生了許多開創性的實施案例,這些案例隨後被全球各地的子公司效仿。中型企業的併購正在推動新ERP系統的採用和整合,所有這些都需要重新評估角色(職責分離)。

亞太地區複合年成長率最高,達到17.20%,這主要得益於日本憑證人員編制案件的激增、印度《資料保護法》的實施以及新加坡修訂後的《個人資料保護法》(對延遲通知違規行為處以100萬新元(約合75萬美元)的罰款)。中國的資料在地化法規迫使跨國公司在國內部署ERP系統,本地雲端服務供應商(CSP)與國際安全廠商合作,以滿足雙重合規要求。由於技能嚴重短缺,託管服務供應商正在填補這一空白,加速SaaS安全解決方案的普及。

在歐洲,隨著GDPR罰款額度的增加,市場穩定成長,預計到2025年將超過21億歐元(23億美元)。 NIS2指令擴大了關鍵基礎設施的定義,將數位服務供應商納入其中,並將運輸和物流納入合規範圍。南美洲的趨勢反映了巴西《通用資料保護法》(Lei Geral de Protecao de Dados)和阿根廷基於同意的資料保護法的影響。儘管中東和非洲地區的支出落後於其他地區,但隨著主權雲計劃和基於NIST模型的框架要求將ERP層控制與國家網路防禦戰略相整合,該地區正經歷兩位數的成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 雲端ERP採用率的擴大

- 各行各業的監理合規要求都在不斷提高。

- ERP環境中的內部威脅和資料外洩事件日益增多

- 在多ERP環境中,對集中式SoD管理的需求日益成長

- 將人工智慧驅動的行為分析整合到即時風險評分中

- 對與ESG保證相關的持續控制監控的需求

- 市場限制因素

- 較高的初始整合和實施成本

- 缺乏熟練的ERP安全專業人員

- IGA 和 PAM 工具集的重疊導致採購決策停滯不前。

- 供應商整合限制了針對特定合規要求的最佳選擇。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章:預測市場規模與成長率

- 按組件

- 軟體

- 服務

- 透過部署方法

- 現場

- 雲

- 混合

- 按組織規模

- 大公司

- 小型企業

- 按最終用途行業分類

- 製造業

- 銀行、金融服務和保險業 (BFSI)

- 醫療保健

- 零售與電子商務

- 政府/公共部門

- IT/通訊

- 其他終端用戶產業

- 按地區

- 北美洲

- 南美洲

- 歐洲

- 亞太地區

- 中東

- 非洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Pathlock Inc.

- Appsian Security Inc.

- SafePaaS Inc.

- Onapsis Inc.

- Delinea Inc.

- Fastpath Solutions LLC

- Soterion Ltd.

- MTC Skopos AG

- Access Informer Pty Ltd

- Dynaflow Compliance Solutions Inc.

- ERP Armor LLC

- Saviynt Inc.

- Security Weaver LLC

- CSI Tools NV

- SmartERP Solutions Inc.

- ERP Maestro Inc.

- SailPoint Technologies Holdings Inc.

- Netwrix Corporation

- Kainos Group plc

- IBS Schreiber GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the eRP security and compliance market size is projected to expand from USD 28.34 billion in 2025 and USD 30.92 billion in 2026 to USD 54.51 billion by 2031, registering a CAGR of 12.01% between 2026 and 2031.

This report is Segmented by Component (Software and Services), Deployment Mode (On-Premise, Cloud, and Hybrid), Organization Size (Large Enterprises and SMEs), End-Use Industry (Manufacturing, Banking, Financial Services and Insurance, Healthcare, Retail and E-Commerce, Government and Public Sector, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global ERP Security And Compliance Market Trends and Insights

Proliferation of Cloud-Based ERP Deployments

Three out of four enterprises ran at least one cloud ERP instance in 2025, but the shared-responsibility model blurs accountability between vendor and customer for access governance. Multi-tenant architectures expose application programming interfaces that adversaries weaponize, while voice-phishing accounted for 23% of cloud compromises in 2025. The U.S. Securities and Exchange Commission now compels public companies to disclose material cyber incidents within four business days, forcing boards to scrutinize ERP role design and SoD hygiene. Continuous monitoring that ingests user-behavior telemetry and flags privilege escalations in real time is emerging as a board-level requirement. Vendors that automate the mapping of roles to business-process risk scenarios gain purchase precedence because they cut audit preparation from weeks to hours.

Escalating Regulatory Compliance Requirements Across Industries

PCI DSS v4.0 became compulsory in March 2025, adding 64 new requirements that strengthen authentication and require quarterly penetration testing in ERP-linked cardholder environments. Europe's Corporate Sustainability Reporting Directive extends oversight to non-financial data, obliging finance teams to reconcile ESG metrics with general ledger entries. Banks' face Basel III operational resilience proofs that map critical business services to ERP modules, creating steady demand for automated evidence generation. Auditors in North America are increasingly rejecting manual SoD attestations and moving toward continuous digital substantiation. Together, the multifaceted mandates ensure sustained purchasing momentum for the ERP security and compliance market as firms seek to unify controls across financial and sustainability disclosures.

Integration of AI-Driven Behavioral Analytics

AI-based anomaly engines now parse millions of ERP transactions per hour, correlating unusual posting times, location anomalies, and peer-group deviations to generate real-time risk scores. Early adopters in North America and Europe cite a 60% reduction in false-positive alerts relative to rule-centric systems, freeing analysts to investigate high-fidelity threats. Onapsis's Agentic Gateway showcases large-language-model summarization that turns forensic signals into plain-English incident narratives, enabling finance and audit staff to validate alerts without cybersecurity jargon. AI explainability is also moving up the regulatory agenda, with European watchdogs exploring guidance that requires clear audit trails for machine-generated access decisions, further boosting investment in transparent behavioral engines.

Other drivers and restraints analyzed in the detailed report include:

- Rising Incidence of Insider Threats and Data Breaches

- Growing Need for Centralized SoD Management

- Demand for Continuous Controls Monitoring Linked to ESG Assurance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software dominated the ERP security and compliance market in 2025, yet the narrative is shifting. Enterprises have already purchased core SoD engines and continuous controls dashboards; now they crave the expertise to operationalize them. Services revenue, consulting, implementation, and managed detection, grows at 16.80% CAGR, reflecting this pivot. Advisory engagements increasingly incorporate business-process reengineering to ensure SoD enforcement aligns with ISO 27001:2022 risk-based principles, while managed-service subscriptions bundle 24/7 alert triage and quarterly access attestations.

Software vendors, meanwhile, race to lower the total cost of ownership through low-code API orchestration. Pathlock's August 2025 link-up with Microsoft Sentinel demonstrates how ERP-centric anomalies can feed directly into existing security operations workflows, eliminating the need for separate SIEM dashboards. Over the forecast horizon, platform vendors will embed AI-assisted configuration that guides customers through context-aware role definitions, further closing the skills gap and sustaining software renewal momentum inside the ERP security and compliance market.

Cloud deployments accounted for 58.50% of 2025 revenue and continue to outpace alternatives as financial-management, supply-chain, and human-capital-management suites migrate to Oracle Fusion Cloud, SAP S/4HANA Cloud, and Microsoft Dynamics 365. The ERP security and compliance market size tied to cloud instances is forecast to increase at an 18.30% CAGR through 2031 as SaaS ERP becomes the default choice for greenfield installations. FedRAMP's 325-control moderate baseline serves as a benchmark well beyond U.S. federal agencies, prompting private enterprises to insist on equivalent coverage. Continuous API log ingestion, serverless agents, and in-memory analytics deliver minute-level anomaly detection, collapsing mean-time-to-detect from days to minutes.

On-premises estates persist in the defense and critical infrastructure sectors, where data sovereignty rules and air-gapped networks require local hosting. Maintenance costs escalate as vendors funnel research and development toward cloud-native feature sets. Hybrid deployments, which splice on-premise financial modules with cloud-based talent systems, introduce cross-identity complexities that force security teams to manage entitlements across at least two directories. Unified dashboards that consolidate risk postures across modes are now table stakes in request-for-proposal scoring.

Geography Analysis

North America remains the largest regional slice at 34.10% in 2025, anchored by Sarbanes-Oxley audits, deep cybersecurity vendor benches, and aggressive cloud ERP adoption among Fortune 500 companies. Artificial-intelligence anomaly engines gain traction first in this region, producing lighthouse implementations that global subsidiaries later replicate. Mergers and acquisitions among mid-cap players spark new ERP instances and consolidation efforts, both of which require fresh SoD review.

Asia-Pacific posts the fastest 17.20% CAGR, driven by Japan's spike in credential-stuffing incidents, India's data-protection statute, and Singapore's amended Personal Data Protection Act that levies fines of SGD 1 million (USD 750,000) for delayed breach notifications. Chinese data-localization rules compel multinationals to deploy in-country ERP stacks, in which local CSPs partner with international security vendors to satisfy dual compliance requirements. Skill shortages are acute, so managed service providers fill gaps, accelerating SaaS security adoption.

Europe grows steadily as GDPR fines escalate, crossing EUR 2.1 billion (USD 2.3 billion) in 2025. The NIS2 directive widens the definition of critical infrastructure to include digital service providers, adding transportation and logistics to the compliance roster. South America's trajectory reflects the influence of Brazil's Lei Geral de Protecao de Dados and Argentina's consent-centric data-protection law. The Middle East and Africa trail in spend but experience double-digit growth as sovereign-cloud initiatives and National Institute of Standards and Technology model-led frameworks require ERP-layer controls merged with national cyber-defense strategies.

- Pathlock Inc.

- Appsian Security Inc.

- SafePaaS Inc.

- Onapsis Inc.

- Delinea Inc.

- Fastpath Solutions LLC

- Soterion Ltd.

- MTC Skopos AG

- Access Informer Pty Ltd

- Dynaflow Compliance Solutions Inc.

- ERP Armor LLC

- Saviynt Inc.

- Security Weaver LLC

- CSI Tools NV

- SmartERP Solutions Inc.

- ERP Maestro Inc.

- SailPoint Technologies Holdings Inc.

- Netwrix Corporation

- Kainos Group plc

- IBS Schreiber GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Cloud-based ERP Deployments

- 4.2.2 Escalating Regulatory Compliance Requirements Across Industries

- 4.2.3 Rising Incidence of Insider Threats and Data Breaches in ERP Environments

- 4.2.4 Growing Need for Centralized SoD Management in Multi-ERP Landscapes

- 4.2.5 Integration of AI-Driven Behavioral Analytics for Real-Time Risk Scoring

- 4.2.6 Demand for Continuous Controls Monitoring Tied to ESG Assurance

- 4.3 Market Restraints

- 4.3.1 High Initial Integration and Implementation Costs

- 4.3.2 Shortage of Skilled ERP Security Professionals

- 4.3.3 Overlapping IGA and PAM Toolsets Creating Purchase Decision Paralysis

- 4.3.4 Vendor Consolidation Limiting Best-of-Breed Options for Niche Compliance Needs

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-use Industry

- 5.4.1 Manufacturing

- 5.4.2 Banking, Financial Services and Insurance

- 5.4.3 Healthcare

- 5.4.4 Retail and E-commerce

- 5.4.5 Government and Public Sector

- 5.4.6 IT and Telecom

- 5.4.7 Other End-use Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.2 South America

- 5.5.3 Europe

- 5.5.4 Asia-Pacific

- 5.5.5 Middle East

- 5.5.6 Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Pathlock Inc.

- 6.4.2 Appsian Security Inc.

- 6.4.3 SafePaaS Inc.

- 6.4.4 Onapsis Inc.

- 6.4.5 Delinea Inc.

- 6.4.6 Fastpath Solutions LLC

- 6.4.7 Soterion Ltd.

- 6.4.8 MTC Skopos AG

- 6.4.9 Access Informer Pty Ltd

- 6.4.10 Dynaflow Compliance Solutions Inc.

- 6.4.11 ERP Armor LLC

- 6.4.12 Saviynt Inc.

- 6.4.13 Security Weaver LLC

- 6.4.14 CSI Tools NV

- 6.4.15 SmartERP Solutions Inc.

- 6.4.16 ERP Maestro Inc.

- 6.4.17 SailPoint Technologies Holdings Inc.

- 6.4.18 Netwrix Corporation

- 6.4.19 Kainos Group plc

- 6.4.20 IBS Schreiber GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment