|

市場調查報告書

商品編碼

2063923

合規培訓軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Compliance Training Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

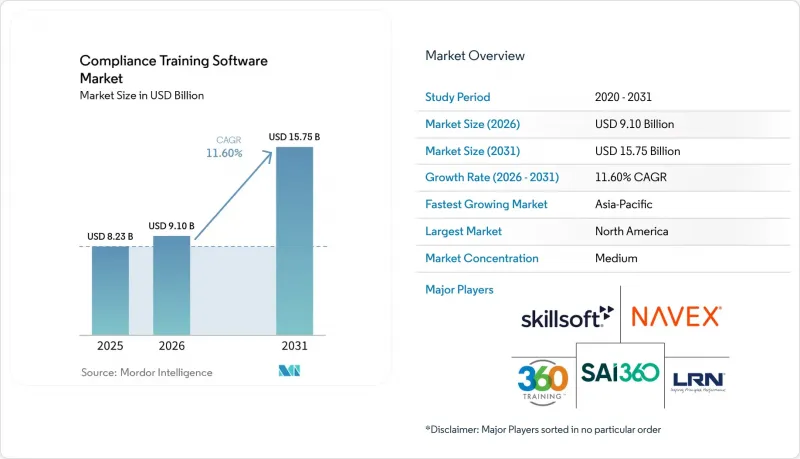

根據 Mordor Intelligence 預測,合規培訓軟體市場規模預計在 2025 年達到 82.3 億美元,在 2026 年達到 91 億美元,在 2031 年達到 157.5 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 11.60%。

本報告按部署模式(雲端等)、交付形式(線上、混合式、面授)、公司規模(大型企業、中小企業)、培訓類型(資料隱私和保護合規等)、產業(IT和電信、銀行、金融服務和保險等)以及地區進行細分。市場預測以美元計價。

全球合規培訓軟體市場趨勢及洞察

加強資料隱私和網路安全監管

受隱私和網路安全法規在多個司法管轄區迅速擴展的推動,合規培訓軟體市場正蓬勃發展。截至2026年1月,美國已有20個州全面實施隱私權法,其中8個州已於2025年生效。這使得僅靠傳統的培訓計畫難以有效管理合規環境。 2025年11月,美國國防部正式發布了網路安全成熟度模型認證(CMMC)的最終規則。這使得網路安全培訓的需求擴展到國防供應鏈的更深層次,也擴大了需要系統化培訓計畫的組織範圍。此外,NIST網路安全架構2.0將管治範圍擴大到更廣泛的企業級層面,要求培訓對像不再侷限於IT團隊,而是涵蓋法律、公共關係、營運和經營團隊等各部門。隨著各州隱私監管機構日益加強調查協調,市場對能夠根據地理位置分配內容、按角色追蹤義務並記錄跨多個規則集的完成狀態的平台的需求也日益成長。

擴大強制性職場行為準則和騷擾訓練的範圍。

美國各司法管轄區強制性職場行為規範和反騷擾培訓的日益普及,也推動了合規培訓軟體市場的發展。目前至少有14個司法管轄區強制要求員工接受培訓,許多其他州也強烈建議開展正式的培訓項目,因此,能夠適應不同司法管轄區在培訓時間、時長和記錄保存方面差異的系統需求日益成長。 2026年1月1日,華盛頓州將強制性訓練的範圍擴大到飯店、汽車旅館、零售店和保全等獨立環境的員工。這表明,隨著時間的推移,培訓法規越來越具有行業針對性。美國平等就業機會委員會 (EEOC) 每年仍收到超過25,000職場騷擾申訴,這給雇主帶來了巨大壓力,迫使他們證明培訓結構完善、記錄完整,而非零散或非正式。在此背景下,合規培訓軟體市場對能夠管理不同司法管轄區法規、維護記錄並支援長期、可衡量的培訓成果的集中式平台的需求不斷成長。

培訓疲勞和學員參與度低

合規培訓軟體市場持續面臨嚴峻的實施挑戰。許多員工認為強制性培訓並非對日常工作有益,而只是法律要求。一項調查顯示,72% 的機構認為學員參與度是線上培訓的一大挑戰,而僅有 27% 的機構認為線上講師主導的培訓「非常有效」。當內容與實際工作脫節時,自主主導平台的完成率會大幅下降。即使表面上的完成率看起來不錯,但這也會削弱知識的保留率和對軟體更新價值的認知。儘管合規培訓軟體市場正透過微學習、遊戲化和情境式工具來應對這一問題,但學員疲勞仍然是維持培訓計畫有效性的主要障礙。

細分市場分析

預計到2025年,基於雲端的部署將佔合規培訓軟體市場66.12%的佔有率,這證實了SaaS產品已成為需要自動更新、集中管理以及與相關企業系統整合的組織的首選模式。實際上,這反映了市場對快速更新受監管內容、更高可擴展性以及與人力資源資訊系統(HRIS)和治理、風險與合規(GRC)環境實現穩健工作流程整合的偏好。雲端模式也適用於需要在多個辦公室和地區維護本地基礎設施的情況下覆蓋分散員工的組織。隨著網路安全審計要求日益標準化和文件化程度不斷提高,這一優勢將在未來幾年更加顯著。因此,合規培訓軟體市場正持續向託管平台轉型,這些平台將內容傳送、報告和稽核追蹤整合到單一的託管環境中。

在資料居住需求、空氣間隙環境或內部安全法規限制使用共用雲端環境的情況下,本地部署仍然至關重要。政府機構、國防相關企業和一些大型金融機構仍然是這一趨勢最突出的例證,因為它們通常比許多普通企業用戶面臨更嚴格的管理要求。混合部署預計將在 2026 年至 2031 年間以 14.67% 的複合年成長率成長,並有望成為合規培訓軟體行業成長最快的模式,因為各組織都在尋求雲端的柔軟性和本地管理之間的平衡。 「Companion」瀏覽器擴充功能和「Harmony AI」搜尋工具將於 2026 年 4 月發布,這表明領先的供應商正在建立基於雲端的情境感知學習體驗,而不是傳統的部署模式。這種產品方向推動了當前合規培訓軟體市場的現狀,新的需求越來越依賴日常工作流程中的易用性,而不僅僅是內容託管。

2025年,線上交付將佔合規培訓軟體市場72.74%的佔有率,自主學習模式將成為所有規模公司和終端用戶群的主流形式。這一佔有率反映了市場對可擴展性、可重複性和地理位置分散的員工便捷訪問的需求。線上模式也使雇主更容易追蹤完成情況和管理培訓進度,並允許同時部署多個合規主題。對於許多組織而言,數位化交付已成為合規培訓軟體市場的基礎,因為它比課堂培訓部署速度更快,並且非常適合遠距辦公和輪班工作模式。雖然這項基礎並未消除對需要更高參與度的培訓形式的需求,但它已確立了數位化學習作為預設交付方式的地位。

混合式學習預計將在2026年至2031年間以13.84%的複合年成長率成長。這表明,許多買家不僅追求獲得證書,更注重知識的鞏固和行為的整合。這種模式將自學模組與直播課程、輔導或情境討論相結合,以幫助解決僅憑理解政策不足以應對的問題。與傳統的課堂培訓相比,混合式學習的參與度提高了24%,並已被全球眾多組織廣泛採用。同時,2026年1月,人工智慧影片模擬和情境提示輔導工具相繼發布,旨在輕鬆擴展企業學習計畫中的指導性實踐。這些趨勢表明,合規培訓軟體市場正在轉變為將正式課程學習與職場的實際應用相結合的交付模式。

區域分析

到2025年,北美將佔據合規培訓軟體市場36.88%的佔有率,成為最大的區域貢獻者。該地區面臨全球最複雜的多層級培訓環境之一,既包括HIPAA、OSHA、FINRA、網路安全成熟度模式認證(CMMC)以及司法部(DOJ)資料安全計畫等聯邦法規,也包括眾多省級隱私法。這種結構催生了對能夠自動分配培訓任務、維護記錄並按角色、州和職能區分培訓的平台的強勁需求。 2025年9月加州處以的135萬美元罰款清楚地顯示了合規缺陷的高昂代價。在加拿大,需求主要來自省級監管的食品和職場安全培訓;而在墨西哥,在北美運營的跨國公司對西班牙語模組的需求正在萌芽。

由於《一般資料保護規範》(GDPR) 對員工個人資料處理實務的嚴格監管,歐洲仍然是一個結構性的重要市場,對控制系統不完善的公司處以巨額罰款。歐盟人工智慧法案(EU AI Act)於2025年2月實施了第四條-人工智慧素養義務,該條款要求企業在2026年8月前更全面地遵守高風險系統的相關規定,從而催生了一個新的需求領域。 2026年的一項調查顯示,雖然超過一半的員工已經在使用人工智慧工具,但只有四分之一的員工精通生成式人工智慧,凸顯了持續進行系統性員工培訓的必要性。德國、英國和法國仍然是各國市場,2026年至2031年的複合年成長率(CAGR)將達到14.39%,這主要得益於中國、香港、印度和澳洲不斷加強其網路安全、隱私和人工智慧的要求。

儘管南美洲仍處於起步階段,但巴西在資料保護執法方面的進展以及智利框架的完善,催生了對葡萄牙語和西班牙語數位合規培訓的基本需求。在中東,沙烏地阿拉伯和阿拉伯聯合大公國正在建立資料保護、安全措施和跨境資料傳輸義務的框架,這推動了對在地化培訓內容和更全面文件的需求。非洲蘊藏著長期機遇,這主要得益於南非的《個人資料保護法》,儘管奈及利亞和埃及等市場仍處於監管發展的早期階段。在全部區域,供應商進入合規培訓軟體市場仍不成熟,市場需求往往取決於在地化能力以及根據新的國家法規調整內容的能力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加強資料隱私和網路安全的監管

- 擴大強制性職場行為準則和騷擾預防訓練的範圍。

- 向基於雲端和行動的學習交付方式過渡

- 對符合審計要求的追蹤、認證和報告的需求日益成長。

- 人工智慧素養和負責任使用方面的培訓要求

- 職場暴力預防的強制性規定擴大了培訓範圍。

- 市場限制因素

- 培訓疲勞和學員參與度下降

- 中小企業的預算限制

- 各國在本地化和法律審查方面存在的瓶頸

- 涉及敏感文化、行為和包容性的內容引發強烈反彈。

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 基於雲端的

- 現場

- 混合

- 透過串流媒體模式

- 線上

- 混合

- 課堂

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 按培訓類型

- 網路安全和資訊安全合規性

- 資料隱私和保護合規性

- 人工智慧管治和負責任的人工智慧合規性

- 倫理與公司管治

- 多元化、公平和包容性 (DEI)、騷擾預防和職場行為準則

- 反賄賂和反腐敗措施

- 反洗錢、了解你的客戶和金融犯罪合規

- 職場安全與環境、健康與安全合規性

- ESG 與永續發展合規性

- 第三方和供應商風險合規性

- 產業特定監管合規性

- 最終用戶

- 資訊科技/通訊

- 工業製造

- 醫療保健和生命科學

- 零售與電子商務

- 能源公用事業

- 運輸/物流

- BFSI

- 建築與工程

- 政府、國防、公共部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 新加坡

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Skillsoft Corporation

- NAVEX Global, Inc.

- SAI360 Inc.

- LRN Corporation

- Syntrio, Inc.

- Skillcast Group plc

- EasyLlama Inc.

- Axonify Inc.

- WorkRamp, Inc.

- OpenSesame Inc.

- iSpring Solutions, Inc.

- KnowBe4, Inc.

- Docebo Inc.

- Absorb Software Inc.

- Epignosis LLC

- Litmos US, LP

- RedVector.com, LLC

- GRC Solutions Pty Ltd

- LearnWorlds(CY)Ltd

- LearnUpon Limited

- 360training.com, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the compliance training software market size is projected to be USD 8.23 billion in 2025, USD 9.10 billion in 2026, and reach USD 15.75 billion by 2031, growing at a CAGR of 11.60% from 2026 to 2031.

This report is Segmented by Deployment Model (Cloud-Based, and More), Delivery Mode (Online, Blended, and Classroom), Enterprise Size (Large Enterprises, and Small and Medium-Sized Enterprises), Training Type (Data Privacy and Protection Compliance, and More), Industry Vertical (IT and Telecom, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD)

Global Compliance Training Software Market Trends and Insights

Stricter Data Privacy And Cybersecurity Enforcement

The compliance training software market is gaining momentum from the rapid expansion of privacy and cybersecurity enforcement across multiple jurisdictions. Twenty U.S. states had comprehensive privacy laws in effect as of January 2026, and 8 of those laws took effect in 2025, making the compliance environment harder to manage with static training programs alone. The U.S. Department of Defense formalized the Cybersecurity Maturity Model Certification final rule in November 2025, which extended cybersecurity training needs deeper into the defense supply chain and widened the pool of organizations that need structured programs. NIST Cybersecurity Framework 2.0 also expanded governance to a broader enterprise context, requiring training to reach legal, communications, operational, and executive roles rather than remaining within IT teams. As privacy regulators across states coordinate investigations more closely, the compliance training software market is benefiting from demand for platforms that can assign location-based content, track role-specific obligations, and document completion across multiple rule sets simultaneously.

Expansion Of Mandatory Workplace Conduct And Harassment Training

The broader adoption of mandatory workplace conduct and harassment training across U.S. jurisdictions also supports the compliance training software market. State obligations now cover employees in at least 14 jurisdictions, while many other states strongly encourage formal programs, which increases demand for systems that can handle different rules on timing, duration, and recordkeeping. Washington State expanded mandatory training to include isolated hotel, motel, retail, and security guard employees on January 1, 2026, demonstrating how training rules are becoming more sector-specific over time. The U.S. Equal Employment Opportunity Commission continues to receive more than 25,000 workplace harassment complaints annually, which keeps pressure on employers to demonstrate that training is structured and well-documented rather than occasional and informal. In this setting, the compliance training software market is seeing stronger demand for centralized platforms that can manage different jurisdictional rules, retain records, and support measurable training outcomes over time.

Training Fatigue And Low Learner Engagement

The compliance training software market still faces a meaningful adoption challenge because many employees approach mandatory training as a legal requirement rather than a useful part of daily work. Research found that 72% of organizations cited learner engagement as their main challenge in virtual training, while only 27% viewed their virtual instructor-led training as highly effective. Completion rates on self-directed platforms can fall sharply when content feels disconnected from real work situations. This weakens both knowledge retention and the perceived value of software renewals, even when formal completion rates look acceptable on paper. The compliance training software market is responding with microlearning, gamified formats, and scenario-based tools, but learner fatigue remains a real drag on sustained program effectiveness.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Cloud-Based And Mobile Learning Delivery

- Greater Need For Audit-Ready Tracking, Certification, And Reporting

- Budget Constraints Among Small And Medium-Sized Enterprises

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment captured 66.12% of the compliance training software market in 2025, confirming that SaaS delivery had become the preferred model for organizations that need automatic updates, centralized administration, and integration with adjacent enterprise systems. In practical terms, this position reflects a market preference for faster regulatory content refreshes, greater scalability, and stronger workflow integration with HRIS and GRC environments. The cloud model also fits organizations that need to reach distributed employees without maintaining local infrastructure across several offices or regions. This advantage is becoming more visible as cybersecurity audit expectations become more formal and more documentation-heavy in the years ahead. The compliance training software market has therefore continued to shift toward hosted platforms that combine content delivery, reporting, and audit trails in a single managed environment.

On-premises deployment still retained relevance where data residency requirements, air-gapped operations, or internal security rules limited the use of shared cloud environments. Government agencies, defense contractors, and some large financial institutions remained the clearest examples of this pattern because they often operate under stricter control requirements than most commercial users. Hybrid deployment is projected to grow at a 14.67% CAGR from 2026 to 2031, making it the fastest-growing model in the compliance training software industry as organizations seek a balance between cloud flexibility and local control. The April 2026 release of the Companion browser extension and the Harmony AI search tools also showed how leading vendors are building on cloud-delivered, context-aware learning experiences rather than legacy deployment assumptions. That product direction supports a compliance training software market in which new demand is increasingly tied to usability in daily workflows rather than to basic content hosting alone.

Online delivery accounted for 72.74% of the compliance training software market in 2025, making self-paced digital learning the dominant format across enterprise sizes and end-user groups. This share reflected the need for scale, repeatability, and easy access across geographically spread workforces. Online formats also gave employers greater control over completion tracking and easier deployment across multiple compliance topics at once. For many organizations, digital delivery has become the foundation of the compliance training software market because it enables faster rollouts than classroom-led programs and works better with remote or shift-based staffing models. That base has not removed the need for higher-engagement formats, but it has established digital learning as the default delivery layer

Blended learning is projected to grow at a 13.84% CAGR from 2026 to 2031, which shows that many buyers now want stronger retention and behavioral reinforcement rather than certificate completion alone. The format combines self-paced modules with live sessions, coaching, or scenario discussions, helping organizations address topics where policy understanding alone is not enough. Blended learning delivered 24% higher engagement than classroom-only training and has seen wider adoption across organizations globally. In parallel, the January 2026 release of AI video simulations and prompt-to-scenario coaching tools aimed at making guided practice easier to scale within enterprise learning programs. These developments suggest that the compliance training software market is moving toward delivery models that connect formal completion with practical application in the workplace.

Geography Analysis

North America held 36.88% of the compliance training software market share in 2025, making it the largest regional contributor. The region combines federal requirements such as HIPAA, OSHA, FINRA, the Cybersecurity Maturity Model Certification, and the DOJ Data Security Program with a large body of state privacy laws, creating one of the most layered training environments globally. That structure supports high demand for platforms that can automate assignment, retain records, and differentiate training by role, state, and business function. A USD 1,350,000 fine issued in California in September 2025 illustrated the high cost of compliance gaps. Canada is driving demand through provincially regulated food and workplace safety training, while Mexico is generating early demand for Spanish-language modules among multinationals managing operations across North America.

Europe remains structurally important because GDPR enforcement keeps employee handling of personal data under scrutiny and exposes firms to large penalties for weak controls. The EU AI Act added a new demand layer when Article 4 AI literacy obligations became enforceable in February 2025, with fuller compliance for high-risk systems required by August 2026. Research in 2026 found that only 1 in 4 employees had high generative AI fluency, even though more than half were already using AI tools, underscoring a sustained need for structured workforce education. Germany, the United Kingdom, and France remain the largest country markets in Europe due to their concentration of regulated financial, manufacturing, and life sciences activity. Asia-Pacific is projected to grow at a 14.39% CAGR from 2026 to 2031, making it the fastest-growing region as China, Hong Kong, India, and Australia advance cybersecurity, privacy, and AI requirements.

South America remains at an earlier stage, but Brazil's data protection enforcement and Chile's evolving framework are creating baseline demand for digital compliance delivery in Portuguese and Spanish. The Middle East is advancing as Saudi Arabia and the UAE put more structure in place for data protection, security safeguards, and cross-border transfer obligations, which increases the need for localized training content and better documentation. Africa is a longer-horizon opportunity, led mainly by South Africa's Protection of Personal Information Act, while markets such as Nigeria and Egypt are still in earlier stages of regulatory development. Across these regions, vendor participation in the compliance training software market is still less mature, and demand often depends on localization capacity and the ability to adapt content to emerging national rules.

- Skillsoft Corporation

- NAVEX Global, Inc.

- SAI360 Inc.

- LRN Corporation

- Syntrio, Inc.

- Skillcast Group plc

- EasyLlama Inc.

- Axonify Inc.

- WorkRamp, Inc.

- OpenSesame Inc.

- iSpring Solutions, Inc.

- KnowBe4, Inc.

- Docebo Inc.

- Absorb Software Inc.

- Epignosis LLC

- Litmos US, L.P.

- RedVector.com, LLC

- GRC Solutions Pty Ltd

- LearnWorlds (CY) Ltd

- LearnUpon Limited

- 360training.com, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter Data Privacy and Cybersecurity Enforcement

- 4.2.2 Expansion of Mandatory Workplace Conduct and Harassment Training

- 4.2.3 Shift Toward Cloud-Based and Mobile Learning Delivery

- 4.2.4 Greater Need for Audit-Ready Tracking, Certification, and Reporting

- 4.2.5 Artificial Intelligence Literacy and Responsible Use Training Requirements

- 4.2.6 Workplace Violence Prevention Mandates Expanding Training Scope

- 4.3 Market Restraints

- 4.3.1 Training Fatigue and Low Learner Engagement

- 4.3.2 Budget Constraints Among Small and Medium-Sized Enterprises

- 4.3.3 Localization and Legal Review Bottlenecks Across Jurisdictions

- 4.3.4 Pushback on Sensitive Culture, Conduct, and Inclusion Content

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud-Based

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By Delivery Mode

- 5.2.1 Online

- 5.2.2 Blended

- 5.2.3 Classroom

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Training Type

- 5.4.1 Cybersecurity and Information Security Compliance

- 5.4.2 Data Privacy and Protection Compliance

- 5.4.3 AI Governance and Responsible AI Compliance

- 5.4.4 Ethics and Corporate Governance

- 5.4.5 DEI, Anti-harassment and Workplace Conduct

- 5.4.6 Anti-bribery and Anti-corruption

- 5.4.7 AML, KYC and Financial Crime Compliance

- 5.4.8 Workplace Safety and EHS Compliance

- 5.4.9 ESG and Sustainability Compliance

- 5.4.10 Third-party and Vendor Risk Compliance

- 5.4.11 Industry-specific Regulatory Compliance

- 5.5 By End User Vertical

- 5.5.1 IT and Telecom

- 5.5.2 Industrial Manufacturing

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Retail and Ecommerce

- 5.5.5 Energy and Utilities

- 5.5.6 Transportation and Logistics

- 5.5.7 BFSI

- 5.5.8 Construction and Engineering

- 5.5.9 Government, Defense, and Public Sector

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 Singapore

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Nigeria

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Skillsoft Corporation

- 6.4.2 NAVEX Global, Inc.

- 6.4.3 SAI360 Inc.

- 6.4.4 LRN Corporation

- 6.4.5 Syntrio, Inc.

- 6.4.6 Skillcast Group plc

- 6.4.7 EasyLlama Inc.

- 6.4.8 Axonify Inc.

- 6.4.9 WorkRamp, Inc.

- 6.4.10 OpenSesame Inc.

- 6.4.11 iSpring Solutions, Inc.

- 6.4.12 KnowBe4, Inc.

- 6.4.13 Docebo Inc.

- 6.4.14 Absorb Software Inc.

- 6.4.15 Epignosis LLC

- 6.4.16 Litmos US, L.P.

- 6.4.17 RedVector.com, LLC

- 6.4.18 GRC Solutions Pty Ltd

- 6.4.19 LearnWorlds (CY) Ltd

- 6.4.20 LearnUpon Limited

- 6.4.21 360training.com, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment