|

市場調查報告書

商品編碼

2065528

醫療保健產業的人才管理:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Talent Management In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

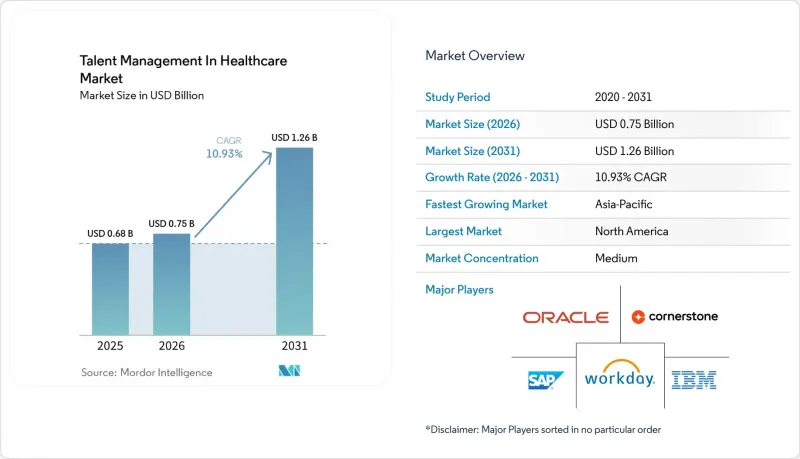

2025 年醫療保健產業的人才管理市場價值為 6.8 億美元,預計到 2031 年將達到 12.6 億美元,而 2026 年為 7.5 億美元,預測期(2026-2031 年)的複合年成長率為 10.93%。

本報告按組件(軟體和服務)、部署模式(雲端、本地部署、混合部署)、應用程式(績效管理、學習和技能發展、繼任計畫等)、最終用戶產業(醫院和醫療保健系統、門診和專科診所、居家醫療等)以及地區進行細分。市場預測以價值(美元)表示。

全球醫療保健人才管理市場的趨勢和見解。

急診護理人員嚴重短缺,加劇了人才競爭。

註冊護理師 (RN) 的持續短缺顯著增加了急診護理領域對人力資源管理平台的需求。到 2026 年初,超過 33% 的醫院報告註冊護理師空缺率超過 10%,預計全國註冊護理師缺口將達到 158,600 人。平均每家醫院有 43 個註冊護理師職缺,凸顯了問題的嚴重性。這種短缺分佈不均,某些專科,例如遙測病房和過渡病房,大約每 4.5 年就會發生一次人員全部更迭。由於如此高的離職率,人工人力資源管理不僅效率低下,而且成本高昂。因此,醫療機構正擴大採用先進的人力資源管理解決方案。憑藉人才儲備分析、內部調動追蹤和人員流動預測模型等功能,這些平台不再被視為可有可無的工具,而是成為降低財務風險和確保營運穩定性的必要手段。這一趨勢表明,醫療保健市場越來越依賴技術來解決人才挑戰,進一步推動了人才管理系統的採用。

關注醫療保健專業人員因職業倦怠導致的留任率

儘管疫情尖峰時段期已過,但職業倦怠仍是一項重大的人力資源成本。美國醫學會 (AMA) 2024 年對 43 個州的約 18,000 名醫生進行的一項調查發現,仍有 43.2% 的醫生報告至少出現一種職業倦怠症狀,而工作滿意度則上升至 76.5%,這表明透過組織干預可以提高員工敬業度。對於人才管理供應商而言,一項策略性洞察是,員工福祉計畫帶來的邊際效益是可以衡量的。一項於 2025 年在美國 50 家「磁性認證」醫院進行的多中心研究表明,擁有完善的共用管治模式、強大的工作量管理能力和積極主動的內部獎勵機制的機構,其員工倦怠發生率顯著低於其他機構。醫療保健系統越來越要求人才管理平台超越傳統的員工滿意度調查,納入針對臨床醫師的敬業度分析、工作量強度監測、職涯停滯徵兆和獎勵頻率等功能。 Prolink 於 2026 年對 400 多名外派醫護人員進行的一項調查顯示,職業倦怠 (29%)、士氣低落 (21%) 和員工留任率低 (20%) 是 2026 年醫療產業面臨的最大威脅。這證實了將員工留任率提升工具與敬業度數據掛鉤不僅僅是一種理想,而是當前優先考慮的採購事項。

中型醫療機構的IT基礎設施分散

根據CHIME發布的2026年醫療技術領導者領導力脈搏調查,76%的受訪者表示,工具的激增和碎片化導致營運困難,一些機構甚至管理超過100種企業級工具;85%的受訪者認為,資金限制是技術現代化的主要障礙。人力資源管理供應商面臨的最大挑戰是整合複雜性。 74%的受訪者表示,他們需要新平台與現有電子病歷(EHR)系統無縫連接,而許多中型人力資源管理解決方案若不投入大量資金用於專業服務,則難以克服這一難題。對於床位少於200張的醫療機構而言,這個問題更為嚴重,因為這些機構通常缺乏專門的介面工程團隊來管理預約安排、認證和薪資核算系統之間的API整合。聯邦監測數據顯示,獨立營運的重點接取醫院的EHR互通性遠低於隸屬於醫療集團的同類醫院,類似的結構性差異也存在於人力資源科技領域。無法提供與主流EHR平台預先建置和認證整合功能的供應商,在中型市場(潛在客戶數量龐大)中,將面臨銷售週期過長的風險。

細分市場分析

依組件分類,2025年醫療保健人力資源管理市場中,軟體銷售額佔比高達72.28%。這反映了大規模醫療保健系統以平台為中心的採購模式,投資者投資於多模組企業套件,並將初始授權成本累計。預計服務板塊的表現將優於整體市場,2026年至2031年的複合年成長率將達到12.43%。這是因為各種規模的供應商都意識到,配置、工作流程重組和變更管理往往決定人力資源平台能否帶來可衡量的成果。專業服務(包括實施諮詢和客製化)在服務板塊中佔據最大佔有率,但隨著企業從有時限的實施合約轉向持續的平台最佳化,對支援和維護服務的需求也在不斷成長。從策略角度來看,這意味著傳統上以軟體功能競爭的供應商現在正在擴展其服務能力並透過收購來維持年度合約價值並降低客戶流失率。

推動業務收益成長的一個細分市場趨勢是,對醫療保健特定配置專業知識的需求日益成長。即使是通用的人力資本管理 (HCM) 系統,也需要進行大量的客製化,才能滿足護理執照追蹤、多州執照協議以及醫療機構聯合委員會 (JCAHO) 要求的能力文件管理等需求。像 HealthStream 這樣的供應商正在透過建立人工智慧驅動的配置工具和預置的醫療保健內容庫來應對這項挑戰,例如 HealthStream 於 2025 年 1 月發布的學習體驗平台。這些工具和內容庫可以縮短客戶實現價值所需的時間,降低實施服務的成本,並透過內容訂閱產生持續收入。從競爭角度來看,隨著人工智慧自動化執行日常實施任務,以及供應商將託管服務層級納入訂閱定價,軟體收入和業務收益之間的界線將繼續變得模糊。

到2025年,雲端採用率將佔醫療保健人力資源管理市場68.31%的佔有率,並將成為成長最快的採用模式,到2031年複合年成長率將達到13.47%。這種由本地部署和混合環境遷移驅動的獨特組合表明,該領域不僅佔據市場主導地位,而且還在持續積極擴張。行動工作人員模式的加速發展進一步強化了醫療保健系統中的「雲端優先」趨勢。 2024年,美國5.3%的註冊護理師從事行動護理師工作,約20%的護理師在同一年更換了工作單位。這導致了資質認證和排班管理的分散化,造成了本地部署基礎設施難以應對的複雜性。 IHH Healthcare 於 2026 年 5 月在 10 個國家的 89 家醫院部署 Oracle Fusion Cloud HCM 的案例表明,一家大型跨國醫療保健集團如何利用雲端平台實現大規模人力資源可視性,而這在本地系統中是結構上不可能實現的。

儘管本地部署的市場佔有率正在下降,但在資料主權要求嚴格的國家,本地部署對政府醫院系統仍然至關重要。在中國、印度和中東地區尤其如此,這些地區的國家衛生資料法規可能會限制跨境雲端傳輸。混合部署正逐漸成為一種中間架構,它允許在本地保留高度敏感的員工數據,同時利用基於雲端的分析和人工智慧功能。對於那些已在電子健康記錄 (EHR) 基礎設施上投入巨資,但又無法承受完整平台遷移帶來的資金衝擊的系統而言,這種配置尤其重要。德國的監管合規框架,特別是聯邦勞動法院 2022 年關於強制要求記錄工時的裁決(該裁決於 2024 年經行政法院重申),正在催生對合規主導數位化人力資源工具的需求,而這種需求與部署模式無關,從而維持了混合部署在歐洲企業客戶中的有效性。

區域分析

至2025年,北美將以39.42%的市佔率引領醫療保健人力資源管理市場。這主要得益於美國無與倫比的急診護理機構密度、成熟的SaaS採購基礎設施,以及來自CMS(醫療保健服務中心)基於價值的醫療保健指示和聯合委員會認證標準的持續監管壓力。到2026年,光是美國就將面臨約158,600名註冊護理師(RN)的缺口,醫院RN離職的平均成本將達到每位護理師60,090美元。這為技術投資提供了強大的經濟獎勵。加拿大和墨西哥是規模較小但成長迅速的細分市場。加拿大也出現了與職業倦怠相關的類似離職趨勢,而墨西哥不斷擴張的私立醫院產業也開始投資基於雲端的人力資源平台。美國醫療保險和醫療補助服務中心(CMS)於2026年1月啟動了一項名為“農村醫療轉型計劃”的500億美元舉措,旨在為美國醫療服務不足的社區提供人力資源管理技術方面的資金支持。其中,科羅拉多州等州已專門撥款2.555億美元用於遠端醫療和技術整合。預計這項聯邦計畫將在預測期內鼓勵先前不願進入目標市場的本地醫療服務提供者積極參與。

預計到2025年,歐洲將佔據市場收入的相當大佔有率。德國和英國引領這一趨勢,兩國強制性的數位化考勤管理法規以及英國國家醫療服務體系(NHS)的人員短缺危機,正促使傳統的紙質人力資源流程向平台化轉型。德國聯邦勞動法院關於強制記錄工時的裁決,以及漢堡行政法院於2024年8月重申的裁決,催生了對合規驅動型數位化勞動力管理的需求,尤其是在約43萬名醫療助理(其中約50%為兼職人員)中。這些醫療助理的工作安排複雜,無法透過人工系統進行準確追蹤。英國國家醫療服務體系(NHS)仍然是主要的需求來源,NHS Management報告稱,自實施UKG Rapid Hire以來,招聘時間縮短了10天,並新增了220萬美元的年收入。法國、義大利和其他歐洲國家在醫療保健領域採用企業人力資源平台仍處於早期階段,這為擁有多語言產品組合的供應商提供了中期擴張機會。

亞太地區預計將成為成長最快的地區,到2031年複合年成長率將達到13.89%,這反映了該地區對醫療基礎設施的投資、促進醫院數位化的政策以及人力資源管理軟體市場結構性不足。印度政府運營的全印醫學科學研究所(AIIMS)網路報告稱,截至2026年3月,約有2316個教職空缺和15525個非教職空缺,分別約佔其總容量的36%和26%。此外,2026年2月,聯邦衛生部長將人工智慧輔助診斷和快速招聘教職人員列為同等重要的優先事項,這表明人力資源管理技術正在進入國家政策討論的範疇。中國國家衛生健康委員會的《智慧醫療分階段評估標準》要求在二級認證後實施數位化人力資源模組,這將影響到包括約35,000家註冊機構在內的整個公立醫院系統,並促使延方軟體和美潤等國內供應商採用相關技術。在2026年1月舉行的「亞洲醫院管理2025」大會上,一項針對醫療保健領導者的調查顯示,人力資源管理是該地區面臨的最普遍的系統性挑戰,其重要性超過了財務限制和數位轉型。在以沙烏地阿拉伯和阿拉伯聯合大公國為首的中東和非洲地區,作為與「2030願景」一致的廣泛數位轉型計畫的一部分,對醫療保健工作者管理技術的投資正在穩步推進。同時,在南美洲,特別是巴西,已經出現了早期需求,主要來自大規模私立醫院集團。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 急診護理人員嚴重短缺,加劇了競爭。

- 關注醫療保健專業人員因職業倦怠而導致的人才流失問題

- 對臨床工作人員進行強制性績效考核

- 向價值導向型醫療保健的轉變需要技能發展。

- 利用人工智慧簡化候選人匹配流程

- 遠端醫療的擴展催生了對遠距辦公人員的需求。

- 市場限制因素

- 中型供應商的IT基礎設施碎片化

- 關於員工資格記錄的資料隱私問題

- 地方醫療保健機構人力資源技術預算的限制

- 工會抵制演算法績效評估

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 專業服務

- 支援和維護服務

- 部署模式

- 雲

- 現場

- 混合

- 透過使用

- 績效管理

- 學習與技能發展

- 繼任計劃

- 薪資管理

- 招募和人才獲取

- 人員規劃

- 員工敬業度與職涯發展

- 其他人力資源管理應用

- 按最終用戶行業分類

- 醫院和醫療系統

- 門診部和專科診所

- 長期照護與復健中心

- 居家醫療服務提供者

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Oracle Corporation

- SAP SE(SuccessFactors)

- IBM Corporation(Kenexa)

- Cornerstone OnDemand, Inc.

- Workday, Inc.

- UKG Inc.

- HealthStream Inc.

- Infor Inc.

- Cerner Corporation

- ADP Inc.

- PeopleFluent(LTG)

- HealthcareSource HR Inc.

- OnShift Inc.

- Shiftboard Inc.

- Avature

- BambooHR LLC

- iCIMS

- SmartRecruiters Inc.

- PageUp People Ltd.

- Paylocity Holding Corp.

第7章 市場機會與未來展望

According to Mordor Intelligence, the talent management in healthcare market size was valued at USD 0.68 billion in 2025 and estimated to grow from USD 0.75 billion in 2026 to reach USD 1.26 billion by 2031, at a CAGR of 10.93% during the forecast period (2026-2031).

This report is Segmented by Component (Software, and Services), Deployment Mode (Cloud, On-Premise, and Hybrid), Application (Performance Management, Learning and Development, Succession Planning, and More), End User Industry (Hospitals and Health Systems, Ambulatory and Specialty Clinics, Home Healthcare Agencies, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Talent Management In Healthcare Market Trends and Insights

Acute Nursing Staff Shortage Intensifying Competition For Talent

The ongoing shortage of registered nurses (RNs) is driving significant demand for talent management platforms within the acute care sector. By early 2026, more than 33% of hospitals reported RN vacancy rates exceeding 10%, with the national shortage estimated at 158,600 RNs. On average, hospitals are managing 43 unfilled RN positions, highlighting the critical nature of this issue. This shortage is not evenly distributed, as certain specialties, such as telemetry and step-down units, are experiencing complete staff turnover approximately every 4.5 years. Such high turnover rates make manual human resource tracking both inefficient and costly. As a result, healthcare organizations are increasingly adopting advanced talent management solutions. These platforms, which offer features like pipeline analytics, internal mobility tracking, and predictive attrition modeling, are no longer viewed as optional tools. Instead, they are becoming essential for mitigating financial risks and ensuring operational stability. This trend underscores the growing reliance on technology to address workforce challenges in the healthcare market, further propelling the adoption of talent management systems.

Clinician-burnout-led Retention Focus

Burnout remains a material talent cost even as peak-pandemic rates ease. A 2024 AMA survey of nearly 18,000 physicians across 43 states found that 43.2% still reported at least one burnout symptom, while job satisfaction rose to 76.5%, signaling that improvements in engagement are achievable through organizational intervention. The strategic insight for talent management vendors is that the marginal return on well-being programs is measurable: organizations with stronger shared-governance models, better workload-control features, and active internal-recognition tools showed statistically lower burnout odds in a 2025 multicenter study across 50 Magnet-status US hospitals. Health systems have begun requiring talent platforms to include clinician-specific engagement analytics, monitoring workload intensity, career stagnation signals, and recognition frequency, beyond traditional employee satisfaction surveys. A 2026 Prolink survey of over 400 travel healthcare professionals identified burnout (29%), declining morale (21%), and workforce retention (20%) as the top perceived threats to healthcare in 2026, reinforcing that retention tooling tied to engagement data is a current, not aspirational, purchasing priority.

Fragmented IT Infrastructure In Mid Tier Providers

A 2026 CHIME Leadership Pulse Survey of healthcare technology leaders found that 76% cited tool sprawl and fragmentation as making operations harder, with some organizations managing over 100 enterprise tools, while 85% identified financial limitations as the primary barrier to technology modernization. The most consequential challenge for talent management vendors is integration complexity: 74% of survey respondents require new platforms to offer seamless connectivity with existing EHR systems, a threshold many mid-tier talent management solutions cannot clear without substantial professional services investment. For providers below the 200-bed threshold, the problem compounds, as these organizations typically lack dedicated interface engineering teams to manage API integrations across clinical scheduling, credentialing, and payroll systems. Independent critical access hospitals demonstrated substantially lower EHR interoperability than system-affiliated peers in federal monitoring data, and the same structural gap applies to HR technology. Vendors that fail to offer pre-built, certified integrations with dominant EHR platforms risk a protracted sales cycle in the mid-market, which represents a significant volume of potential accounts.

Other drivers and restraints analyzed in the detailed report include:

- Competency-tracking Mandates for Clinical Staff

- Shift to Value-based Care Demanding Upskilling

- Data Privacy Concerns Around Staff Credential Records And HR Data

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Across the component segmentation, software held a 72.28% revenue share of the talent management in healthcare market in 2025, reflecting the platform-centric buying pattern of large health systems that invest in multi-module enterprise suites and capitalize the initial license outlay. The services segment is forecast to grow at 12.43% CAGR from 2026 to 2031, outpacing the overall market, as providers of all sizes recognize that configuration, workflow redesign, and change management often determine whether a talent platform delivers measurable outcomes. Professional services, which encompass implementation consulting and customization, contribute the largest share within the services segment, while support and maintenance services are gaining traction as organizations move away from time-limited deployment contracts toward continuous platform optimization. The strategic implication is that vendors who have historically competed on software features are now building out or acquiring services capabilities to defend annual contract value and reduce churn.

A niche dynamic amplifying services revenue growth is the increasing demand for healthcare-specific configuration expertise. General-purpose HCM implementations require extensive customization to handle nurse licensure tracking, multistate compact licensure and JCAHO-required competency documentation. Vendors like HealthStream have responded by building AI-assisted configuration tooling and pre-built healthcare content libraries, such as the HealthStream Learning Experience platform launched in January 2025, that accelerate time-to-value and reduce implementation services cost for clients, while still generating recurring revenue through content subscriptions. The competitive implication is that the line between software and services revenue will continue to blur as AI automates routine implementation tasks and vendors bundle managed-service tiers into subscription pricing.

Cloud deployment held 68.31% share of the talent management in healthcare market in 2025 and is simultaneously the fastest-growing mode at 13.47% CAGR through 2031, an unusual combination indicating that this segment is both dominant and still in active expansion, driven by migration from on-premise and hybrid environments. The cloud-first preference among health systems is reinforced by accelerating mobile workforce dynamics: 5.3% of all US registered nurses worked as travel nurses in 2024, and approximately 20% changed work settings in the same year, creating distributed credential and scheduling complexity that is difficult to manage on locally hosted infrastructure. IHH Healthcare's May 2026 deployment of Oracle Fusion Cloud HCM across 89 hospitals in 10 countries illustrates how major multi-national healthcare groups are leveraging cloud platforms to achieve workforce visibility at scale that on-premise systems structurally cannot deliver.

On-premise deployment, while declining in share, retains relevance for government-owned hospital systems in countries with strict data sovereignty requirements, particularly in China, India, and the Middle East, where national health data regulations can restrict cross-border cloud transfers. Hybrid deployment is emerging as an intermediate architecture that allows organizations to maintain sensitive staff data on-premises while leveraging cloud-based analytics and AI capabilities, a configuration particularly valued in systems that have made substantial EHR infrastructure investments and cannot absorb the capital disruption of a full platform migration. Regulatory compliance frameworks in Germany, including the Federal Labor Court's 2022 mandatory time-tracking ruling reaffirmed by administrative courts in 2024, are creating compliance-driven demand for digitized HR tools regardless of deployment model, keeping hybrid viable in European enterprise accounts.

Geography Analysis

North America dominated the talent management in healthcare market with a 39.42% share in 2025, driven by the United States' unmatched density of acute-care facilities, a mature SaaS procurement infrastructure, and sustained regulatory pressure from CMS value-based care mandates and Joint Commission accreditation standards. The United States alone carries an estimated 158,600 RN shortage as of 2026, with hospital RN turnover costs averaging USD 60,090 per bedside nurse, creating a powerful financial incentive for technology investment. Canada and Mexico represent smaller but growing sub-markets: Canada is experiencing similar burnout-linked attrition dynamics, while Mexico's expanding private hospital sector is beginning to invest in cloud-based HR platforms. The CMS Rural Health Transformation Program, a USD 50 billion initiative launched in January 2026, is channeling capital into workforce technology for underserved US communities, with states like Colorado allocating USD 255.5 million specifically for telehealth and technology integration. This federal program is expected to pull previously technology-resistant rural providers into the addressable market over the forecast period.

Europe accounted for a meaningful share of market revenue in 2025, led by Germany and the United Kingdom, where mandatory digital time-tracking regulations and national health service staffing crises are converting previously paper-based HR processes into platform-enabled ones. Germany's Federal Labor Court ruling on mandatory working-hours tracking, reaffirmed by Hamburg administrative courts in August 2024, created a compliance-driven stimulus for digitized workforce management, particularly among the approximately 430,000 medical assistants, nearly 50% of whom work part-time, generating scheduling complexity that manual systems cannot accurately capture. The United Kingdom's NHS remains a major demand generator, with NHS Management reporting a 10-day reduction in time-to-hire and USD 2.2 million in new annual revenue after deploying UKG Rapid Hire. France, Italy, and the rest of Europe are at earlier stages of enterprise HR platform adoption in healthcare, offering a mid-term expansion opportunity for vendors with multilingual product configurations.

Asia-Pacific is the fastest-growing region at 13.89% CAGR through 2031, reflecting healthcare infrastructure investment, hospital digitization mandates, and a structurally under-served talent management software market. India's government-run AIIMS network reported approximately 2,316 faculty and 15,525 non-faculty vacancies as of March 2026, representing roughly 36% and 26% of sanctioned posts respectively, and the Union Health Minister linked AI-enabled diagnostics with faster faculty recruitment as co-equal priorities in February 2026, signaling that workforce technology is entering the national policy conversation. China's National Health Commission Smart Management Graded Evaluation Standard mandates digital HR modules from Level 2 certification onwards, affecting public hospitals across a system of approximately 35,000 registered facilities and driving adoption of domestic vendors such as Yanfang Software and Medrun. A January 2026 survey of healthcare leaders at the Hospital Management Asia 2025 conference identified workforce and talent management as the most prevalent systemic challenge facing the region, ahead of both financial constraints and digital transformation. The Middle East and Africa, led by Saudi Arabia and the UAE, are investing in healthcare workforce technology as part of broader Vision 2030-aligned digital transformation programs, while South America, principally Brazil, shows early-stage demand concentrated in large private hospital groups.

- Oracle Corporation

- SAP SE (SuccessFactors)

- IBM Corporation (Kenexa)

- Cornerstone OnDemand, Inc.

- Workday, Inc.

- UKG Inc.

- HealthStream Inc.

- Infor Inc.

- Cerner Corporation

- ADP Inc.

- PeopleFluent (LTG)

- HealthcareSource HR Inc.

- OnShift Inc.

- Shiftboard Inc.

- Avature

- BambooHR LLC

- iCIMS

- SmartRecruiters Inc.

- PageUp People Ltd.

- Paylocity Holding Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Acute Nursing-Staff Shortage Intensifying Competition

- 4.2.2 Clinician-burnout-led Retention Focus

- 4.2.3 Competency-tracking Mandates for Clinical Staff

- 4.2.4 Shift to Value-based Care Demanding Upskilling

- 4.2.5 AI-driven Candidate-matching Efficiencies

- 4.2.6 Telehealth Expansion Creating Remote-workforce Needs

- 4.3 Market Restraints

- 4.3.1 Fragmented IT Infrastructure in Mid-tier Providers

- 4.3.2 Data Privacy Concerns Around Staff Credential Records

- 4.3.3 Limited HR-tech Budgets in Rural Healthcare

- 4.3.4 Union Resistance to Algorithmic Performance Scoring

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Professional Services

- 5.1.2.2 Support and Maintenance Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premise

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Performance Management

- 5.3.2 Learning and Development

- 5.3.3 Succession Planning

- 5.3.4 Compensation Management

- 5.3.5 Recruitment and Talent Acquisition

- 5.3.6 Workforce Planning

- 5.3.7 Employee Engagement and Career Development

- 5.3.8 Other Talent Management Applications

- 5.4 By End User Industry

- 5.4.1 Hospitals and Health Systems

- 5.4.2 Ambulatory and Specialty Clinics

- 5.4.3 Long-Term Care and Rehab Centers

- 5.4.4 Home Healthcare Agencies

- 5.4.5 Other End User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of the Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Oracle Corporation

- 6.4.2 SAP SE (SuccessFactors)

- 6.4.3 IBM Corporation (Kenexa)

- 6.4.4 Cornerstone OnDemand, Inc.

- 6.4.5 Workday, Inc.

- 6.4.6 UKG Inc.

- 6.4.7 HealthStream Inc.

- 6.4.8 Infor Inc.

- 6.4.9 Cerner Corporation

- 6.4.10 ADP Inc.

- 6.4.11 PeopleFluent (LTG)

- 6.4.12 HealthcareSource HR Inc.

- 6.4.13 OnShift Inc.

- 6.4.14 Shiftboard Inc.

- 6.4.15 Avature

- 6.4.16 BambooHR LLC

- 6.4.17 iCIMS

- 6.4.18 SmartRecruiters Inc.

- 6.4.19 PageUp People Ltd.

- 6.4.20 Paylocity Holding Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment