|

市場調查報告書

商品編碼

2063462

醫療保健人力資源管理資訊科技:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Medical Talent Management IT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

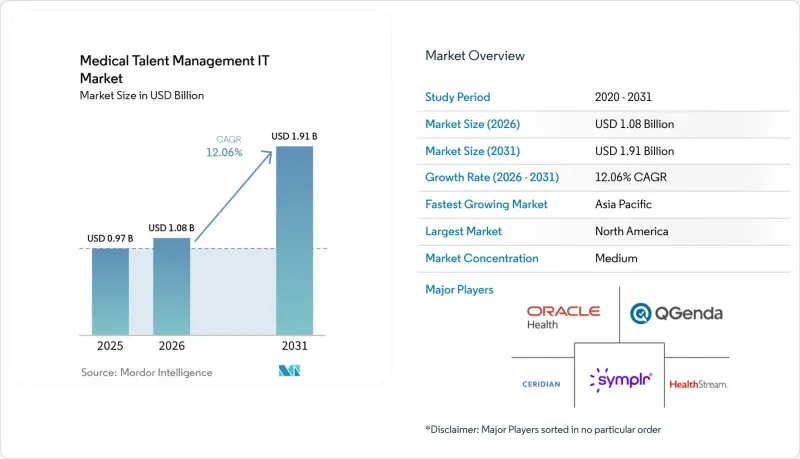

據 Mordor Intelligence 稱,2025 年醫療保健人力資源管理 IT 市場價值為 9.7 億美元,預計到 2031 年將從 2026 年的 10.8 億美元成長至 19.1 億美元,預測期(2026-2031 年)的複合年成長率為 12.06%。

本報告按組件(軟體、服務)、部署類型(Web/雲端、本地部署)、模組(招聘/應徵者追蹤、學習/合規、其他)、最終用戶(醫院/醫療保健系統、其他)、組織規模(大型企業、中型企業、中小企業)和地區(北美、歐洲、亞太、中東和非洲、南美)進行分類。預測值以美元計價。

全球醫療保健人力資源管理IT市場趨勢與洞察

由於勞動力短缺和人事費用上升的壓力,招聘、排班、提高員工留任率和分析工具的採用正在加速。

全球護理師和醫療保健專業人員短缺問題持續加劇,預計到2038年,光是美國就將面臨108,960名註冊護理師的缺口。由於醫院已將超過一半的營運預算用於人事費用,財務長們正優先考慮預測人員流動模型和人工智慧驅動的輪班管理系統,以便將員工時間重新分配到直接的患者照護中。能夠提前90天檢測潛在離職情況的即時分析,使管理人員早期療育,例如提供指導和調整輪班模式,而成本僅為填補空缺成本的十分之一左右。這些工具將人才管理系統從單純的記錄保存空間轉變為能夠直接影響產能和品質指標的營運儀表板。隨著基於價值的薪酬體系的擴展,經營團隊擴大將人員最佳化項目與再入院罰款和患者體驗獎金掛鉤,從而鞏固了對醫療保健人才管理IT市場投資的預算支持。

以雲端為先導、人工智慧驅動的人才分析和排班加速現代化進程。

2024 年 Change Healthcare 遭受的網路攻擊凸顯了單一供應商和本地部署架構帶來的系統性風險,導致薪資核算和資格資料饋送中斷數週。因此,對於缺乏資源進行全天候安全監控的中型和區域性醫院而言,採用雲端技術已成為標準的採購模式。在多站點系統中,將人工智慧演算法整合到雲端資料庫中,根據即時患者數量和病情嚴重程度評分來調整人員配置,已在運作的前六個月內實現了兩位數的加班時間減少。供應商越來越重視輪班偏好預測而非履歷篩檢,因為更精細的排班能夠更快地實現投資回報,並避免因排班不當而導致的訴訟風險。因此,醫療保健人力資源管理 IT 市場正以季度為單位發布雲端原生產品,縮短了創新週期,並推動了訂閱收入的成長。

網路安全/隱私風險和 HIPAA 合規成本正在延緩其普及。

2024年,醫療產業發生了725起可通報的資料外洩事件,平均每起事件造成的損失高達1,093萬美元。人才平台儲存著高價值數據,這些數據特別容易受到勒索軟體攻擊,例如個人識別資訊、紀律處分記錄和社會安全號碼。中型供應商每年需要花費高達30萬美元來維持HITRUST和SOC 2認證,這給他們的產品開發預算帶來了壓力,並限制了他們進入醫療保健人才管理IT市場新細分領域的能力。因此,一些醫療保健系統正在推遲全面遷移,僅在投資回報率明顯大於風險時才選擇性地採用雲端模組,同時保留其核心的人力資源和薪資核算系統在本地運作。

細分市場分析

儘管軟體支出在2025年將佔65.12%,但預計到2031年,業務收益將以14.78%的複合年成長率成長,超過醫療保健人力資源管理IT市場的軟體成長率。在大規模醫療保健系統中,隨著分散的ATS(應徵者追蹤系統)、LMS(學習管理系統)和排班產品被整合到統一的套件中,實施、資料遷移和變更管理諮詢在專案總成本中所佔的比例越來越高。

託管服務(供應商代表客戶處理認證和日程安排)發展最為迅速,它將一次性項目轉變為持續性契約,從而穩定收入。 Oracle的「勞動力即服務」 (Workforce-as-a-Service) 套件將認證專家整合到醫院團隊中,使 IT 部門擺脫了平台管理任務,這預示著定價模式正向基於結果的方向轉變。這種轉變將重塑供應商的收入模式,使那些結合軟體智慧財產權 (IP) 和深厚專業知識(而不僅僅是純粹的程式碼庫)的公司獲得豐厚回報。

預計到2025年,Web和雲端技術的採用率將佔總採用率的59.24%,複合年成長率(CAGR)為15.61%。這反映了醫療保健人力資源管理IT市場的趨勢,即買家更傾向於訂閱模式和供應商管理的安全性更新。區域性醫院表示,難以獲得網路安全人才是其放棄本地資料中心的主要原因。

儘管如此,仍有相當數量的部署保留在本地,尤其是在大學醫院、聯邦機構以及資料居住法律嚴格的地區。例如,德國的「雲端合規管理目錄」強制要求憑證必須儲存在歐盟境內,並採用混合架構,將敏感文件儲存在本地,同時將匿名化的日程資料傳送到雲端進行機器學習最佳化。供應商現在提供其 SaaS 程式碼庫的容器化版本,使客戶能夠在不影響功能的情況下切換託管模式。

區域分析

到2025年,北美將佔全球銷售額的45.23%。這是因為美國醫療保險和醫療補助服務中心 (CMS) 的人員配備要求以及《健康保險流通與責任法案》(HIPAA) 的安全法規迫使醫療服務提供者將排班、培訓和認證流程數位化。在美國醫療保健系統中,隨著勞動市場趨於膨脹,將人才分析整合到經營團隊儀表板中以提高利潤率的趨勢日益明顯。在加拿大,由於各省之間的差異,全國推廣速度較慢,但聯邦政府撥款2億加元用於建立一個可互通的醫療服務提供者註冊系統,這正在推動對基於雲端的資質認證平台的需求。墨西哥的私立醫院正在實施雙語招聘入口網站,以服務跨境醫療遊客,這為精通英語和西班牙語法規結構的供應商提供了一條獨特的成長路徑。

預計到2025年,歐洲將佔大部分支出。德國43億歐元的醫院數位化基金補貼了大部分軟體成本,促進了軟體的快速普及,同時也促使更多醫療機構選擇本地部署,以滿足GDPR的居住要求。英國的NHS員工資料舉措集中管理130萬名員工的人力資源記錄,鼓勵各醫療機構採用標準化的API進行考勤管理和績效評估資料處理。面臨預算限制的南歐國家則更傾向於選擇開放原始碼的人才管理套件,並結合本地整合商的服務。

預計到2031年,亞太地區醫療保健人員管理IT市場將以14.13%的複合年成長率成長,在所有地區中增速最高。中國計畫在2030年新增100萬名全科醫生,需要各省衛生部門大規模實現認證流程自動化。印度的國家數位健康使命已製定互通性指南,間接促使醫療機構採用基於雲端的資格認證和排班系統,以參與政府報銷計畫。在日本,一項基於人工智慧的排班試點計畫正在進行中,該計畫將護理人員的技能與老年護理的嚴重程度評分相匹配,以應對勞動力老化的挑戰。同時,澳洲和韓國正在優先考慮遠端醫療資格認證的檢驗,以維持跨轄區視訊會診。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人手不足和人事費用上升帶來的壓力正在加速招募、輪班管理、提高員工留任率和分析工具的採用。

- 以雲端優先和人工智慧驅動的勞動力分析和排班將加速現代化進程。

- LMS在合規性主導的訓練和能力追蹤(HIPAA、TJC)中的應用

- PBJ在護理領域推廣數據利用,將加速考勤管理和輪班管理的數位化。

- 更嚴格的 NCQA 認證和授權(更短的檢驗週期、持續監控)將促進認證的自動化。

- 市場限制因素

- 網路安全和隱私風險,以及 HIPAA 合規成本,都在延緩實施。

- 與電子病歷/人力資源/薪資系統整合的複雜性增加了實施的負擔。

- 圍繞長期照護 (LTC) 最低人員配備標準的政策變化降低了護理機構遵守規定的緊迫性。

- 預算限制和相互競爭的IT優先事項導致對勞動力平台的投資延遲。

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 不同的發展

- 基於Web/雲端

- 現場

- 按模組/按功能

- 應徵者追蹤系統(ATS)

- 學習與合規(LMS/LXP;繼續教育追蹤)

- 績效和繼任者發展

- 薪資福利

- 工作安排和考勤管理

- 認證和付款人登記

- 勞動力分析

- 最終用戶

- 醫院和醫療系統

- 門診護理/診所和醫生團體

- 長期照護/專業護理

- 行為醫學

- 居家醫療和臨終關懷

- 支付者/健康保險(重點在於資格認證)

- 按組織規模

- 大公司

- 中型公司

- 小規模企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- ADP

- ATOSS Software

- CAQH

- Ceridian(Dayforce)

- HealthStream

- Infor

- Modio Health

- Ntracts

- Oracle Health

- PMG Credentialing

- QGenda

- Relias

- RLDatix

- SAP SuccessFactors(SAP SE)

- Smartlinx

- Strata Decision Technology

- Streamline Verify

- symplr

- Workday

第7章 市場機會與未來展望

According to Mordor Intelligence, the medical talent management iT market size was valued at USD 0.97 billion in 2025 and is estimated to grow from USD 1.08 billion in 2026 to reach USD 1.91 billion by 2031, at a CAGR of 12.06% during the forecast period (2026-2031).

This report is Segmented by Component (Software, Services), Deployment (Web/Cloud, On-Premise), Module (Recruiting & Applicant Tracking, Learning & Compliance, and More), End User (Hospitals & Health Systems, and More), Organization Size (Large, Mid-Size, Small), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts in Value (USD).

Global Medical Talent Management IT Market Trends and Insights

Workforce Shortages and Labor Cost Pressure Intensify Adoption of Recruiting, Scheduling, Retention and Analytics Tools

Global nurse and allied-health shortfalls continue to widen, with the United States alone projecting a gap of 108,960 registered nurses by 2038. Hospitals already devote more than half of their operating budgets to labor, so CFOs are prioritizing predictive turnover models and AI-driven scheduling that can redeploy staff hours toward direct patient care. Real-time analytics that flag likely resignations 90 days in advance allow managers to intervene early with coaching or shift-pattern adjustments, which costs roughly one-tenth of back-filling an open role. Such tools convert talent systems from administrative record keepers into frontline operational dashboards that directly affect throughput and quality metrics. As value-based reimbursement expands, executives increasingly tie staffing optimization projects to readmission penalties and patient-experience bonuses, cementing budget support for Medical talent management IT market investments.

Cloud-First and AI-Enabled Workforce Analytics/Scheduling Accelerate Modernization

The Change Healthcare cyberattack in 2024 demonstrated that single-vendor or on-premise architectures create systemic risk when payroll and credentialing feeds are disrupted for weeks. Consequently, cloud deployment has become the default procurement model for mid-sized and community hospitals that lack the resources for round-the-clock security monitoring. Multi-site systems are layering AI algorithms on top of cloud databases to adjust staffing to live census and acuity scores, trimming overtime hours by double-digit percentages in the first six months after go-live. Increasingly, vendors emphasize shift-preference prediction rather than resume screening because granular scheduling improvements yield faster ROI and avoid bias litigation concerns. As a result, the Medical talent management IT market sees cloud-native releases arriving quarterly, shortening innovation cycles and reinforcing subscription revenue growth.

Cybersecurity/Privacy Risk and HIPAA Compliance Costs Slow Rollouts

Healthcare experienced 725 reportable breaches in 2024, with an average cost of USD 10.93 million per incident . Talent platforms store personal identifiers, disciplinary notes, and Social Security numbers, high-value data that attract ransomware gangs. Mid-size vendors must spend up to USD 300,000 annually to maintain HITRUST or SOC 2 certifications, eroding product-development budgets and limiting their ability to enter new Medical talent management IT market niches. Some health systems, therefore defer full-suite migration, keeping core HR or payroll on-premise while selectively adopting cloud modules only where clear ROI outweighs risk.

Other drivers and restraints analyzed in the detailed report include:

- Compliance-Driven Training and Competency Tracking Embed LMS Usage

- NCQA Credentialing/Delegation Tightening Catalyzes Credentialing Automation

- Integration Complexity with EHR/HR/Payroll Ecosystems Raises Implementation Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 65.12% of 2025 spending, yet services revenue is forecast to rise at a 14.78% CAGR through 2031, outpacing software growth in the Medical talent management IT market. Implementation, data migration, and change management consulting now account for a significant share of total project costs for large health systems as they consolidate disparate ATS, LMS, and scheduling products into unified suites.

Managed services, where a vendor operates credentialing or scheduling on the client's behalf, are expanding fastest, converting one-time projects into recurring contracts that smooth revenue. Oracle's workforce-as-a-service bundle embeds certified credentialing specialists within hospital teams and shifts platform administration off IT's plate, signaling a broader move toward outcome-based pricing. The transition reshapes vendor profitability models, rewarding companies that pair software IP with deep domain expertise rather than pure-play code bases.

Web and cloud implementations accounted for 59.24% of total installations in 2025 and are projected to grow at a 15.61% CAGR, reflecting buyer preference for subscription economics and vendor-managed security updates in the Medical talent management IT market. Community hospitals cite the inability to recruit cybersecurity talent as a top reason for exiting on-premises data centers.

Even so, a significant number of deployments remain on-premise, especially in academic medical centers, federal institutions, and regions with strict data-residency laws. Germany's Cloud Compliance Controls Catalogue, for instance, requires credential files to be stored within EU borders, prompting hybrid architectures that store sensitive documents locally while sending anonymized scheduling data to the cloud for machine learning optimization. Vendors now offer containerized versions of their SaaS code bases, letting customers switch between hosting models without functional trade-offs

Geography Analysis

North America generated 45.23% revenue in 2025 as CMS staffing mandates and HIPAA security rules forced providers to digitize scheduling, learning, and credentialing workflows. U.S. health systems increasingly embed workforce analytics into board-level dashboards, framing them as levers for margin expansion amid inflationary labor markets. Canada's provincial fragmentation slows national roll-outs, yet a federal CAD 200 million allocation for interoperable provider registries is boosting demand for cloud credentialing platforms. Mexico's private hospitals deploy bilingual recruiting portals to serve cross-border medical tourists, signaling a niche growth path for vendors fluent in both English and Spanish regulatory frameworks.

Europe contributed a significant share of the 2025 spending. Germany's EUR 4.3 billion hospital digitization fund reimburses the majority of software costs, spurring rapid procurement but also reinforcing on-premise hosting preferences to meet GDPR residency clauses. The United Kingdom's NHS Workforce Data Initiative centralizes staffing records for 1.3 million employees, pushing trusts to adopt standardized APIs for time-and-attendance and competency feeds. Southern European countries face budget constraints, so they favor open-source talent suites bundled with local integrator services.

Asia-Pacific is projected to grow at a 14.13% CAGR through 2031, the fastest among all regions in the Medical talent management IT market. China aims to license 1 million new general practitioners by 2030, requiring mass-scale credentialing automation across provincial health bureaus. India's National Digital Health Mission sets interoperability guidelines that indirectly compel provider organizations to adopt cloud credentialing and scheduling to participate in government reimbursement programs. Japan's aging workforce drives AI-based scheduling pilots that match nurse skills to geriatric-care acuity scores, while Australia and South Korea prioritize telemedicine credential validation to sustain cross-jurisdiction video consultations.

- ADP

- ATOSS Software

- CAQH

- Ceridian (Dayforce)

- HealthStream

- Infor

- Modio Health

- Ntracts

- Oracle Health

- PMG Credentialing

- QGenda

- Relias

- RLDatix

- SAP SuccessFactors (SAP SE)

- Smartlinx

- Strata Decision Technology

- Streamline Verify

- symplr

- Workday

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Workforce Shortages and Labor Cost Pressure Intensify Adoption of Recruiting, Scheduling, Retention and Analytics Tools

- 4.2.2 Cloud-First And AI-Enabled Workforce Analytics/Scheduling Accelerate Modernization

- 4.2.3 Compliance-Driven Training and Competency Tracking (HIPAA, TJC) Embed LMS Usage

- 4.2.4 PBJ Staffing-Data Enforcement in Long-Term Care Accelerates Time/Attendance And Scheduling Digitization

- 4.2.5 NCQA Credentialing/Delegation Tightening (Shorter Verification Windows, Continuous Monitoring) Catalyzes Credentialing Automation

- 4.3 Market Restraints

- 4.3.1 Cybersecurity/privacy risk and HIPAA compliance costs slow rollouts

- 4.3.2 Integration complexity with EHR/HR/payroll ecosystems raises implementation burden

- 4.3.3 Policy volatility around LTC staffing minimums reduces compliance-driven urgency in nursing homes

- 4.3.4 Budget constraints and competing IT priorities delay workforce platform investments

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 Web/Cloud-based

- 5.2.2 On-premise

- 5.3 By Module / Function

- 5.3.1 Recruiting & Applicant Tracking (ATS)

- 5.3.2 Learning & Compliance (LMS/LXP; CE tracking)

- 5.3.3 Performance & Succession

- 5.3.4 Compensation & Benefits

- 5.3.5 Scheduling & Time & Attendance

- 5.3.6 Credentialing & Payer Enrollment

- 5.3.7 Workforce Analytics

- 5.4 By End User

- 5.4.1 Hospitals & Health Systems

- 5.4.2 Ambulatory/Clinics & Physician Groups

- 5.4.3 Long-term Care / Skilled Nursing

- 5.4.4 Behavioral Health

- 5.4.5 Home Health & Hospice

- 5.4.6 Payers / Health Plans (credentialing-focused)

- 5.5 By Organization Size

- 5.5.1 Large Enterprises

- 5.5.2 Mid-size Enterprises

- 5.5.3 Small Enterprises

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 ADP

- 6.3.2 ATOSS Software

- 6.3.3 CAQH

- 6.3.4 Ceridian (Dayforce)

- 6.3.5 HealthStream

- 6.3.6 Infor

- 6.3.7 Modio Health

- 6.3.8 Ntracts

- 6.3.9 Oracle Health

- 6.3.10 PMG Credentialing

- 6.3.11 QGenda

- 6.3.12 Relias

- 6.3.13 RLDatix

- 6.3.14 SAP SuccessFactors (SAP SE)

- 6.3.15 Smartlinx

- 6.3.16 Strata Decision Technology

- 6.3.17 Streamline Verify

- 6.3.18 symplr

- 6.3.19 Workday

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment