|

市場調查報告書

商品編碼

2064543

GPU 和 AI 伺服器電源管理模組 (VRM):市場佔有率分析、行業趨勢與統計數據以及成長預測 (2026-2031)Power Delivery Module (VRM) For GPU And AI Servers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

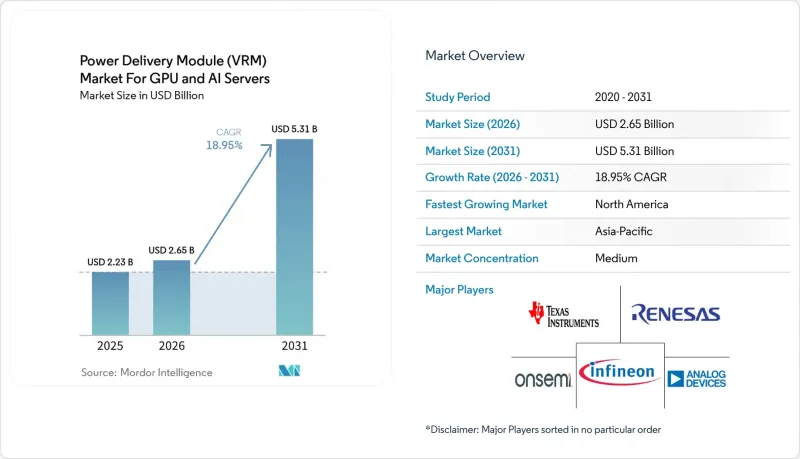

根據 Mordor Intelligence 預測,電源模組 (VRM) 的市場規模預計將從 2024 年的 17.8 億美元成長到 2025 年的 22.3 億美元,到 2031 年達到 53.1 億美元,2026 年至 2031 年的複合年成長率為 18.95%。

本報告按VRM類型(多相數字式、模擬式等)、相數(6相及以下、7-12相、13-20相、20相及以上)、功率容量(低功率(小於100A)、中功率(100-300A)、其他)、組件(功率級、PWM控制器等)、最終用途(GPU卡、AI/HPC伺服器等)和地區進行分類。市場預測以美元(USD)計價。

全球GPU及AI伺服器電源模組(VRM)市場趨勢及分析

超大規模資料中心對GPU加速器的需求日益成長。

到 2025 年,隨著運算架構向大型語言模型和建議引擎轉型,超大規模營運商將部署超過 300 萬個 GPU 加速器。 NVIDIA H200 和 AMD MI300X 顯示卡單張功耗高達 1000 瓦,因此 VRM 需要從亞伏級電源軌提供 1200 安培的電流,且漣波小於 10 毫伏特。直接水冷機架可實現超過 100 千瓦的功率密度,從而加速整合式電源模組的普及,縮小基板面積。超大規模資料中心業者現在需要即時遙測相電流、溫度和效率,這些規範有利於數位多相控制器的應用。這些業者擴大在 24-36 個月的供貨合約下合作開發特定應用模組,繞過了傳統的通路。

向 3D 堆疊式 HBM 記憶體的過渡將提高瞬態負載要求。

HBM3E 於 2024 年下半年開始量產,其瞬態階躍電流高達每微秒 200 安培。此外,HBM4 原型機預計到 2027 年單堆疊功率將超過 50 瓦。 VRM 供應商正透過採用耦合電感和自適應電壓調節器來應對這項挑戰,從而將輸出電阻降低 40%。 2025 年 3 月,德克薩斯(TI) 的 6 相參考設計實現了 500 安培電流下 15 毫伏特的瞬態響應。 GPU 晶片和記憶體之間垂直距離的縮短提高了電阻差,迫使 VRM 必須放置在距離基板20 毫米以內。垂直於基板安裝的垂直電源模組可將迴路電感降低 50%,但需要專用的機械固定裝置和散熱介面。

高性能功率級供應鏈面臨壓力。

由於基板供應商優先生產利潤較高的晶片,到2026年初,DrMOS和智慧功率等級的前置作業時間延長至26週。 Vishay報告稱其運轉率率達95%,訂單積壓已持續到2025年下半年。 Onsemi於2025年10月收購Vcore,確保了氮化鎵晶圓的產能,並標誌著其正朝著垂直整合的方向邁進,以穩定供應。英飛凌累計8億歐元(9.04億美元)用於增購碳化矽晶圓,但預計新晶圓廠要到2027年下半年才能滿載運作。每相電流超過100安培的裝置短缺最為嚴重,因為這類裝置需要銅夾鍵結以確保足夠的散熱裕度。 VRM設計人員將不得不對替代供應商進行認證並修改韌體,這將使開發週期延長至多9個月。

細分市場分析

多相數位控制單元 (DCU) 正在推動電源模組 (VRM)韌體佔有率的成長,預計到 2025 年將占到總銷售額的 61%。這些單元之所以備受青睞,是因為它們具備韌體可更新的控制迴路和 PMBus 遙測等先進功能,使其成為超大規模資料中心業者叢集監控系統的理想之選。韌體更新確保了系統能夠適應不斷變化的需求,而 PMBus 遙測則支援即時監控,從而在大規模運行中實現高效率和高可靠性。整合式電源模組 (IPM) 雖然到 2025 年的市佔率較小,但預計在預測期內將以 19.74% 的複合年成長率 (CAGR) 實現最高成長。這一成長主要得益於伺服器製造商對緊湊型即插即用解決方案的需求不斷成長,這些解決方案能夠簡化設計並縮短開發週期。

在電源模組 (VRM) 領域,整合模組的市場佔有率正穩步成長,這得益於 48 伏特中間總線和水冷機架等技術的進步,這些技術能夠實現更緊湊、更高效的佈局。 Vicor 等廠商引領著這一趨勢,提供將控制器、功率級和耦合電感器整合到單一封裝中的創新解決方案。這種整合可減少約 40% 的基板面積,為製造商帶來顯著的空間節省優勢。雖然類比控制器在邊緣設備中仍然具有成本效益,但長期趨勢正在轉向數位或混合設計。這些先進的設計提供了一種平衡的方法,將低延遲與增強的遙測功能相結合,這對於需要精確電源管理和監控的現代應用至關重要。

2025年,13相至20相供電方案將佔銷售額的43%,成為功耗高達700瓦加速器的標準配備。這些方案被廣泛採用,以滿足高效能運算系統的電力需求。然而,受GPU功耗需求不斷成長的推動(預計未來幾年GPU功耗將超過1200瓦),20相及以上供電方案預計將以19.63%的複合年成長率成長。

此層級電源管理模組 (VRM) 市場的成長主要得益於耦合電感技術的進步,該技術能夠在緊湊的 6 相封裝內實現相當於 12 相的性能。這項創新不僅提高了電源傳輸效率,也最佳化了基板空間。此外,整合電流偵測技術的智慧功率等級有助於減少佈線擁塞,並簡化 24 相和 32 相的佈局設計。能夠有效整合高相位控制器和垂直安裝解決方案的供應商,將能夠更好地掌握下一代 GPU 發布帶來的市場需求,因為這些技術與不斷變化的市場需求相契合。

區域分析

預計到2025年,亞太地區將佔全球營收的58%,這主要得益於台積電(TSMC)封裝技術的進步以及中國百萬兆級計算叢集的建設。日本的Rapidus舉措已獲得9,200億韓元(約62億美元)的資金籌措,旨在2027年實現2奈米邏輯晶片的生產,預計將顯著提升對0.6V以下電壓調節模組(VRM)的需求。韓國的K-Chips法案正在投資26兆韓元(約195億美元)用於國內電源管理IC生產線建設,這將促進SK海力士和三星等主要企業的業務擴張。同時,印度150億美元的補貼計畫正在吸引組裝投資,儘管控制器晶片的大部分矽晶圓仍然來自台灣和美國。

預計北美將迎來最高成長率,到2031年複合年成長率將達到20.95%,這主要得益於《晶片法案》(CHIPS Act)的推動,該法案旨在促進半導體製造能力的本土化。英特爾位於亞利桑那州、投資200億美元的製造工廠預計將於2026年底前完成電源管理生產線的安裝;而Wolfspeed位於北卡羅來納州、投資65億美元的碳化矽(SiC)工廠預計也將於2026年投產。此外,微軟Azure和亞馬遜網路服務(AWS)等雲端服務供應商計劃在2027年分別部署超過50萬個GPU,預計將導致對電壓調節模組(VRM)的需求超過500兆瓦。

由於歐洲地區GPU產能不足,其市佔率仍有限。然而,總額達430億歐元(約486億美元)的《歐洲晶片法案》正積極資助德國和荷蘭等國建立電源管理設計中心。相較之下,中東、非洲和南美市場仍處於發展初期,嚴重依賴進口VRM來支持政府主導的人工智慧研究叢集。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 超大規模資料中心對GPU加速器的需求日益成長。

- 雲端服務供應商必須採取的能源效率措施

- 向 3D 堆疊式 HBM 記憶體的過渡提高了瞬態負載要求。

- 採用先進的FinFET製程節點,降低了核心電壓。

- 邊緣人工智慧推理正在推動緊湊型、高電流電壓調節模組 (VRM) 的發展。

- 政府對國內半導體供應鏈的獎勵

- 市場限制因素

- 高性能功率級供應鏈面臨壓力。

- 高密度GPU卡佈局中的基板空間限制

- 電流超過 800 安培的軌道面臨溫度控管的挑戰

- 伺服器OEM廠商VRM規範缺乏標準化

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章:預測市場規模與成長率

- 按類型分類的 VRM

- 多相電壓調節模組(數位控制)

- 類比電壓調節模組

- 整合式電源模組

- 混合型 VRM

- 按階段

- 6相或更少

- 第 7-12 階段

- 第 13-20 階段

- 超過20個階段

- 按功率容量

- 低功率(小於100安培)

- 中等功率(100-300 安培)

- 高功率(300-800 安培)

- 超高功率(超過 800 安培)

- 依組件類型

- 功率級(DrMOS/SPS)

- PWM控制器

- 電感器(扼流圈)

- 電容器

- 按最終用途

- GPU加速卡

- AI/HPC伺服器

- 人工智慧訓練系統

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 世界其他地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- Infineon Technologies AG

- onsemi

- Analog Devices, Inc.

- Monolithic Power Systems, Inc.

- Rohm Co., Ltd.

- STMicroelectronics NV

- Vicor Corporation

- Delta Electronics, Inc.

- Bel Fuse Inc.(Bel Power Solutions)

- Advanced Energy Industries, Inc.

- Murata Manufacturing Co., Ltd.

- Vishay Intertechnology, Inc.

- Coilcraft, Inc.

- TDK Corporation

- Lite-On Technology Corporation

- Foxconn Interconnect Technology Ltd.

- FSP Technology Inc.

- XP Power Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the power delivery module (VRM) market size is expected to increase from USD 1.78 billion in 2024 to USD 2.23 billion in 2025 and reach USD 5.31 billion by 2031, growing at an 18.95% CAGR over 2026-2031.

This report is Segmented by VRM Type (Multiphase Digital, Analog, and More), Phase Count (<=6, 7-12, 13-20, and 20+), Current Capacity (Low <<100A, Mid 100-300A, and More), Component (Power Stages, PWM Controllers, and More), End Application (GPU Cards, AI/HPC Servers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Insights and Trends of Power Delivery Module (VRM) Market For GPU And AI Servers

Growing Demand for GPU Accelerators in Hyperscale Data Centers

Hyperscale operators deployed more than 3 million GPU accelerators in 2025 as compute fabrics shifted toward large language models and recommendation engines. Each NVIDIA H200 or AMD MI300X card draws up to 1,000 watts, forcing VRMs to deliver 1,200 amperes at sub-volt rails with ripple below 10 millivolts. Direct liquid-cooled racks enable power densities above 100 kilowatts, encouraging the use of integrated power modules that compress board footprint. Hyperscalers now require real-time telemetry for phase current, temperature, and efficiency, a specification that favors digital multiphase controllers. These operators increasingly co-develop application-specific modules under 24- to 36-month supply agreements, bypassing traditional distribution channels.

Transition Toward 3D Stacked HBM Memory Raising Transient Load Requirements

HBM3E, in volume since late 2024, introduces transient steps of 200 amperes per microsecond; HBM4 prototypes will push per-stack power past 50 watts by 2027. VRM suppliers respond with coupled inductors and adaptive voltage positioning, lowering output impedance by 40%. A Texas Instruments six-phase reference design achieved a 15-millivolt transient response at 500 amperes in March 2025. The vertical distance between the GPU die and the memory is shrinking, tightening impedance budgets and forcing VRM placement within 20 millimeters of the substrate. Vertical power modules mounted perpendicular to the board reduce loop inductance by 50%, but they demand custom mechanical fixtures and thermal interfaces.

Supply Chain Tightness for High-Performance Power Stages

Lead times for DrMOS and smart power stages stretched to 26 weeks in early 2026 as substrate suppliers prioritized high-margin chiplets. Vishay reported 95% utilization and a backlog into late 2025. Onsemi's October 2025 acquisition of Vcore secured gallium nitride wafer capacity, illustrating vertical integration moves to stabilize supply. Infineon earmarked EUR 800 million (USD 904 million) for additional silicon-carbide wafers, though new fabs will not reach full output until late 2027. Shortages are most acute above 100 amperes per phase, where copper-clip bonding is needed for thermal headroom. VRM designers must qualify alternate vendors and revise firmware, extending development cycles by up to 9 months.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Mandates from Cloud Service Providers

- Adoption of Advanced FinFET Nodes Lowering Core Voltages

- Thermal Management Challenges Above 800 A Rails

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Multiphase, digitally controlled units led the Power Delivery Module (VRM) market share, accounting for 61% of revenue in 2025. These units are preferred due to their advanced features, including firmware-updatable control loops and PMBus telemetry, which are well-suited for hyperscaler fleet monitoring systems. The ability to update firmware ensures adaptability to evolving requirements, while PMBus telemetry provides real-time monitoring and control, making these units highly efficient and reliable for large-scale operations. Integrated power modules, although representing a smaller market share in 2025, are projected to experience the fastest CAGR of 19.74% during the forecast period. This growth is driven by server builders' increasing preference for compact, drop-in solutions that simplify design and reduce development time.

The market share of integrated modules in the Power Delivery Module (VRM) sector is steadily increasing, supported by advancements such as 48-volt intermediate buses and liquid-cooled racks, which enable tighter, more efficient layouts. Vendors like Vicor are at the forefront of this trend, offering innovative solutions that integrate controllers, power stages, and coupled inductors into a single package. This integration reduces board area by approximately 40%, providing significant space-saving benefits for manufacturers. While analog controllers remain cost-effective for edge devices, the long-term trend is shifting toward digital or hybrid designs. These advanced designs offer a balanced approach, combining low latency with enhanced telemetry capabilities, which are critical for modern applications requiring precise power management and monitoring.

Thirteen- to 20-phase solutions accounted for 43% of the revenue in 2025, establishing themselves as the standard for accelerators requiring up to 700 watts of power. These solutions are widely adopted because they meet the power demands of high-performance computing systems. However, the 20-plus phase tier is projected to grow at a compound annual growth rate (CAGR) of 19.63%, driven by the increasing power requirements of GPUs, which are expected to surpass 1,200 watts in the coming years.

The growth of the Power Delivery Module (VRM) market in this tier is supported by advancements in coupled inductors, which enable 12-phase performance within a compact six-phase footprint. This innovation allows for more efficient power delivery while optimizing space on circuit boards. Additionally, smart power stages with integrated current sensing technology help reduce routing congestion and streamline the design of 24- and 32-phase layouts. Suppliers who can effectively integrate high-phase controllers with vertical packaging solutions are well positioned to capitalize on demand for next-generation GPU launches, as these technologies align with evolving market requirements.

Geography Analysis

Asia-Pacific generated 58% of 2025 revenue, driven by Taiwan Semiconductor Manufacturing Company's advancements in packaging technologies and China's development of exascale training clusters. Japan's Rapidus initiative secured JPY 920 billion (USD 6.2 billion) in funding to achieve 2-nanometer logic production by 2027, which is expected to create significant demand for sub-0.6-volt Voltage Regulator Modules (VRMs). South Korea's K-Chips Act is channeling KRW 26 trillion (USD 19.5 billion) into domestic power-management IC production lines, facilitating expansions by major players such as SK hynix and Samsung. Meanwhile, India's USD 15 billion subsidy program is attracting assembly investments; however, the majority of controller silicon is still sourced from Taiwan and the United States.

North America is anticipated to experience the fastest Compound Annual Growth Rate (CAGR) of 20.95% through 2031, primarily due to the CHIPS Act, which is incentivizing the localization of semiconductor manufacturing capacity. Intel's USD 20 billion Arizona fabrication facility is set to include a power-management production line by late 2026, while Wolfspeed's USD 6.5 billion silicon carbide (SiC) plant in North Carolina is expected to begin operations in 2026. Additionally, cloud service providers such as Microsoft Azure and Amazon Web Services are planning to deploy over 500,000 GPUs each by 2027, resulting in a projected VRM demand exceeding 500 megawatts.

Europe's market share remains limited due to the region's lack of GPU manufacturing capabilities. However, the EUR 43 billion (USD 48.6 billion) European Chips Act is actively funding the establishment of power-management design hubs in countries like Germany and the Netherlands. In contrast, the markets in the Middle East, Africa, and South America are still in their early stages of development, relying heavily on imported VRMs to support government-sponsored AI research clusters.

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- Infineon Technologies AG

- onsemi

- Analog Devices, Inc.

- Monolithic Power Systems, Inc.

- Rohm Co., Ltd.

- STMicroelectronics N.V.

- Vicor Corporation

- Delta Electronics, Inc.

- Bel Fuse Inc. (Bel Power Solutions)

- Advanced Energy Industries, Inc.

- Murata Manufacturing Co., Ltd.

- Vishay Intertechnology, Inc.

- Coilcraft, Inc.

- TDK Corporation

- Lite-On Technology Corporation

- Foxconn Interconnect Technology Ltd.

- FSP Technology Inc.

- XP Power Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand For GPU Accelerators In Hyperscale Data Centers

- 4.2.2 Energy-Efficiency Mandates From Cloud Service Providers

- 4.2.3 Transition Toward 3D Stacked HBM Memory Raising Transient Load Requirements

- 4.2.4 Adoption Of Advanced FinFET Nodes Lowering Core Voltages

- 4.2.5 AI Inference At The Edge Driving Compact High-Current VRMs

- 4.2.6 Government Incentives For Domestic Semiconductor Supply Chains

- 4.3 Market Restraints

- 4.3.1 Supply Chain Tightness For High-Performance Power Stages

- 4.3.2 Board Space Constraints In Dense GPU Card Layouts

- 4.3.3 Thermal Management Challenges Above 800 A Rails

- 4.3.4 Limited Standardization Across Server OEM VRM Specifications

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By VRM Type

- 5.1.1 Multiphase VRMs (Digital-controlled)

- 5.1.2 Analog VRMs

- 5.1.3 Integrated Power Modules

- 5.1.4 Hybrid VRMs

- 5.2 By Phase Count

- 5.2.1 <=6 Phases

- 5.2.2 7-12 Phases

- 5.2.3 13-20 Phases

- 5.2.4 20+ Phases

- 5.3 By Current Handling Capacity

- 5.3.1 Low Power (<100 A)

- 5.3.2 Mid Power (100-300 A)

- 5.3.3 High Power (300-800 A)

- 5.3.4 Ultra High Power (800 A+)

- 5.4 By Component Type

- 5.4.1 Power Stages (DrMOS / SPS)

- 5.4.2 PWM Controllers

- 5.4.3 Inductors (Chokes)

- 5.4.4 Capacitors

- 5.5 By End Application

- 5.5.1 GPU Accelerator Cards

- 5.5.2 AI / HPC Servers

- 5.5.3 AI Training Systems

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Rest of the World

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Texas Instruments Incorporated

- 6.4.2 Renesas Electronics Corporation

- 6.4.3 Infineon Technologies AG

- 6.4.4 onsemi

- 6.4.5 Analog Devices, Inc.

- 6.4.6 Monolithic Power Systems, Inc.

- 6.4.7 Rohm Co., Ltd.

- 6.4.8 STMicroelectronics N.V.

- 6.4.9 Vicor Corporation

- 6.4.10 Delta Electronics, Inc.

- 6.4.11 Bel Fuse Inc. (Bel Power Solutions)

- 6.4.12 Advanced Energy Industries, Inc.

- 6.4.13 Murata Manufacturing Co., Ltd.

- 6.4.14 Vishay Intertechnology, Inc.

- 6.4.15 Coilcraft, Inc.

- 6.4.16 TDK Corporation

- 6.4.17 Lite-On Technology Corporation

- 6.4.18 Foxconn Interconnect Technology Ltd.

- 6.4.19 FSP Technology Inc.

- 6.4.20 XP Power Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

全球功率分離式元件和模組市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球功率分離式元件和模組市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026 年至 2035 年電動車動力模組的市場機會、成長要素、產業趨勢分析與預測。SiC功率元件和模組專利監測功率分離式元件模組市場機會、成長促進因素、產業趨勢分析及2026-2035年預測

2026 年至 2035 年電動車動力模組的市場機會、成長要素、產業趨勢分析與預測。SiC功率元件和模組專利監測功率分離式元件模組市場機會、成長促進因素、產業趨勢分析及2026-2035年預測 汽車電源模組市場:2026-2032年全球市場預測(按模組類型、驅動系統、額定電壓、冷卻方式、應用和銷售管道)碳化矽功率模組市場:按產品類型、冷卻技術、額定電壓、應用和最終用戶分類-2026-2032年全球預測小型高壓功率模組市場:按拓撲結構、額定功率、輸出電壓、安裝方式和應用分類-全球預測,2026-2032年IGBT 和 SiC 模組市場按技術、類型、額定電壓、材料、應用、終端用戶產業和最終用戶分類,全球預測,2026-2032 年

汽車電源模組市場:2026-2032年全球市場預測(按模組類型、驅動系統、額定電壓、冷卻方式、應用和銷售管道)碳化矽功率模組市場:按產品類型、冷卻技術、額定電壓、應用和最終用戶分類-2026-2032年全球預測小型高壓功率模組市場:按拓撲結構、額定功率、輸出電壓、安裝方式和應用分類-全球預測,2026-2032年IGBT 和 SiC 模組市場按技術、類型、額定電壓、材料、應用、終端用戶產業和最終用戶分類,全球預測,2026-2032 年 功率分離式元件和模組市場分析及預測(至2035年):按類型、產品、服務、技術、應用、最終用戶、功能、安裝類型和設備分類

功率分離式元件和模組市場分析及預測(至2035年):按類型、產品、服務、技術、應用、最終用戶、功能、安裝類型和設備分類 全球碳化矽功率模組市場預測至2034年:依產品類型、技術、額定電壓、冷卻技術、應用、最終用戶和地區分類

全球碳化矽功率模組市場預測至2034年:依產品類型、技術、額定電壓、冷卻技術、應用、最終用戶和地區分類