|

市場調查報告書

商品編碼

2064513

員工流動率預測軟體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Employee Attrition Prediction Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

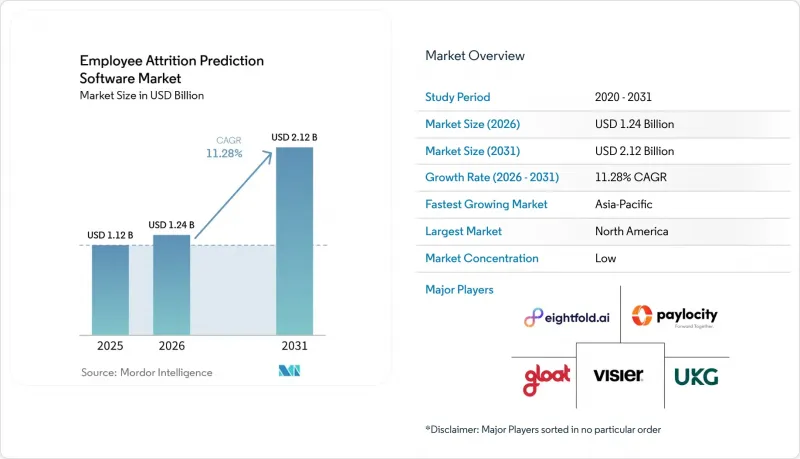

根據 Mordor Intelligence 預測,員工離職率預測軟體的市場規模預計將在 2025 年達到 11.2 億美元,2026 年達到 12.4 億美元,到 2031 年達到 21.2 億美元,2026 年至 2031 年的複合年成長率為 11.28%。

本報告按元件(軟體、服務)、應用程式(例如,員工流動預測和風險評分)、部署方式(雲端、本地部署)、組織規模(大型企業、中小企業)、最終用戶產業(例如,零售、電子商務)和地區進行細分。市場預測以美元計價。

全球員工離職率預測軟體市場趨勢與分析

員工流動率過高和替代人員招募延遲導致成本增加。

不斷上漲的員工更替成本使得員工離職預測軟體在業務部門層級更具合理性。這是因為人才保留技術如今與可避免的人事費用直接相關。預計到2026年,員工離職成本將達到45,236美元,高於2025年的36,723美元,其中50%的美國公司預計2026年員工自願離職率將進一步上升。這項轉變意義重大,因為採購方現在不僅將員工離職視為人力資源問題,更將其視為一項成本管理問題,會對預算產生直接影響。根據Gloat的一份報告,如果能夠比經理獨立識別高風險員工提前六週識別出來,這些被識別員工的留任率可達到68%。此外,干預成本為28,000美元,而替代招聘的成本則高達340,000美元,這意味著一個業務部門總共節省了480萬美元。隨著員工保留策略在採購談判中被越來越頻繁地提及,員工離職預測軟體的市場正從可選的試點階段轉向主流的人力資源投資。現在,在考慮購買時,實際的挑戰已經從公司是否需要預測性客戶留存軟體,轉變為哪個平台最適合其內部招聘成本、管理工作流程和乾預能力。

擴大人工智慧和機器學習在員工離職風險評分的應用

員工離職預測軟體市場也受益於機器學習的廣泛應用,機器學習被視為一種可靠的手段,能夠幫助管理者在明顯的預警訊號出現之前識別離職風險。 Lotis Blue 的概念驗證部署表明,機器學習模式能夠以 90% 的準確率預測醫護人員的離職情況,且 45% 的離職員工先前未收到任何留任溝通。這一結果支持了預測系統日益普及的觀點,因為它們能夠揭示人工審核中經常被忽略的潛在風險。這也解釋了為什麼買家現在需要的不僅僅是儀表板,因為僅憑基礎報告無法改變結果,除非這些報告能夠促使管理層採取行動。隨著部署規模的擴大以及績效評估、員工敬業度和其他人力資源數據的輸入變得日益複雜,能夠保持模型更新的供應商很可能在員工離職預測軟體市場中佔據優勢。這催生了對模型重新調優、可解釋性和資料品管,尤其對於那些已經在人力資源流程中使用生成式人工智慧的公司而言更是如此。

員工資料隱私與人工智慧管治合規性

合規壓力仍然是員工離職預測軟體市場的主要阻力,因為許多雇主被迫將其視為高風險的人工智慧應用案例。歐盟人工智慧法律的法律分析指出,附件三中關於透明度、人工監督和偏見測試的義務適用於評估或影響員工行為的勞動力管理工具,即使合規期限已延長,相關規劃要求也已生效。這意味著產品部署不再只是一項技術任務,因為法律審查、文件編制、管治設計和審計準備都已成為同一專案的一部分。 GDPR的執行也持續施加巨大的壓力,根據2025年的一份報告,累積罰款首次超過50億歐元(54億美元)。員工離職預測軟體市場受到的影響顯而易見,銷售週期延長,第一年的部署負擔加重,尤其是在歐洲和具有類似課責規則的司法管轄區。即使產品在技術上更勝一籌,如果供應商無法證明其產品具備清晰的同意邏輯、人工審核管道和偏見控制機制,其轉換速度往往也會較慢。

細分市場分析

儘管軟體仍是核心收入來源,但預計到2031年,服務板塊的複合年成長率將達到12.91%,並有望在2025年成為員工離職預測軟體市場中成長最快的板塊。軟體仍然是大部分商業性價值的基礎,因為它提供了買家最初購買許可的預測引擎、資料模型、工作流程邏輯和報告介面。這種基礎性定位意味著軟體仍然是每筆重大交易的核心,尤其對於那些尋求跨地區和業務部門廣泛了解員工留存情況的大型組織而言更是如此。同時,員工離職預測軟體產業正朝著更複雜的部署模式轉變,這些模式依賴於設定、上線和跨職能部署支援。隨著許多買家需要協助將模型輸出轉換為管理員行為、政策變更和持續管治的常規流程,服務板塊的擴張正在加速。

隨著員工離職預測軟體市場從簡單的儀錶板部署轉向整合到業務流程中的營運階段,實施和整合工作變得日益重要。供應商投入更多時間配置連接器、設計干預措施、調整警報並促進管理員採用,因為這些步驟以及模型準確性現在都會顯著影響最終交付的價值。服務團隊也正在幫助客戶避免流失,因為依賴供應商進行流程重組和變更協助的客戶不太可能將平台視為可替代的。這使得供應商能夠建立更牢固的長期合作關係,而服務也成為供應商和買家切實可行的員工保留工具。類似的趨勢也提升了認證合作夥伴網路的重要性,因為買家正在尋找已經了解關鍵人力資本管理 (HCM) 技術堆疊及其公司管治要求的部署資源。

到2025年,員工離職預測和風險評分將佔總收入的36.71%,這一應用情境在員工離職預測軟體市場中仍佔據核心地位。許多公司仍從這裡入手,因為離職風險評分是展現人才數據價值最直接的方式。這為人力資源團隊和業務經理提供了一個清晰的切入點,並為後續應用情境(例如乾預計劃和內部調動)建立了資料基礎。從這個意義上講,離職風險評分仍然是進入更廣泛的員工離職預測軟體市場的實用切入點,而不僅僅是眾多應用情境之一。預計到2031年,留任支持干預措施和指導性行動計畫的複合年成長率將達到11.92%,這表明買家越來越傾向於尋求可操作的建議,而不僅僅是觀察性的警告。

這一轉變意義重大,因為該領域正從預測轉向「引導式回應」。 2026年4月,Gloat將員工留存率提升建議整合到Microsoft 365 Copilot和Microsoft Teams中,使管理員能夠在熟悉的辦公室工具中回應風險訊號,而無需開啟單獨的應用程式。員工敬業度和情緒分析仍然至關重要,因為它可以在員工直接表明離職意向之前,提供早期背景信息,解釋離職風險高的原因。隨著雇主面臨審計壓力,需要就與薪資相關的留存問題提供合理的解釋,薪資和薪資差距分析也變得越來越重要。對於希望將留存、重新部署和技能策略整合到單一規劃框架中的大型企業而言,人才規劃和內部調動分析仍然至關重要。

區域分析

2025年,北美持續維持領先地位,佔據員工離職預測軟體市場37.22%的佔有率。該地區受益於高昂的員工離職成本、強大的供應商基礎以及習慣於透過正規軟體採購管道部署分析工具的企業買家。美國仍然是需求中心,這主要是因為美國雇主面臨高昂的員工更替成本,而且與許多歐洲國家相比,美國對員工資料的使用監管通常更為寬鬆。加拿大也在取得進展,但由於人們對隱私改革和演算法課責的預期,合規負擔日益加重,這可能會減緩軟體的普及。南美洲仍處於起步階段,巴西和智利是需求最明確的中心,但目前大部分需求僅限於跨國公司內部,這些公司將總部選定的平台部署到區域營運部門。

在歐洲,各項發展過程呈現不同的模式,法規、勞資談判、實施方案設計以及技術準備也各不相同,所有這些因素都將決定最終結果。德國、英國和法國仍是主要的收入來源,但在員工流動預測軟體市場,各國採取的採用路徑卻不盡相同。德國的情況尤其突出,由於共同決策規則的限制,員工代表委員會的參與延遲可能會延長實施週期,導致一些雇主選擇在匯總的職位層面而非個人層面建立模型。英國在國內採用略佔優勢,因為脫歐後的課責框架尚未完全反映歐盟的要求。

預計到2031年,亞太地區將以12.34%的複合年成長率成長,成為員工離職預測軟體市場成長最快的地區。印度受益於人力資源技術的日益普及以及雇主(尤其是全球產能中心企業)需求的成長,這些雇主希望將員工隊伍的穩定性轉化為永續的商業優勢。日本則另闢蹊徑,國內供應商和科技公司紛紛推出產品,以因應勞動力短缺和人才保留方面的挑戰。Canon電子於2026年3月推出了“員工離職風險診斷服務”,該服務利用PC操作日誌作為行為指標;Ginger也宣布將於2026年6月發布員工離職預警功能。儘管中國和韓國擁有龐大的市場規模,但有關在地化和資料管理的法規仍然使海外供應商難以進入這些市場,因為這些法規會影響產品架構和市場准入。中東地區,特別是阿拉伯聯合大公國和沙烏地阿拉伯,由於勞動力在地化和私營部門的轉型計劃,對人才保留分析的興趣和重視程度日益提高。非洲仍然是一個發展中地區,但南非、奈及利亞和埃及已經出現了早期採用徵兆,跨國公司和國內大型企業正在朝著人力資源流程數位化的方向發展。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 員工流動率過高和替代人員招募延遲導致成本增加。

- 擴展雲端原生人力資源分析與人力資本管理生態系。

- 擴大人工智慧和機器學習在員工離職風險評分的應用

- 需要將混合型人才視覺化並持續監控。

- 需要預測性保留訊號的基於技能的內部轉移計劃

- 財務長主導了對員工流動風險進行財務評估的需求。

- 市場限制因素

- 員工資料隱私與人工智慧管治合規性

- 資料孤島和傳統人力資源資訊系統整合的複雜性

- 工人代表和員工抗議數位化廢氣監測。

- GenAI產生的回饋雜訊會降低模型的準確性。

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章:預測市場規模與成長率

- 按組件

- 軟體

- 服務

- 實施和整合服務

- 諮詢和顧問服務

- 支援和維護服務

- 透過使用

- 員工離職預測與離職風險評分

- 針對員工留任的干預式和處以方式行動計劃

- 員工敬業度與情緒分析

- 人員規劃與內部調動分析

- 薪資、薪資差距與公平性分析

- 其他用途

- 部署模式

- 基於雲端的

- 現場

- 按組織規模

- 大公司

- 小型企業

- 按最終用戶行業分類

- IT/通訊

- 銀行、金融服務和保險業 (BFSI)

- 醫學與生命科學

- 零售與電子商務

- 製造業

- 政府/公共部門

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Visier, Inc.

- Eightfold AI Inc.

- Culture Amp Pty Ltd

- Perceptyx, Inc.

- One Model Inc.

- Degree, Inc. d/b/a Lattice

- ChartHop, Inc.

- Gloat Ltd.

- Leapsome GmbH

- 15Five, Inc.

- Hi Bob Limited

- Darwinbox Digital Solutions Private Limited

- PeopleStrong Technologies Private Limited

- WorkTango, Inc.

- Qualtrics, LLC

- Bamboo HR LLC

- Cornerstone OnDemand, Inc.

- Dayforce, Inc.

- UKG Inc.

- Paycom Payroll LLC

- Paylocity Corporation

- Career Engagement Group d/b/a Fuel50

第7章 市場機會與未來展望

According to Mordor Intelligence, the employee attrition prediction software market size is projected to be USD 1.12 billion in 2025, USD 1.24 billion in 2026, and reach USD 2.12 billion by 2031, growing at a CAGR of 11.28% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Application (Turnover Prediction and Flight-Risk Scoring, and More), Deployment Mode (Cloud-Based, and On-Premises), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), End-User Industry (Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Employee Attrition Prediction Software Market Trends and Insights

Rising Cost of Regrettable Attrition and Backfill Delays

Rising replacement costs have made the employee attrition prediction software market easier to justify at the business-unit level, as retention technology is now tied directly to avoidable labor expense. Turnover cost per worker reached USD 45,236 in 2026, up from USD 36,723 in 2025, and 50% of US companies expected voluntary separations to rise further in 2026. That shift matters because buyers are no longer treating attrition as a soft human resources issue; they are treating it as a cost-control problem with immediate budget consequences. Gloat reported that identifying high-flight-risk employees 6 weeks earlier than managers could do on their own helped retain 68% of flagged employees, while the intervention cost was USD 28,000 against USD 340,000 in replacement outlay, and total savings reached USD 4.8 million in one business unit. As more return cases enter procurement discussions, the employee attrition prediction software market is moving from optional pilot spending to mainstream workforce investment. The practical buying question is now less about whether a company needs predictive retention software and more about which platform best aligns with internal hiring costs, manager workflows, and intervention capacity.

Growing Use of AI and Machine Learning for Flight-Risk Scoring

The employee attrition prediction software market is also benefiting from the wider acceptance of machine learning as a credible way to identify departure risk before managers see visible warning signs. A clinical deployment by Lotis Blue showed that an ML model predicted healthcare worker turnover with 90% accuracy, and 45% of employees who later quit had received no proactive retention conversation. That result supports the view that predictive systems are gaining traction because they can expose silent risk pockets that manual review often misses. It also explains why buyers now expect more than dashboards, because basic reporting alone does not change outcomes unless it triggers action at the manager level. As adoption expands, the employee attrition prediction software market is likely to reward vendors that can keep models current when performance reviews, engagement inputs, and other people's data become noisier. This creates a secondary demand layer for recalibration, explainability, and data-quality controls, especially in enterprises that already use generative AI in HR processes.

Employee Data Privacy and AI Governance Compliance

Compliance pressure remains a major brake on the employee attrition prediction software market, as many employers must now treat it as a high-risk AI use case. Legal analysis of the EU AI Act noted that Annex III obligations on transparency, human oversight, and bias testing apply to workforce tools that assess or influence employee behavior, and that planning requirements are already in effect, even after the compliance timeline was extended. This means product deployment is no longer a pure technology exercise, as legal review, documentation, governance design, and audit readiness are now part of the same project. GDPR enforcement also kept pressure high, with reporting in 2025 showing that cumulative penalties moved past EUR 5 billion (USD 5.4 billion) for the first time. The effect on the employee attrition prediction software market is evident in longer sales cycles and a higher first-year deployment burden, especially in Europe and in jurisdictions with similar accountability rules. Vendors that cannot show clear consent logic, human review pathways, and bias controls face slower conversion even when the product itself is technically strong.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Cloud-Native HR Analytics and HCM Ecosystems

- CFO-Led Demand to Quantify Attrition Risk in Dollar Terms

- Data Silos and Legacy HRIS Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are projected to grow at a 12.91% CAGR through 2031, making them the fastest-growing segment of the employee attrition prediction software market,, even though software remained the core revenue base in 2025. Software still anchors most commercial value because it houses the prediction engine, data model, workflow logic, and reporting interface that buyers license first. That base position keeps software central to every major deal, especially in large organizations that want broad retention visibility across regions and business units. At the same time, the employee attrition prediction software industry is moving toward more complex deployments that depend on configuration, onboarding, and cross-functional rollout support. This is why services are expanding faster, because many buyers now need help translating model output into manager actions, policy changes, and ongoing governance routines.

Implementation and integration work have become more important as the employee attrition prediction software market moves beyond simple dashboard deployment into embedded operational use. Vendors are spending more time on connector setup, intervention design, alert calibration, and manager adoption because those steps now affect realized value as much as model accuracy does. Service teams also help reduce customer churn, since accounts that rely on a vendor for process redesign and change support are less likely to treat the platform as replaceable. This gives vendors a stronger long-term relationship and makes services a practical retention tool for both the supplier and the buyer. The same trend is raising the importance of certified partner networks, because buyers want implementation resources that already understand major HCM stacks and enterprise governance requirements.

Turnover prediction and flight-risk scoring accounted for 36.71% of revenue in 2025, keeping this use case at the center of the employee attrition prediction software market. Most enterprises still start here because flight-risk scoring is the clearest way to show immediate value from people data. It provides HR teams and line managers with a clear entry point and lays the data foundation for later use cases, such as intervention planning or internal mobility targeting. In that sense, flight-risk scoring remains the operational gateway to the broader employee attrition prediction software market rather than a single use case among many. Retention intervention and prescriptive action planning are expected to grow at a 11.92% CAGR through 2031, indicating that buyers increasingly want recommendations tied to action, not just flags tied to observation.

This shift matters because the category is moving from prediction toward guided response. Gloat integrated retention recommendations into Microsoft 365 Copilot and Microsoft Teams in April 2026, which let managers respond to risk signals inside familiar work tools instead of opening a separate application. Employee engagement and sentiment analytics still play an important role because they provide early context that helps explain why flight risk is rising before an employee signals intent directly. Compensation and pay equity analytics are also becoming more relevant where employers face audit pressure and need a defensible view of pay-linked retention issues. Workforce planning and internal mobility analytics remain important for large enterprises that want to connect retention, redeployment, and skills strategy within a single planning framework.

Geography Analysis

North America held 37.22% of the employee attrition prediction software market share in 2025, maintaining its lead. The region benefits from high per-worker turnover costs, a dense vendor base, and enterprise buyers accustomed to adopting analytics tools through formal software procurement channels. The United States remains the center of demand because employers there face high replacement costs and generally operate under more permissive employee data-use practices than many of their European peers. Canada is also progressing, though privacy reform and algorithmic accountability expectations are adding a layer of compliance work that can delay deployment. South America remained at an earlier stage, with Brazil and Chile representing the clearest demand pockets, mostly within multinational organizations extending centrally selected platforms into regional operations.

Europe develops through a different pattern because regulation, labor consultation, and deployment design shape outcomes as much as technology readiness. Germany, the United Kingdom, and France remain the main revenue anchors, but each follows a different adoption path inside the employee attrition prediction software market. Germany stands out because co-determination rules can stretch deployment timelines when works councils are engaged late, and some employers have responded by building models at an aggregated grade level rather than at the individual level. The United Kingdom keeps a modest timing advantage in domestic adoption because its post-Brexit accountability framework does not mirror every EU requirement in the same way.

Asia-Pacific is projected to grow at a 12.34% CAGR through 2031, making it the fastest-growing region in the employee attrition prediction software market. India is benefiting from wider HR technology formalization and from employer demand to turn workforce stability into a sustained operating advantage, especially in global capability center environments. Japan is taking a distinct path, with domestic vendors and technology firms launching products that address labor scarcity and retention pressures. Canon Electronics launched its Retirement Risk Diagnosis Service in March 2026 using PC operation logs as behavioral indicators, and Jinjer announced an attrition alert function scheduled for launch in June 2026. China and South Korea offer scale but remain more challenging for foreign vendors because localization and data control rules shape product architecture and market access. The Middle East is becoming more relevant, led by the UAE and Saudi Arabia, as workforce nationalization and private-sector transformation programs raise interest in retention analytics. Africa is still nascent, but South Africa, Nigeria, and Egypt are showing early signs of adoption as HR digitalization deepens across multinational and larger domestic employers.

- Visier, Inc.

- Eightfold AI Inc.

- Culture Amp Pty Ltd

- Perceptyx, Inc.

- One Model Inc.

- Degree, Inc. d/b/a Lattice

- ChartHop, Inc.

- Gloat Ltd.

- Leapsome GmbH

- 15Five, Inc.

- Hi Bob Limited

- Darwinbox Digital Solutions Private Limited

- PeopleStrong Technologies Private Limited

- WorkTango, Inc.

- Qualtrics, LLC

- Bamboo HR LLC

- Cornerstone OnDemand, Inc.

- Dayforce, Inc.

- UKG Inc.

- Paycom Payroll LLC

- Paylocity Corporation

- Career Engagement Group d/b/a Fuel50

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Cost of Regrettable Attrition and Backfill Delays

- 4.2.2 Expansion of Cloud-Native HR Analytics and HCM Ecosystems

- 4.2.3 Growing Use of AI and Machine Learning for Flight-Risk Scoring

- 4.2.4 Need for Hybrid Workforce Visibility and Continuous Listening

- 4.2.5 Skills-Based Internal Mobility Programs Requiring Predictive Retention Signals

- 4.2.6 CFO-Led Demand to Quantify Attrition Risk in Dollar Terms

- 4.3 Market Restraints

- 4.3.1 Employee Data Privacy and AI Governance Compliance

- 4.3.2 Data Silos and Legacy HRIS Integration Complexity

- 4.3.3 Works Council and Employee Pushback on Digital Exhaust Monitoring

- 4.3.4 GenAI-Generated Feedback Noise Weakening Model Precision

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration Services

- 5.1.2.2 Consulting and Advisory Services

- 5.1.2.3 Support and Maintenance Services

- 5.2 By Application

- 5.2.1 Turnover Prediction and Flight-Risk Scoring

- 5.2.2 Retention Intervention and Prescriptive Action Planning

- 5.2.3 Employee Engagement and Sentiment Analytics

- 5.2.4 Workforce Planning and Internal Mobility Analytics

- 5.2.5 Compensation, Pay Equity, and Fairness Analytics

- 5.2.6 Other Applications

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-Sized Enterprises

- 5.5 By End-User Industry

- 5.5.1 Information Technology and Telecommunications

- 5.5.2 Banking, Financial Services, and Insurance

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Retail and E-Commerce

- 5.5.5 Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Egypt

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Visier, Inc.

- 6.4.2 Eightfold AI Inc.

- 6.4.3 Culture Amp Pty Ltd

- 6.4.4 Perceptyx, Inc.

- 6.4.5 One Model Inc.

- 6.4.6 Degree, Inc. d/b/a Lattice

- 6.4.7 ChartHop, Inc.

- 6.4.8 Gloat Ltd.

- 6.4.9 Leapsome GmbH

- 6.4.10 15Five, Inc.

- 6.4.11 Hi Bob Limited

- 6.4.12 Darwinbox Digital Solutions Private Limited

- 6.4.13 PeopleStrong Technologies Private Limited

- 6.4.14 WorkTango, Inc.

- 6.4.15 Qualtrics, LLC

- 6.4.16 Bamboo HR LLC

- 6.4.17 Cornerstone OnDemand, Inc.

- 6.4.18 Dayforce, Inc.

- 6.4.19 UKG Inc.

- 6.4.20 Paycom Payroll LLC

- 6.4.21 Paylocity Corporation

- 6.4.22 Career Engagement Group d/b/a Fuel50

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

增強型分析市場:組件、技術、部署模式、最終用戶、應用與最終用途-2026-2032年全球市場預測

增強型分析市場:組件、技術、部署模式、最終用戶、應用與最終用途-2026-2032年全球市場預測 增強型分析市場預測至 2034 年—按組件、部署類型、企業規模、技術、應用、最終用戶和地區分類的全球分析超自動化軟體平台市場預測至2034年-按組件、開發模式、企業規模、部門、技術、最終用戶和地區分類的全球分析

增強型分析市場預測至 2034 年—按組件、部署類型、企業規模、技術、應用、最終用戶和地區分類的全球分析超自動化軟體平台市場預測至2034年-按組件、開發模式、企業規模、部門、技術、最終用戶和地區分類的全球分析 增強型分析市場規模、佔有率、趨勢和預測:按組件、部署模式、企業規模、行業和地區分類,2026-2034 年

增強型分析市場規模、佔有率、趨勢和預測:按組件、部署模式、企業規模、行業和地區分類,2026-2034 年 2026年銀行業、金融服務業和保險業(BFSI)擴展分析全球市場報告2026年全球擴展分析市場報告2026年全球創作者薪酬分析市場報告

2026年銀行業、金融服務業和保險業(BFSI)擴展分析全球市場報告2026年全球擴展分析市場報告2026年全球創作者薪酬分析市場報告 增強型分析市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署類型、最終用戶及功能分類

增強型分析市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、部署類型、最終用戶及功能分類 增強型分析市場 - 全球產業規模、佔有率、趨勢、機會及預測(按部署方式、組織規模、最終用戶、地區和競爭格局分類,2021-2031 年)

增強型分析市場 - 全球產業規模、佔有率、趨勢、機會及預測(按部署方式、組織規模、最終用戶、地區和競爭格局分類,2021-2031 年) 增強分析市場規模、佔有率和成長分析(按組件、公司規模、部署類型、垂直產業和地區分類)-2026-2033年產業預測

增強分析市場規模、佔有率和成長分析(按組件、公司規模、部署類型、垂直產業和地區分類)-2026-2033年產業預測