|

市場調查報告書

商品編碼

2064508

美國滅菌設備:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)U.S. Sterilization Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

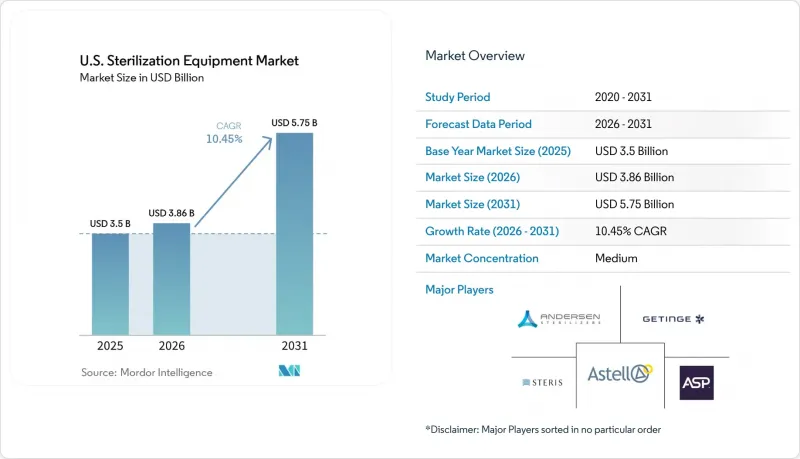

據 Mordor Intelligence 稱,2025 年美國滅菌設備市場價值為 35 億美元,預計到 2031 年將從 2026 年的 38.6 億美元成長至 57.5 億美元,預測期(2026-2031 年)複合年成長率為 10.45%。

本報告按設備類型(高溫、低溫、過濾、電離輻射)、最終用戶(醫院、門診手術中心、專科診所、製藥和生物製藥公司、醫療設備製造商和合約研發生產機構、其他)、應用領域(手術器械再處理、內視鏡再處理、熱敏醫療設備、最終滅菌、無菌處理、實驗室廢棄物)以及實驗室廢棄物進行分類。預測值以美元(USD)計價。

美國滅菌設備市場趨勢與洞察

手術數量的增加和器械複雜性的提高,正在重新定義消毒能力的要求。

由於住院和門診手術的數量和複雜程度不斷增加,美國消毒設備市場正在改變。美國醫院協會 (AHA) 報告稱,到 2025 年,與疫情前相比,2024 年初接受手術的住院患者的生存率將提高 20%,這反映了更嚴格的消毒流程。重症病例需要使用機械臂和多腔器械等先進設備,這些設備對消毒流程的再處理要求更高,耗時更長。此外,預計 2025 年門診病人就診量將增加 9.8%,這將增加器械周轉率,從而推動對高容量設備和高效工作流程的需求,以最佳化空間利用和處理時間。

加強醫院感染預防和消毒流程標準化將有助於基礎投資。

在美國,感染防控要求持續推動對滅菌設備的需求。儘管美國疾病管制與預防中心(CDC)的數據顯示,急性護理醫院的醫療相關感染病例預計將從2023年的132,913例下降到2024年的123,204例,但持續投資的必要性依然凸顯。醫院必須維持更高的感染控制水平,因此需要更加重視監測、驗證和審核準備。美國醫療器材促進協會(AAMI)2025年更新的指南提高了化學滅菌和環氧乙烷(EtO)滅菌的標準,使得在品質審查中更難證明過時系統的合理性,從而刺激了設備升級的需求。

高額資本投資、驗證和公用設施維修。

對於資金預算有限的醫療機構而言,雖然先進的滅菌平台必不可少,但高昂的實施成本仍是一大挑戰。大容量低溫滅菌系統和自動化中央消毒供應室(CSSD)生產線通常需要大規模的驗證、安裝維修和公用設施升級,推高了整體成本。區域性醫院和獨立門診手術中心(ASC)也面臨額外的負擔,例如漫長的重新驗證、員工再培訓和工作流程重新設計。

細分市場分析

2025年,高溫滅菌仍維持其最大市場佔有率,佔據美國滅菌設備市場48.45%的佔有率。由於蒸氣系統具有擴充性和易於整合到中央滅菌流程中,因此仍是耐熱器械、預包裝物品和大批量手術托盤的首選滅菌方式。然而,隨著越來越多的器械包含無法透過傳統蒸氣循環處理的零件,高溫滅菌的成長速度趨於穩定,而非加速。

低溫滅菌是成長最快的細分市場,預計到2031年,美國市場的複合年成長率將達到11.28%。這一成長主要得益於機器人手術器械、軟性內視鏡和熱敏設備等需要檢驗的處理方法的設備的日益普及。 Getinge公司計劃於2026年推出Poladus 150 VHP滅菌器,以擴展其GSS67N蒸氣滅菌平台的處理能力,這反映了該公司在滿足處理能力和空間效率方面的需求方面所做的努力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 手術數量的增加和醫療設備。

- 醫院內部感染控制和再處理合規性的徹底性

- ASC的擴張和對小型滅菌器的需求

- 過渡到環氧乙烷將有助於實現更低溫度的升級。

- 對中央供應室自動化和可追溯性的投資

- 市場限制因素

- 高昂的初始成本、檢驗和公用設施維修負擔

- ETO授權和合規性所帶來的停機風險。

- 透過改用一次性產品來減輕醫院內再處理工作的負擔。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過裝置

- 高溫滅菌

- 濕式/蒸氣滅菌

- 乾熱滅菌

- 低溫滅菌

- 環氧乙烷(ETO)

- 過氧化氫等離子體

- 臭氧

- 其他低溫滅菌方法

- 過濾滅菌

- 電離放射線殺菌

- 電子束

- 伽瑪射線

- 其他電離輻射技術

- 高溫滅菌

- 最終用戶

- 醫院和診所

- 門診手術中心

- 專科診所和醫療實踐型醫療保健

- 製藥和生物製藥製造商

- 醫療設備製造商和合約研發生產機構

- 其他

- 透過使用

- 手術器械的再處理

- 軟式內視鏡的再處理與滅菌

- 熱敏醫療設備的滅菌

- 成品醫療設備的最終滅菌

- 無菌加工支援和無菌運輸

- 生物危害物、培養基及實驗室廢棄物的滅菌

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Advanced Sterilization Products, Inc.

- Andersen Products, LLC

- Astell Scientific Ltd

- BMM Weston Ltd

- BMT USA, LLC

- Cisa Group

- Consolidated Sterilizer Systems

- De Lama SpA

- Fedegari Autoclavi SpA

- Getinge AB

- LTE Scientific Ltd

- MATACHANA Group

- MMM Group

- Noxilizer, Inc.

- Priorclave North America

- SteelcoBelimed

- Steriflow

- STERIS plc

- Systec GmbH & Co. KG

- Tuttnauer

第7章 市場機會與未來展望

According to Mordor Intelligence, the u.S. sterilization equipment market size was valued at USD 3.5 billion in 2025 and is estimated to grow from USD 3.86 billion in 2026 to reach USD 5.75 billion by 2031, at a CAGR of 10.45% during the forecast period (2026-2031).

This report is Segmented by Equipment (High-Temp, Low-Temp, Filtration, Ionizing Radiation), End User (Hospitals, Ascs, Specialty Clinics, Pharma/Biopharma, Device Manufacturers and CDMOs, Others), Application (Surgical Instrument Reprocessing, Endoscope Reprocessing, Heat-Sensitive Device, Terminal Sterilization, Aseptic Processing, Lab Waste), and Geography (United States). Forecasts in Value (USD).

U.S. Sterilization Equipment Market Trends and Insights

Rising Procedure Volumes and Instrument Complexity Redefine Sterilization Throughput Requirements

The United States sterilization equipment market is evolving due to increasing surgical volumes and complexity in inpatient and outpatient settings. In 2025, the American Hospital Association reported a 20% higher survival rate for hospitalized surgical patients in early 2024 compared to pre-pandemic benchmarks, reflecting stricter sterility protocols. Higher acuity cases now require advanced instruments like robotic arms and multi-lumen devices, which demand more time and precision for reprocessing. Additionally, a 9.8% rise in outpatient visits in 2025 has increased instrument turnover, driving demand for high-throughput equipment and efficient workflows to optimize space and turnaround times.

HAI Prevention and Reprocessing Compliance Intensity Sustain Baseline Investment

Infection prevention requirements continue to sustain demand for sterilization equipment in the United States. CDC data showed healthcare-associated infections in acute care hospitals dropped from 132,913 in 2023 to 123,204 in 2024, indicating progress but highlighting the need for ongoing investment. Hospitals must maintain improved infection outcomes, increasing the focus on monitoring, validation, and audit readiness. Updated AAMI guidance in 2025 raised standards for chemical and EtO sterilization, making outdated systems harder to justify during quality reviews and driving replacement demand.

High Capital, Validation, and Utility Retrofit Burden

High acquisition costs remain a significant challenge for providers requiring advanced sterilization platforms but operating with limited capital budgets. Large capacity low-temperature systems and automated CSSD lines often necessitate extensive validation, installation modifications, and utility upgrades, adding to the overall expense. Community hospitals and independent ASCs face additional burdens, such as prolonged revalidation, staff retraining, and workflow redesign.

Other drivers and restraints analyzed in the detailed report include:

- ASC Expansion and Compact Sterilizer Demand Reshape Market Geography

- EtO Transition Driving Low-Temperature Equipment Upgrades

- EtO Permitting and Compliance-Driven Downtime Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, high-temperature sterilization held a 48.45% share of the United States sterilization equipment market, maintaining its position as the largest segment. Steam systems remained the preferred choice for heat-tolerant instruments, wrapped goods, and large surgical tray volumes due to their scalability and integration into central sterile workflows. However, their growth is steady rather than accelerating, as more instruments now include components incompatible with traditional steam cycles.

Low-temperature sterilization is the fastest-growing segment, projected to expand at an 11.28% CAGR through 2031 in the United States market. This growth is driven by the increasing use of robotic instruments, flexible scopes, and heat-sensitive devices requiring validated processing. Getinge's introduction of the Poladus 150 VHP sterilizer and the expanded capacity of its GSS67N steam platform in 2026 reflect a shift toward addressing throughput and space efficiency needs.

List of Companies Covered in this Report:

- Advanced Sterilization Products, Inc.

- Andersen Products, LLC

- Astell Scientific Ltd

- BMM Weston

- BMT USA, LLC

- Cisa Group

- Consolidated Sterilizer Systems

- De Lama S.p.A.

- Fedegari Autoclavi

- Getinge

- LTE Scientific Ltd

- MATACHANA Group

- MMM Group

- Noxilizer

- Priorclave North America

- SteelcoBelimed

- Steriflow

- STERIS

- Systec GmbH & Co. KG

- Tuttnauer

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Procedure Volumes and Instrument Complexity

- 4.2.2 HAI Prevention and Reprocessing Compliance Intensity

- 4.2.3 ASC Expansion and Compact Sterilizer Demand

- 4.2.4 Eto Transition Driving Low-Temperature Upgrades

- 4.2.5 CSSD Automation and Traceability Investments

- 4.3 Market Restraints

- 4.3.1 High Capital, Validation, and Utility Retrofit Burden

- 4.3.2 Eto Permitting and Compliance-Driven Downtime Risk

- 4.3.3 Single-Use Substitution Reducing In-House Reprocessing Load

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining power of suppliers

- 4.7.2 Bargaining power of buyers

- 4.7.3 Threat of new entrants

- 4.7.4 Threat of substitutes

- 4.7.5 Intensity of rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Equipment

- 5.1.1 High-temperature Sterilization

- 5.1.1.1 Wet/Steam Sterilization

- 5.1.1.2 Dry Heat Sterilization

- 5.1.2 Low-temperature Sterilization

- 5.1.2.1 Ethylene Oxide (ETO)

- 5.1.2.2 Hydrogen Peroxide Plasma

- 5.1.2.3 Ozone

- 5.1.2.4 Other Low-temperature Methods

- 5.1.3 Filtration Sterilization

- 5.1.4 Ionizing Radiation Sterilization

- 5.1.4.1 E-beam

- 5.1.4.2 Gamma

- 5.1.4.3 Other Ionizing Technologies

- 5.1.1 High-temperature Sterilization

- 5.2 By End User

- 5.2.1 Hospitals and Clinics

- 5.2.2 Ambulatory Surgery Centers

- 5.2.3 Specialty Clinics And Office-Based Care

- 5.2.4 Pharmaceutical And Biopharmaceutical Manufacturers

- 5.2.5 Medical Device Manufacturers And CDMOs

- 5.2.6 Others

- 5.3 By Application

- 5.3.1 Surgical Instrument Reprocessing

- 5.3.2 Flexible Endoscope Reprocessing And Sterilization

- 5.3.3 Heat-Sensitive Device Sterilization

- 5.3.4 Terminal Sterilization Of Finished Medical Devices

- 5.3.5 Aseptic Processing Support And Sterile Transfer

- 5.3.6 Biohazard, Media, And Lab Waste Sterilization

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Advanced Sterilization Products, Inc.

- 6.3.2 Andersen Products, LLC

- 6.3.3 Astell Scientific Ltd

- 6.3.4 BMM Weston Ltd

- 6.3.5 BMT USA, LLC

- 6.3.6 Cisa Group

- 6.3.7 Consolidated Sterilizer Systems

- 6.3.8 De Lama S.p.A.

- 6.3.9 Fedegari Autoclavi S.p.A.

- 6.3.10 Getinge AB

- 6.3.11 LTE Scientific Ltd

- 6.3.12 MATACHANA Group

- 6.3.13 MMM Group

- 6.3.14 Noxilizer, Inc.

- 6.3.15 Priorclave North America

- 6.3.16 SteelcoBelimed

- 6.3.17 Steriflow

- 6.3.18 STERIS plc

- 6.3.19 Systec GmbH & Co. KG

- 6.3.20 Tuttnauer

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

滅菌設備市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。

滅菌設備市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。 滅菌設備市場:2026-2032年全球市場預測(依滅菌技術、產品類型、應用、最終用戶及通路分類)環氧乙烷滅菌設備市場:依設備類型、滅菌能力、應用及最終用戶分類-2026-2032年全球市場預測

滅菌設備市場:2026-2032年全球市場預測(依滅菌技術、產品類型、應用、最終用戶及通路分類)環氧乙烷滅菌設備市場:依設備類型、滅菌能力、應用及最終用戶分類-2026-2032年全球市場預測 滅菌設備市場規模、佔有率、趨勢和預測:按產品、最終用戶和地區分類,2026-2034年

滅菌設備市場規模、佔有率、趨勢和預測:按產品、最終用戶和地區分類,2026-2034年 全球滅菌設備市場:依產品、技術和地區分類-預測(至2031年)

全球滅菌設備市場:依產品、技術和地區分類-預測(至2031年) 2026年全球滅菌設備和消毒劑市場報告2026年全球滅菌設備市場報告

2026年全球滅菌設備和消毒劑市場報告2026年全球滅菌設備市場報告 全球滅菌設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本滅菌設備市場報告:按產品、最終用戶和地區分類(2026-2034年)全球滅菌設備市場:市場規模、佔有率、成長率、產業分析、按類型、應用和地區劃分的考量因素以及未來預測(2026-2034)

全球滅菌設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本滅菌設備市場報告:按產品、最終用戶和地區分類(2026-2034年)全球滅菌設備市場:市場規模、佔有率、成長率、產業分析、按類型、應用和地區劃分的考量因素以及未來預測(2026-2034)