|

市場調查報告書

商品編碼

2061441

滅菌設備市場:商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。Sterilization Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

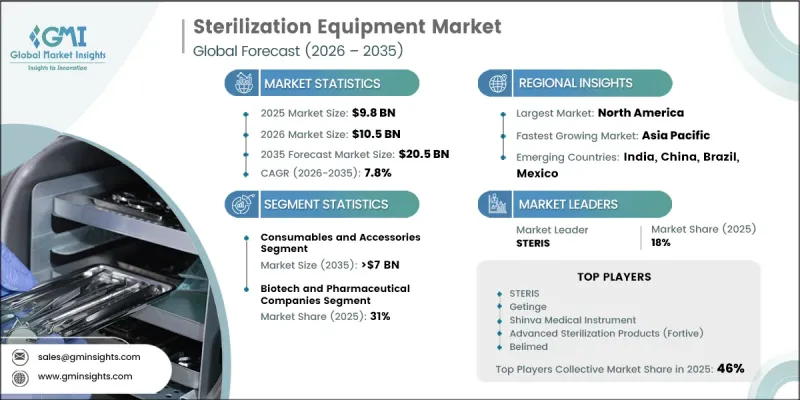

2025年全球滅菌設備市場價值為98億美元,預計2035年將以7.8%的複合年成長率成長至205億美元。

強勁的市場成長主要受以下因素驅動:醫療相關感染的增加、對先進感染預防技術日益成長的需求,以及全球製藥和生物技術製造活動的擴張。外科手術數量的增加和對無菌保證更嚴格的監管要求也顯著促進了該行業的擴張。感染控制在醫療機構中日益受到重視,旨在提高病患安全、減少治療相關併發症並最大限度地降低與醫院感染相關的醫療成本。人們對污染預防和滅菌合規性的認知不斷提高,正在加速醫院、實驗室和醫療機構採用先進的滅菌系統。此外,生物技術和生物製藥產業的快速發展也催生了對高效滅菌技術的巨大需求,這些技術對於維持無污染的生產環境至關重要。自動化滅菌系統的技術進步、低溫滅菌技術的日益普及,以及醫療和工業應用領域對環保和永續滅菌解決方案日益成長的需求,也都在推動市場成長。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 98億美元 |

| 預測金額 | 205億美元 |

| 複合年成長率 | 7.8% |

門診診所和日間手術中心的擴張進一步推動了消毒設備市場的發展,這些機構需要高效的消毒流程來維持營運安全標準。醫療保健投資的增加和醫療基礎設施的持續現代化正在推動已開發市場和新興市場採用先進的消毒技術。隨著對感染預防規程和品質保證措施的日益重視,全球對可靠的消毒設備及相關耗材的需求持續成長。

預計2025年,耗材及配件市場佔有率將達34.9%,2035年將達70億美元,年複合成長率(CAGR)為7.6%。耗材及配件是業界至關重要的組成部分,因為它們在滅菌程序和合規流程中反覆使用。此類別涵蓋旨在支援滅菌驗證、包裝、監測和感染控制措施的產品。對維持嚴格的監管標準和確保有效滅菌效果的日益重視,推動了醫療保健和工業領域對高品質耗材及配件的持續需求。

預計到2025年,生技和製藥公司將佔市場佔有率的31%,到2035年將達到67億美元。生技和製藥公司高度依賴滅菌技術,以在其製藥生產和研發活動的整體維持無菌生產環境。在整個製藥生產過程中,無菌操作至關重要,以確保產品安全、品質和符合法規要求。對生物製藥生產、注射療法和先進藥物研發活動的投資不斷增加,進一步推動了該領域對先進滅菌系統的需求。

預計到2025年,北美滅菌設備市佔率將達到35.8%。該地區憑藉其先進的醫療基礎設施、高度的感染控制意識以及技術先進的滅菌系統的廣泛應用,持續保持著強勁的市場地位。醫療相關感染率的上升和外科手術量的增加,顯著推動了全部區域對高效滅菌解決方案的需求。此外,嚴格的滅菌驗證和病人安全監管標準也促使醫療機構採用先進的自動化和低溫滅菌技術。持續的創新和主要市場參與企業的強大實力也支撐著北美市場的持續成長。

目錄

第1章:調查方法

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 影響產業的因素

- 促進因素

- 醫療相關感染發生率增加

- 手術數量增加

- 擴大製藥和生物技術製造

- 嚴格的監管要求以確保無菌

- 產業潛在風險與挑戰

- 先進醫療設備的消毒

- 化學消毒劑的有害影響

- 市場機遇

- 採用低溫和替代滅菌方法

- 人工智慧和物聯網整合用於智慧消毒

- 促進因素

- 成長潛力分析

- 監理情勢

- 技術展望

- 最新科技趨勢

- 新興技術

- 未來市場趨勢

- 波特的分析

- PESTLE分析

- 價格趨勢分析

- 滅菌服務展望

- 人工智慧和生成式人工智慧對市場的影響

- 投資與資金籌措分析

- 差距分析

第4章 競爭情勢

- 介紹

- 企業矩陣分析

- 企業市佔率分析

- 世界

- 北美洲

- 歐洲

- 亞太地區

- 競爭定位矩陣

- 主要市場公司的競爭分析

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估價與預測:依產品分類,2022-2035年

- 熱力消毒器

- 濕熱滅菌器

- 乾熱滅菌器

- 低溫滅菌器

- 環氧乙烷滅菌器

- 過氧化氫消毒裝置

- 其他低溫滅菌設備

- 無菌膜過濾器

- 放射線殺菌

- 電子束

- 伽瑪射線

- 其他放射線殺菌設備

- 耗材和配件

第6章 市場估算與預測:依最終用途分類,2022-2035年

- 醫院和診所

- 生物技術和製藥公司

- 醫療設備製造商

- 食品飲料業

- 其他最終用戶

第7章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第8章:公司簡介

- 3M Company

- Advanced Sterilization Products(Fortive)

- Anderson Products

- Belimed

- Cardinal Health

- Getinge

- Matachana Group

- Melag

- Merck

- MMM Group

- Shinva Medical Instrument

- STERIS

- Stryker

- Systec

- Tuttnauer

The Global Sterilization Equipment Market was valued at USD 9.8 billion in 2025 and is estimated to grow at a CAGR of 7.8% to reach USD 20.5 billion by 2035.

Strong market growth is being driven by the increasing prevalence of healthcare-associated infections, rising demand for advanced infection prevention technologies, and expanding pharmaceutical and biotechnology manufacturing activities worldwide. The growing volume of surgical procedures and stricter regulatory requirements related to sterility assurance are also contributing significantly to industry expansion. Healthcare facilities are increasingly prioritizing infection control measures to improve patient safety, reduce treatment complications, and minimize healthcare costs associated with hospital-acquired infections. Rising awareness regarding contamination prevention and sterilization compliance is accelerating the adoption of advanced sterilization systems across hospitals, laboratories, and healthcare facilities. In addition, rapid growth in the biotechnology and biopharmaceutical sectors is creating substantial demand for highly efficient sterilization technologies required to maintain contamination-free manufacturing environments. The market is also benefiting from technological advancements in automated sterilization systems, increasing adoption of low-temperature sterilization methods, and growing demand for environmentally sustainable sterilization solutions across healthcare and industrial applications.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.8 Billion |

| Forecast Value | $20.5 Billion |

| CAGR | 7.8% |

The sterilization equipment market is further supported by the expansion of outpatient healthcare facilities and ambulatory surgical centers that require efficient sterilization processes to maintain operational safety standards. Increasing healthcare investments and ongoing modernization of healthcare infrastructure are encouraging the adoption of advanced sterilization technologies across developed and emerging markets. Growing emphasis on infection prevention protocols and quality assurance practices continues to strengthen demand for reliable sterilization equipment and related consumable products worldwide.

The consumables and accessories segment accounted for 34.9% share in 2025 and is expected to reach USD 7 billion by 2035, growing at a CAGR of 7.6%. Consumables and accessories represent a critical segment within the industry due to their recurring usage across sterilization procedures and compliance processes. This category includes products designed to support sterilization validation, packaging, monitoring, and infection prevention practices. Rising focus on maintaining strict regulatory standards and ensuring effective sterilization outcomes is driving sustained demand for high-quality consumables and accessories across healthcare and industrial environments.

The biotech and pharmaceutical companies segment held a share of 31% in 2025 and is projected to reach USD 6.7 billion by 2035. Biotechnology and pharmaceutical organizations rely extensively on sterilization technologies to maintain contamination-free production environments throughout drug manufacturing and research activities. Sterility remains essential for ensuring product safety, quality, and regulatory compliance across pharmaceutical production processes. Increasing investments in biologics manufacturing, injectable therapies, and advanced drug development activities are further strengthening demand for sophisticated sterilization systems within this segment.

North America Sterilization Equipment Market held a 35.8% share in 2025. The region continues to maintain a strong market position due to advanced healthcare infrastructure, high awareness regarding infection prevention practices, and widespread adoption of technologically advanced sterilization systems. Increasing incidence of healthcare-associated infections and growing surgical procedure volumes are driving substantial demand for effective sterilization solutions across healthcare facilities throughout the region. In addition, strict regulatory standards related to sterilization validation and patient safety are encouraging healthcare providers to adopt advanced automated and low-temperature sterilization technologies. Continuous innovation and the strong presence of leading market participants are also supporting sustained market growth across North America.

Major companies operating in the Global Sterilization Equipment Market include 3M Company, Advanced Sterilization Products (Fortive), Anderson Products, Belimed, Cardinal Health, Getinge, Matachana Group, Melag, Merck, MMM Group, Shinva Medical Instrument, STERIS, Stryker, Systec, and Tuttnauer. Companies operating in the sterilization equipment market are adopting multiple strategic initiatives to strengthen their market presence and improve competitive positioning globally. Leading industry participants are investing heavily in research and development activities to introduce advanced sterilization technologies with improved automation, efficiency, and environmental sustainability. Strategic acquisitions, partnerships, and collaborations are helping companies expand product portfolios and strengthen distribution networks across international markets. Organizations are also focusing on developing low-temperature and eco-friendly sterilization systems to meet evolving regulatory and environmental requirements. Increasing investments in digital monitoring technologies, integrated sterilization tracking systems, and infection control solutions are further supporting innovation strategies. In addition, companies are expanding manufacturing capabilities, enhancing after-sales service networks, and strengthening relationships with healthcare providers to improve customer retention and reinforce their foothold within the global sterilization equipment industry.

Table of Contents

Chapter 1 Research Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of healthcare-associated infections

- 3.2.1.2 Increasing number of surgical procedures

- 3.2.1.3 Growing pharmaceutical and biotechnology manufacturing

- 3.2.1.4 Stringent regulatory requirements for sterility assurance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Sterilization of advanced medical instruments

- 3.2.2.2 Adverse effects of chemical disinfectants

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of low-temperature and alternative sterilization methods

- 3.2.3.2 AI and IoT integration for smart sterilization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape (Driven by primary research)

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends (Driven by primary research)

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing trend analysis (Driven by primary research)

- 3.10 Sterilization services outlook

- 3.11 Impact of AI & generative AI on the market

- 3.12 Investment & funding analysis

- 3.13 Gap analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis (Driven by primary research)

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Heat sterilizers

- 5.2.1 Moist heat sterilizers

- 5.2.2 Dry heat sterilizers

- 5.3 Low-temperature sterilizers

- 5.3.1 Ethylene oxide sterilizers

- 5.3.2 Hydrogen peroxide sterilizers

- 5.3.3 Other low-temperature sterilizers

- 5.4 Sterile membrane filters

- 5.5 Radiation sterilization devices

- 5.5.1 Electron beams

- 5.5.2 Gamma rays

- 5.5.3 Other radiation sterilization devices

- 5.6 Consumables and accessories

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals and clinics

- 6.3 Biotech and pharmaceutical companies

- 6.4 Medical device companies

- 6.5 Food and beverage industry

- 6.6 Other end users

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 3M Company

- 8.2 Advanced Sterilization Products (Fortive)

- 8.3 Anderson Products

- 8.4 Belimed

- 8.5 Cardinal Health

- 8.6 Getinge

- 8.7 Matachana Group

- 8.8 Melag

- 8.9 Merck

- 8.10 MMM Group

- 8.11 Shinva Medical Instrument

- 8.12 STERIS

- 8.13 Stryker

- 8.14 Systec

- 8.15 Tuttnauer

美國滅菌設備:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

美國滅菌設備:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 滅菌設備市場:2026-2032年全球市場預測(依滅菌技術、產品類型、應用、最終用戶及通路分類)環氧乙烷滅菌設備市場:依設備類型、滅菌能力、應用及最終用戶分類-2026-2032年全球市場預測

滅菌設備市場:2026-2032年全球市場預測(依滅菌技術、產品類型、應用、最終用戶及通路分類)環氧乙烷滅菌設備市場:依設備類型、滅菌能力、應用及最終用戶分類-2026-2032年全球市場預測 滅菌設備市場規模、佔有率、趨勢和預測:按產品、最終用戶和地區分類,2026-2034年

滅菌設備市場規模、佔有率、趨勢和預測:按產品、最終用戶和地區分類,2026-2034年 全球滅菌設備市場:依產品、技術和地區分類-預測(至2031年)

全球滅菌設備市場:依產品、技術和地區分類-預測(至2031年) 2026年全球滅菌設備和消毒劑市場報告2026年全球滅菌設備市場報告

2026年全球滅菌設備和消毒劑市場報告2026年全球滅菌設備市場報告 全球滅菌設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本滅菌設備市場報告:按產品、最終用戶和地區分類(2026-2034年)全球滅菌設備市場:市場規模、佔有率、成長率、產業分析、按類型、應用和地區劃分的考量因素以及未來預測(2026-2034)

全球滅菌設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)日本滅菌設備市場報告:按產品、最終用戶和地區分類(2026-2034年)全球滅菌設備市場:市場規模、佔有率、成長率、產業分析、按類型、應用和地區劃分的考量因素以及未來預測(2026-2034)