|

市場調查報告書

商品編碼

2064469

美國滅菌服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Sterilization Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

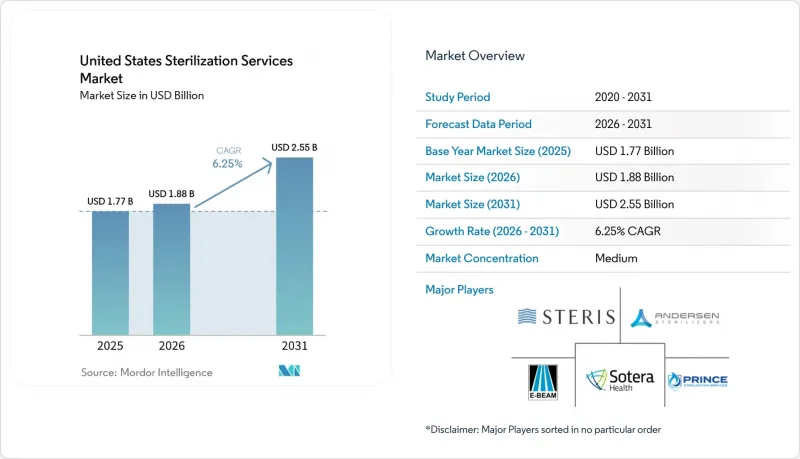

根據 Mordor Intelligence 預測,美國消毒服務市場規模將從 2025 年的 17.7 億美元和 2026 年的 18.8 億美元成長到 2031 年的 25.5 億美元,2026 年至 2031 年的複合年成長率為 6.25%。

本報告按滅菌方法(乙氧基化滅菌、伽馬射線輻照、電子束輻照等)、交付方式(異地、現場/內部服務)、服務類型(合約滅菌、驗證/測試等)以及最終用戶(醫療設備製造商、製藥/生物製藥公司、醫院/日間手術中心等)進行分類。市場預測以美元計價。

美國消毒服務市場的趨勢與見解。

醫院感染負擔加重,治療次數增加

醫療相關感染 (HAI) 持續引發人們對臨床環境中消毒表現的密切關注。根據美國疾病管制與預防中心 (CDC) 2023 年發布的國家和州級報告,醫療設備相關感染和手術相關感染控制仍然是急診機構面臨的關鍵問題。由於越來越多的手術在門診診所進行,這些診所需要達到醫院級別的消毒標準,但又缺乏完善的內部先進基礎設施,因此,這種壓力對美國消毒服務市場產生了重大影響。高風險病例向門診手術中心的轉移,增加了對檢驗的處理流程、包裝完整性和運輸控制記錄的需求。許多中心空間有限,難以容納多功能設備,且對流程故障的接受度較低,因此,這種轉變推動了對異地服務的需求成長。因此,手術量增加和感染預防標準提高將同時促進美國消毒服務市場的發展,因為這兩方面都將促使客戶建立更正式的消毒夥伴關係關係。

醫療設備和製藥製造商的外包

QMSR(品質管理系統監管條例)提高了合規內部滅菌操作的營運成本,並使供應商在檢查期間的監管更加透明,從而導致市場外包趨勢日益成長。根據RAPS(風險評估和採購服務)的報告,在2026年5月之前完成的100多項QMSR檢查中,外包和採購管理是第二大常見的QMSR違規行為,這表明FDA對供應商管理的審查非常嚴格。 ISO 13485:2016標準第4.1.5節在實務上如今更具意義,因為外包流程需要基於風險的管理,而滅菌正是這項規則最典型的例子之一。大規模合約供應商在此框架下具有優勢,因為它們可以提供文件化的品質系統、驗證記錄和隨時可供審核的可追溯性作為其服務的一部分。因此,美國滅菌服務市場正朝著規模更大、多模態的平台以及長期外包合約的方向發展。

環氧乙烷(EtO)排放和合規性差異

儘管環氧乙烷 (EtO) 對許多熱敏產品仍然至關重要,但由於排放相關的法規結構快速變化且仍存在爭議,美國滅菌服務市場面臨不確定性。美國環保署 (EPA) 2024 年的最終規則預計,89 家商業 EtO 設施將產生 3.13 億美元的資本支出和 7,400 萬美元的年度合規成本,這將顯著改變單一氣體業務的經濟效益。隨後,2026 年 3 月的修訂將基於風險的標準、關閉要求和持續監測等核心問題重新提上日程,縮短了營運商和客戶的規劃時間。 STERIS 公司於 2025 年 1 月宣布其在伊利諾伊州的 EtO 訴訟已結束,這表明即使對於大型營運商而言,法律風險也是商業環境的一部分。在美國滅菌服務市場,這種波動性正促使客戶轉向那些僅在需要時提供環氧乙烷 (EtO) 的供應商,並將剩餘的處理工作轉向輻射或其他低溫處理方案。

細分市場分析

截至2025年,環氧乙烷(EtO)滅菌將占美國滅菌服務市場(按滅菌方法分類)的45.31%,這一地位仍反映出其對熱敏醫療設備和複雜組件的適用性。據美國環保署(EPA)稱,EtO滅菌用於滅菌美國50%的醫療設備,每年超過200億件,這解釋了為什麼即使法規日益嚴格,這種方法也難以被取代。伽馬射線輻照佔據第二大市場佔有率,這得益於成熟的客戶檢驗流程以及鈷-60的供給能力。 Sotera Health報告稱,2026年第一季Nordion鈷-60的銷售額成長了25.8%(不計外匯波動的影響),顯示市場對與更廣泛的滅菌生態系統相關的輻照材料的需求持續存在。

在美國滅菌服務市場,X光輻照是成長最快的滅菌方法,預計到2031年將維持9.38%的年成長率。 Sterigenics和STERIS兩家公司都在擴建其商業X光設施,這表明基於加速器的輻射技術在合約服務中正逐漸成為主流。此外,BGS USA計劃於2025年擴建其位於賓夕法尼亞州的電子束(E-Beam)處理能力,從而為東北部和大西洋中部地區的製造商提供更多輻射處理選擇。雖然VHP、NO2、電子束和乾熱滅菌目前仍屬於小眾領域,但當客戶需要低溫處理、短交貨期或與光敏材料具有高相容性時,這些技術的應用價值正在不斷提升。

截至2025年,異地服務中心滅菌在美國滅菌服務市場中佔據66.24%的佔有率(按服務方式分類)。這主要是因為在每個製造地內維護符合規範的多模態基礎設施成本高昂。這種模式仍然具有吸引力,因為客戶無需完全擁有設施,即可利用檢驗的流程、訓練有素的操作人員和完善的放行文件。它也適用於能夠為大規模合約滅菌商提供穩定業務量的長期服務合約。事實上,即使客戶越來越要求更高的冗餘性和接近性生產線,異地模式仍然是美國滅菌服務市場的核心。

現場服務,或稱“內部即服務”,是成長最快的交付模式,預計到2031年,美國滅菌服務市場在該領域的複合年成長率將達到8.52%。這種模式是指服務供應商在現場安裝、認證和操作設備,同時保持外包流程所需的品質可追溯性。品質機制標準責任制(QMSR)正在推動這一轉變,因為它更加強調對外包活動的記錄控制,以及在整個供應商關係中更清晰的課責。因此,這種模式對需要更高供應鏈柔軟性但又不想承擔滅菌設備全部監管責任的大批量製藥項目和醫療設備線尤其具有吸引力。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 醫院感染負擔加重和手術數量增加

- 醫療設備和製藥製造商的外包

- FDA QMSR 與 ISO 13485 的一致性

- 一次性及微創醫療設備的擴張

- 人工智慧驅動的分銷流程管理和週期追蹤

- 擴大X光設備的產能將消除環氧乙烷 (EtO) 和鈷-60 的瓶頸。

- 市場限制因素

- 環氧乙烷 (EtO)排放和合規性的變化

- 為符合規定,對多模態能力進行大量資本投資

- 無菌保證領域人員短缺

- 治療方法改變所引起的材料相容性問題

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 透過方法

- 環氧乙烷(EtO)滅菌

- 伽瑪射線照射

- 電子束(E-beam)輻照

- X光照射

- 蒸氣(濕熱)滅菌

- 乾熱滅菌

- 氣化過氧化氫/氣體等離子體滅菌

- 二氧化氮滅菌

- 按配送方式

- 異地(服務中心)消毒

- 現場/內部即服務式滅菌

- 按服務類型

- 外包消毒服務

- 滅菌驗證和測試服務

- 流程開發、諮詢和最佳化服務

- 最終用戶

- 醫療設備製造商

- 製藥和生物製藥製造商

- 醫院及門診手術中心

- 臨床檢查室和研究機構

- 其他最終用戶

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Advanced Sterilization Products(ASP)

- American Sterilizer Services

- BGS US LLC

- Cosmed Group

- Eagle Medical, Inc.

- E-BEAM Services, Inc.

- Infinity Laboratories/Eurofins Infinity Laboratory Group

- IsoTex, Inc.

- Life Science Outsourcing, Inc.

- Midwest Sterilization Corporation

- Noxilizer, Inc.

- Prince Sterilization Services, LLC

- Quantum EBX

- Remington Medical

- SGS SA

- Sotera Health

- STERIS plc

- Steri-Tek

- VPT Rad, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states sterilization services market size is projected to expand from USD 1.77 billion in 2025 and USD 1.88 billion in 2026 to USD 2.55 billion by 2031, registering a CAGR of 6.25% between 2026 to 2031.

This report is Segmented by Method (EtO Sterilization, Gamma Irradiation, E-Beam, and More), Mode of Delivery (Off-Site, On-site/In-house-as-a-Service), Service Type (Contract Sterilization, Validation & Testing, and More), and End User (Medical Device Manufacturers, Pharma & Biopharma, Hospitals & ASCs, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Sterilization Services Market Trends and Insights

Rising HAI Burden and Procedure Throughput

Healthcare-associated infections continue to keep sterilization performance under close clinical scrutiny, and the CDC's 2023 national and state report showed that device-related and procedure-related infection control remains a material issue for acute care settings. In the United States sterilization services market, that pressure matters because more procedures are moving through ambulatory settings that want hospital-grade sterility assurance without the full footprint of advanced in-house infrastructure. Higher-acuity case migration into ambulatory surgery centers increases the need for validated processing, packaging integrity, and documented release controls. That shift supports more off-site contract demand because many centers have limited space for multi-modal equipment and limited tolerance for process failure. The United States sterilization services market therefore benefits when procedure growth and infection prevention standards rise together, since both push customers toward more formal sterilization partnerships.

Outsourcing by Device and Pharma Manufacturers

The market is seeing stronger outsourcing momentum because QMSR raises the cost of running compliant internal sterilization operations and makes vendor oversight more visible during inspections. RAPS reported that outsourcing and purchasing controls ranked as the second-most-cited QMSR observation in more than 100 completed inspections as of May 2026, which shows how closely the FDA is reviewing supplier management. ISO 13485:2016 Clause 4.1.5 now carries more weight in practice because outsourced processes must be controlled in proportion to risk, and sterilization is one of the clearest examples of that rule. Large contract providers gain an advantage under this framework because they can offer documented quality systems, validation records, and audit-ready traceability as part of the service. That is why the United States sterilization services market is shifting toward bigger, multi-modal platforms for long-term outsourced agreements.

EtO Emissions and Compliance Volatility

EtO remains indispensable for many heat-sensitive products, but the United States sterilization services market faces uncertainty because the regulatory framework around emissions has changed quickly and remains contested. The EPA's 2024 final rule projected USD 313 million in capital investment and USD 74 million in annualized compliance costs across 89 commercial EtO facilities, which materially changed the economics of standalone gas operations. The March 2026 reconsideration proposal then reopened core issues including risk-based standards, enclosure requirements, and continuous monitoring, which shortened planning horizons for operators and customers alike. STERIS stated in January 2025 that an Illinois EtO trial had concluded, which highlights that legal exposure has become part of the operating environment for major participants as well. In the United States sterilization services market, this volatility pushes customers toward suppliers that can offer EtO only where needed and shift the rest of the load into radiation or other lower-temperature options.

Other drivers and restraints analyzed in the detailed report include:

- Single-Use and Minimally Invasive Device Expansion

- X-Ray Capacity Build-Outs Reducing EtO and Cobalt-60 Bottlenecks

- High Capex for Compliant Multi-Modal Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

EtO sterilization accounted for 45.31% of the United States sterilization services market share by method in 2025, and that position still reflects its fit for heat-sensitive devices and complex assemblies. The EPA stated that EtO sterilizes 50% of all medical devices used in the country each year, or more than 20 billion units, which explains why the method remains hard to displace even under tighter regulation. Gamma irradiation held the second-largest position, supported by established customer validation pathways and cobalt-60-linked supply capacity. Sotera Health reported 25.8% constant-currency growth in Nordion cobalt-60 revenue in Q1 2026, which showed continued demand for radiation inputs tied to the broader sterilization ecosystem.

X-ray irradiation is the fastest-growing method in the United States sterilization services market, with forecast growth of 9.38% through 2031. Sterigenics and STERIS both expanded commercial X-ray capacity, which signals that accelerator-based radiation is moving into a more mainstream role for contract services. BGS US also added E-Beam capacity in Pennsylvania in 2025, which widened the radiation choice set for manufacturers in the Northeast and mid-Atlantic. VHP, NO2, E-Beam, and dry-heat remain smaller niches, but their role rises when customers need low-temperature processing, fast turnaround, or better compatibility with sensitive materials.

Off-site service-center sterilization held 66.24% of United States sterilization services market share by delivery mode in 2025, supported by the high cost of maintaining compliant multi-modal infrastructure inside each manufacturing site. The model remains attractive because it gives customers access to validated processes, trained operators, and established release documentation without full facility ownership. It also fits the long-duration service agreements that stabilize throughput for large contract sterilizers. In practice, this keeps the off-site model central to the United States sterilization services market even as customers ask for more redundancy and closer proximity to production lines.

On-site or in-house-as-a-service is the fastest-growing delivery model, with the United States sterilization services market size for this segment projected to grow at an 8.52% CAGR through 2031. Under this approach, the service provider installs, qualifies, and operates equipment at the customer site while maintaining the quality trail expected for outsourced processes. QMSR supports that shift because it places stronger emphasis on documented control over outsourced activities and clearer accountability across supplier relationships. That makes the model especially attractive for high-volume pharmaceutical programs and device lines that need more supply chain flexibility without taking on full regulatory responsibility for the sterilization unit.

List of Companies Covered in this Report:

- Advanced Sterilization Products (ASP)

- American Sterilizer Services

- BGS US LLC

- Cosmed Group

- Eagle Medical, Inc.

- E-BEAM Services, Inc.

- Infinity Laboratories / Eurofins Infinity Laboratory Group

- IsoTex, Inc.

- Life Science Outsourcing, Inc.

- Midwest Sterilization Corporation

- Noxilizer

- Prince Sterilization Services

- Quantum EBX

- Remington Medical

- SGS

- Sotera Health

- STERIS

- Steri-Tek

- VPT Rad, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising HAI Burden and Procedure Throughput

- 4.2.2 Outsourcing by Device and Pharma Manufacturers

- 4.2.3 FDA QMSR and ISO 13485 Alignment

- 4.2.4 Single-Use and Minimally Invasive Device Expansion

- 4.2.5 AI-Enabled Chain-of-Custody and Cycle-Tracking

- 4.2.6 X-Ray Capacity Build-Outs Reducing EtO and Cobalt-60 Bottlenecks

- 4.3 Market Restraints

- 4.3.1 EtO Emissions and Compliance Volatility

- 4.3.2 High Capex for Compliant Multi-Modal Capacity

- 4.3.3 Sterility-Assurance Talent Shortage

- 4.3.4 Material-Compatibility Failures When Shifting Modalities

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Method

- 5.1.1 Ethylene Oxide (EtO) Sterilization

- 5.1.2 Gamma Irradiation

- 5.1.3 Electron-Beam (E-beam) Irradiation

- 5.1.4 X-ray Irradiation

- 5.1.5 Steam (Moist-Heat) Sterilization

- 5.1.6 Dry-Heat Sterilization

- 5.1.7 Vaporized Hydrogen Peroxide / Gas Plasma Sterilization

- 5.1.8 Nitrogen Dioxide Sterilization

- 5.2 By Mode of Delivery

- 5.2.1 Off-site (Service-Center) Sterilization

- 5.2.2 On-site / In-house-as-a-Service Sterilization

- 5.3 By Service Type

- 5.3.1 Contract Sterilization Services

- 5.3.2 Sterilization Validation & Testing Services

- 5.3.3 Process Development, Advisory & Optimization Services

- 5.4 By End User

- 5.4.1 Medical Device Manufacturers

- 5.4.2 Pharmaceutical & Biopharmaceutical Manufacturers

- 5.4.3 Hospitals & Ambulatory Surgery Centers

- 5.4.4 Clinical Laboratories & Research Organizations

- 5.4.5 Other End Users

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Advanced Sterilization Products (ASP)

- 6.3.2 American Sterilizer Services

- 6.3.3 BGS US LLC

- 6.3.4 Cosmed Group

- 6.3.5 Eagle Medical, Inc.

- 6.3.6 E-BEAM Services, Inc.

- 6.3.7 Infinity Laboratories / Eurofins Infinity Laboratory Group

- 6.3.8 IsoTex, Inc.

- 6.3.9 Life Science Outsourcing, Inc.

- 6.3.10 Midwest Sterilization Corporation

- 6.3.11 Noxilizer, Inc.

- 6.3.12 Prince Sterilization Services, LLC

- 6.3.13 Quantum EBX

- 6.3.14 Remington Medical

- 6.3.15 SGS SA

- 6.3.16 Sotera Health

- 6.3.17 STERIS plc

- 6.3.18 Steri-Tek

- 6.3.19 VPT Rad, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

全球滅菌服務市場預測(至2034年)-依產品、方法、最終使用者和地區分類的分析

全球滅菌服務市場預測(至2034年)-依產品、方法、最終使用者和地區分類的分析 滅菌服務市場報告:按方法、類型、交付方式、最終用戶和地區分類(2026-2034 年)

滅菌服務市場報告:按方法、類型、交付方式、最終用戶和地區分類(2026-2034 年) 滅菌服務市場:按類型、交付方式、技術和最終用途產業分類-2026-2032年全球預測

滅菌服務市場:按類型、交付方式、技術和最終用途產業分類-2026-2032年全球預測 滅菌服務市場:依方法、商業模式、最終用戶和地區分類

滅菌服務市場:依方法、商業模式、最終用戶和地區分類 滅菌服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

滅菌服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 全球滅菌服務市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球異地滅菌服務市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034年)全球消毒服務市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034)

全球滅菌服務市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球異地滅菌服務市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034年)全球消毒服務市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034) 滅菌服務市場規模、佔有率和成長分析(按方法、類型、交付方式、最終用戶和地區分類)-2026-2033年產業預測

滅菌服務市場規模、佔有率和成長分析(按方法、類型、交付方式、最終用戶和地區分類)-2026-2033年產業預測 全球滅菌服務市場-產業規模、佔有率、趨勢、機會和預測,依方法、服務類型、交付方式、最終用戶、地區和競爭格局分類,2020-2030 年預測

全球滅菌服務市場-產業規模、佔有率、趨勢、機會和預測,依方法、服務類型、交付方式、最終用戶、地區和競爭格局分類,2020-2030 年預測