|

市場調查報告書

商品編碼

1940552

滅菌服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Sterilization Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

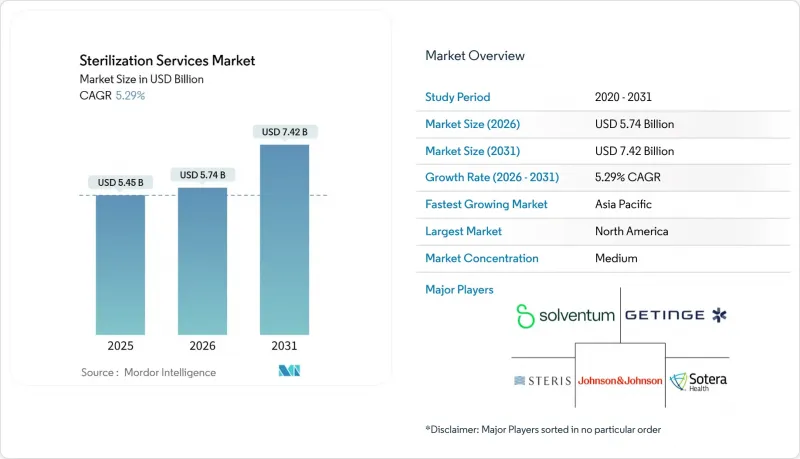

預計消毒服務市場將從 2025 年的 54.5 億美元成長到 2026 年的 57.4 億美元,到 2031 年將達到 74.2 億美元,2026 年至 2031 年的複合年成長率為 5.29%。

持續擴張的驅動力來自嚴格的感染控制通訊協定的不斷實施、ISO 13485標準的監管趨同以及外包加工的快速普及。從高排放環氧乙烷(EtO)技術向X光、電子束和過氧化氫技術的加速轉型,既帶來了資金壓力,也為創新提供了空間。隨著一次性生物加工組件和微創醫療設備進入全球供應鏈,市場需求也不斷成長。市場領導正透過收購擴大其地理覆蓋範圍和驗證技術專長,而新興的專業公司則專注於小眾材料數位化監控。這些因素共同作用,在日益激烈的競爭中維持了定價權。

全球滅菌服務市場趨勢與洞察

全球醫院感染病例增加推動了消毒需求。

世界各地的醫療機構都在加強消毒通訊協定,以遏制感染疾病的蔓延,避免延長住院時間和增加醫療成本。美國疾病管制與預防中心 (CDC)的指南將徹底的環境清潔視為第一道防線,迫使醫療機構採用檢驗的、大量的滅菌服務。資源匱乏的地區,其感染率是已開發國家的數倍,這些地區擴大將處理流程外包,以在無需大量資本支出的情況下獲得可靠的滅菌保障。支付方將報銷與感染指標掛鉤,也助長了這個趨勢。醫療設備製造商將無菌包裝納入生產批次,簡化了監管申報流程,合約處理商也因此受益。這些趨勢共同推動了每年進入滅菌服務市場的手術數量不斷增加。

全球醫療設備和藥品製造地擴張

醫療設備組裝線和生物製藥填充廠向亞太地區的轉移,推動了該地區對檢驗的滅菌能力的需求。全球供應商正在建造多模態樞紐,以在物流中斷的情況下維持供應鏈的韌性。注射用生技藥品需要最高等級的無菌保證,其外包週期比例日益增加。擁有業界領先的劑量映射和微生物挑戰測試技術的專業處理商正獲得高價。吸引外資的政府正為新建放射線殺菌設施提供誘因,加速在地化進程,並加強對ISO 11137標準的遵守。

建立符合規範的滅菌設施需要高昂的資本和營運成本。

輻照器、真空環氧乙烷(EtO)室和氣化過氧化氫隔離器都需要數百萬美元的初始投資、專用通風設備和冗餘監控系統。年度維護成本包括生物指示劑檢測、過濾器驗證和監管審核。小規模社區醫院通常會推遲投資,轉而尋求多年外包協議。資金壁壘也限制了新進入者,並可能導致產業整合,造成供給能力不足地區的醫療資源短缺。

細分市場分析

到2025年,環氧乙烷將佔據滅菌服務市場49.30%的佔有率,這反映了其與熱敏性和高通量醫療設備無與倫比的兼容性。然而,累積的監管壓力和公眾健康問題正在加速市場多元化。 X光循環滅菌技術已在多種產品中檢驗,預計到2031年將以12.15%的複合年成長率成長,成為成長最快的細分市場。劑量均勻性研究表明,其滅菌效果與伽馬射線輻照相當,同時避免了鈷-60滅菌帶來的物流挑戰。伽馬射線滅菌擁有成熟的基礎設施和可靠的深度穿透能力,但同位素供應的限制促使人們開發替代方案。電子束輻照可以實現高速處理,但受限於高密度托盤。過氧化氫等離子體和氣相系統適用於電子內視鏡等溫度敏感物品,並在高價值手術包領域建立了忠實的基本客群。隨著材料科學的發展,方法選擇越來越依賴聚合物在氧化壓力下的行為,這就要求加工商提供多模態功能。

滅菌服務市場持續將資本投資重新分配至具備雙能切換功能的放射治療室,從而實現從同位素放射源到機械放射源的無縫轉換。供應商正與設備工程師合作,在設備設計階段納入劑量分佈圖,以減少生產後的變異性。蒸氣氧化氫作為成熟的A類方法獲得監管部門核准,簡化了510(k)申報流程,並進一步豐富了治療方式的市場佔有率。由此帶來的治療方式多元化正在重塑收入結構,並確保供應的持續性。

至2025年,異地服務中心將佔據滅菌服務市場67.05%的佔有率,利用規模經濟攤提資本投資和環境控制成本。集中式樞紐全天候處理混合貨物,並提供檢驗的運輸路線和數位化監管鏈報告。面對人員短缺和手術器械積壓,醫院擴大將托盤傳輸到區域異地再處理中心,以提高合規性和可預測的交付時間。同時,現場服務模式預計將以10.98%的複合年成長率成長,並受到高產量製藥園區的青睞,因為即時放行可以減少庫存週轉天數。混合模式正在興起,將用於超量處理的移動式乙醇消毒艙與預定的異地輻照相結合,使客戶能夠更好地平衡成本和週期時間。

不斷變化的地緣政治風險凸顯了冗餘的重要性。跨國製造商在地理位置分散的供應商之間部署重複驗證機制,以確保應對疫情和自然災害的能力。作為應對措施,合約加工商正在開發鏡像數位文件系統,以實現工廠與客戶品質入口網站之間週期資料的即時傳輸。

區域分析

北美將在2025年繼續保持主導地位,市場佔有率將達到39.10%,這得益於其健全的報銷模式、密集的醫療設備叢集以及積極的環境監測。美國環保署(EPA)將於2025年最終確定一項法規,要求環氧乙烷(EtO)的捕集率達到99.99%,這將迫使醫療機構維修清除技術,並加速向機械放射源的過渡。儘管合規成本增加,但對替代方法的投資將確保供應的連續性,並維持該地區的主導地位。

亞太地區是成長最快的市場,預計到2031年複合年成長率將達到10.82%。中國、印度和馬來西亞醫療設備契約製造的擴張需要附近具備符合美國和歐盟審核標準的滅菌能力。 STERIS計畫於2025年在蘇州運作一座X光滅菌設施,這便是以多能量滅菌能力為核心的打入市場策略的典型案例。各國政府鼓勵國內輻照以減少出口瓶頸,而地方監管機構則積極推動符合ISO 11137和ISO 13408標準,以簡化跨境貿易。

預計到2025年,歐洲將維持約30.20%的市場佔有率,其特點是醫療設備法規(MDR)對設備和包裝驗證規定極為嚴格。為了實現永續性目標,供應商正積極拓展業務,採用超臨界二氧化碳和氣化過氧化氫循環技術。 SGS擴大了MDR滅菌認證範圍,凸顯了製程廣度帶來的競爭優勢。如今,企業競標中納入的永續性指標正在影響供應商的選擇,推動企業投資於節能型加速器和熱回收通風系統。

其他福利:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章 引言

- 研究假設和市場定義

- 調查範圍

第2章調查方法

第3章執行摘要

第4章 市場情勢

- 市場概覽

- 市場促進因素

- 全球醫院感染發生率不斷上升,推動了消毒需求的成長。

- 全球醫療設備和藥品製造地擴張

- 更嚴格、更統一的國際滅菌標準(ISO、FDA、EMA)

- 為了應對合規性和成本壓力,企業越來越傾向於選擇外包滅菌服務。

- 由於一次性醫療器材和微創醫療設備的日益普及,消毒量也隨之增加。

- 市場限制

- 建立符合規範的滅菌設施需要高昂的資本和營運成本。

- 關於環氧乙烷和放射性同位素的使用,有嚴格的環境和勞動法規。

- 全球認證無菌保證和驗證專業人員短缺

- 技術展望

- 波特五力模型

- 新進入者的威脅

- 買方的議價能力

- 供應商的議價能力

- 替代品的威脅

- 競爭對手之間的競爭

第5章 市場規模與成長預測

- 透過方法

- 環氧乙烷(EtO)滅菌

- 伽瑪射線照射

- 電子束(E-beam)輻照

- X光輻射

- 蒸氣(濕熱)滅菌

- 乾熱滅菌

- 過氧化氫和等離子體滅菌

- 透過供應表格

- 異地(服務中心)消毒

- 現場消毒(作為內部服務)

- 按服務類型

- 合約滅菌服務

- 滅菌驗證和測試服務

- 流程諮詢與最佳化服務

- 最終用戶

- 醫療設備製造商

- 製藥和生物技術製造商

- 醫院和診所

- 食品飲料業

- 研究機構及科研單位

- 其他工業用戶

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 亞太其他地區

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲地區

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- STERIS PLC

- Sotera Health(Sterigenics, Nordion, Nelson Labs)

- Getinge AB

- Solventum Corporation

- Johnson & Johnson(Ethicon)

- BGS Beta-Gamma-Service GmbH

- E-BEAM Services Inc.

- Medistri SA

- Noxilizer Inc.

- Stryker Corporation

- Prince Sterilization Services LLC

- Advanced Sterilization Products(ASP)

- GERMITECH Srl

- Cosmed Group

- MMM Group

- Belimed AG

第7章 市場機會與未來展望

The sterilization services market is expected to grow from USD 5.45 billion in 2025 to USD 5.74 billion in 2026 and is forecast to reach USD 7.42 billion by 2031 at 5.29% CAGR over 2026-2031.

Consistent adoption of stringent infection-control protocols, regulatory convergence toward ISO 13485, and rapid uptake of outsourced processing underpin steady expansion. Accelerating transition away from high-emission ethylene oxide (EtO) toward X-ray, electron-beam, and hydrogen-peroxide technologies adds both capital pressure and innovation headroom. Demand also rises as single-use bioprocess components and minimally invasive devices flood global supply chains. Market leaders leverage acquisitions to broaden geographic reach and validation expertise, while emerging specialists focus on niche materials and digitalized monitoring. Collectively, these forces sustain pricing power even as competitive intensity grows.

Global Sterilization Services Market Trends and Insights

Escalating Global Incidence of Hospital-Acquired Infections Driving Sterilization Demand

Healthcare facilities worldwide are intensifying decontamination protocols to curb infections that prolong hospital stays and inflate costs. Guidance from the Centers for Disease Control and Prevention positions thorough environmental cleaning as a frontline defense, pushing providers to adopt validated, high-capacity sterilization services. Low-resource regions, which report infection rates several times higher than advanced economies, increasingly outsource processing to achieve reliable sterility assurance without heavy capital spending. Insurance payers reinforce the shift by linking reimbursement to infection metrics. Contract processors benefit as device manufacturers bundle sterile packaging with production runs to streamline regulatory submissions. Collectively, these behaviors lift annual procedure volumes flowing into the sterilization services market.

Expansion of Medical Device & Pharmaceutical Manufacturing Footprint Worldwide

Relocation of device assembly lines and biologics fill-finish plants toward Asia-Pacific fuels regional demand for validated sterilization capacity. Global suppliers establish multi-modal hubs so that supply chains stay resilient amid logistics disruption. Injectable biologics, which require the highest sterility assurance level, now represent a growing slice of outsourced cycles. Specialized processors with class-leading dose mapping and microbial challenge expertise capture premium pricing. Governments courting foreign investment offer incentives for greenfield irradiation facilities, accelerating local availability and reinforcing compliance with ISO 11137.

High Capital & Operating Costs of Establishing Compliant Sterilization Facilities

Irradiators, vacuum-draw EtO chambers, and vaporized hydrogen-peroxide isolators each demand multimillion-dollar outlays, specialized ventilation, and redundant monitoring. Annual upkeep includes biological indicators, filter validation, and regulatory audits. Smaller regional hospitals defer investment and instead pursue multiyear outsourcing contracts. Financial barriers also restrict new competitors, leading to industry consolidation that can strain capacity in underserved territories.

Other drivers and restraints analyzed in the detailed report include:

- Tightening & Harmonization of International Sterilization Standards (ISO, FDA, EMA)

- Growing Preference for Outsourced Sterilization to Manage Compliance & Cost Pressures

- Stringent Environmental & Occupational Regulations on EtO and Radio-isotope Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ethylene oxide retained a dominant 49.30% slice of the sterilization services market size in 2025, reflecting unmatched compatibility with heat-sensitive, lumen-rich devices. Yet, cumulative regulatory pressure and public health concerns accelerate diversification. X-ray cycles, already validated for a widening catalog, are forecast to record a 12.15% CAGR through 2031, the fastest within the segment. Dose-uniformity studies show its efficacy equals gamma irradiation while avoiding cobalt-60 logistics. Gamma retains entrenched infrastructure and reliable deep-penetration performance, although isotope supply constraints spur contingency planning. Electron-beam offers rapid throughput but faces limitations with dense pallets. Hydrogen-peroxide plasma and vapor-phase systems capture temperature-sensitive items like electronic endoscopes, building a loyal customer base in high-value surgical kits. As material science evolves, method selection increasingly hinges on polymer behavior under oxidative stress, pushing processors to offer multi-modal capabilities.

The sterilization services market continues reallocating capex toward radiation vaults equipped for dual-energy switching, enabling seamless migration from isotope to machine sources. Providers collaborate with device engineers to embed dose mapping at the design stage, reducing post-production inconsistencies. Regulatory acceptance of vaporized hydrogen-peroxide as an Established Category A method simplifies 510(k) submissions, further fragmenting modal shares. Consequently, method diversification reshapes revenue streams and safeguards supply continuity.

Off-site service centers captured 67.05% of the sterilization services market in 2025, leveraging scale to amortize capital outlays and environmental controls. Centralized hubs process mixed loads 24/7, offering validated truck routes and digital chain-of-custody reporting. Hospitals pressured by staffing shortages and surgical-instrument backlogs increasingly divert trays to regional off-site re-processing centers, citing improved compliance and predictable turnaround. Conversely, on-site service models, projected to advance at an 10.98% CAGR, appeal to high-volume pharma campuses where real-time release trims inventory days. Hybrid models emerge, blending mobile EtO pods for overflow with routine off-site irradiation, permitting clients to fine-tune cost versus cycle time.

Evolving geopolitical risks underscore redundancy. Multinational manufacturers allocate dual validation across geographically separated providers to ensure pandemic or natural-disaster resilience. In response, contract processors develop mirrored digital documentation systems, enabling instant transfer of cycle data between facilities and clients' quality portals.

The Sterilization Services Market Report is Segmented by Method (Ethylene Oxide (ETO) Sterilization, Gamma Irradiation, and More), Mode of Delivery (Off-Site Sterilization, and More), Service Type (Contract Sterilization Services, and More), End User (Medical Device Manufacturers, Hospitals and Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the sterilization services market with a 39.10% share in 2025, underpinned by robust reimbursement models, dense medical-device clusters, and proactive environmental oversight. The Environmental Protection Agency's 2025 final rule demanding 99.99% EtO capture forces providers to retrofit abatement technology and accelerates migration toward machine-source radiation. Investment in alternative modalities safeguards supply continuity and sustains regional leadership despite higher compliance costs.

Asia-Pacific represents the fastest-growing arena at an 10.82% CAGR through 2031. Expanding device contract-manufacturing organizations in China, India, and Malaysia require proximity sterilization capacity that satisfies U.S. and EU audits. STERIS's 2025 commissioning of an X-ray facility in Suzhou exemplifies market-entry strategies oriented toward multi-energy resilience. Governments encourage domestic irradiation to minimize export bottlenecks, and local regulators are aligning with ISO 11137 and ISO 13408, streamlining cross-border trade.

Europe maintains roughly 30.20% share in 2025, characterized by the Medical Device Regulation's stringent device and packaging validation clauses. Providers diversify into super-critical carbon-dioxide and vaporized hydrogen-peroxide cycles to meet sustainability objectives. SGS's expanded MDR sterilization certification scope highlights competitive advantage through process breadth. Sustainability metrics embedded in corporate tenders now influence vendor selection, prompting investment in energy-efficient accelerators and heat-recovery ventilation.

- STERIS

- Sotera Health (Sterigenics, Nordion, Nelson Labs)

- Getinge

- Solventum Corporation

- Johnson & Johnson

- BGS Beta-Gamma-Service GmbH

- E-BEAM Services Inc.

- Medistri

- Noxilizer Inc.

- Stryker

- Prince Sterilization Services LLC

- Advanced Sterilization Products (ASP)

- GERMITECH Srl

- Cosmed Group

- MMM Group

- Belimed

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Incidence of Hospital-Acquired Infections Driving Sterilization Demand

- 4.2.2 Expansion of Medical Device & Pharmaceutical Manufacturing Footprint Worldwide

- 4.2.3 Tightening & Harmonization of International Sterilization Standards (ISO, FDA, EMA)

- 4.2.4 Growing Preference for Outsourced Sterilization to Manage Compliance & Cost Pressures

- 4.2.5 Rising Adoption of Single-Use & Minimally Invasive Devices Increasing Sterilization Volumes

- 4.3 Market Restraints

- 4.3.1 High Capital & Operating Costs of Establishing Compliant Sterilization Facilities

- 4.3.2 Stringent Environmental & Occupational Regulations on EtO and Radio-isotope Use

- 4.3.3 Global Shortage of Certified Sterility Assurance & Validation Professionals

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Method

- 5.1.1 Ethylene Oxide (EtO) Sterilization

- 5.1.2 Gamma Irradiation

- 5.1.3 Electron-Beam (E-beam) Radiation

- 5.1.4 X-ray Radiation

- 5.1.5 Steam (Moist-Heat) Sterilization

- 5.1.6 Dry-Heat Sterilization

- 5.1.7 Hydrogen Peroxide & Plasma Sterilization

- 5.2 By Mode of Delivery

- 5.2.1 Off-site (Service-Center) Sterilization

- 5.2.2 On-site (In-house as a Service) Sterilization

- 5.3 By Service Type

- 5.3.1 Contract Sterilization Services

- 5.3.2 Sterilization Validation & Testing Services

- 5.3.3 Process Advisory & Optimization Services

- 5.4 By End-user

- 5.4.1 Medical Device Manufacturers

- 5.4.2 Pharmaceutical & Biotech Manufacturers

- 5.4.3 Hospitals & Clinics

- 5.4.4 Food & Beverage Industry

- 5.4.5 Laboratory & Research Organizations

- 5.4.6 Other Industrial Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 STERIS PLC

- 6.3.2 Sotera Health (Sterigenics, Nordion, Nelson Labs)

- 6.3.3 Getinge AB

- 6.3.4 Solventum Corporation

- 6.3.5 Johnson & Johnson (Ethicon)

- 6.3.6 BGS Beta-Gamma-Service GmbH

- 6.3.7 E-BEAM Services Inc.

- 6.3.8 Medistri SA

- 6.3.9 Noxilizer Inc.

- 6.3.10 Stryker Corporation

- 6.3.11 Prince Sterilization Services LLC

- 6.3.12 Advanced Sterilization Products (ASP)

- 6.3.13 GERMITECH Srl

- 6.3.14 Cosmed Group

- 6.3.15 MMM Group

- 6.3.16 Belimed AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

美國滅菌服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

美國滅菌服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 全球滅菌服務市場預測(至2034年)-依產品、方法、最終使用者和地區分類的分析

全球滅菌服務市場預測(至2034年)-依產品、方法、最終使用者和地區分類的分析 滅菌服務市場報告:按方法、類型、交付方式、最終用戶和地區分類(2026-2034 年)

滅菌服務市場報告:按方法、類型、交付方式、最終用戶和地區分類(2026-2034 年) 滅菌服務市場:按類型、交付方式、技術和最終用途產業分類-2026-2032年全球預測

滅菌服務市場:按類型、交付方式、技術和最終用途產業分類-2026-2032年全球預測 滅菌服務市場:依方法、商業模式、最終用戶和地區分類

滅菌服務市場:依方法、商業模式、最終用戶和地區分類 全球滅菌服務市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球異地滅菌服務市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034年)全球消毒服務市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034)

全球滅菌服務市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球異地滅菌服務市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034年)全球消毒服務市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析、未來預測(2026-2034) 滅菌服務市場規模、佔有率和成長分析(按方法、類型、交付方式、最終用戶和地區分類)-2026-2033年產業預測

滅菌服務市場規模、佔有率和成長分析(按方法、類型、交付方式、最終用戶和地區分類)-2026-2033年產業預測 全球滅菌服務市場-產業規模、佔有率、趨勢、機會和預測,依方法、服務類型、交付方式、最終用戶、地區和競爭格局分類,2020-2030 年預測

全球滅菌服務市場-產業規模、佔有率、趨勢、機會和預測,依方法、服務類型、交付方式、最終用戶、地區和競爭格局分類,2020-2030 年預測