|

市場調查報告書

商品編碼

2064411

美國頁岩氣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)United States Shale Gas - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

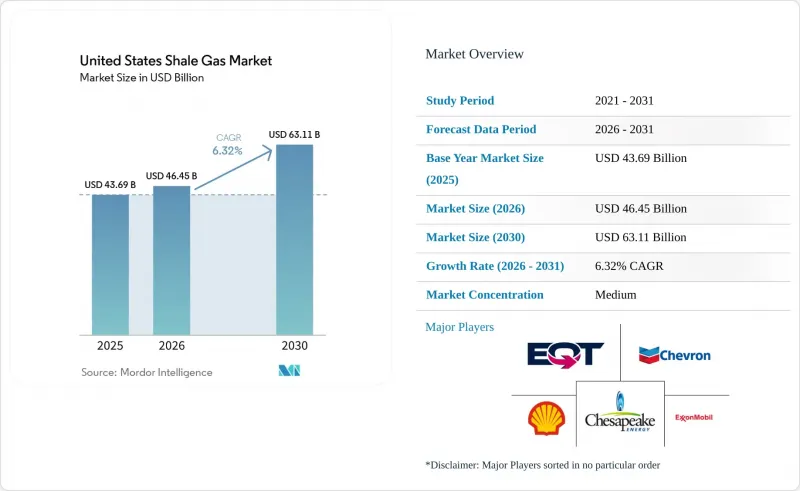

據 Mordor Intelligence 稱,2025 年美國頁岩氣市場價值 436.9 億美元,預計到 2030 年將達到 631.1 億美元,而 2026 年為 464.5 億美元,預測期內(2026-2030 年)的複合年成長率預計為 6.32%。

本報告按碳氫化合物類型(頁岩氣、頁岩油)、開採技術(僅水平鑽井、僅水力壓裂、水平鑽井與水力壓裂相結合)和應用領域(發電、工業和石化原料、住宅和商業供暖、交通運輸)進行分類。市場預測以美元計價。

美國頁岩氣市場趨勢與分析

自2026年起,液化天然氣出口能力將穩定成長。

Golden Pass LNG計畫將於2026年初投產,日產能為2.3億立方英尺(Bcf/d)。 Chenier公司的Corpus Christi第三期擴建工程將於2029年新增2.7億立方英尺/日(Bcf/d)的產能。加上Prakmins和Carcacheux Pass項目,這些項目將額外吸收7億至8億立方英尺/日的供應,從而收緊供需平衡,並將Henry Hub的價格從2024年的每百萬英熱單位(MMBtu)2.21美元推高至2025年的3.52美元。聯邦能源監理委員會(FERC)已將前期建設週期縮短至多18個月,以便更快做出最終投資決策。

由於藍氫項目,需求增加

雪佛龍公司位於貝城的「拉布拉多計畫」投資50億美元,預計到2027年,當其低碳氫氣年產能達到120萬噸時,該計畫每天將消耗0.3億立方英尺天然氣。空氣產品公司位於路易斯安那州的氫氣生產綜合體規模與此類似。根據《通貨膨脹控制法案》,45V稅額扣抵(最高可達3美元/公斤)正引導投資者轉向以天然氣為供應、可透過管道儲存二氧化碳的項目。

暫停聯邦政府對公共土地的租賃

美國土地管理局 (BLM) 的一項指令 IM-2025-028 將地塊審查期縮短至六個月,並恢復了季度銷售。這促使租賃業務復甦,此前租賃業務在 2021 年至 2024 年間下降了 80%。 《一項大型美麗建築法案》將特許權使用費最低標準設定為 12.5%,並向參與企業開放了新墨西哥州和懷俄明州的庫存。

細分市場分析

2025年,頁岩氣在美國頁岩氣市場仍佔78.8%的佔有率,但頁岩油在2031年之前以6.8%的複合年成長率成長,原因是二疊紀盆地的運營商競相開發富含液態烴的區域,這些區域的盈虧平衡點低於每桶40美元。 2026年2月,德文能源公司告知投資者,公司將「盡可能專注於石油生產」。這項政策導致鑽井鑽機從海恩斯維爾轉移到德拉瓦盆地,但伴生氣日產量達27.7億立方英尺,年增11%。到2026年初,這項政策轉變使盆地內的油氣鑽探比例縮小至1:5,但由於液態烴的開發不可避免地提高了甲烷產量,天然氣總供應量並未減少。阿巴拉契亞地區的馬塞勒斯頁岩和尤蒂卡頁岩層幾乎仍然全部是乾氣。 EQT已獲得一份長期液化天然氣契約,每年供應450萬噸,到2025年中期,日產能將達到6.2億立方英尺。這使其三分之一的產量免受現貨價格波動的影響。

液態烴價格飆升也影響二疊紀盆地以外地區的資本流入。 2024年10月,雪佛龍公司以65億美元出售其在加拿大的油砂和杜弗內頁岩資產,為美國二疊紀盆地的鑽探活動籌集了資金。該盆地基礎設施完善,監管程序也相對寬鬆。相較之下,海恩斯維爾地區的營運商直到2025年亨利樞紐天然氣價格回升至3.52美元/百萬英熱單位後才開始鑽探更深、成本更高的地層。這表明,即使企業標榜“穩健成長”,大宗商品價格仍然主導著市場活動。然而,在液化烴資源豐富的地區進行鑽探並不能縮小甚至消除產量差距。由於探勘成本較低且管道網路完善,乾氣生產仍是美國頁岩氣市場規模的主要支撐。因此,供應結構呈現兩極化,乾氣生產區能夠提供價格穩定性,而富含液態烴的地區在原油價格上漲期間則能獲得更高的利潤率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 從2026年起,液化天然氣出口能力將穩定成長。

- 由於藍氫項目,需求增加

- 由於傳統資源枯竭,從傳統資源轉型為頁岩資源

- 甲烷排放強度認證進階版

- 利用數位雙胞胎進行油井最佳化

- 二氧化碳壓裂法獲得監管部門支持。

- 市場限制因素

- 暫停聯邦政府對公共土地的租約

- 受環境、社會及公司治理(ESG)因素驅動的資本外流不斷擴大

- 與沙子和水相關的物流瓶頸依然存在。

- 阿巴拉契亞地區的當地反對派

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- PESTLE分析

第5章:預測市場規模與成長率

- 按烴類類型

- 頁岩氣

- 頁岩油

- 透過萃取技術

- 僅水平開挖

- 僅水力壓裂

- 水平鑽井與水力壓裂技術的結合應用

- 透過使用

- 發電

- 工業和石油化學原料

- 住宅和商業供暖

- 運輸(液化天然氣/壓縮天然氣)

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Exxon Mobil Corporation

- EQT Corporation

- Chesapeake Energy Corp.

- Chevron Corporation

- Shell plc

- ConocoPhillips Company

- Coterra Energy Inc.

- Southwestern Energy Co.

- Pioneer Natural Resources Co.

- Devon Energy Corporation

- EOG Resources Inc.

- Range Resources Corp.

- Antero Resources Corp.

- Continental Resources Inc.

- Marathon Oil Corporation

- Cabot Oil & Gas(now Coterra)

- Murphy Oil Corporation

- TotalEnergies SE

- Baker Hughes Company

- Schlumberger NV

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states shale gas market size was valued at USD 43.69 billion in 2025 and is estimated to grow from USD 46.45 billion in 2026 to reach USD 63.11 billion by 2030, at a CAGR of 6.32% during the forecast period (2026-2030).

This report is Segmented by Hydrocarbon Type (Shale Gas, Shale Oil), Extraction Technology (Horizontal Drilling Only, Hydraulic Fracturing Only, Combined Horizontal and Hydraulic Fracturing), and Application (Power Generation, Industrial and Petrochemical Feedstock, Residential and Commercial Heating, Transportation). The Market Forecasts are Provided in Terms of Value (USD).

United States Shale Gas Market Trends and Insights

Robust LNG Export Capacity Additions Post-2026

Golden Pass LNG began service in early 2026 with 2.3 Bcf/d, while Cheniere's Corpus Christi Stage 3 expansion adds 2.7 Bcf/d by 2029. Together with Plaquemines and Calcasieu Pass, these projects absorb 7-8 Bcf/d of incremental supply, tightening balances and lifting Henry Hub from USD 2.21/MMBtu in 2024 to USD 3.52/MMBtu in 2025. The Federal Energy Regulatory Commission trimmed pre-construction timelines by up to 18 months, enabling faster final-investment decisions.

Rising Demand from Blue-Hydrogen Projects

Chevron's USD 5 billion Project Labrador in Baytown will consume 0.3 Bcf/d of gas when it reaches 1.2 million t/yr of low-carbon hydrogen capacity in 2027. Air Products' Louisiana complex follows a comparable scale. The Inflation Reduction Act's 45V credit of up to USD 3/kg steers investors toward gas-fed projects where pipeline CO2 storage is available.

Federal Leasing Pauses on Public Lands

BLM's Instruction Memorandum IM-2025-028 shortened parcel reviews to six months and reinstated quarterly sales, reversing an 80% decline in lease volumes between 2021 and 2024. The One Big Beautiful Bill Act locked in a 12.5% royalty floor, unlocking inventory in New Mexico and Wyoming for United States shale gas market participants.

Other drivers and restraints analyzed in the detailed report include:

- Depletion-Driven Shift from Conventional to Shale

- Growth in Data-Center Power-Purchase Agreements

- Escalating EPA Waste Emissions Charge

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shale gas retained a 78.8% United States shale gas market share in 2025, but shale oil is expanding at a 6.8% CAGR through 2031 as Permian operators chase liquids-rich zones where breakevens sit below USD 40 per barrel. Devon Energy told investors in February 2026 that it would "stay as oily as we can," a stance that redirected rigs from the Haynesville to the Delaware Basin even though associated gas output still climbed 11% year over year to 27.7 Bcf/d. This pivot compressed the basin's gas-to-oil drilling ratio to 1:5 by early 2026, yet it did not erode total gas supply because liquids development inevitably lifts methane volumes. Appalachia's Marcellus and Utica formations remain almost entirely dry gas; EQT produced 6.2 Bcf/d in mid-2025 and locked 4.5 MTPA into long-term LNG contracts that hedge one-third of its output against spot volatility.

The liquids premium also influences capital flows outside the Permian. Chevron's USD 6.5 billion divestiture of Canadian oil sands and Duvernay shale assets in October 2024 freed cash for U.S. Permian drilling where infrastructure is ready and regulatory timelines are short. In contrast, Haynesville operators drilled deeper, higher-cost intervals only after Henry Hub recovered to USD 3.52/MMBtu in 2025, proving commodity prices still steer activity despite corporate statements about "disciplined growth". Even so, liquids-rich drilling narrows but does not eliminate the volume gap; dry-gas provinces continue to anchor the United States shale gas market size because of their low finding costs and existing pipeline networks. The result is a bifurcated supply stack in which dry-gas basins provide price stability while liquids-heavy plays offer margin upside during oil rallies.

List of Companies Covered in this Report:

- Exxon Mobil Corporation

- EQT Corporation

- Chesapeake Energy Corp.

- Chevron Corporation

- Shell plc

- ConocoPhillips Company

- Coterra Energy Inc.

- Southwestern Energy Co.

- Pioneer Natural Resources Co.

- Devon Energy Corporation

- EOG Resources Inc.

- Range Resources Corp.

- Antero Resources Corp.

- Continental Resources Inc.

- Marathon Oil Corporation

- Cabot Oil & Gas (now Coterra)

- Murphy Oil Corporation

- TotalEnergies SE

- Baker Hughes Company

- Schlumberger NV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust LNG export capacity additions post-2026

- 4.2.2 Rising demand from blue-hydrogen projects

- 4.2.3 Depletion-driven shift from conventional to shale resources

- 4.2.4 Methane-intensity certification premiums

- 4.2.5 Digital twin-enabled well optimization

- 4.2.6 CO2-based fracturing gaining regulatory support

- 4.3 Market Restraints

- 4.3.1 Federal leasing pauses on public lands

- 4.3.2 Growing ESG-led capital flight

- 4.3.3 Persistent sand & water logistics bottlenecks

- 4.3.4 Community opposition in Appalachia

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 PESTLE Analysis

5 Market Size & Growth Forecasts

- 5.1 By Hydrocarbon Type

- 5.1.1 Shale Gas

- 5.1.2 Shale Oil

- 5.2 By Extraction Technology

- 5.2.1 Horizontal Drilling Only

- 5.2.2 Hydraulic Fracturing Only

- 5.2.3 Combined Horizontal and Hydraulic Fracturing

- 5.3 By Application

- 5.3.1 Power Generation

- 5.3.2 Industrial and Petrochemical Feedstock

- 5.3.3 Residential and Commercial Heating

- 5.3.4 Transportation (LNG and CNG)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Exxon Mobil Corporation

- 6.4.2 EQT Corporation

- 6.4.3 Chesapeake Energy Corp.

- 6.4.4 Chevron Corporation

- 6.4.5 Shell plc

- 6.4.6 ConocoPhillips Company

- 6.4.7 Coterra Energy Inc.

- 6.4.8 Southwestern Energy Co.

- 6.4.9 Pioneer Natural Resources Co.

- 6.4.10 Devon Energy Corporation

- 6.4.11 EOG Resources Inc.

- 6.4.12 Range Resources Corp.

- 6.4.13 Antero Resources Corp.

- 6.4.14 Continental Resources Inc.

- 6.4.15 Marathon Oil Corporation

- 6.4.16 Cabot Oil & Gas (now Coterra)

- 6.4.17 Murphy Oil Corporation

- 6.4.18 TotalEnergies SE

- 6.4.19 Baker Hughes Company

- 6.4.20 Schlumberger NV

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

北美頁岩氣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

北美頁岩氣:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 頁岩氣市場:2026-2032年全球市場預測(依開採技術、產品類型、純度等級及應用分類)

頁岩氣市場:2026-2032年全球市場預測(依開採技術、產品類型、純度等級及應用分類) 頁岩氣市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年)

頁岩氣市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年) 頁岩氣市場:按技術、應用和地區分類

頁岩氣市場:按技術、應用和地區分類 2026年全球頁岩氣市場報告

2026年全球頁岩氣市場報告 頁岩氣市場規模、佔有率及成長分析(按技術、應用及地區分類)-2026-2033年產業預測

頁岩氣市場規模、佔有率及成長分析(按技術、應用及地區分類)-2026-2033年產業預測 2025-2029年全球頁岩氣市場

2025-2029年全球頁岩氣市場 頁岩氣市場-全球產業規模、佔有率、趨勢、機會及預測(細分領域、按應用、按最終用戶、按開採方式、按地區及競爭格局,2020-2030 年預測)

頁岩氣市場-全球產業規模、佔有率、趨勢、機會及預測(細分領域、按應用、按最終用戶、按開採方式、按地區及競爭格局,2020-2030 年預測) 2032 年頁岩氣市場預測:按產品類型、技術、應用、最終用戶和地區進行的全球分析頁岩氣 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)

2032 年頁岩氣市場預測:按產品類型、技術、應用、最終用戶和地區進行的全球分析頁岩氣 -市場佔有率分析、產業趨勢/統計、成長預測(2025-2030)