|

市場調查報告書

商品編碼

2064401

雞蛋包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Egg Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

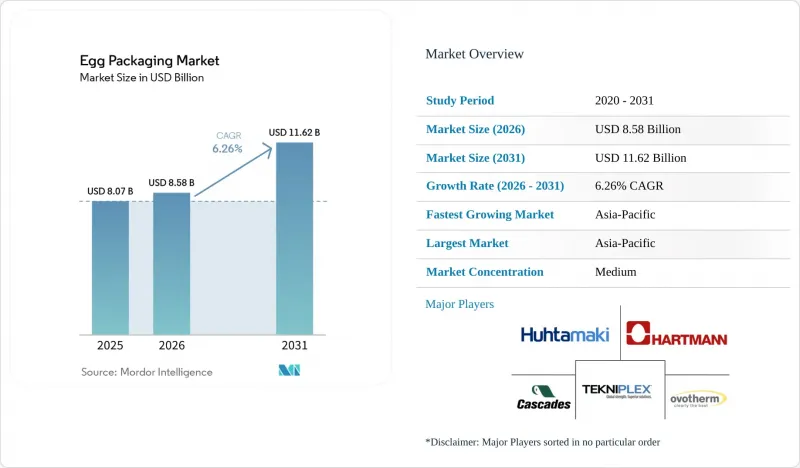

根據 Mordor Intelligence 預測,雞蛋包裝市場規模預計在 2025 年達到 80.7 億美元,2026 年達到 85.8 億美元,到 2031 年達到 116.2 億美元,2026 年至 2031 年的複合年成長率為 6.26%。

本報告按產品類型(紙盒、托盤、容器等)、材料類型(塑膠、紙張、模塑纖維等)、分銷管道(超級市場/大賣場、便利商店、線上零售、專賣店)和地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。市場預測以美元計價。

全球雞蛋包裝市場趨勢及洞察

全球雞蛋消費量和家禽產量增加

2023年全球雞蛋產量超過9,100萬噸,儘管部分產區出現雞群損失,但雞蛋包裝需求仍強勁。亞洲佔全球雞蛋產量的70%以上,中國佔全球近一半的產量,亞洲也持續是包裝需求成長的中心。根據經合組織-糧農組織《2025-2034年農業展望》,中低收入國家肉類、乳製品和雞蛋的蛋白質消費量預計將持續成長,隨著零售體系的改善,這將進一步推動包裝需求。 2023年,印度是世界第二大雞蛋生產國(佔8%),由於散裝銷售向零售包裝銷售的轉變,其包裝使用量的成長速度超過了僅由產量成長所預期的速度。此外,2022 年至 2024 年的高致病性禽流感 (HPAI) 疫情改變了貿易流向,提高了標準化防護包裝在跨國運輸中的作用,並強化了雞蛋包裝市場的長期需求趨勢。

加快向模塑纖維和可回收包裝的過渡

隨著零售商、監管機構和消費者越來越重視可回收和低塑膠包裝,雞蛋包裝市場正向模塑纖維和紙基包裝轉型。在歐盟,行銷和包裝法規不斷加重傳統塑膠包裝的合規負擔,推動雞蛋包裝盒向纖維性替代品的更廣泛轉型。 2024年,德國雞蛋產量增加了4.2%,其中自由放養和有機雞蛋的產量也呈現成長趨勢。這促進了注重高階和永續性的貨架包裝形式的發展。在日本,政策主導的包裝轉型也在推進,由於塑膠資源回收措施和零售商的脫碳計劃,模塑紙漿包裝越來越受到關注。 2024年6月,Cascade公司推出“Fresh GUARD EnVision”,進一步強化了這一趨勢。本產品採用模塑紙漿基材和再生紙板套相結合的混合設計。這表明,雞蛋包裝市場正在超越簡單的材料一對一轉換,走向一體化、永續的包裝形式。

紙漿、再生紙和樹脂的價格波動

原料成本波動仍然是雞蛋包裝市場最明顯的業務限制因素之一。這是因為纖維、紙張和塑膠的價格波動對加工商利潤率的影響速度遠遠超出與客戶調整合約條款的速度。 Fastmarkets 的報告顯示,歐洲紙包裝成本指數在 2025 年之前持續飆升,反映出能源和纖維原物料價格正以對包裝製造商不利的速度快速上漲。在北美,Packaging Dive 的報告指出,到 2025 年,箱板紙價格每噸上漲高達 70 美元,持續對瓦楞紙板和紙包裝的獲利能力構成壓力。 PaperIndex 也指出,紙漿通常佔牛皮紙生產成本的 40% 至 60%。這解釋了為什麼即使纖維價格短期上漲也會立即影響造紙廠的出貨價格和加工商的利潤率。如果這種週期持續更長時間,小規模的區域性加工商將更加脆弱。這是因為他們通常購買力和避險能力較低,而且在雞蛋包裝市場中調整原料平衡的選擇也較少。

細分市場分析

截至2025年,紙盒佔雞蛋包裝市場佔有率的59.16%,但預計從2026年到2031年,托盤的複合年成長率將達到7.63%,成為成長最快的包裝形式。紙盒憑藉其強大的品牌認知度、便於消費者使用以及與超級市場、大賣場和專賣店貨架的廣泛兼容性,在零售主導的供應鏈中仍然扮演著核心角色。托盤的快速普及主要得益於30枚裝運輸方式在從農場到分揀、供應餐飲服務業以及散養和自由放養系統中大批量加工等方面的廣泛應用。高速分類設備也在影響產品設計。例如,SANOVO的OptiGrader 600每小時可處理多達21.6萬枚雞蛋,這就要求包裝具有尺寸穩定性和可靠的拆箱性能。容器和其他形式的包裝仍然存在於高階和特殊產品項目中,但預計在預測期內不會改變雞蛋包裝市場的整體結構。

從營運角度來看,一個關鍵的考慮因素是,與傳統的籠養方式相比,放養系統往往會導致雞蛋尺寸差異更大,因此在初始搬運階段,具有更優異減震性能的托盤形狀更為重要。這一趨勢支撐了對托盤的需求,甚至在雞蛋進入品牌零售包裝之前就已存在,這表明推動成長的並非促銷偏好,而是生產實踐中固有的因素。在雞蛋包裝市場,產品開發也正在向混合結構轉變,將運輸過程中的保護與品牌產品的展示效果結合在一個包裝中。 Cascade 的「Fresh GUARD EnVision」產品體現了這一方向,它將模塑紙漿基材與塗層再生紙板套筒相結合,表明托盤和紙盒的功能在高價值包裝形式中開始融合。因此,雞蛋包裝行業越來越重視那些能夠減少換型次數、支援自動化,並在無需額外包裝系統的情況下滿足零售展示和分銷保護需求的包裝設計。

區域分析

預計到2025年,亞太地區將佔據全球雞蛋包裝市場42.64%的佔有率,並在2031年之前以7.38%的複合年成長率持續成長。根據聯合國糧農組織的數據,中國約佔全球雞蛋產量的49%,仍是核心市場,為該地區提供了龐大的托盤和紙盒國內需求。印度以8%的產量位居全球第二,其銷售模式正從散裝銷售轉向有組織的零售包裝銷售,從而在都市區和郊區配銷通路中催生了結構性的包裝需求。另一方面,日本的需求模式則有所不同,由於政策壓力限制塑膠的使用以及零售商的脫碳計劃,模塑包裝和紙質包裝的使用率不斷提高。在整個亞太雞蛋包裝市場,有組織的零售和日益增強的食品安全意識正逐步推動銷售模式從散裝托盤轉向帶有標籤的消費者包裝。

儘管北美和歐洲在銷售上落後於亞太地區,但由於其完善的可追溯性、非籠養模式的推廣以及高階銷售標準,它們仍然是雞蛋包裝市場價值最高的地區之一。德國的雞蛋產量在2024年成長了4.2%,達到137億枚,其中自由放養和有機雞蛋產量的強勁成長支撐了對高階模塑纖維包裝的需求。在歐洲,監管趨勢持續推動更嚴格的生產和標籤標準。同時,在美國,FDA的可追溯性框架持續向包裝供應商施壓,要求其支援批號和追蹤功能。美國多個州於2025年生效的非籠養立法也促進了對與動物福利聲明和差異化零售定位相關的高價值紙盒的需求。

南美洲、中東和非洲雖然與成熟市場相比包裝滲透率仍然較低,且存在顯著的區域差異,但它們代表著雞蛋包裝市場下一個結構性成長前沿。巴西和阿根廷受益於超級市場的擴張、低溫運輸的改善以及都市區消費的成長,這些因素共同推動了雞蛋銷售從散裝銷售向小型獨立包裝銷售的轉變。在中東,國內家禽自給自足計劃和出口主導的貿易流動增加了對標準化保護性包裝的需求。此外,土耳其在2025年緊急雞蛋出口中所扮演的角色表明,貿易中斷如何迅速擴大對便於運輸包裝的需求。在非洲,儘管商業性家禽養殖業正在擴張,但基礎設施的不平衡和有限的再生纖維生產能力意味著低成本塑膠包裝在短期內仍將佔據主導地位,儘管在預測期的後半段,模塑纖維產品仍有成長空間。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球雞蛋消費量和家禽產量增加

- 向模塑纖維和可回收包裝的過渡正在加速。

- 現代食品零售業的擴張和網路食品配送的成長。

- 加強對食品安全、標籤和可追溯性的要求。

- 對放養、有機和功能性雞蛋的優質包裝需求增加

- 用於高速分類和履約的自動化包裝設計。

- 市場限制因素

- 紙漿、再生紙和樹脂的價格波動

- 為遵守有關食品接觸材料和包裝廢棄物的法規而增加的成本

- 禽流感導致雞蛋供應和紙盒需求波動

- 食品接觸用PCR短缺及審核瓶頸

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 紙盒

- 托盤

- 容器

- 其他產品類型

- 材料類型

- 塑膠

- 紙

- 模塑纖維

- 其他材料類型

- 透過分銷管道

- 超級市場和大賣場

- 便利商店

- 線上零售

- 專賣店

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 澳洲和紐西蘭

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Hartmann Packaging A/S

- Huhtamaki Oyj

- Tekni-Plex, Inc.

- Cascades Inc.

- Ovotherm International Handels GmbH

- CKF Inc.

- Primapack

- EUROPACK, as

- Dispak Ltd.

- Omni-Pac Group

- Nippon Molding Co., Ltd.

- GREENLINK GROUP CORP.

- Keyes Packaging Group

- Eipack Barneveld BV

- Eggbox GmbH

- EnviroPAK Corporation

- Henry Molded Products, Inc.

- Carton Packaging Pty Ltd

第7章 市場機會與未來展望

According to Mordor Intelligence, the egg packaging market size is projected to be USD 8.07 billion in 2025, USD 8.58 billion in 2026, and reach USD 11.62 billion by 2031, growing at a CAGR of 6.26% from 2026 to 2031.

This report is Segmented by Product Type (Cartons, Trays, Containers, and More), Material Type (Plastic, Paper, Molded Fiber, and More), Distribution Channel (Supermarkets and Hypermarkets, Convenience Stores, Online Retail, and Specialty Stores), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Egg Packaging Market Trends and Insights

Rising Global Egg Consumption and Poultry Output

Global hen egg production exceeded 91 million MT in 2023, which kept the base demand floor for the egg packaging market broad, even when flock losses affected some producing regions. Asia accounted for more than 70% of global egg output, and China alone accounted for nearly half of global production, keeping Asia at the center of packaging demand growth. The OECD-FAO Agricultural Outlook 2025-2034 stated that protein consumption from meat, dairy, and eggs will continue rising in lower-middle-income countries, which supports additional packaging demand as retail systems formalize. India ranked second globally in egg production in 2023, with an 8% share, and its shift from loose egg sales to packaged retail formats is increasing packaging intensity faster than production alone would suggest. HPAI also changed trade flows between 2022 and 2024, increasing the role of standardized protective packs in cross-border shipments and strengthening the long-term demand profile of the egg packaging market.

Accelerating Shift Toward Molded Fiber and Recyclable Packs

The egg packaging market is moving toward molded fiber and paper-based formats as retailers, regulators, and consumers place greater emphasis on recyclable, lower-plastic packaging. In the European Union, marketing and packaging rules have continued to increase the compliance burden on conventional plastic formats, supporting a broader migration toward fiber-based alternatives in egg packs. Germany reported a 4.2% increase in egg production in 2024, while free-range and organic output also grew, which supported formats that better match premium and sustainability-led shelf positioning. Japan has also been moving through a policy-led packaging transition, with plastic resource circulation measures and retailer decarbonization programs drawing more attention to molded pack formats. Cascades reinforced this direction in June 2024 when it launched Fresh GUARD EnVision, a hybrid design that combines a molded pulp base with a recycled-board sleeve, showing that the egg packaging market is moving toward integrated sustainable formats rather than a simple one-for-one material switch.

Pulp, Recycled Paper, and Resin Price Volatility

Input cost volatility remains one of the clearest operating restraints in the egg packaging market because fiber, paper, and resin swings can pass through converter margins faster than customer contracts adjust. Fastmarkets reported a sharp rise in European paper packaging cost indices during 2025, which reflected how quickly energy and fiber inputs can move against pack producers. In North America, Packaging Dive reported containerboard price increases of up to USD 70 per ton entering 2025, which continued to put pressure on corrugated and paper-based packaging economics. PaperIndex also noted that pulp commonly accounts for 40-60% of kraft paper production costs, which explains why even short spikes in fiber pricing quickly affect mill-gate economics and converter margins. Smaller regional converters are more exposed when these cycles persist, because they usually have less buying leverage, less hedging capacity, and fewer options to rebalance between materials within the egg packaging market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Modern Grocery Retail and Online Grocery Fulfillment

- Tightening Food Safety, Labeling, and Traceability Requirements

- Rising Compliance Costs for Food-Contact and Packaging-Waste Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cartons held 59.16% of the egg packaging market share in 2025, while trays are projected to record the fastest CAGR at 7.63% from 2026 to 2031. Cartons remain central to retail-led supply chains because they offer strong brand visibility, familiar consumer handling, and broad compatibility across supermarket, hypermarket, and specialty shelf formats. Trays are gaining popularity faster because cage-free and free-range systems rely heavily on 30-egg transport formats for farm-to-grader movement, food-service supply, and higher-volume handling. High-speed grading equipment is also shaping product design, as SANOVO's OptiGrader 600 can process up to 216,000 eggs per hour and therefore requires packs with stable dimensions and reliable denesting performance. Containers and other formats remain present in premium and specialty programs, but they do not alter the broad structure of the egg packaging market during the forecast period.

What matters operationally is that cage-free systems often produce wider egg-size variation than conventional cage operations, which makes shock-absorbing tray geometry more useful in earlier handling stages. That pattern supports tray demand even before eggs reach branded retail packs, so the growth driver is embedded in production practices rather than in merchandising preferences. Within the egg packaging market, product development is also moving toward hybrid structures that combine transport protection with branded shelf appeal in a single pack. Cascades illustrated that direction with Fresh GUARD EnVision, which paired a molded pulp base with a coated recycled-board sleeve and showed how tray and carton functions are starting to overlap in higher-value formats. The egg packaging industry is therefore placing more value on designs that can reduce changeovers, support automation, and serve both retail presentation and distribution protection without forcing separate packaging systems.

Geography Analysis

Asia-Pacific held 42.64% of the egg packaging market share in 2025 and is projected to expand at a 7.38% CAGR through 2031. China remained the core anchor because FAO data showed it accounted for nearly 49% of global egg production, providing the region with a very large domestic demand base for trays and cartons. India ranked second globally with an 8% share of output, and its ongoing move from loose egg sales toward organized packaged retail is adding structural packaging demand in urban and peri-urban channels. Japan has a different demand profile, as policy pressure on plastic use and retailer decarbonization programs are driving greater adoption of molded packs and paper-based formats. Across the wider Asia-Pacific egg packaging market, retail formalization and food-safety awareness are gradually converting open-tray sales into labeled consumer packs.

North America and Europe did not match Asia-Pacific in volume, but they remained among the highest-value parts of the egg packaging market because traceability, cage-free conversion, and premium merchandising standards were already well established. Germany's egg production rose 4.2% in 2024 to 13.7 billion eggs, with stronger growth in free-range and organic output, which supported demand for premium molded-fiber formats. In Europe, the regulatory path continued to support tighter production and labeling standards, while in the United States the FDA traceability framework kept pressure on packaging suppliers to support lot coding and tracking capability. Several U.S. state cage-free laws that took effect in 2025 also supported stronger demand for higher-value cartons tied to animal welfare claims and differentiated retail positioning.

South America, the Middle East, and Africa represent the next structural growth frontier for the egg packaging market, even though packaging penetration remains lower and more uneven than in mature markets. Brazil and Argentina are benefiting from supermarket expansion, cold-chain improvement, and urban consumption growth, which together support movement from bulk presentation toward pre-packed formats. In the Middle East, domestic poultry self-sufficiency programs and export-led trade flows are strengthening the need for standardized protective packaging, and Turkey's role in emergency egg exports during 2025 showed how trade disruptions can quickly expand demand for transport-ready pack formats. In Africa, commercial poultry operations are expanding, but infrastructure gaps and limited recycled fiber capacity still favor lower-cost plastic formats in the near term while leaving room for molded-fiber growth later in the forecast period.

- Hartmann Packaging A/S

- Huhtamaki Oyj

- Tekni-Plex, Inc.

- Cascades Inc.

- Ovotherm International Handels GmbH

- CKF Inc.

- Primapack

- EUROPACK, a.s.

- Dispak Ltd.

- Omni-Pac Group

- Nippon Molding Co., Ltd.

- GREENLINK GROUP CORP.

- Keyes Packaging Group

- Eipack Barneveld B.V.

- Eggbox GmbH

- EnviroPAK Corporation

- Henry Molded Products, Inc.

- Carton Packaging Pty Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Egg Consumption and Poultry Output

- 4.2.2 Accelerating Shift Toward Molded Fiber and Recyclable Packs

- 4.2.3 Expansion of Modern Grocery Retail and Online Grocery Fulfillment

- 4.2.4 Tightening Food Safety, Labeling, and Traceability Requirements

- 4.2.5 Premium Packaging Demand for Cage-Free, Organic, and Functional Eggs

- 4.2.6 Automation-Ready Pack Designs for High-Speed Grading and Fulfillment

- 4.3 Market Restraints

- 4.3.1 Pulp, Recycled Paper, and Resin Price Volatility

- 4.3.2 Rising Compliance Costs for Food-Contact and Packaging-Waste Rules

- 4.3.3 Avian Influenza-Driven Egg Supply Swings and Carton Demand Volatility

- 4.3.4 Food-Contact PCR Scarcity and Approval Bottlenecks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Cartons

- 5.1.2 Trays

- 5.1.3 Containers

- 5.1.4 Other Product Types

- 5.2 By Material Type

- 5.2.1 Plastic

- 5.2.2 Paper

- 5.2.3 Molded Fiber

- 5.2.4 Other Material Types

- 5.3 By Distribution Channel

- 5.3.1 Supermarkets and Hypermarkets

- 5.3.2 Convenience Stores

- 5.3.3 Online Retail

- 5.3.4 Specialty Stores

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Hartmann Packaging A/S

- 6.4.2 Huhtamaki Oyj

- 6.4.3 Tekni-Plex, Inc.

- 6.4.4 Cascades Inc.

- 6.4.5 Ovotherm International Handels GmbH

- 6.4.6 CKF Inc.

- 6.4.7 Primapack

- 6.4.8 EUROPACK, a.s.

- 6.4.9 Dispak Ltd.

- 6.4.10 Omni-Pac Group

- 6.4.11 Nippon Molding Co., Ltd.

- 6.4.12 GREENLINK GROUP CORP.

- 6.4.13 Keyes Packaging Group

- 6.4.14 Eipack Barneveld B.V.

- 6.4.15 Eggbox GmbH

- 6.4.16 EnviroPAK Corporation

- 6.4.17 Henry Molded Products, Inc.

- 6.4.18 Carton Packaging Pty Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

雞蛋包裝市場成長機會、成長要素、產業趨勢分析及2026-2035年預測。

雞蛋包裝市場成長機會、成長要素、產業趨勢分析及2026-2035年預測。 雞蛋盒和托盤市場規模、佔有率和趨勢分析報告:按分銷管道、應用、材料、產品類型、地區和細分市場預測(2026-2033 年)

雞蛋盒和托盤市場規模、佔有率和趨勢分析報告:按分銷管道、應用、材料、產品類型、地區和細分市場預測(2026-2033 年) 模塑纖維蛋盒:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

模塑纖維蛋盒:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 2026-2030年全球雞蛋包裝市場

2026-2030年全球雞蛋包裝市場 雞蛋包裝市場報告:按產品類型、材料、應用和地區分類(2026-2034 年)

雞蛋包裝市場報告:按產品類型、材料、應用和地區分類(2026-2034 年) 雞蛋包裝市場:全球市場預測(按產品類型、材料類型、包裝類型、分銷管道和最終用途分類)- 2026-2032年

雞蛋包裝市場:全球市場預測(按產品類型、材料類型、包裝類型、分銷管道和最終用途分類)- 2026-2032年 2026年全球雞蛋托盤市場報告

2026年全球雞蛋托盤市場報告 雞蛋包裝市場規模、佔有率和成長分析(按材料類型、包裝類型、雞蛋品種和地區分類)-2026-2033年產業預測

雞蛋包裝市場規模、佔有率和成長分析(按材料類型、包裝類型、雞蛋品種和地區分類)-2026-2033年產業預測 全球雞蛋包裝市場全球雞蛋托盤市場

全球雞蛋包裝市場全球雞蛋托盤市場