|

市場調查報告書

商品編碼

2064377

員工體驗平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Employee Experience Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

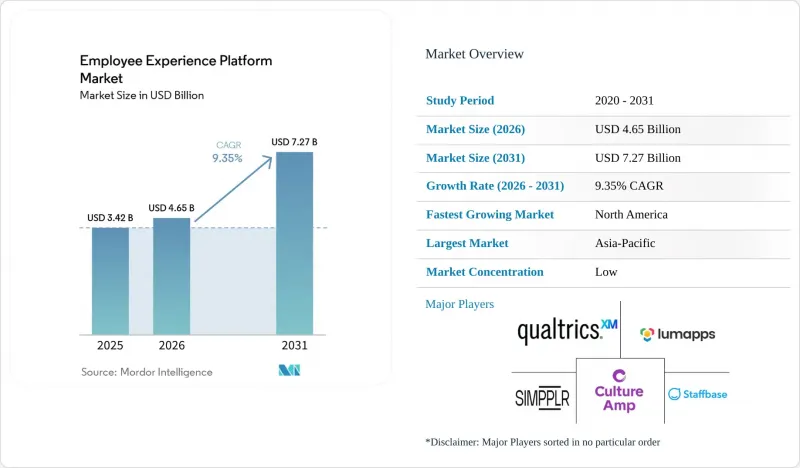

根據 Mordor Intelligence 預測,員工體驗平台市場規模預計在 2025 年達到 34.2 億美元,在 2026 年達到 46.5 億美元,在 2031 年達到 72.7 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 9.35%。

本報告按部署方式(雲端部署、本地部署等)、公司規模(中小企業、大型企業)、應用領域(員工溝通與協作、員工敬業度與獎勵等)、最終用戶行業(銀行、金融服務和保險、醫療保健、IT和電信等)以及地區進行細分。市場預測以美元計價。

全球員工體驗平台市場趨勢與洞察。

建立混合式和分散式工作模式

混合辦公已成為大型企業的標準商業模式,員工體驗平台市場的發展與工作場所的重新設計密切相關,而非曇花一現的流行。一項2025年的全球調查發現,雖然88%的雇主提供某種形式的混合辦公,但只有32%的雇主對協作技術進行了充分的投資,這為平台供應商填補市場空白留下了明顯的空間。調查也顯示,90%的員工重視協作工具,77%的員工認為嚴格的返崗要求反映了他們對遠距辦公效率缺乏信心。這種差距迫使人力資源和IT團隊推動共用平台的普及,以改善跨站點的溝通、回饋和存取。此外,歐洲退休潮帶來的勞動力短缺壓力也推動了員工體驗平台市場的發展。在德語區(德國、奧地利和瑞士),預計到2030年代中期將有1,290萬名嬰兒潮世代退休,這將提升人才保留基礎設施的價值。因此,買家不再僅僅將員工體驗工具視為員工敬業度軟體,而是將其視為員工留任計畫的一部分。

人工智慧驅動的個人化和員工自助服務

人工智慧驅動的個人化正在將平台從被動的調查工具轉變為主動的系統,能夠即時路由請求、推薦內容並解決常見的人力資源任務。這項轉變意義重大,因為企業現在期望職場工具更快、更相關、更易於在日常工作流程中使用。例如,一個平台在2024年處理了超過1150萬次交互,其中94%的問題在系統內得到解決,並帶來了35億美元的生產力提升和成本節約,充分展現了精心構建的自助服務模式所能創造的巨大價值。這些成果正在影響員工體驗平台市場的買家預期,尤其是對於那些需要在不增加支援人員的情況下支援更多員工的人力資源團隊而言。這些成果也促使供應商將管治功能與治理控制結合,從而在不產生新風險的情況下實現自動化規模化。因此,市場對能夠將監聽功能、工作流程自動化和人工智慧驅動的自助服務整合到單一營運層的平台的需求日益成長。

資料隱私和系統整合的複雜性

資料隱私和整合的複雜性持續阻礙員工體驗平台市場的發展,尤其是在平台需要同時從多個系統獲取情緒、行為和績效資料的情況下。歐洲買家對人工智慧驅動的監聽和分析功能採取了更嚴格的審查標準,導致部署前需要更長的法律和技術檢驗期。此外,整合難度也超出了許多買家的預期,因為人力資源資訊系統 (HRIS)、協作系統、薪資系統、績效系統和安全系統通常以不同的格式儲存員工數據,並採用不同的權限設定。這導致許多專案在從試點運行過渡到全公司部署的過程中出現延誤。對於跨境營運的組織而言,這種影響尤其顯著,因為資料儲存位置、本地託管以及員工代表委員會的期望都會影響部署設計。提供「隱私設計」控制措施和更精簡的整合框架的供應商,則更有能力將這些限制轉化為採購優勢。

細分市場分析

到2025年,雲端平台將佔據員工體驗平台市場67.42%的佔有率,反映出支援分散式團隊和促進現代人力資源系統間持續資料交換的需求。雲端採用符合員工體驗平台市場的當前發展方向,因為它能夠實現更快的更新、更便利的整合以及更廣泛的跨地域存取。此外,它還為供應商提供了更強大的基礎,使其能夠建立基於即時資料流的AI驅動型監聽、工作流程自動化和分析功能。對於希望透過單一整合架構運作溝通、回饋、評估和支援工具的組織而言,這項優勢尤其重要。本地部署仍然重要,但其應用範圍正日益局限於某些特定情況,在這些情況下,嚴格的網路隔離和高度專業化的內部控制比雲端模式的柔軟性更為重要。

混合部署模式是成長最快的模式,複合年成長率高達 11.38%,這表明買家仍然希望對敏感員工資料的儲存位置擁有更大的控制權。隨著受監管行業和大型企業尋求在資料居住要求和基於雲端的分析需求之間取得平衡,混合部署的員工體驗平台市場正在不斷擴大。這一點在歐洲市場尤其明顯,當地對本地託管的偏好持續影響採購方案的設計。發展方向仍然是“雲端優先”,但並非“不惜一切代價只依賴雲端”,而是“雲端優先”並輔以更強大的管治機制。

到2025年,大型企業將佔據員工體驗平台市場62.19%的佔有率。這反映了它們需要管理跨業務部門、跨地區、跨多層級匯報結構的大規模員工隊伍。這些企業通常需要與人力資源資訊系統 (HRIS)、學習管理系統、薪資核算管理系統、績效評估系統和身分管理系統進行深度整合,這增加了實施的範圍和成本。這種複雜性有利於那些擁有更強大的實施能力、更廣泛的產品套件和清晰的管治控制的供應商。這也是為什麼儘管有新的買家加入,大型企業仍然是員工體驗平台市場的主要收入來源。通常,這些企業購買的並非單一功能,而是能夠連結溝通、傾聽、獎勵和管理工作流程的整合系統。

中小企業是成長最快的細分市場,預計到2031年複合年成長率將達到12.74%,這表明成本和採用門檻正在降低。員工體驗平台市場的中小企業佔有率正在擴大,模組化、雲端原生產品降低了擁有100至2000名員工的企業的進入門檻。這些買家正在尋求應對日益激烈的競爭和不斷提高的員工期望,尤其是在那些小規模企業過去主要依靠非正式企業文化來留住人才的行業。能夠透過單一產品架構滿足企業和中型市場需求的供應商,無需建立單獨的平台即可輕鬆擴展業務。

區域分析

到2025年,北美將佔據員工體驗平台市場36.91%的佔有率,成為最大的區域叢集。該地區受益於企業軟體的高普及率、成熟的人力資源技術基礎以及眾多支持混合辦公和知識密集型員工隊伍的供應商。雖然美國仍然是主要的收入來源,但隨著雇主在其北美業務中實現平台標準化,加拿大和墨西哥也為市場擴張提供了支持。該市場的需求也從基本的員工敬業度調查轉向人員流動預測、人工智慧驅動的管理工具以及更廣泛的勞動力分析。技術服務、商業服務以及金融和保險業是混合辦公模式普及率最高的行業之一,這推動了對平台驅動的員工溝通和協作的需求。

亞太地區是成長最快的地區,預計到2031年複合年成長率將達到14.87%。亞太市場規模的擴張得益於企業快速數位轉型、行動優先的勞動力策略以及製造業、零售業和物流業對現場工作人員的巨大未滿足需求。印度龐大的IT服務基礎設施持續支持用於提升員工敬業度和績效的工具的普及,而中國和韓國對現場通訊平台的興趣也日益濃厚。這些區域趨勢為市場提供了更廣泛的成長基礎,使其不再局限於辦公室主導的應用。

在德國、英國、法國、荷蘭和西班牙的支持下,歐洲仍保持第二大區域叢集的地位。該地區之所以脫穎而出,是因為員工體驗、資料管治和報告需求在採購決策中日益緊密地交織在一起。 ESRS S1框架要求披露員工信息,重點關注工作條件、培訓、多元化和福祉,這推動了對能夠持續收集和整理員工數據的系統的需求。南美洲仍然是一個發展中的市場,巴西和阿根廷的金融和專業服務業發展活躍。在中東,隨著大型企業員工在地化專案和計畫的興起,對系統化入職和溝通的需求日益成長,投資也不斷擴大。另一方面,非洲仍處於起步階段,南非和奈及利亞是跨國營運公司的重要入口。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 建立混合式和分散式工作模式

- 人工智慧驅動的個人化和員工自助服務

- 重點關注董事會層面的員工留任率和生產力指標。

- 現場工作人員數位化

- 根據 CSRD 和 ESRS S1 揭露員工資訊的準備情況

- 使技能圖譜與內部人才流動性相匹配

- 市場限制因素

- 資料隱私和系統整合的複雜性

- ROI歸因分析和變化疲勞

- 歐盟人工智慧法及對工人代表委員會監督職能的限制

- 商品搭售和生態系統鎖定壓力

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按部署模式

- 基於雲端的

- 現場

- 混合

- 按最終用戶公司規模分類

- 小型企業

- 大公司

- 透過使用

- 員工溝通與協作

- 員工敬業度和獎勵

- 員工訪談與分析

- 員工福祉與支持

- 其他用途

- 按最終用戶行業分類

- 銀行、金融服務和保險業 (BFSI)

- 醫學與生命科學

- 資訊科技/通訊

- 零售與電子商務

- 工業製造

- 政府/公共部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Qualtrics, LLC

- Culture Amp Pty Ltd

- Perceptyx, Inc.

- Medallia, Inc.

- WorkTango Inc.

- Achievers Solutions Inc.

- Lattice, Inc.

- 15Five, Inc.

- Quantum Workplace, Inc.

- Motivosity, Inc.

- Staffbase GmbH

- Simpplr Inc.

- LumApps SAS

- Unily Group Ltd.

- MangoApps Inc.

- Haiilo GmbH

- Firstup, Inc.

- Appspace Inc.

- Akumina, Inc.

- Powell Software Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the employee experience platform market size is projected to be USD 3.42 billion in 2025, USD 4.65 billion in 2026, and reach USD 7.27 billion by 2031, growing at a CAGR of 9.35% from 2026 to 2031.

This report is Segmented by Deployment Model (Cloud-Based, On-Premises, and More), Enterprise Size (Small and Medium-Sized Enterprises, and Large Enterprises), Application (Employee Communication and Collaboration, Employee Engagement and Recognition, and More), End-User Industry (BFSI, Healthcare, IT and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Employee Experience Platform Market Trends and Insights

Hybrid And Distributed Work Normalization

Hybrid work has become a standard operating model across large employers, tying the employee experience platform market to workplace redesign rather than a short-lived adoption wave. A 2025 global study found that 88% of employers offered some form of hybrid work, while only 32% invested adequately in collaboration technology, leaving a clear gap for platform vendors to fill. The same study showed that 90% of employees value collaboration tools and 77% view strict return-to-office mandates as a sign of low trust in remote productivity. This gap is pushing HR and IT teams to support shared platforms that improve communication, feedback, and access across locations. The employee experience platform market is also benefiting from retirement-driven labor pressure in Europe, where 12.9 million baby boomers in the DACH region are moving toward retirement through the mid-2030s, which raises the value of retention infrastructure. As a result, buyers are treating employee experience tools as part of workforce continuity planning, not just as engagement software.

AI-Powered Personalization And Employee Self-Service

AI personalization is moving platforms away from passive survey tools and toward active systems that route requests, recommend content, and resolve common HR tasks in real time. This shift matters because organizations now expect workplace tools to feel faster, more relevant, and easier to use across daily workflows. A platform example showed it handled more than 11.5 million interactions in 2024, resolving 94% of them within the system, and contributed USD 3.5 billion in productivity savings, demonstrating the scale of value that well-built self-service models can unlock. These results are shaping buyer expectations inside the employee experience platform market, especially where HR teams are under pressure to serve larger workforces without adding support headcount. They are also pushing vendors to connect personalization features with governance controls so that automation can scale without creating new risk. The result is a stronger demand for platforms that combine listening, workflow automation, and AI-assisted self-service into a single operating layer.

Data Privacy And Cross-System Integration Complexity

Data privacy and integration complexity continue to slow the employee experience platform market, especially when platforms pull sentiment, behavioral, and performance data from many systems at once. Buyers in Europe are applying stricter review standards to AI-enabled listening and analytics features, which extends legal and technical validation before rollout. Integration work is also heavier than many buyers first expect, because HRIS, collaboration, payroll, performance, and security systems often store workforce data in different formats and under different permissions. This creates delays at the point where many projects move from pilot use into enterprise-wide deployment. The effect is strongest in organizations that operate across borders, where data residency, local hosting, and works council expectations all shape implementation design. Vendors that offer privacy-by-design controls and cleaner integration frameworks are better placed to convert this restraint into a procurement advantage.

Other drivers and restraints analyzed in the detailed report include:

- Board-Level Focus On Retention And Productivity Metrics

- Frontline Workforce Digitization

- ROI Attribution And Change Fatigue

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based platforms held 67.42% of the employee experience platform market share in 2025, which reflects the need to support distributed teams and continuous data exchange across modern HR systems. Cloud deployment aligns with the current direction of the employee experience platform market by enabling faster updates, easier integration, and broader access across locations. It also provides vendors with a stronger foundation for AI-enabled listening, workflow automation, and analytics features that depend on real-time data flow. That advantage is especially important for organizations that want communication, feedback, recognition, and support tools to operate through one connected architecture. On-premises deployments remain relevant, but they are increasingly tied to narrow cases where strict network isolation or highly specific internal controls outweigh the flexibility of cloud models.

Hybrid deployment is the fastest-growing model, with a 11.38% CAGR, indicating that buyers still want greater control over where sensitive workforce data is stored. The employee experience platform market for hybrid deployment is growing as regulated industries and large enterprises seek to balance data residency requirements with the need for cloud-based analytics. This is especially visible in European markets where local hosting preferences continue to shape procurement design. The direction of travel is still cloud-first, but it is cloud-first with stronger governance layers rather than cloud-only at any cost.

Large enterprises captured 62.19% of the employee experience platform market in 2025, which reflects their need to manage large workforces across business units, geographies, and layered reporting structures. These organizations typically require deep integration with HRIS, learning, payroll, performance, and identity systems, which raises both the scope and cost of deployment. That complexity favors vendors with stronger implementation capacity, broader product suites, and clearer governance controls. It also explains why large enterprises remain the core revenue base of the employee experience platform market even as new buyers enter. In many cases, these organizations are not buying a single feature but a connected system that ties communication, listening, recognition, and manager workflows together.

Small and medium-sized enterprises are the fastest-growing cohort, with a CAGR of 12.74% through 2031, indicating that cost and setup barriers are easing. The employee experience platform market size for SMEs is growing as modular cloud-native products lower entry thresholds for companies with 100-2,000 employees. These buyers are responding to tighter labor competition and higher employee expectations, especially in sectors where smaller firms once depended on informal culture as their main retention tool. Vendors that can serve enterprise and mid-market needs with a single product architecture are in a stronger position to expand without building separate platforms.

Geography Analysis

North America held 36.91% of the employee experience platform market share in 2025, making it the largest regional cluster. The region benefits from high enterprise software adoption, a mature HR technology base, and a dense concentration of vendors serving hybrid and knowledge-based workforces. The United States remained the main revenue center, while Canada and Mexico supported expansion as employers standardized platforms across North American operations. Demand in this part of the market is also moving from basic engagement surveys toward predictive attrition, AI-supported manager tools, and broader workforce analytics. Technology services, business services, and finance and insurance had among the highest hybrid adoption rates, supporting continued demand for platform-enabled employee communication and coordination.

Asia-Pacific is the fastest-growing region with a CAGR of 14.87% through 2031. Market size in Asia-Pacific is rising on the back of rapid enterprise digitization, mobile-first workforce strategies, and significant unmet demand among frontline workers in manufacturing, retail, and logistics. India's large IT services base continues to support the adoption of engagement and performance tools, while China and South Korea are driving stronger interest in frontline communication platforms. This regional pattern provides the market with a broader growth base beyond office-led deployments.

Europe remained the second-largest regional cluster, supported by Germany, the United Kingdom, France, the Netherlands, and Spain. The region stands out because workforce experience, data governance, and reporting needs are becoming more closely linked in buying decisions. The ESRS S1 framework keeps workforce disclosures focused on working conditions, training, diversity, and well-being, which reinforces demand for systems that can collect and organize employee data more consistently. South America is still a developing market, with Brazil and Argentina showing stronger activity in financial and professional services. The Middle East is seeing more investment as workforce localization programs and large-employer projects increase the need for structured onboarding and communication, while Africa remains early-stage, with South Africa and Nigeria serving as the main entry points for cross-border employers.

- Qualtrics, LLC

- Culture Amp Pty Ltd

- Perceptyx, Inc.

- Medallia, Inc.

- WorkTango Inc.

- Achievers Solutions Inc.

- Lattice, Inc.

- 15Five, Inc.

- Quantum Workplace, Inc.

- Motivosity, Inc.

- Staffbase GmbH

- Simpplr Inc.

- LumApps SAS

- Unily Group Ltd.

- MangoApps Inc.

- Haiilo GmbH

- Firstup, Inc.

- Appspace Inc.

- Akumina, Inc.

- Powell Software Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hybrid and Distributed Work Normalization

- 4.2.2 AI-Powered Personalization and Employee Self-Service

- 4.2.3 Board-Level Focus on Retention and Productivity Metrics

- 4.2.4 Frontline Workforce Digitization

- 4.2.5 CSRD and ESRS S1 Workforce Disclosure Readiness

- 4.2.6 Skills Graphs and Internal Talent Mobility Orchestration

- 4.3 Market Restraints

- 4.3.1 Data Privacy and Cross-System Integration Complexity

- 4.3.2 ROI Attribution and Change Fatigue

- 4.3.3 EU AI Act and Works Council Limits on Monitoring Features

- 4.3.4 Suite Bundling and Ecosystem Lock-In Pressure

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud-based

- 5.1.2 On-premises

- 5.1.3 Hybrid

- 5.2 By End User Enterprise Size

- 5.2.1 Small and Medium-sized Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Application

- 5.3.1 Employee Communication and Collaboration

- 5.3.2 Employee Engagement and Recognition

- 5.3.3 Employee Listening and Survey Analytics

- 5.3.4 Employee Wellbeing and Support

- 5.3.5 Other Applications

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 IT and Telecom

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial Manufacturing

- 5.4.6 Government and Public Sector

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Qualtrics, LLC

- 6.4.2 Culture Amp Pty Ltd

- 6.4.3 Perceptyx, Inc.

- 6.4.4 Medallia, Inc.

- 6.4.5 WorkTango Inc.

- 6.4.6 Achievers Solutions Inc.

- 6.4.7 Lattice, Inc.

- 6.4.8 15Five, Inc.

- 6.4.9 Quantum Workplace, Inc.

- 6.4.10 Motivosity, Inc.

- 6.4.11 Staffbase GmbH

- 6.4.12 Simpplr Inc.

- 6.4.13 LumApps SAS

- 6.4.14 Unily Group Ltd.

- 6.4.15 MangoApps Inc.

- 6.4.16 Haiilo GmbH

- 6.4.17 Firstup, Inc.

- 6.4.18 Appspace Inc.

- 6.4.19 Akumina, Inc.

- 6.4.20 Powell Software Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

神經多樣性員工體驗平台市場預測-全球分析(按組件、體驗階段、平台功能、組織規模、最終用戶和地區分類)——2034年

神經多樣性員工體驗平台市場預測-全球分析(按組件、體驗階段、平台功能、組織規模、最終用戶和地區分類)——2034年 2026年全球員工關係管理市場報告2026年全球員工體驗管理市場報告

2026年全球員工關係管理市場報告2026年全球員工體驗管理市場報告 員工體驗管理市場:按組件、工作方式、定價模式、應用、部署模式、組織規模和產業分類-2026年至2032年全球市場預測2026年全球員工監控軟體市場報告

員工體驗管理市場:按組件、工作方式、定價模式、應用、部署模式、組織規模和產業分類-2026年至2032年全球市場預測2026年全球員工監控軟體市場報告 2026-2030年全球人力分析在員工體驗領域的成長機會

2026-2030年全球人力分析在員工體驗領域的成長機會 員工監控解決方案市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、類型、應用、行業垂直領域、地區和競爭對手分類,2021-2031 年

員工監控解決方案市場 - 全球產業規模、佔有率、趨勢、機會、預測:按組件、類型、應用、行業垂直領域、地區和競爭對手分類,2021-2031 年 員工監控軟體市場規模、佔有率和成長分析(按組件、部署類型、監控類型、組織規模、最終用戶產業和地區分類)-2026-2033年產業預測

員工監控軟體市場規模、佔有率和成長分析(按組件、部署類型、監控類型、組織規模、最終用戶產業和地區分類)-2026-2033年產業預測 員工體驗管理市場機會、成長要素、產業趨勢分析及預測(2026-2035年)

員工體驗管理市場機會、成長要素、產業趨勢分析及預測(2026-2035年) 全球員工體驗管理市場

全球員工體驗管理市場