|

市場調查報告書

商品編碼

2064023

北美汽車LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)North America Automotive LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

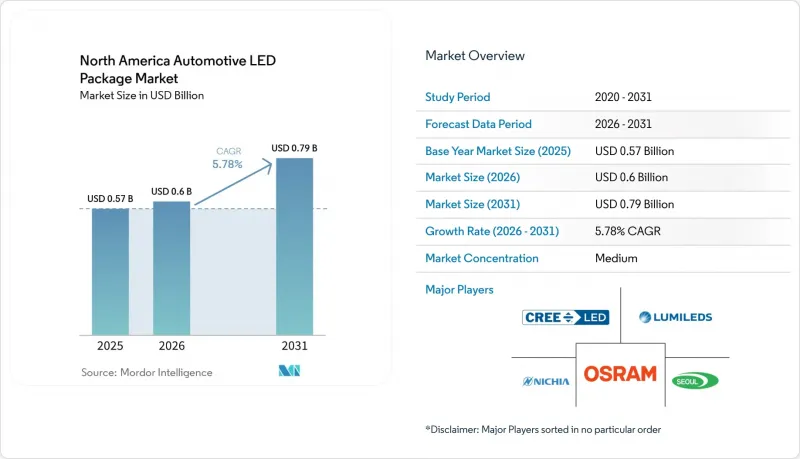

根據 Mordor Intelligence 預測,北美汽車LED構裝市場規模將從 2025 年的 5.7 億美元和 2026 年的 6 億美元成長到 2031 年的 7.9 億美元,2026 年至 2031 年的複合年成長率為 5.78%。

本報告按封裝架構(SMD、CSP、覆晶LED構裝、COB)、功率等級(低功率、中功率、高功率)、應用領域(外部照明、內部照明、感測/紅外線應用、其他)、車輛類型(乘用車、商用車)和國家進行細分。市場預測以美元(USD)為單位。

北美汽車LED構裝市場趨勢與洞察。

電動車自我調整遠光燈的採用率迅速提高。

隨著電動車平台向48V架構過渡,自我調整遠光燈正變得越來越普及,因為48V架構簡化了高電流LED驅動器的設計。隨著FMVSS 108標準的修訂消除了最後的監管障礙,特斯拉在2025年4月在其所有北美車型中啟用了防眩光遠光燈功能。歐司朗的「EVIYOS HD25」擁有25,600個可尋址像素,已在蔚來汽車的ET9工廠開始量產。這表示汽車製造商願意為以安全為中心的差異化產品支付30-40%的溢價。 Rivian已在R1T和R1S車型中實現了480像素陣列的量產,這表明商用級照明標準和乘用車照明期望正在趨於一致。由於像素密度的提高需要小於2毫米的封裝間距,許多一級供應商現在都採用覆晶CSP,這種封裝可以實現更薄的光學元件,同時顯著降低熱阻。因此,北美汽車LED構裝市場正從控制光束模式的硬體升級和軟體授權中獲得附加價值。

用於先進ADAS感測器的µLED陣列整合

微型LED陣列可為駕駛監視錄影機提供均勻的紅外線照明,並為道路場景投影提供高解析度可見光。日亞化學的µPLS平台採用256x64矩陣,包含16,384個微型LED,將於2025年開始量產用於乘員檢測模組。SONY的IMX775通過AEC-Q100認證,結合緊湊型940奈米LED陣列,將於2026年春季開始實現注重隱私的車載監控。 VueReal和Flex-N-Gate共同開發了一個煞車燈模組,該模組將車對車通訊訊息直接嵌入到動態LED像素中,模糊了照明和數據連接之間的界限。這些整合感測器的封裝正推動北美汽車LED構裝市場朝著在通用基板上共製造發射器-檢測器堆疊的方向發展,而這種架構正受到老牌企業和新興企業企業的競相申請專利。

高功率CSP封裝的溫度控管限制

高功率晶片級封裝會將高達 80% 的輸入能量以熱量的形式散失,長時間使用遠光燈會導致結溫超過 125 度C。達到此閾值會導致 5000 小時內光通量下降 15-20%,從而危及許多汽車製造商承諾的 10000 小時保固。 Lumileds 的 LUXEON Altilon SMD-A 透過採用銅導線架將熱阻降低至 2.5 度C/W,但通常仍需要主動散熱,從而增加了模組品質。覆晶結構改善了散熱路徑,但需要昂貴的晶圓級底部填充。早期生產批次的良率較低,導致單晶片成本增加。除非散熱器設計和磷光體穩定性有同步進步,否則這些限制將阻礙北美汽車LED構裝市場向超高密度頭燈陣列的快速轉型。

細分市場分析

晶片級封裝 (CSP) 在北美汽車LED構裝市場以 6.42% 的複合年成長率 (CAGR) 擴大了市場佔有率,但預計到 2025 年,表面黏著型元件(SMD) 仍將保持 43.78% 的市場佔有率。 CSP 無需焊線,並將封裝尺寸縮小至晶片尺寸的 20% 以內,從而形成直接的熱傳導路徑,並將結到基板的熱阻降低 30-40%。覆晶CSP 還支援小於 2 毫米的像素間距,這對於擁有 400 個或更多像素的頭燈模組至關重要。然而,智慧財產權糾紛——例如億光半導體 (Everlight) 於 2026 年 2 月就美國覆晶專利 7,554,126 對 Lumileds 和首爾半導體 (Seoul Semiconductor) 提起的訴訟——給 CSP 的普及帶來了風險。對於注重成本的商用車而言,SMD 架構仍是首選。特別是,ams OSRAM 的 Oslon Compact PL 在 1A 電流下實現了 395 流明的光通量,這表明效率的逐步提高可以延長傳統封裝的使用壽命。

Bridgelux 的 CSP 產品線目前在 350mA 電流下可實現 209 lm/W 的光效,使汽車製造商能夠在滿足亮度目標的同時,減少 20-30% 的 LED 數量,從而降低驅動電路和光學元件的成本。雖然板載晶片(COB) 解決方案可實現最高的流明密度,但其應用僅限於高階頭燈,因為在這些應用中,設計柔軟性比可維護性更為重要,單一晶片故障需要更換整個模組。預計在 2026 年至 2031 年間,CSP 的出貨量將與 SMD 的市佔率差距縮小一半,鞏固其作為北美汽車LED構裝市場成長最快類別的地位。

預計到2025年,功率超過1W的高功率LED將佔總銷售額的57.31%,並預計在2031年之前保持6.55%的複合年成長率,因為自我調整光束系統的目標是實現單封裝超過400流明的輸出。首爾半導體公司在2024年推出的Genesis GV80中採用的WICOP架構,與傳統封裝相比,亮度提高了一倍,散熱器體積減少了40%,並且由於取消了基板,散熱裕量也得到了提升。雖然中功率元件主要用於室內照明和輔助外部訊號,但低功率LED的應用仍限於開關背光和小型指示燈。

然而,微型LED陣列模糊了這些分類之間的界限,它將數萬個單顆功耗低於0.1瓦的像素整合到功耗超過5瓦的模組中。在未來十年,這種高密度佈局中的溫度控管將影響北美汽車LED構裝市場功率等級的定義。隨著亮度限制的提高,整合導熱通孔和基板散熱器的供應商有望擴大其市場佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車自我調整遠光燈的採用率迅速提高。

- 原始設備製造商 (OEM) 轉向動態外觀造型元素的轉變

- 實現具有按需照明功能的新型車載人機互動介面。

- 用於先進ADAS感測器的µLED陣列整合

- 美國日間行車燈標準化監管舉措

- 美墨加協定生效後,墨西哥近岸LED構裝將獲得優惠待遇

- 市場限制因素

- 高功率CSP封裝的溫度控管限制

- 藍寶石基板供不應求對供應鏈的影響

- 加拿大乘用車LED燈的普及率已趨於穩定。

- 覆晶晶圓級封裝中的智慧財產權訴訟風險

- 產業供應鏈分析

- 監理情勢

- 宏觀經濟因素對市場的影響

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依封裝架構

- SMD(表面黏著型元件)

- CSP(晶片級封裝)

- 覆晶LED構裝

- COB(板載晶片)

- 按輸出類別

- 低功耗(小於0.5瓦)

- 中功率(0.5–1 瓦)

- 高功率(超過 1 瓦)

- 透過使用

- 戶外照明

- 室內照明

- 感測/紅外線應用

- 其他用途

- 車輛類型

- 搭乘用車

- 商用車輛

- 國家

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- ams OSRAM AG

- Lumileds Holding BV

- Seoul Semiconductor Co., Ltd.

- CreeLED, Inc.

- Samsung Electronics Co., Ltd.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- LITE-ON Technology Corporation

- Toyoda Gosei Co., Ltd.

- Stanley Electric Co., Ltd.

- Rohm Co., Ltd.

- Vishay Intertechnology, Inc.

- Harvatek Corporation

- Nationstar Optoelectronics Co., Ltd.

- MLS Co., Ltd.(Forest Lighting)

- Brightek Optoelectronic Co., Ltd.

- Luminus Devices, Inc.

- Epistar Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america automotive LED package market size is projected to expand from USD 0.57 billion in 2025 and USD 0.60 billion in 2026 to USD 0.79 billion by 2031, registering a CAGR of 5.78% between 2026 to 2031.

This report is Segmented by Package Architecture (SMD, CSP, Flip-Chip LED Packages, and COB), Power Class (Low Power, Mid Power, and High Power), Application (Exterior Lighting, Interior Lighting, Sensing/IR Applications, and Other Applications), Vehicle Type (Passenger Vehicles and Commercial Vehicles), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America Automotive LED Package Market Trends and Insights

Surge in EV Headlamp Adoption for Adaptive Driving Beams

Adaptive driving-beam headlamps are proliferating as EV platforms migrate to 48-volt architectures that simplify high-current LED driver design. Tesla activated glare-free high beams across its North American fleet in April 2025, following amendments to FMVSS 108 that cleared the last regulatory hurdle. ams OSRAM's EVIYOS HD25 entered series production on NIO's ET9 with 25,600 addressable pixels, demonstrating that automakers are willing to pay a 30-40% price premium for safety-driven differentiation. Rivian brought 480-pixel arrays to volume production in the R1T and R1S, signaling the convergence of commercial-grade lighting standards with passenger-car expectations. Because pixel density demands sub-2 mm package pitch, many tier-ones are now specifying flip-chip CSPs that slash thermal resistance while enabling thinner optics. As a result, the North America automotive LED package market is capturing incremental value from both upgraded hardware and the software licenses that orchestrate beam patterns.

Integration of µLED Arrays for Advanced ADAS Sensors

Micro-LED arrays provide uniform infrared illumination for driver-monitoring cameras and high-resolution visible light for road-scene projection. Nichia's µPLS platform, with 16,384 micro-LEDs on a 256 X 64 matrix, entered mass production for occupant-detection modules in 2025. Sony's AEC-Q100-qualified IMX775 pairs with compact 940 nm LED arrays to deliver privacy-friendly cabin monitoring beginning in spring 2026. VueReal and Flex-N-Gate are co-developing brake-light modules that embed vehicle-to-vehicle messages directly in dynamic LED pixels, blurring lines between lighting and data connectivity. These sensor-integrated packages push the North America automotive LED package market toward co-fabricated emitter-detector stacks on common substrates, an architecture that incumbents and start-ups alike are racing to patent.

Thermal Management Limits for High-Power CSP Packages

High-power chip-scale packages dissipate up to 80% of input energy as heat, and junction temperatures can climb beyond 125 °C during prolonged high-beam use. At that threshold, luminous flux can drop by 15-20% within 5,000 hours, jeopardizing the 10,000-hour warranty many automakers promise. Lumileds' LUXEON Altilon SMD-A reduces thermal resistance to 2.5 °C/W with a copper lead frame, but often still requires active cooling, which adds module mass. Flip-chip configurations improve heat paths yet require costly wafer-level underfill; early production runs have reported yield losses that raise per-die costs. These constraints limit how aggressively the North America automotive LED package market can pivot to ultra-dense headlamp arrays without parallel advances in heat-sink design or phosphor stability.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift Toward Dynamic Exterior Styling Elements

- Light-on-Demand Features Enabling New In-Cabin HMI

- Supply-Chain Exposure to Sapphire Substrate Shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chip-scale packages increased their slice of the North America automotive LED package market to 6.42% CAGR, while surface-mount devices retained a 43.78% lead in 2025. CSPs eliminate wire bonds and shrink the footprint to within 20% of the die size, carving direct thermal paths that cut junction-to-board resistance by 30-40%. Flip-chip CSPs also support pixel pitches below 2 mm, critical for ≥400-pixel headlamp modules. However, intellectual-property disputes-Everlight sued Lumileds and Seoul Semiconductor in February 2026 over flip-chip patent US 7,554,126-inject adoption risk. SMD architectures remain preferred for cost-sensitive commercial vehicles, especially after ams OSRAM's Oslon Compact PL reached 395 lumens at 1 A, showing that incremental efficiency gains can extend the life of conventional packages.

Bridgelux's CSP line now delivers 209 lm/W at 350 mA, allowing automakers to meet brightness targets with 20-30% fewer LEDs, which trims driver-circuit and optics costs. Chip-on-board solutions achieve peak lumen density but require replacing the entire module if one die fails, limiting uptake to premium headlamps where design flexibility outweighs serviceability. Across 2026-2031, CSP shipments are forecast to close half the unit-share gap with SMDs, reinforcing their status as the fastest-advancing category in the North America automotive LED package market.

High-power LEDs above 1 W delivered 57.31% revenue in 2025 and will post a 6.55% CAGR to 2031 as adaptive-beam systems target per-package outputs beyond 400 lumens. Seoul Semiconductor's WICOP architecture in the 2024 Genesis GV80 doubled luminance compared with legacy packages and reduced heat-sink bulk by 40%, demonstrating the thermal headroom created by removing substrates. Mid-power devices occupy ambient lighting and secondary exterior signals, while low-power LEDs remain relegated to switch backlights and small indicators.

Yet micro-LED arrays blur these classes by aggregating tens of thousands of sub-0.1 W pixels into modules that draw more than 5 W. Managing heat across such dense layouts will shape power-class definitions in the North America automotive LED package market over the decade. Suppliers that integrate thermal vias and on-substrate heat spreaders are poised to capture incremental share as luminance ceilings rise.

List of Companies Covered in this Report:

- Nichia Corporation

- ams OSRAM AG

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- CreeLED, Inc.

- Samsung Electronics Co., Ltd.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- LITE-ON Technology Corporation

- Toyoda Gosei Co., Ltd.

- Stanley Electric Co., Ltd.

- Rohm Co., Ltd.

- Vishay Intertechnology, Inc.

- Harvatek Corporation

- Nationstar Optoelectronics Co., Ltd.

- MLS Co., Ltd. (Forest Lighting)

- Brightek Optoelectronic Co., Ltd.

- Luminus Devices, Inc.

- Epistar Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV Headlamp Adoption for Adaptive Driving Beams

- 4.2.2 OEM Shift Toward Dynamic Exterior Styling Elements

- 4.2.3 Light-on-Demand Features Enabling New In-Cabin HMI

- 4.2.4 Integration of µLED Arrays for Advanced ADAS Sensors

- 4.2.5 U.S. Regulatory Push for Daytime Running Lights Standardization

- 4.2.6 Mexico's Near-Shore LED Packaging Incentives Post-USMCA

- 4.3 Market Restraints

- 4.3.1 Thermal Management Limits for High-Power CSP Packages

- 4.3.2 Supply Chain Exposure to Sapphire Substrate Shortages

- 4.3.3 Passenger Vehicle LED Penetration Plateau in Canada

- 4.3.4 IP Litigation Risk in Flip-Chip Wafer-Level Packaging

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Architecture

- 5.1.1 SMD (Surface Mount Device)

- 5.1.2 CSP (Chip Scale Package)

- 5.1.3 Flip-Chip LED Packages

- 5.1.4 COB (Chip-on-Board)

- 5.2 By Power Class

- 5.2.1 Low Power (Less than 0.5 W)

- 5.2.2 Mid Power (0.5-1 W)

- 5.2.3 High Power (More than 1 W)

- 5.3 By Application

- 5.3.1 Exterior Lighting

- 5.3.2 Interior Lighting

- 5.3.3 Sensing / IR Applications

- 5.3.4 Other Applications

- 5.4 By Vehicle Type

- 5.4.1 Passenger Vehicles

- 5.4.2 Commercial Vehicles

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 ams OSRAM AG

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Seoul Semiconductor Co., Ltd.

- 6.4.5 CreeLED, Inc.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Everlight Electronics Co., Ltd.

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 Dominant Opto Technologies Sdn. Bhd.

- 6.4.10 LITE-ON Technology Corporation

- 6.4.11 Toyoda Gosei Co., Ltd.

- 6.4.12 Stanley Electric Co., Ltd.

- 6.4.13 Rohm Co., Ltd.

- 6.4.14 Vishay Intertechnology, Inc.

- 6.4.15 Harvatek Corporation

- 6.4.16 Nationstar Optoelectronics Co., Ltd.

- 6.4.17 MLS Co., Ltd. (Forest Lighting)

- 6.4.18 Brightek Optoelectronic Co., Ltd.

- 6.4.19 Luminus Devices, Inc.

- 6.4.20 Epistar Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment