|

市場調查報告書

商品編碼

2064018

亞太地區汽車LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Asia-Pacific Automotive LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

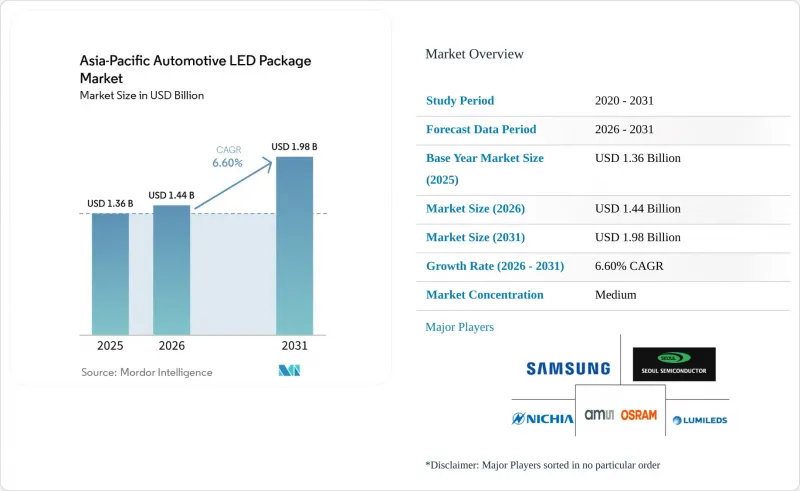

根據 Mordor Intelligence 預測,亞太地區汽車LED構裝市場規模將從 2025 年的 13.6 億美元成長到 2026 年的 14.4 億美元,然後在 2031 年達到 19.8 億美元,2026 年至 2031 年的複合年成長率為 6.60%。

本報告按封裝結構(SMD、CSP、覆晶LED構裝、COB)、功率等級(低功率、中功率、高功率)、應用(外部照明、內部照明、感測/紅外線應用等)、車輛類型(乘用車、商用車)和國家(中國、日本、印度等)進行細分。市場預測以美元(USD)計價。

亞太地區汽車LED構裝市場趨勢及洞察。

對節能型汽車照明的需求日益成長

由於亞太地區的電動車 (EV) 專案主要專注於最大限度地提高續航里程,因此即使照明子系統功耗降低 1 瓦,也能直接轉換為續航里程的增加。 2024 年中國新能源車 (NEV) 的產量預計將達到 1,286 萬輛,這將形成大規模的應用基礎,尤其有利於LED構裝的推廣。 LED 照明組件的耗電量比鹵素燈低 30% 至 50%。這將使緊湊型電池式電動車的續航里程增加 5 至 10 公里。混合動力汽車平台也將受益於發電機負載的降低,進而提高燃油效率,而燃油效率則是印度和泰國獲得補貼的依據。美國能源局預測,到 2035 年,發光效率將達到每瓦 249 流明,將成為未來 LED 照明組件開發藍圖的基礎。鹵素燈的壽命為 1,000 至 2,000 小時,而 LED 燈的壽命長達 25,000 至 50,000 小時,這為東南亞地區的車隊運營商提供了可靠性優勢,降低了保固風險,因為該地區的服務網路通常比較稀少。

乘用車廣泛採用LED頭燈

到2025年,封裝式LED的成本將降至每千流明0.5美元以下,這將使汽車製造商能夠在中檔轎車和SUV上標配LED頭燈。首爾半導體的WICOP晶片級LED元件已被100多款乘用車採用,證明了大規模生產的成本目標的可行性。印度的Bharat NCAP碰撞測試協議對配備日間行車燈(DRL)的車輛給予更高的安全評分,促使汽車製造商採用全LED頭燈和日間行車燈組件。到2024年,中國乘用車產量將超過2,000萬輛,LED頭燈的普及率將超過60%。這是因為國內供應商在亮度和散熱性能方面已達到與日本同業相當的水平,同時價格比現有製造商低20-30%。

與鹵素溶液相比,初始成本較高。

在印度和注重成本的東協市場,入門車型仍使用單價5-8美元的滷素頭燈組件,而基本型LED大燈的組件成本則在15-25美元之間。對於零售價約10,000-12,000美元的緊湊型轎車而言,每盞燈增加10美元的成本會顯著影響汽車製造商的利潤率。雖然目前中功率的表面黏著技術貼裝LED燈的價格低於每千流明0.50美元,但包括驅動器、散熱器和光學元件在內的整個系統的成本卻是鹵素燈的三到四倍。儘管能源效率有所提高,但兩輪電動車仍繼續使用單晶片LED燈或鹵素燈,因為成本效益是購買決策中的首要考慮因素。

細分市場分析

到2025年,表面黏著型元件將佔據亞太地區汽車LED構裝市場43.39%的佔有率,繼續在尾燈、牌照燈和車頂燈等領域保持主導地位,這些領域對可靠性和成熟的供應鏈要求極高。然而,晶片級封裝正以7.06%的複合年成長率快速成長,透過將整體光學高度降低至10毫米,徹底革新了頭燈設計。首爾半導體的WICOP結構將裸晶直接鍵結到電路基板,無需基板或陶瓷框架。隨著中國和日本的汽車製造商追求能夠降低空氣阻力並實現卓越日間可見度的超薄燈具設計,預計亞太地區晶片級裝置相關的汽車LED構裝市場規模將加速成長。

覆晶技術也遵循類似的趨勢,它利用金焊盤鍵合來提高導熱性和電流分散性,從而實現自適應驅動光束陣列。專利之爭愈演愈烈,億光半導體於2026年2月在美國對首爾半導體提起專利侵權訴訟,指控其侵犯了覆晶的電極形狀,這表明隨著對CSP(晶片級封裝)的需求不斷成長,法律摩擦也在加劇。板載晶片(COB)技術目前仍主要應用於商用車輔助射燈,其將多個晶片整合到單一鋁基基板以實現高流明密度。綜上所述,這些趨勢表明,隨著中國本土供應商擴大晶圓層次電子構裝生產線,晶片級封裝和覆晶技術將繼續進一步蠶食傳統SMD(表面貼裝元件)的市場佔有率。

2025年,功率超過1瓦的高功率封裝產品佔總銷售量的57.89%。這反映了自我調整遠光燈系統的快速普及,該系統需要200 cd/mm²或更高的亮度才能實現無眩光遠光燈。亞太地區汽車LED構裝市場規模(主要歸因於此類產品)預計到2028年將隨著中型轎車引入像素化頭燈而擴大。中功率元件則應用於日間行車燈和車內RGB照明等對散熱需求相對寬鬆的應用領域。低功率指示燈逐漸商品化,中國供應商的售價低於每顆0.10美元,這擠壓了利潤空間,並推動了產業整合。

日亞化學株式會社的µPLS微型LED光源引擎正是此趨勢的典型代表。它透過整合16,384顆功率在50至100毫瓦之間的高功率微型LED,實現了超過1000流明的光輸出,能夠將光線投射到路面上。 GB 4599-2021和UNECE R112中關於眩光控制的監管要求,正迫使汽車製造商採用此類陣列。中功率RGB LED在電動車車廂內迅速普及,50至100顆可尋址LED即可實現氣氛照明、導航及充電狀態提示等功能。隨著智慧頭燈每個單元增加100至300個像素,高功率LED仍將佔據市場的大部分佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對節能型汽車照明的需求日益成長

- 乘用車廣泛採用LED頭燈

- 關於汽車照明的嚴格安全法規

- 亞太地區電動車產量快速成長

- 東協地區的在地化供應鏈降低了LED構裝的成本。

- 將智慧像素LED陣列整合到進階駕駛輔助系統(ADAS)中

- 市場限制因素

- 與鹵素溶液相比,初始成本較高。

- 高功率LED構裝的溫度控管挑戰

- 宏觀經濟不確定性導致汽車銷售波動

- 專利訴訟可能會限制新參與企業的創新能力。

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 所以

- SMD(表面黏著型元件)

- CSP(晶片級封裝)

- 覆晶LED構裝

- COB(板載晶片)

- 按輸出類別

- 低功率(小於0.5瓦)

- 中功率(0.5–1 瓦)

- 高功率(超過 1 瓦)

- 透過使用

- 戶外照明

- 室內照明

- 感測/紅外線應用

- 其他用途

- 按車輛類型

- 搭乘用車

- 商用車輛

- 國家

- 中國

- 日本

- 印度

- 東南亞

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- OSRAM GmbH(Ams-OSRAM AG)

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding BV

- Samsung Electronics Co., Ltd.

- Cree LED(SGH Group)

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Lite-On Technology Corporation

- Dominant Opto Technologies Sdn. Bhd.

- Stanley Electric Co., Ltd.

- Rohinni LLC

- Lextar Electronics Corporation

- Toyoda Gosei Co., Ltd.

- EPISTAR Corporation

- TOSPO Lighting Co., Ltd.

- Refond Optoelectronics Co., Ltd.

- ProLight Opto Technology Corporation

- MLS Co., Ltd.(Forest Lighting)

- Lumens Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific automotive LED package market size is expected to grow from USD 1.36 billion in 2025 to USD 1.44 billion in 2026 and is forecast to reach USD 1.98 billion by 2031 at a 6.60% CAGR over 2026-2031.

This report is Segmented by Package Architecture (SMD, CSP, Flip-Chip LED Packages, COB), Power Class (Low Power, Mid Power, and High Power ), Application (Exterior Lighting, Interior Lighting, Sensing/IR Applications, and More), Vehicle Type (Passenger Vehicles, and Commercial Vehicles), and Country (China, Japan, India, and More). Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Automotive LED Package Market Trends and Insights

Increasing Demand for Energy-Efficient Automotive Lighting

Electric vehicle programs across Asia-Pacific center on maximizing range, so every watt shaved from lighting subsystems translates directly into extra driving kilometers. China's 12.86 million new-energy vehicles built in 2024 created a large installed base that values LED packages delivering 30-50% lower power draw than halogens, translating to 5-10 kilometer range gains in compact battery-electric cars. Hybrid platforms also benefit when alternator load falls, improving fuel-economy scores used for subsidy qualification in India and Thailand. Efficacy gains projected by the U.S. Department of Energy, reaching 249 lumens per watt by 2035, underpin future package roadmaps. Reliability advantages, with lifetimes of 25,000-50,000 hours compared with 1,000-2,000 hours for halogens, cut warranty risk for fleet operators in Southeast Asia where service networks are sparse.

Growing Penetration of LED Headlamps in Passenger Vehicles

Packaged LED cost fell below USD 0.50 per kilolumen in 2025, allowing automakers to list LED headlamps as standard equipment on mid-tier sedans and sport-utility vehicles. Seoul Semiconductor's WICOP chip-scale devices underpin more than 100 passenger models, validating cost targets for mass production. India's Bharat NCAP protocol attaches higher safety scores to daytime-running-lamp equipped cars, nudging OEMs toward full LED headlamp-DRL bundles. China's passenger car production exceeded 20 million units in 2024, with LED headlamp penetration crossing 60% as domestic suppliers matched Japanese peers on luminance and thermal performance while pricing 20-30% below incumbent quotes.

High Initial Cost Compared to Halogen Solutions

Entry-level cars in India and cost-sensitive ASEAN markets still rely on halogen assemblies costing USD 5-8 each, whereas a basic LED headlamp bill of materials sits in the USD 15-25 range. For compact sedans retailing at roughly USD 10,000-12,000, the extra USD 10 per lamp materially erodes automaker margin. Although mid-power surface-mount LED prices are now under USD 0.50 per kilolumen, drivers, heat sinks, and optics push full-system cost three-to-four times higher than halogen. Two-wheel EVs, despite energy-efficiency gains, continue opting for single-chip LEDs or halogens because unit economics dominate purchase decisions.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Automotive Lighting Safety Regulations

- Rapid Expansion of Electric Vehicle Production in Asia-Pacific

- Thermal Management Challenges in High-Power LED Packages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface-mount devices captured 43.39% of the Asia-Pacific automotive LED package market share in 2025, maintaining leadership in rear lamps, license-plate illumination, and dome lights where proven reliability and entrenched supply chains matter most. Yet chip-scale packages, expanding at a 7.06% CAGR, are redefining headlamp styling by trimming total optical height to as low as 10 millimeters. Seoul Semiconductor's WICOP structure bonds the bare die directly to the circuit board, eliminating substrates and ceramic frames. The Asia-Pacific automotive LED package market size attached to chip-scale devices is set to accelerate as OEMs in China and Japan seek razor-thin lamp designs that lower drag and enable distinct daytime signatures.

Flip-chip formats ride the same trend, leveraging gold-pad bonding to improve thermal conductivity and current spreading for adaptive driving beam arrays. Patent crossfire is intensifying; Everlight's February 2026 U.S. filing against Seoul Semiconductor alleges infringement on flip-chip electrode geometry, signaling legal friction as CSP demand grows. Chip-on-board remains a niche for auxiliary spot lamps in commercial vehicles where clustering multiple dies on a single aluminum substrate gives high lumen density. Combined, these dynamics indicate that chip-scale and flip-chip will keep eroding legacy SMD share as local Chinese suppliers scale wafer-level packaging lines.

High-power packages above 1 watt delivered 57.89% of 2025 revenue, mirroring rapid uptake of adaptive driving beam systems that require 200-plus cd mm-2 luminance for glare-free high beam. The Asia-Pacific automotive LED package market size attributable to this class will expand alongside pixelated headlights entering mid-tier sedans by 2028. Mid-power devices fill daytime running lamp and interior RGB roles where thermal constraints are modest. Low-power indicators are commoditizing as Chinese vendors quote sub-USD 0.10 per part, squeezing margins and prompting consolidation.

Nichia's µPLS micro-LED light engine shows the trajectory: 16,384 high-power micro-LEDs, each at 50-100 mW, combine for over 1,000 lumens while enabling road-surface projections. Regulatory glare-control requirements in GB 4599-2021 and UNECE R112 push OEMs toward such arrays. Mid-power RGB usage is surging in electric-vehicle cabins where 50-100 addressable LEDs handle mood, navigation, and state-of-charge alerts. The high-power segment will continue to dominate value as each vehicle adds 100-300 pixels for smart headlights.

List of Companies Covered in this Report:

- Nichia Corporation

- OSRAM GmbH (Ams-OSRAM AG)

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- Samsung Electronics Co., Ltd.

- Cree LED (SGH Group)

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Lite-On Technology Corporation

- Dominant Opto Technologies Sdn. Bhd.

- Stanley Electric Co., Ltd.

- Rohinni LLC

- Lextar Electronics Corporation

- Toyoda Gosei Co., Ltd.

- EPISTAR Corporation

- TOSPO Lighting Co., Ltd.

- Refond Optoelectronics Co., Ltd.

- ProLight Opto Technology Corporation

- MLS Co., Ltd. (Forest Lighting)

- Lumens Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions And Market Definition

- 1.2 Scope Of The Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand For Energy-Efficient Automotive Lighting

- 4.2.2 Growing Penetration Of LED Headlamps In Passenger Vehicles

- 4.2.3 Stringent Automotive Lighting Safety Regulations

- 4.2.4 Rapid Expansion Of Electric Vehicle Production In Asia-Pacific

- 4.2.5 Localized Supply Chains Reducing LED Package Costs In ASEAN

- 4.2.6 Integration Of Smart Pixel LED Arrays For Advanced Driver Assistance Systems (ADAS)

- 4.3 Market Restraints

- 4.3.1 High Initial Cost Compared To Halogen Solutions

- 4.3.2 Thermal Management Challenges In High-Power LED Packages

- 4.3.3 Volatility In Automotive Sales Due To Macroeconomic Uncertainties

- 4.3.4 Patent Litigation Risks Limiting New Entrant Innovation

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact Of Macroeconomic Factors On The Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power Of Suppliers

- 4.8.2 Bargaining Power Of Buyers

- 4.8.3 Threat Of New Entrants

- 4.8.4 Threat Of Substitutes

- 4.8.5 Intensity Of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Package Architecture

- 5.1.1 SMD (Surface Mount Device)

- 5.1.2 CSP (Chip Scale Package)

- 5.1.3 Flip-Chip LED Packages

- 5.1.4 COB (Chip-On-Board)

- 5.2 By Power Class

- 5.2.1 Low Power ( Less Than 0.5 W)

- 5.2.2 Mid Power (0.5 to 1 W)

- 5.2.3 High Power (More Than 1 W)

- 5.3 By Application

- 5.3.1 Exterior Lighting

- 5.3.2 Interior Lighting

- 5.3.3 Sensing / IR Applications

- 5.3.4 Others - Applications

- 5.4 By Vehicle Type

- 5.4.1 Passenger Vehicles

- 5.4.2 Commercial Vehicles

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 Southeast Asia

- 5.5.5 Rest Of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share, Products And Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 OSRAM GmbH (Ams-OSRAM AG)

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 Lumileds Holding B.V.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Cree LED (SGH Group)

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Lite-On Technology Corporation

- 6.4.10 Dominant Opto Technologies Sdn. Bhd.

- 6.4.11 Stanley Electric Co., Ltd.

- 6.4.12 Rohinni LLC

- 6.4.13 Lextar Electronics Corporation

- 6.4.14 Toyoda Gosei Co., Ltd.

- 6.4.15 EPISTAR Corporation

- 6.4.16 TOSPO Lighting Co., Ltd.

- 6.4.17 Refond Optoelectronics Co., Ltd.

- 6.4.18 ProLight Opto Technology Corporation

- 6.4.19 MLS Co., Ltd. (Forest Lighting)

- 6.4.20 Lumens Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space And Unmet-Need Assessment