|

市場調查報告書

商品編碼

2063960

北美GPU浸沒式散熱:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)North America GPU Immersion Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

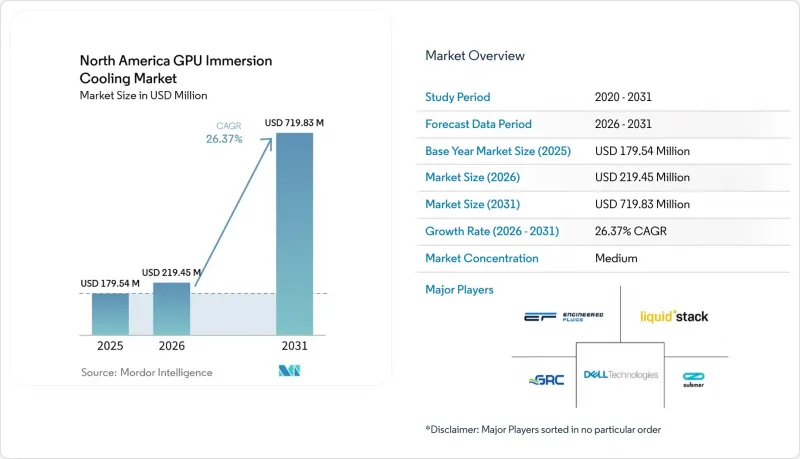

根據 Mordor Intelligence 預測,GPU 液冷市場規模將從 2025 年的 1.7954 億美元和 2026 年的 2.1945 億美元成長到 2031 年的 7.1983 億美元,2026 年至 2031 年的複合成長率為 26.37%。

本報告依浸沒式冷卻方式(單相浸沒式冷卻和兩相浸沒式冷卻)、解決方案類型(浸沒式冷卻槽/系統、浸沒式冷卻最佳化型GPU伺服器系統等)、部署類型(超大規模/雲端、企業級、其他)、GPU功率密度(小於300W、300W-700W、大於700W)以及大於700W)以及大於地區進行細分。市場預測以美元(USD)計價。

北美GPU浸沒式散熱市場趨勢及洞察

生成式人工智慧工作負載對高密度GPU運算的需求日益成長

訓練和推理叢集目前已採用額定功率為 700 瓦的 NVIDIA H100 GPU,而升級到 1000 瓦的 Blackwell B200 晶片後,每個機架的功耗接近 120 千瓦。液冷技術使營運商無需升級冷卻器即可突破這些密度限制,並將 PUE 值保持在 1.1 左右。 xAI 的 Memphis超級電腦配備了 10 萬個液冷 H100S GPU,PUE 值僅為 1.09,這已成為其他超大規模資料中心業者競相追求的效能基準。隨著兆參數語言模型逐漸成為標準配置,即使是企業實驗室也開始意識到風冷散熱的利用率正在下降,而液冷正成為實現 GPU(圖形處理器)滿載運行的成熟方案。

美國雲端服務供應商正在擴大液冷超大規模資料中心的部署。

亞馬遜、微軟、谷歌和甲骨文已宣布浸沒式冷卻技術藍圖,計劃將2025年後新建的所有可用區全部升級為晶片級直接冷卻或浸沒式冷卻設施。 CoreWeave位於魁北克的300兆瓦園區透過將浸沒式冷卻槽與區域供熱迴路結合,展示了利用市政能源銷售抵消冷卻成本的經濟效益。這些備受矚目的措施正使財務長們相信,浸沒式冷卻技術並非實驗性質,而是業界標準,並推動財富500強企業IT部門內部關於技術升級的討論。

UL和EPA認證的合成介電液體供不應求

2025年,3M宣布退出Novec產品線。這使得市場上可用的已通過核准化學品數量從七種大幅減少至四種。選擇範圍的縮小導致二手市場價格上漲40%,進一步加劇了營運商的成本壓力。因此,營運商現在必須使用索爾維、科慕或殼牌提供的替代流體進行重新認證。這個過程通常需要6到9個月,不僅給營運帶來挑戰,而且除非供應商明確提供浸沒條款以解決相容性問題,否則還可能導致GPU保固失效。此外,美國環保署(EPA)收緊揮發性有機化合物(VOC)基準值,進一步限制了可用候選流體的範圍,使情況更加複雜。這些監管變化與需求激增同時發生,加劇了供應限制,並為市場參與企業創造了充滿挑戰的環境。

細分市場分析

單相設計憑藉其管道結構更簡單、可用流體範圍更廣的優勢,預計到2025年將佔據北美GPU液冷市場79.87%的佔有率。雖然企業更傾向於常壓運行,但超大規模資料中心業者正在嘗試使用雙相儲液罐,以實現低於1.05的PUE值,並將矽晶圓溫度降低到環境溫度以下。由於更長的保固期和冷凝器自動化帶來的更低維護成本,預計北美雙相GPU液冷市場規模將穩定成長。然而,單相供應商在易用性方面仍具有優勢,例如GRC的即插即用型ICEraQ Series 3,該產品標配循環和監控功能。

超大規模企業的負責人希望降低延遲以減少每次推理的成本,同時也渴望培訓工程師掌握沸騰流體的動態。 Submer 的 SmartPodX Gen 2 已經整合了蒸氣回收功能和封閉回路型冷凝器,使其能夠滿足人工智慧推理集群的需求,因為即使是冷卻能力的微小提升也至關重要。同時,英特爾對油基系統的保固認可表明,原始設備製造商 (OEM) 已準備好將單相部署標準化,但 GPU 製造商尚未將類似的質保擴展到兩相化學系統,這迫使一些運營商在更廣泛的質保框架建立之前,只能繼續進行試點規模的部署。

2025年,北美GPU浸沒式冷卻市場中,水箱及相關基礎設施的收入佔比高達55.23%,但預計到2031年,針對浸沒式冷卻最佳化的伺服器市場將以26.56%的複合年成長率快速成長。目前,原始設計製造商(ODM)已開始預先整合導熱墊、流體歧管和帶外感測器,從而避免了成本高昂的現場維修。例如,Supermicro的DLC-3平台支援150千瓦機架,並可直接用於H200、MI325X和Gaudi 3加速器。因此,到2020年代末,整合式伺服器平台相關的GPU浸沒式冷卻市場規模將與水箱相關銷售額之間的差距逐漸縮小。

隨著託管業者逐步採用模組化50千瓦冷卻模組,儲罐持續受益,但隨著業者採用可將使用壽命延長兩年的現場回收撬裝設備,冷卻液的銷售量趨於平穩。因此,介電材料供應商正將業務重心轉向包含線上光譜分析功能的捆綁式分析服務,旨在提升銷售預測性維護訂閱服務的銷售。此舉使他們能夠在冷卻液供應趨於平穩的情況下,並繼續與GPU浸沒式冷卻市場保持聯繫。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 生成式人工智慧工作負載對高密度GPU運算的需求日益成長

- 美國雲端服務供應商正在擴大液冷超大規模資料中心的應用。

- 美國能源局為降低 PUE(電源使用效率)而製定的能源效率法規。

- 廠商主導的開放硬體標準(例如 OCP 高級冷卻解決方案)正在加速其普及。

- 維吉尼亞北部和矽谷的電費上漲

- 熱能再利用獎勵,以支持資料中心廢熱回收。

- 市場限制因素

- 難以取得UL和EPA認證的合成絕緣材料。

- 傳統企業資料中心需要大量資金維修

- 關於雙相浸沒式冷卻液的長期GPU保固政策尚不明確

- 東亞地區浸沒式水箱製造供應鏈集中度較高

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 浸沒法

- 單相浸沒式冷卻

- 兩相浸沒式冷卻

- 按解決方案類型

- 浸入式冷卻罐/系統

- 介電液

- 針對液冷散熱最佳化的GPU伺服器系統

- 不同的發展

- 超大規模/雲

- 公司

- 政府和研究機構(高效能運算)

- 按GPU功率密度

- 小於300瓦

- 300W~700W

- 超過700瓦

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- GRC(Green Revolution Cooling)

- Submer Technologies SL

- LiquidStack Holding Pte. Ltd.

- Engineered Fluids Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Super Micro Computer Inc.

- Nvidia Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- 3M Company

- Shell plc

- Fluoramics Inc.

- Asperitas BV

- Wiwynn Corporation

- Midas Immersion Cooling

- CoolIT Systems Inc.

- Asetek A/S

- Schneider Electric SE

- Vertiv Holdings Co.

第7章 市場機會與未來展望

According to Mordor Intelligence, the gPU immersion cooling market size is expected to increase from USD 179.54 million in 2025 and USD 219.45 million in 2026 to USD 719.83 million by 2031, growing at a CAGR of 26.37% over 2026-2031.

This report is Segmented by Immersion Type (Single-Phase Immersion Cooling, and Two-Phase Immersion Cooling), Solution Type (Immersion Cooling Tank/Systems, Immersion-Optimized GPU Server Systems, and More), Deployment (Hyperscale/Cloud, Enterprise, and More), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

North America GPU Immersion Cooling Market Trends and Insights

Growing Demand for High-Density GPU Compute for Generative AI Workloads

Training and inference clusters are already fielding NVIDIA H100 GPUs rated at 700 watts, and the leap to 1,000-watt Blackwell B200 silicon pushes rack power toward 120 kilowatts. Immersion cooling allows operators to crest these density thresholds without chiller upgrades, keeping PUE near 1.1. xAI's Memphis supercomputer reached 100,000 liquid-cooled H100S and logged a PUE of 1.09, setting a performance baseline other hyperscalers now chase. With trillion-parameter language models standardizing, even enterprise labs accept that air cooling throttles utilization, cementing immersion as the pragmatic path to GPU (Graphics Processing Unit) saturation.

Expanding Deployment of Liquid-Cooled Hyperscale Data Centers by U.S. Cloud Providers

Amazon, Microsoft, Google, and Oracle have each publicized liquid-cooling roadmaps that convert every new availability zone after 2025 into either direct-to-chip or immersion builds. CoreWeave's 300-megawatt Quebec campus illustrates the economic upside of combining immersion tanks with district heating loops, offsetting cooling costs through municipal energy sales. These high-profile commitments reassure CFOs that immersion is not an experiment but an industry baseline, strengthening the upgrade narrative inside Fortune 500 IT departments.

Limited Availability of Synthetic Dielectric Fluids with UL and EPA Approvals

In 2025, 3M announced its decision to exit the Novec product line, a move that significantly reduced the number of approved chemistries available in the market from seven to four. This reduction in options triggered a 40% increase in secondary-market pricing, creating additional cost pressures for operators. As a result, operators are now required to undergo a re-qualification process with alternative fluids supplied by Solvay, Chemours, or Shell. This process, which typically spans six to nine months, presents operational challenges and carries the potential risk of voiding GPU warranties unless vendors explicitly provide immersion riders to address compatibility concerns. Adding to these complexities, the Environmental Protection Agency (EPA) has implemented stricter thresholds for volatile organic compounds (VOCs), further limiting the range of candidate fluids available. These regulatory changes coincide with a surge in demand, intensifying supply constraints and creating a challenging environment for market participants.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Regulations by U.S. Department of Energy Targeting PUE Reductions

- Vendor-Led Open Hardware Standards Accelerating Adoption

- Capital-Intensive Retrofit Requirements for Legacy Enterprise Data Halls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase designs captured 79.87% of 2025 North America GPU immersion cooling market revenue by leveraging simpler plumbing and broader fluid options. Enterprises favor atmospheric-pressure operation, while hyperscalers pilot two-phase tanks to chase sub-1.05 PUE targets and sub-ambient silicon temperatures. The NA Graphics Processing Unit immersion cooling market size for two-phase architectures is projected to climb steadily as warranty coverage matures and condenser automation trims maintenance overhead. Yet single-phase vendors retain an edge on ease of use, exemplified by GRC's plug-and-play ICEraQ Series 3, which ships with recirculation and monitoring baked in.

Hyperscale buyers are willing to train technicians on boiling-fluid dynamics, expecting latency cuts that shave cost-per-inference. Submer's SmartPodX Gen 2 already bundles vapor recovery and closed-loop condensers, positioning it for AI inference farms that prize every extra degree of cooling headroom. Meanwhile, Intel's oil-based warranty rider signals OEM readiness to normalize single-phase deployments, but GPU manufacturers have yet to extend similar guarantees for two-phase chemistries, limiting some operators to pilot-scale deployments until broader warranty frameworks emerge.

In 2025, tanks and ancillary infrastructure commanded 55.23% of revenue of the North America GPU immersion cooling market, but immersion-optimized servers are outrunning at a 26.56% CAGR through 2031. ODMs now pre-install thermal interface pads, fluid manifolds, and out-of-band sensors, avoiding costly field retrofits. For example, Supermicro's DLC-3 platform supports 150-kilowatt racks and ships immersion-ready for H200, MI325X, and Gaudi 3 accelerators. As a result, the GPU immersion cooling market size tied to integrated server platforms will narrow the gap with tank revenue by the decade's close.

Tanks continue to benefit from modular 50-kilowatt blocks that colocation landlords deploy incrementally, but fluid revenue is flattening as operators install on-site reclamation skid packages that extend service life by two years. Dielectric suppliers thus pivot to bundled analytics, embedding inline spectroscopy to upsell predictive-maintenance subscriptions, a move that keeps them tethered to the GPU immersion cooling market even as raw-fluid volumes plateau.

List of Companies Covered in this Report:

- GRC (Green Revolution Cooling)

- Submer Technologies SL

- LiquidStack Holding Pte. Ltd.

- Engineered Fluids Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Super Micro Computer Inc.

- Nvidia Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- 3M Company

- Shell plc

- Fluoramics Inc.

- Asperitas BV

- Wiwynn Corporation

- Midas Immersion Cooling

- CoolIT Systems Inc.

- Asetek A/S

- Schneider Electric SE

- Vertiv Holdings Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for High-Density GPU Compute for Generative AI Workloads

- 4.2.2 Expanding Deployment of Liquid-Cooled Hyperscale Data Centers by U.S. Cloud Providers

- 4.2.3 Energy-Efficiency Regulations by the U.S. Department of Energy Targeting PUE Reductions

- 4.2.4 Vendor-Led Open Hardware Standards (e.g., OCP Advanced Cooling Solutions) Accelerating Adoption

- 4.2.5 Rising Electricity Tariffs in Northern Virginia and Silicon Valley

- 4.2.6 Heat-Reuse Incentives Supporting Data-Center Waste-Heat Recovery

- 4.3 Market Restraints

- 4.3.1 Limited Availability of Synthetic Dielectric Fluids with UL and EPA Approvals

- 4.3.2 Capital-Intensive Retrofit Requirements for Legacy Enterprise Data Halls

- 4.3.3 Uncertain Long-Term GPU Warranty Policies for Two-Phase Immersion Fluids

- 4.3.4 Supply-Chain Concentration of Immersion Tank Manufacturing in East Asia

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Immersion Type

- 5.1.1 Single-Phase Immersion Cooling

- 5.1.2 Two-Phase Immersion Cooling

- 5.2 By Solution Type

- 5.2.1 Immersion Cooling Tanks / Systems

- 5.2.2 Dielectric Fluids

- 5.2.3 Immersion-Optimized GPU Server Systems

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W-700W

- 5.4.3 Above 700W

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 GRC (Green Revolution Cooling)

- 6.4.2 Submer Technologies SL

- 6.4.3 LiquidStack Holding Pte. Ltd.

- 6.4.4 Engineered Fluids Inc.

- 6.4.5 Dell Technologies Inc.

- 6.4.6 Hewlett Packard Enterprise Company

- 6.4.7 Super Micro Computer Inc.

- 6.4.8 Nvidia Corporation

- 6.4.9 Advanced Micro Devices Inc.

- 6.4.10 Intel Corporation

- 6.4.11 3M Company

- 6.4.12 Shell plc

- 6.4.13 Fluoramics Inc.

- 6.4.14 Asperitas BV

- 6.4.15 Wiwynn Corporation

- 6.4.16 Midas Immersion Cooling

- 6.4.17 CoolIT Systems Inc.

- 6.4.18 Asetek A/S

- 6.4.19 Schneider Electric SE

- 6.4.20 Vertiv Holdings Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

GPU浸沒式散熱:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

GPU浸沒式散熱:市佔率分析、產業趨勢與統計、成長預測(2026-2031年) 浸沒式冷卻市場規模、佔有率和趨勢分析報告:按產品、冷卻劑、應用、地區和細分市場分類(2026-2033 年)

浸沒式冷卻市場規模、佔有率和趨勢分析報告:按產品、冷卻劑、應用、地區和細分市場分類(2026-2033 年) 浸沒式冷卻市場:2026-2032年全球市場預測(按組件、冷卻方式、冷卻能力、冷卻介質、應用、產業和公司規模分類)

浸沒式冷卻市場:2026-2032年全球市場預測(按組件、冷卻方式、冷卻能力、冷卻介質、應用、產業和公司規模分類) 全球浸沒式冷卻市場(至2040年):產業趨勢與預測

全球浸沒式冷卻市場(至2040年):產業趨勢與預測 相變液浸式冷卻伺服器市場報告:趨勢、預測與競爭分析(至2035年)浸沒式冷卻用含氟液體市場:按類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)

相變液浸式冷卻伺服器市場報告:趨勢、預測與競爭分析(至2035年)浸沒式冷卻用含氟液體市場:按類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年) 液冷市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、材料類型、設備、最終用戶及功能分類

液冷市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、材料類型、設備、最終用戶及功能分類 全球浸沒式冷卻市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球浸沒式冷卻市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 浸沒式冷卻市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、冷卻劑、地區和競爭對手分類,2021-2031年半導體濕式清洗用含氟液體市場按類型、晶圓尺寸、純度等級、應用和最終用戶分類 - 全球預測(2026-2032 年)

浸沒式冷卻市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、冷卻劑、地區和競爭對手分類,2021-2031年半導體濕式清洗用含氟液體市場按類型、晶圓尺寸、純度等級、應用和最終用戶分類 - 全球預測(2026-2032 年)