|

市場調查報告書

商品編碼

2063958

GPU浸沒式散熱:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)GPU Immersion Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

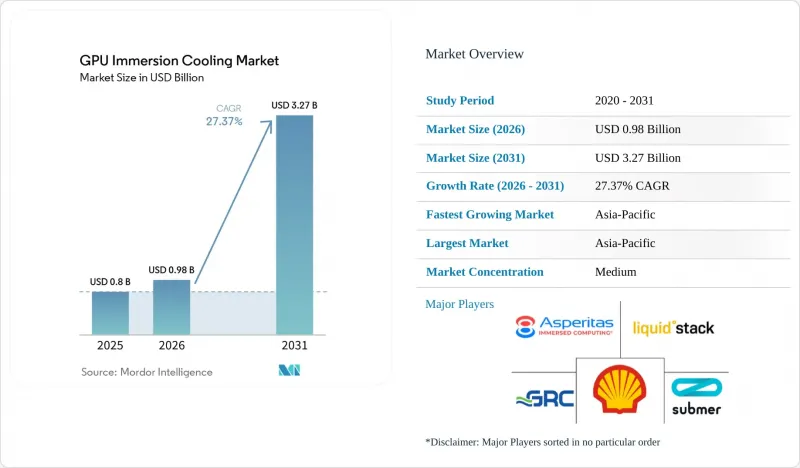

根據 Mordor Intelligence 預測,GPU 浸沒式冷卻市場預計將從 2025 年的 8 億美元成長到 2026 年的 9.8 億美元,到 2031 年達到 32.7 億美元,2026 年至 2031 年的複合年成長率為 27.37%。

本報告按浸沒式冷卻類型(單相浸沒式冷卻和兩相浸沒式冷卻)、冷卻液類型(浸沒式冷卻槽/系統、介電液和浸沒式冷卻最佳化型GPU伺服器系統)、部署方式(超大規模/雲、企業級及其他)、GPU功率密度(低於300W、300W-700W和地區進行細分高於700W。市場預測以美元(USD)計價。

全球GPU浸沒式散熱市場趨勢及洞察

人工智慧訓練設施中機架功率密度的提高

根據NVIDIA的內部藍圖,其GB200 NVL72機架目前可提供132千瓦的功率,預計到2028年,每個機架的功率將大幅提升至240至800千瓦。然而,要滿足如此高的負載需求,需要對空調基礎設施進行大幅升級,包括引入更大的風道和輔助處理器。這些組件會消耗設施中相當一部分電力,可能佔總能耗的40%至50%。相較之下,浸沒式冷卻解決方案提供了更節能的替代方案,其電源使用效率(PUE)低至1.02。這種方法預計在10兆瓦容量的設施中將年度能耗降低高達40%,這為其在高效能運算環境中的應用提供了強力的論證。

加速制定資料中心永續性相關法規

自2026年起,歐盟能源效率指令將強制要求能耗超過1兆瓦的設施採用熱回收技術。該指令將使液冷系統成為歐洲都市區的實際標準解決方案。在德國,該指令規定最低熱回收率必須達到30%,進一步強調了更節能實踐的轉變。同樣,華盛頓州設定了嚴格的目標,力爭在2027年之前達到低於1.2的電源供應效率(PUE)。中國也推出了相關法規,要求新建的超大規模資料中心在2026年之前PUE低於1.25。這些具有約束力的法規結構正在推動浸沒式冷卻技術的廣泛應用,並引發全球能源效率標準的重大變革。

浸沒式冷卻系統現場服務技能不足

浸沒式冷卻要求技術人員管理絕緣液的化學性質、監測溶解氣體分析,並對充滿液體的機箱內的伺服器進行熱插拔維護,這些技能並未包含在傳統的資料中心培訓課程中。設備製造商正透過推出認證項目來應對這項挑戰。 Green Revolution Cooling 於 2022 年推出了“ElectroSafe 合作夥伴計劃”,併計劃到 2025 年在全球範圍內認證 200 多名技術人員,但這仍然不足以支持預計的部署計劃。這種技能缺口在新興市場最為嚴重,這些市場的資料中心基礎設施正在快速擴張,而技術教育基礎設施卻相對落後。印度電子和資訊技術部已與產業組織合作開發浸沒式冷卻培訓模組,但預計要到 2027 年才能全面部署。

細分市場分析

到2025年,單相技術將佔據GPU(圖形處理器)浸沒式冷卻市場79.22%的佔有率,這主要得益於其易於操作和低廉的冷卻液成本。該技術可與現有冷卻器整合,並適用於現有企業設施的改造升級。雙相浸沒式冷卻利用潛熱沸騰,每個機架的處理能力可超過150千瓦,預計年複合成長率將達到27.54%。對於單相方法已達到其熱極限的尖端人工智慧叢集而言,雙相技術是理想之選。

微軟的GB300叢集等超大規模試點項目表明,兩相機架在無需水泵的情況下,PUE值運作低至1.06。挑戰包括含氟液體的高成本以及即將推出的PFAS法規。儘管如此,機架功率密度的提高以及無需主動水泵驅動,預計將推動高電價地區兩相系統的應用激增。

預計到2025年,水箱和外部系統將佔GPU浸沒式冷卻市場總收入的56.45%,凸顯了市場對專為商用伺服器設計的模組化機箱的日益青睞。這一趨勢反映了資料中心基礎設施對靈活可擴展解決方案的需求不斷成長。介電液仍然是穩定可靠的收入來源,但在整體市場價值中的佔有率仍然相對較小。在OEM廠商採用工廠密封底盤的推動下,針對浸沒式冷卻最佳化的圖形處理器(GPU)伺服器預計將實現27.66%的顯著複合年成長率。這些底盤無需第三方水箱,簡化了安裝流程,並可為已安裝系統節省10-15%的成本。

Supermicro 的 HGX B300 以及戴爾、HPE 和聯想的同類產品都整合了冷凝器和防滴漏快速接頭等先進功能。然而,這些創新可能會導致專有液冷生態系統的形成,從而限制互通性。將預測性維護分析和熱再生功能整合到解決方案中的供應商正在獲得競爭優勢。這些改進符合市場垂直整合的趨勢,使企業能夠在競爭日益激烈的環境中脫穎而出。

區域分析

預計到2025年,亞太地區將以67.34%的市佔率引領圖形處理器(GPU)液冷市場,並在2031年之前維持28.05%的複合年成長率。隨著中國強制要求到2026年PUE值低於1.25,液冷對於10兆瓦以上的新建設設施而言已成為不可或缺的配置。日本的「綠色轉型聯盟」為液冷應用提供稅額扣抵,而新加坡的「綠色標誌」則為減少蒸發水的使用提供加分。印度正在開發一套星級評定系統,其中將包含液冷獎勵,預計2027年開始實施。

北美則位居第二,引領美國超大規模資料中心業者的發展。華盛頓州低於 1.2 的 PUE 法規和加州修訂後的第 24 號能源法規正在推動新計畫中採用液冷技術。微軟的 132 千瓦機架實現了 1.06 的 PUE,證明了商業性可行性。加拿大和墨西哥也正在效仿,試點部署工作正在進行中。

歐洲的發展趨勢受法定廢熱再利用義務和每噸60-90歐元(70-105美元)的碳排放成本的影響。德國強制規定廢熱回收率達30%,英國正在討論強制揭露PUE值,法國則為市政供熱整合計畫提供資金。南美洲、中東和非洲仍在發展中,但高昂的電價、水資源短缺以及政府主導的人工智慧計畫正在推動其進步。巴西正在考慮提供關稅激勵措施,阿拉伯聯合大公國則在其國家人工智慧戰略中試點應用浸沒式冷卻技術。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 提高人工智慧訓練設施的機架功率密度

- 加速制定資料中心永續性相關法規

- 水資源短缺正在推動無液冷卻技術的應用。

- 合成介電溶液的成本降低曲線

- OEM廠商發表身臨其境型式GPU參考設計

- 碳定價政策正在擴大空冷系統和碳冷系統之間的總擁有成本差距。

- 市場限制因素

- 身臨其境型系統中缺乏現場服務技術

- 一級雲端服務供應商的認證週期很長

- 新型無 PFAS 冷卻劑的監管不確定性

- 改裝實施需要較高的初始資本投入

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 浸入式

- 單相浸沒式冷卻

- 兩相浸沒式冷卻

- 按解決方案類型

- 浸入式冷卻罐/系統

- 介電液

- 針對液冷散熱最佳化的GPU伺服器系統

- 不同的發展

- 超大規模/雲

- 公司

- 政府和研究機構(高效能運算)

- 按GPU功率密度

- 小於300瓦

- 300W~700W

- 超過700瓦

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 東南亞

- 其他亞太國家

- 南美洲

- 巴西

- 其他南美國家

- 中東和非洲

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Submer Technologies SL

- Green Revolution Cooling Inc.

- LiquidStack Inc.

- Asperitas BV

- Midas Immersion Cooling

- Engineered Fluids LLC

- Shell plc(Immersion Fluids)

- ZutaCore

- Hypertec Immersion Cooling

- Fujitsu Limited

- Dell Technologies Inc.(OEM Immersion-Ready Servers)

- Lenovo Group Limited

- Hewlett Packard Enterprise Company

- NVIDIA Corporation(Reference Designs)

- Super Micro Computer Inc.

- Gigabyte Technology Co., Ltd.

- Wiwynn Corporation

- Allied Control Ltd.

- DCX-The Liquid Cooling Company

- ExaScaler Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the gPU immersion cooling market size is expected to increase from USD 0.80 billion in 2025 to USD 0.98 billion in 2026 and reach USD 3.27 billion by 2031, growing at a CAGR of 27.37% over 2026-2031.

This report is Segmented by Immersion Type (Single-Phase Immersion Cooling, and Two-Phase Immersion Cooling), Solution Type (Immersion Cooling Tanks/Systems, Dielectric Fluids, and Immersion-Optimized GPU Server Systems), Deployment (Hyperscale/Cloud, Enterprise, and More), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global GPU Immersion Cooling Market Trends and Insights

Increasing Rack Power Density In AI Training Facilities

NVIDIA's internal roadmaps indicate that its GB200 NVL72 rack, which currently delivers 132 kilowatts, is expected to scale up significantly to a range of 240-800 kilowatts per rack by 2028. However, supporting these higher loads requires substantial enhancements to air infrastructure, including the implementation of oversized plenums and auxiliary handlers. These components can consume a considerable portion of a facility's power, accounting for approximately 40-50% of total energy usage. In contrast, immersion cooling solutions offer a more energy-efficient alternative, enabling the maintenance of Power Usage Effectiveness (PUE) values as low as 1.02. This approach has the potential to reduce annual energy consumption by up to 40% for facilities with a 10-megawatt capacity, presenting a compelling case for its adoption in high-performance computing environments.

Accelerated Data-Center Sustainability Mandates

Beginning in 2026, the European Energy Efficiency Directive will require the reuse of heat for sites with energy consumption exceeding 1 megawatt. This regulation effectively establishes liquid cooling systems as the default solution in urban areas across Europe. In Germany, the directive mandates a minimum of 30% heat recovery, further emphasizing the shift toward energy-efficient practices. Similarly, Washington state has set a stringent target of achieving a Power Usage Effectiveness (PUE) of less than 1.2 by 2027, while China has introduced a regulation requiring new hyperscale data center builds to meet a PUE threshold of below 1.25 by 2026. These binding regulatory frameworks are driving the widespread adoption of immersion cooling technologies, marking a significant transformation in energy efficiency standards globally.

Limited Field Service Skill Sets For Immersion Systems

Immersion cooling requires technicians to manage dielectric fluid chemistry, monitor dissolved-gas analysis, and perform hot-swap server maintenance within liquid-filled enclosures, competencies absent from traditional data center training curricula. Equipment manufacturers are responding by launching certification programs; Green Revolution Cooling introduced its ElectroSafe Partner Program in 2022, certifying over 200 technicians globally by 2025, yet this remains insufficient to support the projected deployment pipeline. The skill gap is most acute in emerging markets, where data center infrastructure is expanding rapidly but technical education infrastructure lags. India's Ministry of Electronics and Information Technology has partnered with industry associations to develop immersion-cooling training modules, though widespread deployment is not expected until 2027.

Other drivers and restraints analyzed in the detailed report include:

- Water Scarcity Driving Liquid-Free Cooling Adoption

- Declining Cost Curve Of Synthetic Dielectric Fluids

- Long Qualification Cycles For Tier-1 Cloud Providers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase technology carried 79.22% of the GPU (Graphics Processing Unit) immersion cooling market share in 2025, favored for operational simplicity and lower fluid cost. It integrates with existing chillers and suits enterprise retrofits. Two-phase immersion delivers latent-heat boiling that handles >150 kilowatts per rack and is projected for a 27.54% CAGR, ideal for frontier AI clusters where single-phase approaches thermal ceilings.

Hyperscale pilots, such as Microsoft's GB300 cluster, show two-phase racks operating at 1.06 PUE while eliminating pumps. The trade-off remains the high price of fluorinated fluids and looming PFAS regulations. Even so, rising rack power density and the elimination of active pumping are expected to pull two-phase adoption sharply higher in high-electricity jurisdictions.

In 2025, tanks and external systems accounted for 56.45% of total revenue of the GPU immersion cooling market, highlighting the growing preference for modular pods specifically designed to accommodate off-the-shelf servers. This trend reflects the increasing demand for flexible and scalable solutions in data center infrastructure. While dielectric fluids contribute to a steady and recurring revenue stream, their share of the overall value remains comparatively smaller. Immersion-optimized Graphics Processing Unit servers are projected to achieve a significant 27.66% CAGR, driven by the adoption of factory-sealed chassis by OEMs. These chassis eliminate the need for third-party tanks, streamlining the installation process and delivering cost savings of 10-15% on installed systems.

Supermicro's HGX B300, along with equivalent offerings from Dell, HPE, and Lenovo, integrates advanced features such as condensers and drip-less quick disconnects. However, these innovations result in the establishment of proprietary fluid ecosystems, which may limit interoperability. Vendors that incorporate predictive maintenance analytics and heat-reuse integration into their solutions are gaining a competitive edge. These enhancements align with the market's shift toward vertical integration, enabling companies to differentiate themselves in an increasingly competitive landscape.

Geography Analysis

Asia-Pacific led the Graphics Processing Unit immersion cooling market with 67.34% share in 2025 and will likely post a 28.05% CAGR to 2031. China's mandate for sub-1.25 PUE by 2026 forces liquid adoption for new builds above 10 megawatts. Japan's Green Transformation League grants tax credits for liquid cooling, while Singapore's Green Mark adds bonus points for eliminating evaporative water. India is drafting star-ratings that include immersion incentives expected post-2027.

North America ranks second, anchored by U.S. hyperscalers. Washington state's sub-1.2 PUE law and California's updated Title 24 energy code encourage immersion in new projects. Microsoft's 132-kilowatt racks reached 1.06 PUE, proving commercial viability; Canada and Mexico follow with pilot deployments.

Europe's trajectory is shaped by statutory heat-reuse and carbon costs of EUR 60-90 (USD 70-105) per metric ton. Germany demands 30% waste-heat capture, the U.K. is consulting on mandatory PUE disclosure, and France funds municipal heat integrations. South America and the Middle East and Africa are nascent but motivated by high electricity prices, water scarcity, and sovereign AI programs, with Brazil exploring tariff incentives and the UAE piloting immersion for its national AI strategy.

- Submer Technologies SL

- Green Revolution Cooling Inc.

- LiquidStack Inc.

- Asperitas B.V.

- Midas Immersion Cooling

- Engineered Fluids LLC

- Shell plc (Immersion Fluids)

- ZutaCore

- Hypertec Immersion Cooling

- Fujitsu Limited

- Dell Technologies Inc. (OEM Immersion-Ready Servers)

- Lenovo Group Limited

- Hewlett Packard Enterprise Company

- NVIDIA Corporation (Reference Designs)

- Super Micro Computer Inc.

- Gigabyte Technology Co., Ltd.

- Wiwynn Corporation

- Allied Control Ltd.

- DCX - The Liquid Cooling Company

- ExaScaler Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Rack Power Density in AI Training Facilities

- 4.2.2 Accelerated Data-Center Sustainability Mandates

- 4.2.3 Water Scarcity Driving Liquid-Free Cooling Adoption

- 4.2.4 Declining Cost Curve of Synthetic Dielectric Fluids

- 4.2.5 OEM Release of Immersion-Ready GPU Reference Designs

- 4.2.6 Carbon-Pricing Policies Elevating TCO Gap vs. Air Cooling

- 4.3 Market Restraints

- 4.3.1 Limited Field Service Skill Sets for Immersion Systems

- 4.3.2 Long Qualification Cycles for Tier-1 Cloud Providers

- 4.3.3 Regulatory Ambiguity Around New PFAS-Free Coolants

- 4.3.4 High Up-Front CAPEX for Retro-Fit Deployments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Immersion Type

- 5.1.1 Single-Phase Immersion Cooling

- 5.1.2 Two-Phase Immersion Cooling

- 5.2 By Solution Type

- 5.2.1 Immersion Cooling Tanks / Systems

- 5.2.2 Dielectric Fluids

- 5.2.3 Immersion-Optimized GPU Server Systems

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Southeast Asia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Submer Technologies SL

- 6.4.2 Green Revolution Cooling Inc.

- 6.4.3 LiquidStack Inc.

- 6.4.4 Asperitas B.V.

- 6.4.5 Midas Immersion Cooling

- 6.4.6 Engineered Fluids LLC

- 6.4.7 Shell plc (Immersion Fluids)

- 6.4.8 ZutaCore

- 6.4.9 Hypertec Immersion Cooling

- 6.4.10 Fujitsu Limited

- 6.4.11 Dell Technologies Inc. (OEM Immersion-Ready Servers)

- 6.4.12 Lenovo Group Limited

- 6.4.13 Hewlett Packard Enterprise Company

- 6.4.14 NVIDIA Corporation (Reference Designs)

- 6.4.15 Super Micro Computer Inc.

- 6.4.16 Gigabyte Technology Co., Ltd.

- 6.4.17 Wiwynn Corporation

- 6.4.18 Allied Control Ltd.

- 6.4.19 DCX - The Liquid Cooling Company

- 6.4.20 ExaScaler Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

北美GPU浸沒式散熱:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)

北美GPU浸沒式散熱:市佔率分析、產業趨勢與統計及成長預測(2026-2031年) 浸沒式冷卻市場規模、佔有率和趨勢分析報告:按產品、冷卻劑、應用、地區和細分市場分類(2026-2033 年)

浸沒式冷卻市場規模、佔有率和趨勢分析報告:按產品、冷卻劑、應用、地區和細分市場分類(2026-2033 年) 浸沒式冷卻市場:2026-2032年全球市場預測(按組件、冷卻方式、冷卻能力、冷卻介質、應用、產業和公司規模分類)

浸沒式冷卻市場:2026-2032年全球市場預測(按組件、冷卻方式、冷卻能力、冷卻介質、應用、產業和公司規模分類) 全球浸沒式冷卻市場(至2040年):產業趨勢與預測

全球浸沒式冷卻市場(至2040年):產業趨勢與預測 相變液浸式冷卻伺服器市場報告:趨勢、預測與競爭分析(至2035年)浸沒式冷卻用含氟液體市場:按類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年)

相變液浸式冷卻伺服器市場報告:趨勢、預測與競爭分析(至2035年)浸沒式冷卻用含氟液體市場:按類型、應用、最終用戶和分銷管道分類,全球預測(2026-2032年) 液冷市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、材料類型、設備、最終用戶及功能分類

液冷市場分析及預測(至2035年):依類型、產品、服務、技術、組件、應用、材料類型、設備、最終用戶及功能分類 全球浸沒式冷卻市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球浸沒式冷卻市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 浸沒式冷卻市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、冷卻劑、地區和競爭對手分類,2021-2031年半導體濕式清洗用含氟液體市場按類型、晶圓尺寸、純度等級、應用和最終用戶分類 - 全球預測(2026-2032 年)

浸沒式冷卻市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、應用、冷卻劑、地區和競爭對手分類,2021-2031年半導體濕式清洗用含氟液體市場按類型、晶圓尺寸、純度等級、應用和最終用戶分類 - 全球預測(2026-2032 年)