|

市場調查報告書

商品編碼

2063914

冰淇淋冷凍庫:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Ice-Cream Freezers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

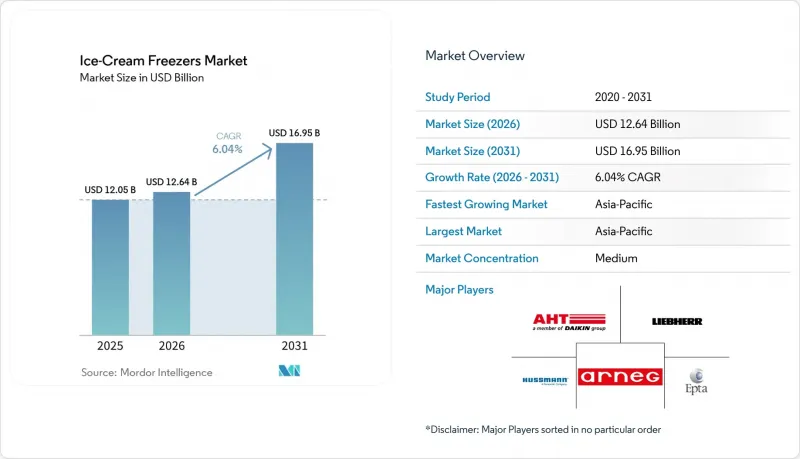

根據 Mordor Intelligence 預測,冰淇淋冷凍庫市場預計將從 2025 年的 120.5 億美元成長到 2026 年的 126.4 億美元,到 2031 年達到 169.5 億美元,2026 年至 2031 年的複合年成長率為 6.04%。

本報告按產品類型(水平、垂直、浸入式、台式、島式/多層式)、冷卻技術(靜態、通風式、混合式、乙二醇/水循環式)、容量(300公升以下、301-600公升、600公升以上)、終端用戶(超級市場、便利商店、冰淇淋店、餐飲分銷服務業、酒吧)細分。市場預測以美元計價。

全球冰淇淋冷凍庫市場趨勢與洞察

氫氟碳化合物分階段減量和能源效率監管正在創造結構性更換需求。

歐盟的《氟氣體法規》(EU) 2024/573禁止自2025年1月1日起在新自主型商用冷凍設備中使用全球暖化潛勢(GWP)為150或更高的氟氣體,這正在推動冰淇淋冷凍庫市場的結構性變革。這將直接影響使用傳統冷媒R134a和R404A的冷凍庫。在美國,《AIM法案》強制要求新獨立式商用冷凍設備從同一日期起過渡到使用GWP為150或更低的冷媒,並且2024-2028年的氫氟碳化合物(HFC)配額上限已降至基準值的60%。歐盟2024年的HFC消費量已比《蒙特婁議定書》的目標低60%,顯示現有系統的使用者正面臨冷媒供應緊張的局面。這項變化對冰淇淋冷凍庫市場有重大影響。這是因為,由於新的HFC供應合約,繼續使用老舊設備的企業將面臨更高的維護成本。因此,企業在決定更換設備時,越來越不僅考慮設備使用壽命的結束,還考慮整體擁有成本和合規風險。

亞太地區零售門市網路的擴張與現代化

亞太地區目前擁有最大的市場規模和最快的成長速度,這使得該地區的冰淇淋冷凍庫市場比其他依賴更新換代需求的地區擁有更強勁的結構性需求基礎。 2023年,印度冰淇淋市場價值達3,000億印度盧比(約35億美元),預計該品類將成長13%至15%,這主要得益於有組織零售的擴張和人均消費量的成長。零售網路的擴張不僅限於大型大賣場。在中國、印度和東南亞,社區雜貨店和便利商店也正在擴大其冷凍食品處理能力。由於這些小規模商店通常需要的是即插即用的冷櫃而非集中式管理系統,因此冰淇淋冷凍庫市場的需求主要集中在300公升以下和301-600公升的容量範圍內。實際上,氣候溫暖的都市區商店數量的增加直接轉化為對新型冷櫃的需求,尤其是在冷凍甜點銷售仍然主要受衝動消費驅動的地區。

缺乏HC/CO2相關技術技能及對安全標準的遵守情況

冰淇淋冷凍庫市場在向R290和二氧化碳系統過渡的過程中面臨瓶頸,因為這一轉變依賴於一群尚未掌握最新安全和操作要求的技術人員。歐盟《氟碳化合物法規》(EU) 2024/573 要求成員國建立天然冷媒技術人員認證項目,相關實施細則將於2025年前陸續制定。認證進度與勞動力短缺之間的差距可能會延誤安裝和設備過渡,即使買家願意為此付費。小規模企業尤其謹慎,因為不當操作碳氫化合物系統可能導致保險問題或違反建築規範。因此,儘管冰淇淋冷凍庫市場需求依然強勁,但實際安裝速度可能會受到勞動力供應和合規風險的限制。

細分市場分析

到2025年,臥式/大型冷凍庫將佔據冰淇淋冷凍庫市場佔有率的34.23%,這反映出它們在亞太、非洲和南美洲品牌冷凍庫專案中的深度滲透。由於跨國冰淇淋品牌繼續根據獨家或半獨家經銷協議在獨立零售商處安裝臥式冷凍櫃,其市場地位仍然穩固。它們的安裝更新周期更多地受到冷媒法規合規性的影響,而非產品展示過時。在衝動消費場所,冰淇淋冷凍庫市場仍依賴臥式冷凍櫃,因為在這些場所,低成本、耐用性和易於維護比視覺展示更為重要。這確保了即使冷凍甜點周轉率穩定,臥式冷凍櫃在占地面積有限的路邊零售商、售貨亭和社區商店仍然保持著高需求。

隨著大型零售商轉向垂直陳列以增強商品可見性和便於比較,預計到2031年,垂直/玻璃門冷凍庫的複合年成長率將達到6.18%,成為所有產品類型中成長最快的。歐盟能源法規是推動這一趨勢的主要因素,自2023年9月1日起,冰淇淋冷凍庫的能源效率指數(EEI)必須低於50%,這促使受監管市場更傾向於選擇新型垂直設計。隨著義式霜淇淋和高級甜點逐漸進入先前鮮有涉足的市場,冰淇淋冷櫃和舀取式冷凍櫃的需求也隨之成長。島式/多層冷凍庫仍然是大型超級市場地面陳列的標配,隨著門市設備的現代化,它們正被升級為全球暖化潛勢(GWP)更低的型號。雖然桌上型冰淇淋冷凍庫仍然是最小的細分市場,但它們受益於咖啡館、快餐店和甜點菜單的擴張,這使得冰淇淋冷凍庫行業能夠在一般零售之外獲得一個利基產品細分市場。

預計到2025年,靜態冷卻系統將佔冰淇淋冷凍櫃銷售額的44.92%,凸顯了冰淇淋冷凍庫市場仍高度依賴品牌店和小規模零售商使用的低成本即插即用型冷凍櫃。這類冷凍櫃經久不衰的原因在於其操作簡單、安裝成本低,以及在鼓勵衝動消費的通路中長期穩定的應用。監管壓力也促使製造商最佳化現有平台而非棄用,從而提升了靜態系統的持續有效性。事實上,許多業者更傾向於選擇維護和安裝更便利的改良型靜態冷凍櫃。這一趨勢解釋了為何即使先進技術日漸普及,冰淇淋冷凍庫市場仍保持著龐大的用戶群。

到2031年,遠端乙二醇/水循環(SPI)系統將以每年6.88%的速度成長,成為所有冷凍技術中成長最快的,因為它們既滿足冷媒法規要求,又能柔軟性商店佈局。 AHT冷凍系統公司於2025年在泰國安裝了其VENTO SPI環形回路系統。該公司報告稱,與R404A機架式系統相比,該系統年能耗降低了12%,冷媒充填量減少了97%。此外,在德國安裝的混合式R290插入式水循環系統使超級市場的總能耗降低了8.8%,並在溫暖季節將暖通空調負載降低了高達40%。 EN IEC 60335-2-89:2022標準中的充填量限制規定進一步推動了分散式架構的普及,這種架構將冷媒分配到小規模的封閉迴路中,而不是單一大型集中式充填器。雖然固定式機組在冰淇淋冷凍庫市場的安裝基數上仍然佔據主導地位,但水循環環形回路系統正在塑造這項技術的未來。

區域分析

預計到2025年,亞太地區將佔據冰淇淋冷凍庫市場37.13%的佔有率,並將在2031年實現7.23%的最高複合年成長率。這種罕見的組合表明,市場需求存在結構性成長,而非只是暫時的更換需求激增。該地區受益於冷凍甜點消費量的成長、零售業的快速復甦以及有利於全年可見式商用冷凍庫需求的氣候條件。印度是強勁的長期成長要素,有組織零售業的擴張提高了低溫運輸滲透率,並使人均消費量從低點持續成長。此外,與許多溫帶市場相比,該地區的高溫使得門市層面的散熱問題更為緊迫,預計環形回路系統和半插電式系統很快就會得到商業性應用。

預計到2031年,歐洲市場將以每年3.50%的速度成長,這主要得益於亞太地區更為溫和但仍明確的設備更新周期,而這一週期又受到監管合規性的推動。由於該地區擁有龐大且成熟的設備裝置基礎,設備更新更依賴法規、效率提升和技術升級,而非新店開業。歐盟的生態設計法規和EPREL法規提高了產品對比的透明度,而歐盟氟碳化合物法規(EU) 2024/573則加速了老舊HFC設備的淘汰壓力。預計到2031年,北美市場將以每年4.50%的速度成長,這主要得益於AIM法案和對高階手工冷凍甜點的需求。在這兩個地區,冰淇淋冷凍庫市場的目標正從單純追求銷售成長轉向追求性能更高、全球暖化潛勢(GWP)更低、數據更透明的設備。

預計到2031年,南美洲將以每年5.00%的速度成長,而西亞預計將在較低的基數上以5-6%的速度成長,非洲則約為4%。由於這些地區尚處於發展初期,短期內,零售現代化和低溫運輸投資將比監管升級更為重要。 《基加利框架》在引導開發中國家逐步減少氫氟碳化合物的使用並支持其從傳統冷媒逐步過渡方面仍然發揮著重要作用。隨著門市網路和餐飲服務業的現代化,這些地區的冰淇淋冷凍庫市場預計不僅會透過大規模的設備升級來實現成長,還會透過新設備的安裝和選擇性升級相結合的方式來實現成長。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對氫氟碳化合物分階段減量和提高效率的要求將加速其替代週期。

- 亞太地區零售門市網路的擴張與現代化

- 採用天然冷媒(R290/CO2)可實現高效的即插即用運作。

- 超級市場、便利商店和高級義式霜淇淋店的成長。

- 能源標籤和採購透明度(歐盟)正在加速更新。

- 水循環/半插入式架構可實現熱回收和靈活佈局。

- 市場限制因素

- 缺乏有關碳氫化合物和二氧化碳的技術技能和對安全標準的遵守情況

- 能源價格波動帶來的高昂初始成本

- 碳氫化合物填充量/房間面積限制限制了某些安裝位置

- 歐盟在市場監管和合規方面的負擔正在延長採購週期。

- 產業價值鏈分析

- 波特五力模型

- 洞察最新產業趨勢與創新

- 近期產業趨勢分析(新產品發布、策略性舉措、投資、合作、合資、業務擴張、併購等)

- 對冰淇淋冷凍機的商用終端使用者購買行為和關鍵選擇標準進行分析。

第5章 市場規模與成長預測

- 依產品類型

- 胸型/大

- 立式/玻璃門

- 浸漬櫃/舀取

- 檯面型

- 島嶼/多層甲板型

- 按類型分類的冷卻技術

- 靜止的

- 通風/強制對流

- 混合

- 乙二醇/水環型(SPI)

- 以體積(公升)

- 300公升或以下

- 301~600L

- 超過600公升

- 最終用戶

- 超級市場和大賣場

- 便利商店和加油站

- 冰淇淋店和義式冰淇淋店

- 餐飲(餐廳、咖啡廳、QSR)

- 酒吧和俱樂部

- 透過分銷管道

- 銷售代理商/經銷商

- OEM直銷/主要客戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- AHT Cooling Systems(Daikin)

- Epta Group(IARP/Eurocryor)

- Arneg Group

- ISA SpA

- Liebherr Professional

- Hussmann(Panasonic)

- Carrier Commercial Refrigeration

- Beverage-Air(Ali Group)

- Turbo Air

- Master-Bilt

- Nor-Lake

- Sanden Intercool

- Blue Star (India)

- Western Refrigeration (India)

- Rockwell Industries

- Vestfrost Solutions

- TEFCOLD

- Jordao

- Maxx Cold

- Avantco

第7章 市場機會與未來展望

According to Mordor Intelligence, the ice-cream freezers market size is expected to increase from USD 12.05 billion in 2025 to USD 12.64 billion in 2026 and reach USD 16.95 billion by 2031, growing at a CAGR of 6.04% over 2026-2031.

This report is Segmented by Product Type (Chest, Upright, Dipping, Countertop, and Island/Multideck), Cooling Technology (Static, Ventilated, Hybrid, and Glycol/Waterloop), Capacity (≤300L, 301-600L, and >600L), End User (Supermarkets, C-Stores, Ice-Cream Parlors, Horeca, and Bars), Sales Channel (Distributors and Direct OEM), and Geography. Market Forecasts in Value (USD).

Global Ice-Cream Freezers Market Trends and Insights

HFC Phase-Down and Efficiency Mandates Creating Structural Replacement Demand

The ice-cream freezer market is entering a structural replacement phase because the European Union F-Gas Regulation (EU) 2024/573 banned fluorinated gases with a GWP of 150 or more in new self-contained commercial refrigeration equipment from January 1, 2025, directly affecting legacy R134a and R404A freezer fleets. In the United States, the AIM Act requires new stand-alone commercial refrigeration units to shift to refrigerants with a GWP below 150 on the same date, while the HFC allowance cap for 2024-2028 fell to 60% of baseline . European Union HFC consumption in 2024 was already 60% below Montreal Protocol targets, which shows how quickly the available refrigerant pool has tightened for owners of legacy systems. That change matters for the ice-cream freezers market because operators who keep older equipment in service face higher servicing exposure due to virgin HFC supply contracts. The result is that replacement decisions are increasingly being justified by total ownership cost and compliance risk rather than by simple end-of-life timing.

Retail Footprint Expansion and Modernization in Asia-Pacific

Asia-Pacific combines the largest current base with the fastest growth path, giving the ice-cream freezers market a stronger structural demand base than in regions where growth depends on replacement. India's ice-cream business was valued at INR 30,000 crore (USD 3.5 billion) in 2023, and the category is expected to grow at 13%-15% as organized retail expands and per-capita consumption rises. That retail build-out is not limited to large-format hypermarkets, because neighborhood grocery and convenience formats are also widening frozen-food capacity across China, India, and Southeast Asia. Those smaller stores usually need plug-in cabinets rather than centralized systems, so demand tilts toward the ≤300L and 301-600L bands in the ice-cream freezers market. The practical effect is that store-count growth in warm-climate urban corridors converts directly into new cabinet demand, especially where impulse purchases still dominate frozen dessert sales.

Technician Skill Gaps and Safety Code Compliance for HC/CO2

The ice-cream freezers market faces a conversion bottleneck because the move to R290 and CO2 systems depends on a technician base that is still catching up with new safety and handling requirements. European Union F-Gas Regulation (EU) 2024/573 requires member states to establish certification programs for natural-refrigerant technicians, and implementing rules began to appear through 2025. The gap between certification timelines and workforce capacity can cause installation and fleet conversion to lag even when buyers are ready to spend. Smaller operators are particularly cautious because improper handling of hydrocarbon systems can raise insurance concerns and trigger building code violations. As a result, the ice-cream freezers market may see demand remain healthy while actual installation velocity is constrained by labor availability and compliance risk.

Other drivers and restraints analyzed in the detailed report include:

- Natural Refrigerant Adoption Enabling Higher-Efficiency Plug-in Units

- Growth of Supermarkets, Convenience Formats, and Premium Gelato Outlets

- High Upfront Costs Amid Energy Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chest/Deep Freezers held 34.23% of the ice-cream freezer market share in 2025, reflecting their deep entrenchment in branded freezer programs across Asia-Pacific, Africa, and South America. Their position remains strong because multinational ice-cream brands continue to place chest units with independent retailers under exclusive or semi-exclusive distribution arrangements. That installed base is replaced on a cycle shaped more by refrigerant compliance than by merchandising obsolescence. The ice-cream freezers market still relies on chest formats in impulse-heavy locations where low cost, durability, and simple maintenance matter more than visual presentation. This keeps chest units highly relevant in roadside retail, kiosks, and neighborhood outlets where frozen dessert turnover is steady, but floor area is limited.

Upright/Glass-Door Freezers are projected to grow at a 6.18% CAGR through 2031, the fastest rate among product types, as organized retail shifts toward vertical visibility and clearer product comparisons. European Union energy rules have reinforced that shift, as ice-cream freezers had to meet an EEI threshold of 50% or less from September 1, 2023, favoring newer vertical designs in regulated markets . Dipping Cabinets and Scooping Freezers are gaining more addressable demand as gelato and premium dessert formats expand into markets where they previously had little formal presence. Island/Multideck Freezers remain tied to larger supermarket floor displays and are being refreshed on lower-GWP platforms as store fleets modernize. Countertop Ice-Cream Freezers remain the smallest sub-segment, yet they benefit from cafe, QSR, and dessert menu expansion, which gives the ice-cream freezers industry a specialist product layer beyond mainstream retail.

Static cooling systems accounted for 44.92% of 2025 revenues, underscoring how much the ice-cream freezers market still relies on low-cost plug-in cabinets used in branded fleets and small-format retail. Their staying power is linked to simplicity, lower acquisition costs, and a long history of installation in impulse channels. Static systems have also remained viable because compliance pressure has pushed manufacturers to optimize familiar platforms rather than abandon them. In practice, many operators prefer an improved static unit that is easy to service and install. That dynamic helps explain why the base of the ice-cream freezers market remains broad even as advanced technologies gain attention.

Remote Glycol/Waterloop (SPI) systems are growing at 6.88% through 2031, the fastest pace among cooling technologies, because they address both refrigerant compliance and store-layout flexibility. AHT Cooling Systems deployed its VENTO SPI waterloop system in Thailand in 2025. They reported a 12% reduction in annual energy use against an R404A rack system, along with a 97% reduction in refrigerant charge. A hybrid R290 plug-in water-loop installation in Germany also cut total supermarket energy use by 8.8% and reduced air-conditioning load by up to 40% in warmer months. Charge-limit rules under EN IEC 60335-2-89:2022 have further strengthened the case for distributed architectures by spreading refrigerant across smaller sealed circuits rather than a single large, centralized charge. In the ice-cream freezers market, which means waterloop systems are shaping the future of technology, even as static units continue to dominate the installed base.

Geography Analysis

Asia-Pacific held 37.13% of the ice-cream freezer market share in 2025 and is also forecast to post the fastest regional CAGR of 7.23% through 2031. That rare combination points to structural demand rather than a short replacement spike. The region benefits from rising frozen dessert consumption, rapid retail formalization, and climate conditions that sustain year-round demand for visible commercial freezer placement. India adds a strong long-term layer because organized retail expansion is improving cold-chain reach while per-capita consumption continues to rise from a low base. The region also offers an early commercial case for waterloop and semi plug-in systems because high ambient temperatures make heat rejection a more immediate store-level issue than in many temperate markets.

Europe is projected to grow at 3.50% through 2031, which is slower than Asia-Pacific but still supported by a clear compliance-led replacement cycle. The region's installed base is large and mature, so equipment refresh depends more on regulations, efficiency, and technology upgrades than on the creation of new outlets. European Union Ecodesign and EPREL rules have made product comparison more transparent, and the European Union F-Gas Regulation (EU) 2024/573 has accelerated pressure on legacy HFC fleets. North America is forecast to grow at 4.50% through 2031, supported by the AIM Act and by demand for premium and artisan frozen dessert formats. In both regions, the ice-cream freezers market is moving toward better-specified, lower-GWP, and more data-visible equipment rather than simply toward higher unit volumes.

South America is projected to grow at 5.00% through 2031, while Western Asia is expected to expand in the 5%-6% range and Africa in the 4% range, from lower bases. These regions are at an earlier stage of development, so retail modernization and cold-chain investment matter more than regulation-driven replacement in the near term. The Kigali framework remains important because it pulls developing economies onto the HFC phase-down path and supports a gradual shift away from legacy refrigerants. As store networks and foodservice formats modernize, the ice-cream freezers market in these geographies should expand through a mix of first-time installations and selective upgrades, rather than solely through broad fleet conversion.

- AHT Cooling Systems (Daikin)

- Epta Group (IARP/Eurocryor)

- Arneg Group

- ISA S.p.A.

- Liebherr Professional

- Hussmann (Panasonic)

- Carrier Commercial Refrigeration

- Beverage-Air (Ali Group)

- Turbo Air

- Master-Bilt

- Nor-Lake

- Sanden Intercool

- Blue Star (India)

- Western Refrigeration (India)

- Rockwell Industries

- Vestfrost Solutions

- TEFCOLD

- Jordao

- Maxx Cold

- Avantco

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 HFC phase-down and efficiency mandates driving replacement cycles

- 4.2.2 Retail footprint expansion and modernization in Asia-Pacific

- 4.2.3 Natural refrigerants (R290/CO2) adoption enabling higher-efficiency plug-ins

- 4.2.4 Growth of supermarkets/convenience formats and premium gelato outlets

- 4.2.5 Energy labeling and procurement transparency (EU) accelerating upgrades

- 4.2.6 Waterloop/semi plug-in architectures enabling heat recovery and flexible layouts

- 4.3 Market Restraints

- 4.3.1 Technician skill gaps and safety code compliance for HC/CO2

- 4.3.2 High upfront costs amid energy price volatility

- 4.3.3 Hydrocarbon charge/room-size limits restricting some sites

- 4.3.4 EU market surveillance and conformity burdens elongating purchase cycles

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Competitive Rivalry

- 4.5.2 Supplier Power

- 4.5.3 Buyer Power

- 4.5.4 Threat of Substitutes

- 4.5.5 Threat of New Entrants

- 4.6 Insights into the Latest Trends and Innovations in the Industry

- 4.7 Insights into the Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, Etc.) in the Industry

- 4.8 Insights into Commercial End Users' Buying Behavior and Key Selection Criteria for Icecream Freezers

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Chest/Deep Freezers

- 5.1.2 Upright/Glass-Door Freezers

- 5.1.3 Dipping Cabinets/Scooping Freezers

- 5.1.4 Countertop Ice-Cream Freezers

- 5.1.5 Island/Multideck Freezers for Ice-Cream

- 5.2 By Cooling Technology

- 5.2.1 Static

- 5.2.2 Ventilated/Forced-Air

- 5.2.3 Hybrid

- 5.2.4 Remote Glycol/Waterloop (SPI)

- 5.3 By Capacity (Liters)

- 5.3.1 <=300 L

- 5.3.2 301-600 L

- 5.3.3 >600 L

- 5.4 By End User

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Convenience Stores/Gas Stations

- 5.4.3 Ice-Cream Parlors & Gelaterias

- 5.4.4 HoReCa (Restaurants, Cafes, QSRs)

- 5.4.5 Bars & Clubs

- 5.5 By Sales Channel

- 5.5.1 Distributors/Dealers

- 5.5.2 Direct OEM/Key Accounts

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Italy

- 5.6.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East And Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East And Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 AHT Cooling Systems (Daikin)

- 6.4.2 Epta Group (IARP/Eurocryor)

- 6.4.3 Arneg Group

- 6.4.4 ISA S.p.A.

- 6.4.5 Liebherr Professional

- 6.4.6 Hussmann (Panasonic)

- 6.4.7 Carrier Commercial Refrigeration

- 6.4.8 Beverage-Air (Ali Group)

- 6.4.9 Turbo Air

- 6.4.10 Master-Bilt

- 6.4.11 Nor-Lake

- 6.4.12 Sanden Intercool

- 6.4.13 Blue Star (India)

- 6.4.14 Western Refrigeration (India)

- 6.4.15 Rockwell Industries

- 6.4.16 Vestfrost Solutions

- 6.4.17 TEFCOLD

- 6.4.18 Jordao

- 6.4.19 Maxx Cold

- 6.4.20 Avantco

7 Market Opportunities & Future Outlook

- 7.1 Digital energy-and-compliance procurement (EPREL + API telemetry) bundles for ice-cream fleets

- 7.2 Tropicalized hydrocarbon semi plug-in (waterloop) retrofits with heat recovery for small-format stores

2026-2030年全球商用冰淇淋冷凍庫市場

2026-2030年全球商用冰淇淋冷凍庫市場 商用冰淇淋冷凍庫:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

商用冰淇淋冷凍庫:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 商用冷凍和冷凍設備市場:2026-2032年全球市場預測(按產品類型、儲存容量、冷媒類型、冷凍系統、價格範圍、控制方式、溫度等級、安裝位置、分銷管道和最終用戶分類)冷藏儲物櫃市場:2026-2032 年全球市場預測(按類型、溫度區、材質、應用和所有權分類)-按類型、溫度區、材料、應用和所有權分類。

商用冷凍和冷凍設備市場:2026-2032年全球市場預測(按產品類型、儲存容量、冷媒類型、冷凍系統、價格範圍、控制方式、溫度等級、安裝位置、分銷管道和最終用戶分類)冷藏儲物櫃市場:2026-2032 年全球市場預測(按類型、溫度區、材質、應用和所有權分類)-按類型、溫度區、材料、應用和所有權分類。 商用冷凍和冷凍設備市場:按產品類型、應用和地區分類

商用冷凍和冷凍設備市場:按產品類型、應用和地區分類 商用冷凍和冷凍設備市場規模、佔有率和趨勢分析報告:按產品類型、系統類型、容量、應用、冷媒、分銷管道、地區和細分市場預測(2026-2033 年)貨運冷藏櫃市場:依產品類型、溫度範圍、冷凍系統、容量、終端用戶產業、通路分類,全球預測(2026-2032年)

商用冷凍和冷凍設備市場規模、佔有率和趨勢分析報告:按產品類型、系統類型、容量、應用、冷媒、分銷管道、地區和細分市場預測(2026-2033 年)貨運冷藏櫃市場:依產品類型、溫度範圍、冷凍系統、容量、終端用戶產業、通路分類,全球預測(2026-2032年) 商用冷凍和冷藏食品市場報告:按產品類型、最終用戶和地區分類(2026-2034 年)

商用冷凍和冷藏食品市場報告:按產品類型、最終用戶和地區分類(2026-2034 年) 全球商用冷凍設備市場規模、佔有率、趨勢及成長分析報告(2026-2034)日本食品服務冷藏解決方案市場規模、佔有率、趨勢和預測:按產品類型、門類型、技術、最終用戶和地區分類(2026-2034 年)

全球商用冷凍設備市場規模、佔有率、趨勢及成長分析報告(2026-2034)日本食品服務冷藏解決方案市場規模、佔有率、趨勢和預測:按產品類型、門類型、技術、最終用戶和地區分類(2026-2034 年)