|

市場調查報告書

商品編碼

2062209

商用冰淇淋冷凍庫:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Commercial Ice Cream Freezers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

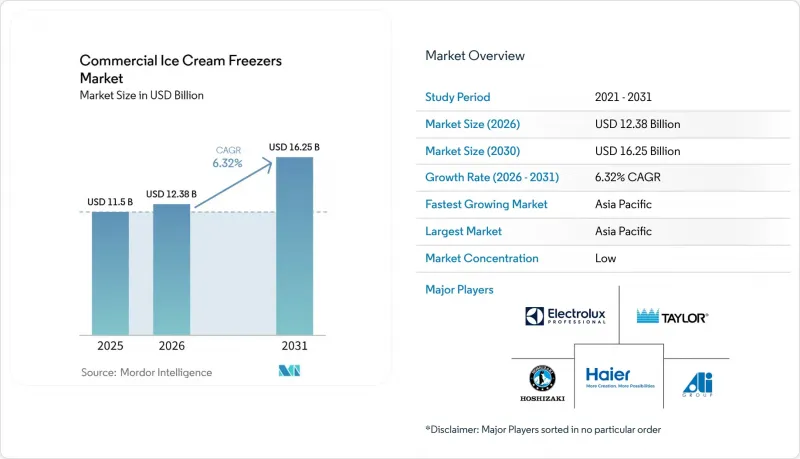

根據 Mordor Intelligence 預測,商用冰淇淋冷凍庫市場規模預計到 2025 年將達到 115 億美元,到 2026 年將達到 123.8 億美元,到 2031 年將達到 162.5 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 6.32%。

本報告按產品類型(臥式冷凍櫃/深冷凍櫃等)、冷凍技術(靜態冷凍等)、容量(300公升以下等)、最終用戶(冰淇淋店/義式冰淇淋店等)、銷售管道(直接銷售給OEM廠商等)和地區(北美等)進行細分。市場預測以美元計價。

全球商用冰淇淋冷凍庫市場趨勢與洞察

新興市場速食連鎖店的擴張

快餐連鎖加盟商正在亞太、中東和拉丁美洲地區擴張其冷凍甜點基礎設施,顯著提升了對商用冰淇淋冷凍庫的需求。 2026年2月,馬來西亞麥當勞宣布了一項高達10億馬幣(約2.55億美元)的大規模投資計畫。其中,6億馬幣將用於新店建設,計劃在未來5至10年內開設45至75家加盟店。每家門市的投資額約為500萬至700馬幣,其中包括冷凍設備。同樣,Dairy Queen也專注於在中東地區擴張,尤其是在阿拉伯聯合大公國和沙烏地阿拉伯。正如FFCC Global所指出的,這些地區的快餐市場預計將以14%的複合年成長率穩步成長,而沙烏地阿拉伯85%的快餐消費者年齡在45歲以下,Dairy Queen的軟冰淇淋和暴風雪冰淇淋等產品非常符合市場需求。 Central Retail也積極拓展越南市場,計劃在2026年至2028年間開設30多家大型門市,其中包括10至12家「Go!」購物中心和大賣場,以及23至25家「Mini Go!」迷你門市。每家店都需要多個冷凍展示櫃,用於銷售衝動型消費品和外帶冰淇淋。由於加盟商需要對整個連鎖店的設備進行標準化,以保持產品一致性並滿足專利經營的要求,因此此次擴張導致對冷凍庫的需求穩定但並不均衡。

便利商店和加油站的衝動性冰淇淋零售量成長。

便利商店和加油站正在重新定位冰淇淋,使其從季節性附加商品轉變為全年熱銷商品,這需要專門的冷凍展示櫃,以便進行醒目的品牌宣傳和靈活的安裝。根據Mini Melts公司預測,到2024年,澳洲加油站和便利商店通路的冰淇淋銷售額將達到2.13億澳元,年增3.1%。單份包裝佔據主導地位,品牌櫃檯式冷凍庫據稱已將衝動性購買量提升了35%。 Mini Melts透過在現有安裝空間內提供70克和72克包裝的冰淇淋,並將其放置在多功能冷凍庫中,在短短六個月內將其在澳洲的便利商店數量從14家擴展到超過950家,這充分展現了產品形式創新如何能夠快速拓展配銷通路。零售商正在最佳化冷凍庫空間,優先展示高周轉率的SKU和開心果、焦糖餅乾和抹茶等高階潮流產品。同時,汽油、飲料和零食等商品的跨品類商品搭售導致購物車容量增大。隨著消費者越來越注重健康和包容性,例如高蛋白、低卡路里、無麩質、無乳製品和純素食產品,零售商擴大採用玻璃頂展示冷凍庫,以便在銷售點展示產品的多樣性和營養成分。

高昂的初始採購和安裝成本

資本密集度仍然是小規模企業和加盟商進入商用冰淇淋冷凍庫市場的一大障礙。步入式冷藏庫和冷凍庫的價格差異很大,從小型 6x6 英尺(約 1.8 公尺 x 1.8 公尺)的 4,000 美元到大型 12x16 英尺(約 3.6 公尺 x 4.8 公尺)的 35,000 美元以上不等。由於冷櫃的隔熱材料更厚、冷卻系統更強大,其價格比冷藏庫冷凍庫高出 20% 到 40%。安裝費用從 2,000 美元到 7,000 美元不等,電氣維修從 200 美元到 500 美元不等,許可證採集費用從 200 美元到 500 美元不等,導致專案總成本比設備標價高出 20% 到 40%。立式冷凍庫的價格差異很大,從入門級經濟型(使用壽命3-5年)的1200美元到高階型(使用壽命15-20年)的10000美元不等,其中還包含一些隱性成本,例如運費(75-300美元)、擱箱費以及腳輪和拆板(每個50-100美元)。能源成本佔總擁有成本的很大一部分,經濟型冷凍櫃每天耗電12千瓦時,而節能之星認證的型號每天僅耗電6千瓦時。以每千瓦時0.12美元計算,節能型冷凍櫃的年耗電成本為525美元,而節能之星認證型號為262美元,10年下來可節省2630美元。

細分市場分析

到2025年,臥式和深型冷凍櫃將佔產品類型銷售額的34.58%,凸顯其在超級市場、大賣場和冷藏倉庫大容量儲存中的重要角色。預計到2031年,用於製作義式義式霜淇淋和軟冰淇淋的批量冷凍機將以7.82%的複合年成長率成長,這主要得益於手工冰淇淋生產商和快餐店(QSR)對高效系統的採用。卡比詹尼(Carpigiani)的「Labotronic HE-H」批量冷凍機採用Hard-O-Dynamic自適應技術,可減少30%的電力和用水量。 Nemox的「Gelato 10K i.Green」大量冷凍機使用R290冷媒(全球暖化潛值3),在12-15分鐘內即可生產10公斤冰淇淋,同時減少99.95%的二氧化碳排放。立式和玻璃頂冷凍庫提高了產品的可見性,尤其是玻璃頂冷凍櫃,已使便利商店的銷售額提高了 35%。

在中國和印度,義式霜淇淋批量冷凍機越來越受歡迎,因為消費者願意為採用天然原料和獨特口味手工製作的產品支付更高的價格。 Cattabriga 的「Multifreeze Icona Hybrid」批量冷凍機採用取得專利的雙冷凝系統,可減少 80% 的用水量,並降低 30% 的電力和水耗。 Gram Equipment 位於丹麥的冰技術中心自 2021 年運作以來,可為新冰淇淋產品提供經濟高效的前導測試,並將測試成本降低 70% 至 80%。雖然臥式冷凍庫在大容量儲存方面仍然經濟實惠,但它們缺乏垂直或玻璃頂冷凍櫃的展示效果。批量冷凍機現在也配備了「Crystal」程序,用於存放單件商品和冷凍蛋糕,從而實現收入來源多元化。

2025年,由於初始成本低且易於安裝,靜態冷卻技術佔了45.62%的市場。遠端乙二醇冷卻系統預計到2031年將以8.11%的複合年成長率成長,這主要得益於大型零售商和冷庫運營商尋求集中式製冷系統以降低製冷劑充注量、符合美國環保署(EPA)法規並降低能耗。雖然遠端冷凝機組具有更大的容量和更高的效率,但額外的安裝要求會使初始成本增加20%至40%。 Hussmann的「Protocol CO2」機架採用模組化架構和鐵/銅管道,符合加州Title 24法規,並且其無霜系統減少了維護工作。 Liebherr的「NoFrost」技術面向食品服務和旅館業,提供氣候等級5的可靠性和C級或更高的能源效率等級。

遠端乙二醇冷卻系統在超級市場和大賣場中越來越受歡迎,因為它們能將冷媒用量控制在EPA(美國環保署)規定的閾閾值以下,並簡化洩漏監測。 Hussmann公司於2023年10月推出的「Krack MicroDS」和「MicroSC Monoblock」系統整合了預充R290冷媒的冷凝器和蒸發器,與HFC(氫氟碳化合物)系統相比,冷媒用量最多可減少95%,年度二氧化碳排放減少6%。由於其結構簡單、成本低廉,靜態冷卻系統在小規模商店和對成本敏感的場所中佔據主導地位。同時,無需人工除霜的免霜系統在冰淇淋店等場所也越來越受歡迎。雖然預計遠程乙二醇冷卻系統將在大型商店的安裝和整修中得到應用,但靜態冷卻系統在價格敏感的市場中仍可能佔據主導地位。

區域分析

到2025年,亞太地區將佔全球冰淇淋市場規模的38.92%,預計到2031年將以7.68%的複合年成長率穩定成長。這一成長主要得益於人均消費量的成長、速食店(QSR)的擴張、電子商務低溫運輸的發展以及中國、印度和東南亞的都市化。 2023年,印度有組織的冰淇淋市場價值為3,000億盧比(約35億美元),預計到2028年將達到5,000億盧比(約58.3億美元)。人均消費量從2011年的400毫升成長到2023年的1.6升。然而,這一數字仍遠低於紐西蘭的28.4公升和美國的20.8公升,凸顯了印度冰淇淋市場巨大的成長潛力。預計到2025年,中國冰淇淋市場規模將達到205.7億美元,到2034年將成長至354.4億美元,年複合成長率(CAGR)為6.23%。這項成長主要得益於千禧世代和Z世代對抹茶、紅豆、芋頭、荔枝和芒果等獨特口味的偏好。在北京、上海、廣東和江蘇等主要城市,手工冰淇淋店和特色精品店正在快速擴張。

在印度,Zepto、Swiggy Instamart 和 Blinkit 等電商平台以及中國大型電商公司正在推動冷凍食品宅配市場的成長。這一趨勢導致暗店和微型倉配中心對冷凍庫容量的需求不斷增加。 Central Retail 正在越南進行大量投資,計劃在 2026 年至 2028 年間開設 30 多家大型門市,其中包括 10-12 家「Go! Mall」購物中心和大賣場,以及 23-25 家「Mini Go!」迷你店。星崎株式會社 (Hoshizaki Corporation) 透過在 2026 年 3 月增持其越南子公司股份,以及在 2025 年 11 月擴大其天然冷媒產品線,展現了對該地區的承諾。北美和歐洲仍然是關鍵市場。旨在減少高全球暖化潛勢 (GWP) 冷媒和提高能源效率的法規正在加速設備更新換代。自2026年1月1日起,美國環保署(EPA)將冷媒充填量閾值從50磅降至15磅。此外,《AIM法案技術過渡條例》也將自2026年1月1日起禁止安裝使用高全球暖化潛勢(GWP)冷媒的新系統。這些條例正在加速淘汰傳統的氫氟碳化合物(HFC)裝置。 2026年3月,Epta以超過20億歐元(約22億美元)的價格收購了Hauser公司,從而增強了其在德語區(德國、奧地利、瑞士)、中歐和東南歐的工業和地理影響力。此次收購新增了位於奧地利和捷克的生產設施,進一步提升了Epta提供天然冷媒和節能解決方案的能力。

中東正崛起為速食店(QSR)投資的重要目的地。冰雪皇后(Dairy Queen)的目標市場是阿拉伯聯合大公國和沙烏地阿拉伯,預計這兩個國家的速食市場將以超過14%的複合年成長率成長。尤其值得注意的是,沙烏地阿拉伯有85%的速食消費者年齡在45歲以下。同時,拉丁美洲面臨電網不穩定和資金限制等挑戰。南非低溫運輸產業報告稱,限電(道路斷電)導致每月成本增加5萬至100萬蘭特,收入損失5萬至50萬蘭特。為了應對電力波動並最大限度地減少停機時間,撒哈拉以南非洲和拉丁美洲部分地區正在使用配備手動控制電池供電警報器的堅固耐用、技術含量低的設備。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 速食連鎖店在新興市場的擴張

- 便利商店和加油站的衝動性購買冰淇淋零售市場成長。

- 能源效率法規正在加速設備的更換。

- 亞太地區冷凍甜點消費量不斷增加。

- 引入利用物聯網的預測性維護

- 透過「冷凍櫃即服務」租賃降低資本支出。

- 市場限制因素

- 高昂的初始採購和安裝成本

- 對氫氟碳化合物、氫氟烯烴和氟化氣體制定嚴格的逐步淘汰規定。

- 發展中地區電網的不穩定性會縮短運作時間。

- 二手設備市場正在蠶食新產品的銷售量。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 臥式冷凍櫃和深式冷凍櫃

- 立式冷凍庫

- 玻璃頂展示冷凍庫

- 冰淇淋沾醬櫃

- 用於製作義式霜淇淋和軟冰淇淋的大量冷凍機

- 冷卻技術

- 靜態冷卻

- 自然通風和強制空氣冷卻

- 防凍和防凍系統

- 遠端乙二醇冷卻系統

- 按產能

- 低於300公升

- 301-600公升

- 超過600公升

- 最終用戶

- 冰淇淋店和冰淇淋店

- 速食店(QSR)

- 超級市場和大賣場

- 便利商店和加油站

- 電影院、體育場和娛樂場所

- 餐飲及機構食品服務

- 按銷售管道

- 直接 OEM

- 分銷商和經銷商

- 線上

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 瑞典

- 波蘭

- 比利時

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 越南

- 印尼

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 智利

- 秘魯

- 哥倫比亞

- 其他南美國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市場排名分析

- 公司簡介

- Ali Group

- AHT Cooling Systems

- Taylor Company

- Electrolux Professional

- Haier Group

- Bonnet Neve

- Delfield(Middleby Corporation)

- Electrolux Professional

- Epta Group

- Excellence Industries

- Fagor Industrial

- Foster Refrigerator(ITV Group)

- GGM Gastro

- Gram Commercial A/S

- Haier Group(GE Appliances)

- Hoshizaki Corporation

- Hussmann Corp.

- Igloo Products Corp.

- Imbera Cooling

- ISA Italy

- Liebherr-Hausgerate GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the commercial ice cream freezers market size is projected to be USD 11.5 billion in 2025, USD 12.38 billion in 2026, and reach USD 16.25 billion by 2031, growing at a CAGR of 6.32% from 2026 to 2031.

This report is Segmented by Product Type (Chest / Deep Freezers, and More), Cooling Technology (Static Cooling, and More), Capacity (Less Than Equal To 300 L, and More), End User (Ice-Cream Parlors & Gelaterias, and More), Sales Channel (Direct OEM, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Commercial Ice Cream Freezers Market Trends and Insights

Expansion of Quick-Service Restaurant Chains in Emerging Markets

QSR franchises are scaling up their frozen-dessert infrastructure across Asia-Pacific, the Middle East, and Latin America, significantly boosting the demand for commercial ice cream freezers. In February 2026, McDonald's Malaysia announced a major RM 1 billion (USD 255 million) investment. Out of this, RM 600 million is allocated for new restaurants, with plans to establish 45 to 75 franchised outlets over the next 5 to 10 years. Each outlet will require an investment of RM 5 million to RM 7 million, including refrigeration equipment. Similarly, Dairy Queen is focusing on expanding in the Middle East, particularly in the UAE and Saudi Arabia. With QSR markets in these regions expected to grow at a strong 14% CAGR and 85% of Saudi Arabia's fast-food consumers under 45, Dairy Queen's soft-serve and Blizzard offerings align well with market demand, as noted by FFCC Global. Central Retail is also pursuing growth in Vietnam, planning to open over 30 large-format stores between 2026 and 2028. This includes 10 to 12 Go! malls and hypermarkets, along with 23 to 25 mini Go! stores. Each store will require multiple freezer cabinets for impulse and take-home ice cream. These expansions are driving a steady yet uneven demand for freezers, as franchisees standardize equipment across chains to maintain product consistency and meet franchisor requirements.

Growth in Impulse Ice-Cream Retail at Convenience and Fuel Stops

Convenience stores and fuel stations are repositioning ice cream from seasonal add-ons to year-round traffic drivers, necessitating dedicated freezer cabinets with branded merchandising and flexible placement. Australia's petrol and convenience channel generated AUD 213 million in ice cream sales in 2024, up 3.1% year-over-year, with single-serve formats dominating and branded counter freezers delivering impulse uplift of up to 35% according to Mini Melts. Mini Melts expanded from 14 to over 950 Australian convenience stores within six months by offering 70g and 72g pouches in multipurpose freezers compatible with existing footprints, demonstrating how product-format innovation can rapidly scale distribution. Operators are rationalizing freezer space to favor high-velocity SKUs and premium trends such as pistachio, Biscoff, and matcha, while cross-category bundling with fuel, drinks, and snacks is boosting basket size. The shift toward health-conscious and inclusive offerings, including high-protein, reduced-calorie, gluten-free, dairy-free, and vegan options, is prompting retailers to install glass-top display freezers that showcase product variety and nutritional credentials at the point of sale.

High Upfront Procurement and Installation Costs

Capital intensity remains a formidable barrier for small operators and franchisees entering the commercial ice cream freezer market. Walk-in coolers and freezers range from USD 4,000 for small 6x6 units to over USD 35,000 for large 12x16 installations, with freezers commanding 20% to 40% premiums over coolers due to thicker insulation and more powerful refrigeration systems. Installation labor adds USD 2,000 to USD 7,000, electrical upgrades cost USD 200 to USD 500, and permits run USD 200 to USD 500, pushing total project costs 20% to 40% higher than equipment sticker prices. Reach-in freezers span USD 1,200 for entry-level economy units with 3 to 5 year lifespans to USD 10,000 for premium spec-line models with 15 to 20 year lifespans, with hidden costs including freight (USD 75 to USD 300), uncrating fees, and casters or shelves at USD 50 to USD 100 each. Energy costs dominate the total cost of ownership, with economy units consuming 12 kWh per day versus Energy Star models at 6 kWh per day, yielding USD 525 versus USD 262 annually at USD 0.12 per kWh and USD 2,630 in savings over 10 years.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Regulations Accelerating Equipment Replacements

- Rising Frozen-Dessert Consumption in Asia-Pacific

- Stringent Refrigerant Phase-Out Rules for HFC, HFO, and F-Gas

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, chest and deep freezers accounted for 34.58% of product-type revenue, emphasizing their role in bulk storage for supermarkets, hypermarkets, and cold-storage warehouses. Gelato and soft-serve batch freezers are projected to grow at a 7.82% CAGR through 2031, driven by artisanal producers and QSRs adopting high-efficiency systems. Carpigiani's Labotronic HE-H batch freezer cuts electricity and water usage by 30% using Hard-O-Dynamic Adaptive technology. Nemox's Gelato 10K i-Green batch freezer, with R290 refrigerant (GWP 3), reduces CO2-equivalent emissions by 99.95% and produces 10 kg per hour in 12 to 15 minutes per cycle. Upright and glass-top freezers enhance product visibility, with glass-top units boosting convenience store sales by up to 35%.

Gelato batch freezers are gaining popularity in China and India, where consumers pay premiums for handcrafted products with natural ingredients and unique flavors. Cattabriga's Multifreeze Icona Hybrid batch freezer reduces water usage by 80% and electricity and water consumption by 30% using a patented dual-condensation system. Gram Equipment's Ice Technology Center in Denmark, operational since 2021, offers cost-effective pilot testing for new ice cream products, reducing testing costs by 70% to 80%. Chest freezers remain cost-effective for bulk storage but lack the merchandising appeal of upright and glass-top units. Batch freezers now incorporate Crystal programs for monoportions and frozen cakes, diversifying revenue streams.

In 2025, static cooling technology held a 45.62% market share due to lower upfront costs and easy installation. Remote glycol-cooled systems are projected to grow at an 8.11% CAGR through 2031, driven by large-format retailers and cold-storage operators seeking centralized refrigeration to reduce refrigerant charges, comply with EPA mandates, and lower energy use. Remote condensing units, while offering larger capacities and higher efficiencies, increase upfront costs by 20% to 40% due to additional installation requirements. Hussmann's Protocol CO2 rack supports California Title 24 compliance with modular architecture and iron/copper piping, while frost-free systems reduce maintenance labor. Liebherr's NoFrost technology targets foodservice and hospitality, offering Climate Class 5 reliability and energy ratings of C or above.

Remote glycol-cooled systems appeal to supermarkets and hypermarkets by reducing refrigerant charges below EPA thresholds and simplifying leak monitoring. Hussmann's Krack MicroDS and MicroSC Monoblock, launched in October 2023, integrate a pre-charged R290 condensing unit and evaporator, cutting refrigerant charges by up to 95% versus HFC systems and reducing annual CO2 emissions by 6%. Static cooling dominates small-format and budget-conscious installations due to simplicity and low costs, while frost-free systems gain traction in ice cream parlors by eliminating manual defrosting. Remote glycol-cooled systems are expected to grow in large-format installations and remodels, while static cooling remains prevalent in price-sensitive markets.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 38.92% of the market value and is expected to grow at a strong 7.68% CAGR through 2031. This growth is primarily driven by increasing per-capita consumption, the expansion of quick-service restaurants (QSRs), the growth of e-commerce cold chains, and urbanization in China, India, and Southeast Asia. India's organized ice cream sector, valued at Rs 30,000 crore (USD 3.5 billion) in 2023, is projected to reach Rs 50,000 crore (USD 5.83 billion) by 2028. Per-capita consumption has risen from 400 ml in 2011 to 1.6 liters in 2023. However, this remains significantly lower than New Zealand's 28.4 liters and the United States' 20.8 liters, highlighting substantial growth potential. China's ice cream market, valued at USD 20.57 billion in 2025, is forecast to grow to USD 35.44 billion by 2034, reflecting a 6.23% CAGR. This growth is fueled by millennial and Gen Z preferences for unique flavors such as matcha, red bean, taro, lychee, and mango. Artisanal shops and specialty boutiques are rapidly expanding in key cities like Beijing, Shanghai, Guangdong, and Jiangsu.

In India, quick-commerce platforms like Zepto, Swiggy Instamart, and Blinkit, along with e-commerce leaders in China, are driving frozen-food delivery growth. This trend necessitates increased freezer capacities at dark stores and micro-fulfillment centers. Central Retail is making significant investments in Vietnam, planning to open over 30 large-format stores between 2026 and 2028, including 10 to 12 Go! malls and hypermarkets, as well as 23 to 25 mini Go! stores. Hoshizaki Corporation has demonstrated its commitment to the region by acquiring additional shares in its Vietnamese subsidiary in March 2026 and expanding its natural-refrigerant lineup in November 2025. North America and Europe remain key markets. Regulatory mandates aimed at reducing high-GWP refrigerants and improving energy efficiency are driving equipment replacement cycles. Effective January 1, 2026, the U.S. EPA lowered the refrigerant charge threshold from 50 lb to 15 lb. Additionally, the AIM Act Technology Transition Rule prohibits the installation of new systems using high-GWP refrigerants after January 1, 2026. These regulations are accelerating the phase-out of legacy HFC-based units. Epta strengthened its industrial and geographic presence in DACH, Central Europe, and Central-Southeastern Europe with its March 2026 acquisition of Hauser for over EUR 2 billion (USD 2.2 billion). This acquisition added production facilities in Austria and the Czech Republic and enhanced Epta's offerings in natural refrigeration and energy-efficient solutions.

The Middle East is emerging as a key destination for QSR investments. Dairy Queen is targeting the UAE and Saudi Arabia, where QSR markets are expected to grow at over 14% CAGR. Notably, 85% of fast-food consumers in Saudi Arabia are under the age of 45. Meanwhile, Latin America faces challenges such as grid instability and capital constraints. South Africa's cold chain sector reports monthly mitigation costs ranging from ZAR 50,000 to over ZAR 1 million, along with revenue losses between ZAR 50,000 and ZAR 500,000 due to load-shedding. To address power fluctuations and minimize downtime, regions in Sub-Saharan Africa and parts of Latin America are adopting robust, low-tech units with manual controls and battery-backed alarms.

- Ali Group

- AHT Cooling Systems

- Taylor Company

- Electrolux Professional

- Haier Group

- Bonnet Neve

- Delfield (Middleby Corporation)

- Electrolux Professional

- Epta Group

- Excellence Industries

- Fagor Industrial

- Foster Refrigerator (ITV Group)

- GGM Gastro

- Gram Commercial A/S

- Haier Group (GE Appliances)

- Hoshizaki Corporation

- Hussmann Corp.

- Igloo Products Corp.

- Imbera Cooling

- ISA Italy

- Liebherr-Hausgerate GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion Of Quick-Service Restaurant Chains In Emerging Markets

- 4.2.2 Growth In Impulse Ice-Cream Retail At Convenience And Fuel Stops

- 4.2.3 Energy-Efficiency Regulations Accelerating Equipment Replacements

- 4.2.4 Rising Frozen-Dessert Consumption In Asia-Pacific

- 4.2.5 IoT-Enabled Predictive Maintenance Adoption

- 4.2.6 Freezer-As-A-Service Leasing Lowering Capital Expenditures

- 4.3 Market Restraints

- 4.3.1 High Upfront Procurement And Installation Costs

- 4.3.2 Stringent Refrigerant Phase-Out Rules For HFC, HFO, And F-Gas

- 4.3.3 Grid Instability In Developing Regions Reducing Uptime

- 4.3.4 Boom In Second-Hand Equipment Trade Cannibalizing New Sales

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Chest And Deep Freezers

- 5.1.2 Upright Freezers

- 5.1.3 Glass-Top Display Freezers

- 5.1.4 Ice-Cream Dipping Cabinets

- 5.1.5 Gelato And Soft-Serve Batch Freezers

- 5.2 By Cooling Technology

- 5.2.1 Static Cooling

- 5.2.2 Ventilated And Forced-Air Cooling

- 5.2.3 Frost-Free And No-Frost Systems

- 5.2.4 Remote Glycol-Cooled Systems

- 5.3 By Capacity

- 5.3.1 Less Than Or Equal To 300 Liters

- 5.3.2 301 To 600 Liters

- 5.3.3 Greater Than 600 Liters

- 5.4 By End User

- 5.4.1 Ice-Cream Parlors And Gelaterias

- 5.4.2 Quick-Service Restaurants (QSRs)

- 5.4.3 Supermarkets And Hypermarkets

- 5.4.4 Convenience Stores And Fuel Stations

- 5.4.5 Cinemas, Stadiums, And Entertainment Venues

- 5.4.6 Catering And Institutional Foodservice

- 5.5 By Sales Channel

- 5.5.1 Direct OEM

- 5.5.2 Distributor And Dealer

- 5.5.3 Online

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Netherlands

- 5.6.2.7 Sweden

- 5.6.2.8 Poland

- 5.6.2.9 Belgium

- 5.6.2.10 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Vietnam

- 5.6.3.7 Indonesia

- 5.6.3.8 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Chile

- 5.6.4.4 Peru

- 5.6.4.5 Colombia

- 5.6.4.6 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Ali Group

- 6.4.2 AHT Cooling Systems

- 6.4.3 Taylor Company

- 6.4.4 Electrolux Professional

- 6.4.5 Haier Group

- 6.4.6 Bonnet Neve

- 6.4.7 Delfield (Middleby Corporation)

- 6.4.8 Electrolux Professional

- 6.4.9 Epta Group

- 6.4.10 Excellence Industries

- 6.4.11 Fagor Industrial

- 6.4.12 Foster Refrigerator (ITV Group)

- 6.4.13 GGM Gastro

- 6.4.14 Gram Commercial A/S

- 6.4.15 Haier Group (GE Appliances)

- 6.4.16 Hoshizaki Corporation

- 6.4.17 Hussmann Corp.

- 6.4.18 Igloo Products Corp.

- 6.4.19 Imbera Cooling

- 6.4.20 ISA Italy

- 6.4.21 Liebherr-Hausgerate GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

2026-2030年全球商用冰淇淋冷凍庫市場

2026-2030年全球商用冰淇淋冷凍庫市場 冰淇淋冷凍庫:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

冰淇淋冷凍庫:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 商用冷凍和冷凍設備市場:2026-2032年全球市場預測(按產品類型、儲存容量、冷媒類型、冷凍系統、價格範圍、控制方式、溫度等級、安裝位置、分銷管道和最終用戶分類)冷藏儲物櫃市場:2026-2032 年全球市場預測(按類型、溫度區、材質、應用和所有權分類)-按類型、溫度區、材料、應用和所有權分類。

商用冷凍和冷凍設備市場:2026-2032年全球市場預測(按產品類型、儲存容量、冷媒類型、冷凍系統、價格範圍、控制方式、溫度等級、安裝位置、分銷管道和最終用戶分類)冷藏儲物櫃市場:2026-2032 年全球市場預測(按類型、溫度區、材質、應用和所有權分類)-按類型、溫度區、材料、應用和所有權分類。 商用冷凍和冷凍設備市場:按產品類型、應用和地區分類

商用冷凍和冷凍設備市場:按產品類型、應用和地區分類 商用冷凍和冷凍設備市場規模、佔有率和趨勢分析報告:按產品類型、系統類型、容量、應用、冷媒、分銷管道、地區和細分市場預測(2026-2033 年)貨運冷藏櫃市場:依產品類型、溫度範圍、冷凍系統、容量、終端用戶產業、通路分類,全球預測(2026-2032年)

商用冷凍和冷凍設備市場規模、佔有率和趨勢分析報告:按產品類型、系統類型、容量、應用、冷媒、分銷管道、地區和細分市場預測(2026-2033 年)貨運冷藏櫃市場:依產品類型、溫度範圍、冷凍系統、容量、終端用戶產業、通路分類,全球預測(2026-2032年) 商用冷凍和冷藏食品市場報告:按產品類型、最終用戶和地區分類(2026-2034 年)

商用冷凍和冷藏食品市場報告:按產品類型、最終用戶和地區分類(2026-2034 年) 全球商用冷凍設備市場規模、佔有率、趨勢及成長分析報告(2026-2034)日本食品服務冷藏解決方案市場規模、佔有率、趨勢和預測:按產品類型、門類型、技術、最終用戶和地區分類(2026-2034 年)

全球商用冷凍設備市場規模、佔有率、趨勢及成長分析報告(2026-2034)日本食品服務冷藏解決方案市場規模、佔有率、趨勢和預測:按產品類型、門類型、技術、最終用戶和地區分類(2026-2034 年)