|

市場調查報告書

商品編碼

2063904

微學習平台:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Microlearning Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

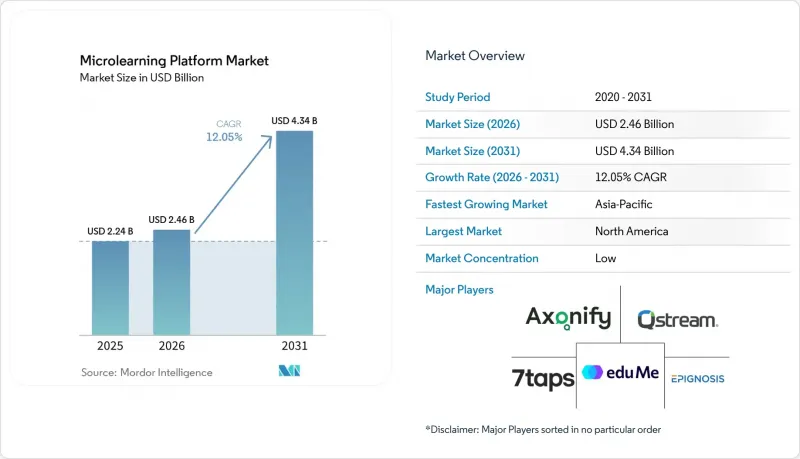

根據 Mordor Intelligence 預測,微學習平台市場規模將從 2025 年的 22.4 億美元和 2026 年的 24.6 億美元成長到 2031 年的 43.4 億美元,2026 年至 2031 年的複合年成長率為 12.05%。

本報告按平台類型(例如,獨立微學習平台)、部署模式(例如,雲端)、企業規模(例如,大型企業、中小企業)、應用領域(例如,合規培訓、員工技能發展和再培訓)、行業(例如,銀行業、金融服務業、保險業)和地區進行細分。市場預測以美元計價。

全球微學習平台市場趨勢與洞察

員工對持續技能發展和再培訓的需求日益成長。

由於當前員工技能與數位化工具、自動化和工作設計變革速度之間存在明顯的不匹配,微學習平台市場正蓬勃發展。根據《2025年未來就業報告》,39%的員工核心技能將在五年內需要更新,這使得持續學習成為私人和公共部門雇主的首要任務。這種壓力促使人們傾向於更短的學習序列,因為它們可以比冗長的訓練形式更快地更新並更頻繁地分配。人工智慧驅動的內容創作也增強了微學習平台市場的商業價值,減少了創建新模組所需的時間和精力。隨著技能再學習週期的縮短,支援快速內容更新和基於工作流程交付的供應商將更有能力滿足大型組織不斷變化的角色需求。正因如此,微學習平台市場正超越週期性培訓,並逐漸成為日常生產力基礎設施不可或缺的一部分。

無固定辦公地點和分散辦公的員工對行動優先學習的需求日益成長。

微學習平台市場的發展也得益於那些工作期間不使用桌上型電腦的遠距辦公人員的學習需求。行動優先的交付方式適用於零售、倉儲、現場服務、餐飲服務和醫療保健等行業,這些行業需要在輪班期間、任務間隙或通訊環境不穩定的情況下為員工提供培訓。透過行動應用或簡訊形式提供的短模組彌合了技能需求與技能保持之間的差距。 2026年1月,Qstream為一支在通訊環境不穩定的地區工作的製藥銷售團隊推出了基於簡訊的微學習交付服務。這表明供應商正在根據實際工作情況調整學習形式。 2026年5月,Bites Learning和EZShift宣佈建立合作關係,將培訓整合到交接班流程中。這預示著學習方式正在從外部學習轉向系統內部學習。因此,微學習平台市場不僅受益於行動訪問,也受益於學習機會與工作執行的緊密結合。

深度概念學習與程序學習能力的局限性

微學習平台市場在需要學習深奧概念或掌握嚴格順序操作流程的應用場景中仍面臨結構性限制。短模組在知識保留、記憶和習慣養成方面效果顯著,但對於需要詳細講解、指導練習或多層次先決條件的學習者而言,效果則不盡如人意。這在學習成果依賴深度和情境的領域尤其突出,例如臨床技能、技術認證、高級軟體開發和複雜設備維護。如果供應商將微學習定位為混合式或主導課程的完全替代品,而未能滿足雇主的期望,則可能面臨抵制。這些平台更永續的角色是作為更廣泛的學習系統之上的“記憶層”,但這也會限制它們能夠佔據的培訓預算比例。因此,微學習平台市場要想最有效地擴張,其行銷策略應該是將其作為混合式學習架構的一部分,而不是將其視為所有培訓形式的萬靈藥。

細分市場分析

截至2025年,整合式LMS平台佔據了微學習平台市場46.21%的佔有率,而人工智慧驅動的學習平台預計到2031年將以15.42%的複合年成長率成長。這一市場格局表明,企業仍然優先考慮與現有學習記錄、能力歷史和管理儀表板的連續性。許多中大型企業更傾向於擴展其現有的LMS環境,而不是添加需要全新工作流程、冗餘報告和自訂整合的獨立工具。因此,整合仍然是微學習平台市場的關鍵採購標準,尤其對於那些擁有成熟學習營運體系的企業而言。雖然獨立供應商仍然吸引著那些尋求更簡單部署流程和專業使用者體驗的團隊,但市場需求正持續轉向能夠與現有企業系統整合的平台。

人工智慧平台的興起正在改變決策流程。買家現在不僅評估內容庫,還關注系統創建、個人化和更新學習材料的速度。 2026年4月,Pluralsight推出了全新的人工智慧沙盒和引導式學習環境,在短學習路徑中加入了即時、可操作的回饋。這顯示人工智慧不再只是附加功能,而是產品差異化的關鍵。 2025年6月,Axonify發布了「Co-Creator」功能,使現場管理人員無需具備教學設計專業知識即可創建品牌化的微學習內容。這進一步降低了頻繁更新內容的門檻。這些發展意義重大,因為微學習平台產業越來越注重其將營運變化轉化為可操作學習機會的速度。因此,平台選擇正從簡單的「內部開發還是外包」轉變為對創建速度、個人化品質和資料連續性等因素進行更詳細的評估。

預計到2025年,基於雲端的微學習平台將佔微學習平台市場規模的68.71%,而混合雲模式預計到2031年將以14.13%的複合年成長率成長。雲端平台憑藉其快速部署、低基礎設施成本、易於更新以及對使用多種設備的分散式工作人員的強大支持,仍然是首選方案。這些優勢與微學習平台市場的日常需求高度契合,即需要快速向學習者提供內容並頻繁更新。雲端系統還使供應商能夠更快地發布新功能,這在該領域至關重要,因為人工智慧工具、報告功能和工作流程整合等功能正在不斷湧現。對於許多雇主,尤其是那些擁有分散式現場團隊的雇主而言,採用雲端仍然是擴展規模而不顯著增加IT相關負擔的最現實方式。

混合部署在某些行業正迅速發展,這些行業希望利用雲端的柔軟性,同時又不必將所有學習者資料和表現記錄置於本地控制之外。銀行、國防、醫療保健和公共部門機構通常需要將敏感資料保存在特定環境中,以滿足資料儲存位置要求、稽核或內部政策方面的要求。 2026 年 4 月,Docebo 透過在 AWS、Azure 和 Google Cloud 區域引入可設定的資料儲存位置控制,直接解決了這些採購的顧慮。支援混合架構對供應商來說是一項更具挑戰性的任務,因為他們必須同時專注於雲端的可擴展性和託管資料管理。這項挑戰構成了一道技術壁壘,將大型供應商與小型企業區分開來,也是微學習平台市場中大型企業供應商與部署能力較為有限的專業供應商之間涇渭分明的界限。

區域分析

到2025年,北美將佔據全球微學習平台市場38.66%的佔有率,成為全球最大的區域收入來源。該地區受益於企業高額的培訓支出、強大的企業軟體基礎設施以及數位化學習在企業營運中的廣泛應用。美國企業持續保持強勁的需求,因為它們已經擁有成熟的學習管理系統(LMS)環境,並配備了能夠將微學習擴展到大量員工的正式學習與發展團隊。隨著製造業和公共部門培訓體系的日益標準化,加拿大和墨西哥也為區域成長做出了貢獻。現有的基礎設施和龐大的企業基本客群為北美微學習平台市場提供了強大的支撐。

亞太地區是微學習平台市場成長最快的地區,預計到2031年將以16.21%的複合年成長率成長。這一成長主要得益於政府主導的技能發展計劃、移動優先的學習習慣以及支持系統化培訓的正規就業體系的擴展。 2024年7月,日本經濟產業省發布了《數位技能標準》1.2版,為制定全國數位人才能力標準做出了貢獻。印度國家技能發展公司(NSDC)報告稱,截至2025年2月,已有超過1,300萬名學習者透過其平台註冊,這充分展現了印度系統化技能發展活動的規模。韓國也支持擴大數位學習,計劃在 2025 年投資 169 億韓元(1,250 萬美元)用於人工智慧和數位技能提升,並透過其「AID 30+」勞動力再培訓舉措額外投資 1,100 億韓元(8,000 萬美元)。

歐洲仍然是一個成熟的區域市場,德國、英國和法國佔了大部分收入,資料管治要求正日益影響採購決策。因此,安全認證、居住管理和人工智慧合規性在整個微學習平台市場中對供應商的選擇變得愈發重要。中東正在崛起為一個重要的成長區域,尤其是在沙烏地阿拉伯和阿拉伯聯合大公國,當地的勞動力多元化計畫正在推動對可擴展數位學習的需求。雖然非洲和南美洲的收入佔有率仍然較小,但智慧型手機的高普及率為在分散式工作環境中進行行動傳輸提供了實際優勢。隨著企業數位化逐步擴展到學習科技的採購,非洲的南非、奈及利亞和肯亞以及南美洲的巴西、阿根廷和哥倫比亞正在各自區域推動需求成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對勞動力持續技能發展和再培訓的需求日益成長。

- 無固定辦公地點和分散式辦公團隊對行動優先學習的需求日益成長。

- 人工智慧驅動的個人化與加速內容創作

- 擴大微學習在合規和風險管理的應用

- 利用協作應用程式、文字訊息和QR碼觸發器提供業務工作流程。

- 人工智慧翻譯與在地化助力全球擴張

- 市場限制因素

- 它不適合加深概念性和程序性學習。

- 雲端和行動傳輸中的資料隱私和網路安全問題

- 嵌入式學習旅程中投資報酬率歸因分析的不足之處

- 通知疲勞和內容片段化

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依平台類型

- 獨立微學習平台

- 整合式學習管理系統平台

- 人工智慧驅動的學習平台

- 按部署模式

- 雲

- 現場

- 混合

- 按最終用戶公司規模分類

- 大公司

- 小型企業

- 透過使用

- 新進員工入職及崗位準備

- 合規培訓

- 銷售賦能與產品培訓

- 勞動力技能發展和再培訓

- 領導力和軟性技能發展

- 面向客戶和合作夥伴的教育

- 按最終用戶行業分類

- BFSI

- 資訊科技/通訊

- 零售與電子商務

- 製造業

- 醫療保健和生命科學

- 教育

- 政府/公共部門

- 媒體與娛樂

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 新加坡

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介。

- Axonify Inc.

- Qstream, Inc.

- eduMe Ltd.

- Epignosis LLC

- 7taps OpCo LLC

- Neovation Corporation

- Gnowbe Pte. Ltd.

- MobieTrain Corp.

- Digemy Pty Ltd.

- Bites Learning Ltd.

- Arist Holdings Inc.

- Throwing Boulders, LLC

- LEADx, Inc.

- RapL Inc.

- Handy Training Technologies Private Limited

- 5Mins AI Ltd.

- Uptime App Ltd.

- Fivel Systems Corporation

- iSpring Solutions, Inc.

- Bigtincan Holdings Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the microlearning platform market size is projected to expand from USD 2.24 billion in 2025 and USD 2.46 billion in 2026 to USD 4.34 billion by 2031, registering a CAGR of 12.05% between 2026 to 2031.

This report is Segmented by Platform Type (Standalone Microlearning Platforms, and More), Deployment Model (Cloud, and More), Enterprise Size (Large Enterprises, and SME), Application (Compliance Training, Workforce Upskilling and Reskilling, and More), Industry Vertical (Banking, Financial Services, and Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Microlearning Platform Market Trends and Insights

Growing Need For Continuous Workforce Upskilling And Reskilling

The microlearning platform market is gaining momentum due to a clear mismatch between current workforce skills and the pace of change in digital tools, automation, and job design. The Future of Jobs 2025 report stated that 39% of workers' core skills will need updating within 5 years, which keeps continuous learning high on employer agendas across both private and public organizations. That pressure favors short learning sequences because they can be updated faster and assigned more frequently than longer training formats. It also strengthens the business case for the microlearning platform market, as AI-assisted authoring reduces the time and effort required to create new modules. As reskilling cycles become shorter, vendors that support rapid content refreshes and workflow-based delivery are better placed to serve large organizations with shifting role requirements. This is why the microlearning platform market is moving closer to day-to-day productivity infrastructure rather than remaining limited to periodic training.

Mobile-First Learning Demand Across Deskless And Distributed Workforces

The microlearning platform market is also being supported by learning demand from deskless and distributed employees who do not spend the workday on desktop systems. Mobile-first delivery fits retail, warehousing, field service, food service, and healthcare settings where training has to reach employees during shifts, between tasks, or in low-connectivity environments. Short modules delivered through mobile apps or text-based formats reduce the gap between when a skill is needed and when it is reinforced. Qstream expanded into SMS-based microlearning delivery in January 2026 for pharmaceutical field sales teams working in low-connectivity settings, showing how vendors are adapting the format to operational realities. Bites Learning and EZShift announced a partnership in May 2026 to embed training into shift handover workflows, signaling a broader shift toward learning within operational systems rather than outside them. The microlearning platform market is therefore benefiting not only from mobile access but also from the closer alignment between learning moments and work execution.

Limited Suitability For Deep Conceptual Or Procedural Mastery

The microlearning platform market still faces a structural ceiling in use cases that require deep conceptual learning or tightly sequenced procedural mastery. Short modules are effective for reinforcement, recall, and habit formation, but they are less effective when learners need long-form explanations, supervised practice, or layered prerequisite knowledge. This matters in areas such as clinical skills, technical certification, advanced software development, and complex equipment maintenance, where learning outcomes depend on depth and context. Vendors that position microlearning as a full replacement for blended or instructor-led programs may face pushback if employer expectations are not met. A more durable role for these platforms is as a reinforcement layer on top of broader learning systems, but that also limits how much of the total training budget they can capture. The microlearning platform market, therefore, expands most effectively when sold as part of a mixed learning architecture rather than as a universal substitute for all training formats.

Other drivers and restraints analyzed in the detailed report include:

- AI-Powered Personalization And Faster Content Authoring

- Rising Use Of Microlearning For Compliance And Risk Management

- Data Privacy And Cybersecurity Concerns In Cloud And Mobile Delivery

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated LMS platforms held 46.21% of the microlearning platform market share in 2025, while AI-enabled learning platforms are projected to grow at a 15.42% CAGR through 2031. That split shows that enterprises still value continuity with their existing learning records, competency histories, and manager dashboards. Many mid-sized and large organizations prefer to extend their current LMS environments rather than add a separate tool that requires new workflows, duplicate reporting, or custom integrations. This explains why integration remains a primary buying criterion for the microlearning platform market, especially among employers with mature learning operations. Standalone vendors still attract interest from teams seeking a simpler deployment path and a more focused user experience, but demand continues to lean toward platforms that integrate with existing enterprise systems.

The rise of AI-enabled platforms is changing that decision process because buyers now assess not only content libraries, but also how quickly a system can produce, personalize, and refresh learning material. Pluralsight launched a new AI sandbox and guided learning environment in April 2026 that added real-time practice feedback within short learning paths, which shows how AI is becoming part of product differentiation rather than a side feature. Axonify launched Co-Creator in June 2025, enabling frontline managers to build branded microlearning content without instructional design expertise, further lowering the barrier to frequent content updates. These moves matter because the microlearning platform industry is increasingly judged by how fast it can turn operational changes into usable learning moments. As a result, platform selection is shifting from a simple build-versus-buy choice to a more detailed evaluation of authoring speed, personalization quality, and data continuity.

Cloud-based deployment accounted for 68.71% of the microlearning platform market size in 2025, while hybrid deployment is forecast to grow at a 14.13% CAGR through 2031. Cloud remains the leading choice because it offers faster implementation, lower infrastructure costs, easier updates, and better support for distributed workers using multiple devices. Those advantages align well with the day-to-day requirements of the microlearning platform market, where content must reach learners quickly and change frequently. Cloud systems also help vendors release new features faster, which matters in a category that is now adding AI tools, reporting layers, and workflow integrations at a steady pace. For many employers, especially those with dispersed frontline teams, cloud deployment remains the most practical way to scale without adding significant IT overhead.

Hybrid deployment is expanding faster because some sectors want cloud flexibility without placing all learner data and performance records outside local control. Banking, defense, healthcare, and public-sector organizations often need to keep sensitive data in specific environments for residency, audit, or internal policy reasons. Docebo introduced configurable data residency controls across AWS, Azure, and Google Cloud regions in April 2026, which directly addressed those procurement concerns. Supporting hybrid architecture is more demanding for vendors because it requires parallel attention to cloud scalability and controlled data management. That challenge creates a technical barrier that can separate larger providers from smaller players, and it gives the microlearning platform market a clearer split between broad-based enterprise vendors and specialists with narrower deployment capabilities.

Geography Analysis

North America accounted for 38.66% of the global microlearning platform market in 2025, making it the largest regional revenue contributor. The region benefits from high corporate training spend, a deep enterprise software base, and widespread acceptance of digital learning as a normal part of work. Enterprises in the United States continue to anchor demand because they already operate mature LMS environments and have formal learning and development teams that can scale microlearning across large employee populations. Canada and Mexico are adding to regional growth as training systems become more formal in manufacturing and public-sector settings. This keeps the microlearning platform market well-supported in North America through both installed infrastructure and a broad enterprise customer base.

Asia-Pacific is the fastest-growing region in the microlearning platform market and is projected to advance at a 16.21% CAGR through 2031. Growth is being driven by government-backed upskilling programs, mobile-first learner behavior, and the expansion of formal employment structures that can support structured training. Japan's Ministry of Economy, Trade, and Industry released Digital Skill Standard version 1.2 in July 2024, which helped define a national benchmark for digital workforce capabilities. India's National Skill Development Corporation reported by February 2025 that more than 13 million candidates had enrolled through its platform, showing the scale of organized skill development activity in the country. South Korea also supported the expansion of digital learning through KRW 16.9 billion (USD 12.5 million) for AI and digital upskilling in 2025, and KRW 110 billion (USD 80 million) through the AID 30+ workforce reskilling initiative.

Europe remains a mature regional market, with Germany, the United Kingdom, and France accounting for much of the revenue base, and data governance requirements increasingly shape procurement decisions. That makes security credentials, residency controls, and AI compliance more important in vendor selection across the microlearning platform market. The Middle East is emerging as a meaningful growth pocket, especially in Saudi Arabia and the United Arab Emirates, where workforce diversification programs are expanding demand for scalable digital learning. Africa and South America still represent smaller revenue pools, but strong smartphone adoption gives mobile delivery a practical edge in dispersed workforce environments. South Africa, Nigeria, and Kenya in Africa, and Brazil, Argentina, and Colombia in South America, are leading demand in their regions as enterprise digitalization gradually extends into learning technology procurement.

- Axonify Inc.

- Qstream, Inc.

- eduMe Ltd.

- Epignosis LLC

- 7taps OpCo LLC

- Neovation Corporation

- Gnowbe Pte. Ltd.

- MobieTrain Corp.

- Digemy Pty Ltd.

- Bites Learning Ltd.

- Arist Holdings Inc.

- Throwing Boulders, LLC

- LEADx, Inc.

- RapL Inc.

- Handy Training Technologies Private Limited

- 5Mins AI Ltd.

- Uptime App Ltd.

- Fivel Systems Corporation

- iSpring Solutions, Inc.

- Bigtincan Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Need for Continuous Workforce Upskilling and Reskilling

- 4.2.2 Mobile-First Learning Demand Across Deskless and Distributed Workforces

- 4.2.3 Ai-Powered Personalization and Faster Content Authoring

- 4.2.4 Rising Use of Microlearning for Compliance and Risk Management

- 4.2.5 Flow-of-Work Delivery Through Collaboration Apps, Text Messaging, and Quick-Response Code Triggers

- 4.2.6 Ai Translation and Localization for Global Rollouts

- 4.3 Market Restraints

- 4.3.1 Limited Suitability for Deep Conceptual or Procedural Mastery

- 4.3.2 Data Privacy and Cybersecurity Concerns in Cloud and Mobile Delivery

- 4.3.3 Weak Roi Attribution Across Embedded Learning Journeys

- 4.3.4 Notification Fatigue and Content Fragmentation

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform Type

- 5.1.1 Standalone Microlearning Platforms

- 5.1.2 Integrated LMS Platforms

- 5.1.3 AI-Enabled Learning Platforms

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises

- 5.4 By Application

- 5.4.1 Employee Onboarding and New Hire Readiness

- 5.4.2 Compliance Training

- 5.4.3 Sales Enablement and Product Training

- 5.4.4 Workforce Upskilling and Reskilling

- 5.4.5 Leadership and Soft Skills Development

- 5.4.6 Customer and Partner Education

- 5.5 By End User Industry Vertical

- 5.5.1 BFSI

- 5.5.2 IT and Telecom

- 5.5.3 Retail and E-commerce

- 5.5.4 Manufacturing

- 5.5.5 Healthcare and Life Sciences

- 5.5.6 Education

- 5.5.7 Government and Public Sector

- 5.5.8 Media and Entertainment

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Singapore

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Saudi Arabia

- 5.6.4.2 United Arab Emirates

- 5.6.4.3 Turkey

- 5.6.4.4 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Nigeria

- 5.6.5.3 Kenya

- 5.6.5.4 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Colombia

- 5.6.6.4 Chile

- 5.6.6.5 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Axonify Inc.

- 6.4.2 Qstream, Inc.

- 6.4.3 eduMe Ltd.

- 6.4.4 Epignosis LLC

- 6.4.5 7taps OpCo LLC

- 6.4.6 Neovation Corporation

- 6.4.7 Gnowbe Pte. Ltd.

- 6.4.8 MobieTrain Corp.

- 6.4.9 Digemy Pty Ltd.

- 6.4.10 Bites Learning Ltd.

- 6.4.11 Arist Holdings Inc.

- 6.4.12 Throwing Boulders, LLC

- 6.4.13 LEADx, Inc.

- 6.4.14 RapL Inc.

- 6.4.15 Handy Training Technologies Private Limited

- 6.4.16 5Mins AI Ltd.

- 6.4.17 Uptime App Ltd.

- 6.4.18 Fivel Systems Corporation

- 6.4.19 iSpring Solutions, Inc.

- 6.4.20 Bigtincan Holdings Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

微學習市場:2026-2032年全球市場預測(依內容類型、設備類型、技能等級、部署模式、應用、最終用戶和產業分類)

微學習市場:2026-2032年全球市場預測(依內容類型、設備類型、技能等級、部署模式、應用、最終用戶和產業分類) 全球微學習市場

全球微學習市場 微學習平台市場預測至2034年:按組件、內容類型、應用、部署模式、最終用戶和地區分類的全球分析

微學習平台市場預測至2034年:按組件、內容類型、應用、部署模式、最終用戶和地區分類的全球分析 微學習市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、形式、部署類型、最終使用者及模式分類

微學習市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、形式、部署類型、最終使用者及模式分類 微學習市場-全球產業規模、佔有率、趨勢、機會、預測:按組件、組織規模、部署模式、最終用戶、地區和競爭對手分類,2021-2031年

微學習市場-全球產業規模、佔有率、趨勢、機會、預測:按組件、組織規模、部署模式、最終用戶、地區和競爭對手分類,2021-2031年 微學習市場規模、佔有率和成長分析(按組件、組織類型、部署類型、最終用戶產業和地區分類)-2026-2033年產業預測行動優先學習平台市場預測至2032年:按產品、組件、部署模式、應用、最終用戶和地區分類的全球分析

微學習市場規模、佔有率和成長分析(按組件、組織類型、部署類型、最終用戶產業和地區分類)-2026-2033年產業預測行動優先學習平台市場預測至2032年:按產品、組件、部署模式、應用、最終用戶和地區分類的全球分析 全球微學習市場規模按組件、部署類型、組織規模、最終用戶產業、區域範圍和預測分類:

全球微學習市場規模按組件、部署類型、組織規模、最終用戶產業、區域範圍和預測分類: 微學習-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

微學習-市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年) 全球微學習市場(2025-2029)

全球微學習市場(2025-2029)