|

市場調查報告書

商品編碼

2063893

北美撓曲油管服務:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Coiled Tubing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

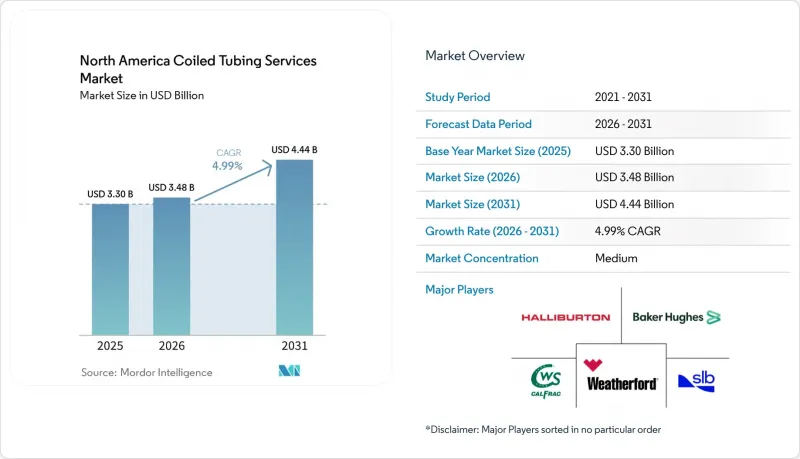

根據 Mordor Intelligence 預測,北美撓曲油管服務市場規模將從 2025 年的 33 億美元成長到 2026 年的 34.8 億美元,到 2031 年將達到 44.4 億美元,2026 年至 2031 年的複合年成長率為 4.99%。

本報告按服務類型(油井清洗和增產、測井鑽井、打撈銑床)、管徑(2英寸以下、2.5-5英寸、5英寸以上)、應用(鑽井、完井、油井干預)、安裝地點(陸上、海上)和地區(美國、加拿大、墨西哥)進行細分。市場預測以美元計價。

北美撓曲油管服務市場趨勢與洞察

用於ESG靶區的電動/混合式CT設備

KLX能源服務公司的Whisper系列電動機組已在二疊紀盆地的專案中減少了40%的柴油消耗,幫助營運商達到加拿大每噸80加元碳價政策下的範圍1減排目標。雖然在偏遠的巴肯油田部署這些機組仍面臨電網接入的限制,但在電力基礎設施完善的井場,預計燃料成本的節省將使投資回報期縮短至18個月以內。

成熟油井中遞減式連續油氣探勘開發的成本優勢

調動一台修井鑽機每天成本高達 15,000 至 25,000 美元,而且通常需要在現場停留一周;而撓曲油管裝置只需四個小時即可完成安裝,每天成本不到 10,000 美元。由於在封裝作業中,連續油管作業可節省 30% 至 50% 的成本,並減少高達 80% 的排放,德克薩斯州、奧克拉荷馬州和亞伯達的運營商正在加速採用這種回流式技術,目前西德克薩斯輕質原油 (WTI) 的價格約為每桶 70 美元。

原油價格波動

2025年,WTI原油均價預計約為每桶65美元,這將給營運商的現金流帶來壓力,並迫使他們削減可自由支配的維修預算。美國能源資訊署(EIA)目前預測2026年油價將達到每桶87美元,但該機構過往的預測修正過程使得決策者仍保持謹慎。許多業者要么簽訂長期契約,要么將重心轉移到地熱或碳捕獲、利用與封存(CCUS)項目上,因為這些項目的盈利能力與原油價格基準無關。

細分市場分析

到2025年,油井清洗和增產作業將佔北美撓曲油管服務市場的47.7%,預計到2031年將以5.3%的複合年成長率成長。在二疊紀盆地的複井平台開發中,採用撓曲油管進行酸循環處理是首選方案,因為它避免了關閉相鄰油井。即時光纖技術使得油井清洗過程中測井(LWC)的整合化成為可能,無需單獨部署有線,從而將作業時間縮短了30%。

雖然測井和射孔的收入規模較小,但隨著作業者現在可以在例行清井作業中取得生產診斷數據,其價值正在不斷提升。在超深水平井中,打撈和銑床仍然是工具堆疊的關鍵環節。 Cudd Energy Services公司31,000英尺長的鑽柱就是一個很好的例子,它展示了服務商如何在風險較高的採油作業中利用鑽井深度和抗張強度。服務配置正向利潤較高的遙測服務轉變,這給僅限於一般清井作業的工作團隊的獲利能力帶來了壓力。

儘管2025年直徑小於2英吋的管柱銷量佔總銷量的39.5%,但預計2-2.5英吋規格的管柱將以5.6%的複合年成長率高速成長,這主要得益於STEP Energy Services公司的UDx作業船隊在Wolfcamp D井推進至35,000英尺的作業深度。較大直徑的管柱能夠達到更高的酸液和丙烷去除流量,同時也能承受更高的崩壞壓力。

直徑大於2.5英吋的油管仍屬於小眾市場,主要用於加拿大蒸氣注入(SAGD)井,以滿足其耐熱性要求。 Copper Tip Energy公司生產的2-6吋油管在3700公尺深處、300°C的高溫環境下運作,充分展現了超大尺寸油管在各種極端環境下的實用價值。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 頁岩氣開發推動了油井干預的蓬勃發展

- 成熟油井中遞減式連續油氣探勘開發的成本優勢

- 自動化和即時數據實施

- 地熱和碳捕集、利用與封存維修需求(未充分報告)

- 用於ESG標靶的電動混合CT掃描儀(缺乏媒體報告)

- 市場限制因素

- 原油價格波動

- 嚴格的健康、安全與環境規章

- 熟練的CT技術人員短缺(報告不足)

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按服務類型

- 良好的清潔和刺激治療

- 測井和鑽井

- 釣魚和火藥

- 按管道直徑

- 2英吋或更小

- 2 至 2.5 英寸

- 2.5吋或更大

- 透過使用

- 挖掘

- 完成

- 井干預

- 按安裝位置

- 土地

- 海

- 按地區

- 美國

- 加拿大

- 墨西哥

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Schlumberger Limited

- Halliburton Company

- Baker Hughes Company

- Weatherford International plc

- National Oilwell Varco Inc.

- Superior Energy Services

- Calfrac Well Services Ltd.

- Trican Well Service Ltd.

- STEP Energy Services

- Key Energy Services LLC

- Essential Energy Services Ltd.

- Conquest Completion Services LLC

- Cudd Energy Services

- Archer Limited

- Nabors Industries Ltd.

- Sanjel Energy Services

- Nine Energy Service

- Pioneer Energy Services

- Welltec A/S

- Peak Well Systems

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america coiled tubing services market size is expected to grow from USD 3.30 billion in 2025 to USD 3.48 billion in 2026 and is forecast to reach USD 4.44 billion by 2031 at 4.99% CAGR over 2026-2031.

This report is Segmented by Service Type (Well Cleaning and Stimulation, Logging and Perforation, Fishing and Milling), Pipe Diameter (Up To 2 In, 2 To 2. 5 In, Above 2. 5 In), Application (Drilling, Completion, Well Intervention), Location of Deployment (Onshore, Offshore), and Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Coiled Tubing Services Market Trends and Insights

Electrified/Hybrid CT Units for ESG Goals

KLX Energy Services' Whisper Series electric unit cut diesel use by 40% on a Permian project, helping operators meet Scope 1 targets under Canada's CAD 80-per-tonne carbon price . While power-grid access still limits deployment in remote Bakken fields, pad sites with electricity infrastructure are seeing sub-18-month paybacks through fuel savings.

Rig-Less CT Cost Advantage for Mature Wells

Mobilizing a workover rig costs USD 15,000-25,000 per day and often requires a week on location, whereas a coiled tubing unit can rig up in four hours at rates below USD 10,000 per day. The 30-50% cost reduction and up to 80% lower emissions in plug-and-abandonment projects encourage operators in Texas, Oklahoma, and Alberta to adopt rig-less techniques when WTI trades near USD 70 per barrel .

Crude-Oil Price Volatility

WTI averaged in the mid-USD 60s during 2025, squeezing operator cash flow and trimming discretionary workover budgets. While EIA now projects USD 87 per barrel for 2026, the agency's forecast revision history keeps decision-makers cautious, leading many to lock in long-term contracts or pivot toward geothermal and CCUS work where revenues decouple from oil benchmarks.

Other drivers and restraints analyzed in the detailed report include:

- Automation & Real-Time Data Adoption

- Geothermal & CCUS Retrofit Demand

- Skilled CT Workforce Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Well cleaning and stimulation accounted for 47.7% of the North America coiled tubing services market size in 2025 and is set for a 5.3% CAGR through 2031. Multi-well pad developments in the Permian favor coiled tubing acid circulations that avoid shutting in adjacent wells. Integrated logging-while-cleaning packages, made possible by real-time fiber optics, eliminate separate wireline mobilizations and cut intervention time by 30%.

Logging and perforation revenues, though smaller, are compounding as operators capture production diagnostics during routine cleanouts. Fishing and milling remain critical for stuck tools in ultra-deep horizontals; Cudd Energy Services' 31,000-foot string exemplifies how providers combine reach with tensile strength for high-risk retrievals. The service mix is pivoting toward higher-margin, telemetry-enabled offerings, squeezing margins for crews restricted to commodity cleanouts.

Strings up to 2 inches held 39.5% of 2025 sales, yet the 2-to-2.5-inch category will clock the fastest 5.6% CAGR as STEP Energy Services' UDx fleet pushes interventions to 35,000 feet in Wolfcamp D wells. Larger diameters deliver greater flow rates for acid and proppant removal while withstanding higher collapse pressures.

Tubing above 2.5 inches remains niche, serving Canadian steam-assisted gravity drainage wells that demand thermal resilience. Copper Tip Energy's 2-⅞-inch strings operate at 3,700 meters in 300 °C service, highlighting the extreme-condition envelope where oversize tubing still plays.

List of Companies Covered in this Report:

- Schlumberger Limited

- Halliburton Company

- Baker Hughes Company

- Weatherford International plc

- National Oilwell Varco Inc.

- Superior Energy Services

- Calfrac Well Services Ltd.

- Trican Well Service Ltd.

- STEP Energy Services

- Key Energy Services LLC

- Essential Energy Services Ltd.

- Conquest Completion Services LLC

- Cudd Energy Services

- Archer Limited

- Nabors Industries Ltd.

- Sanjel Energy Services

- Nine Energy Service

- Pioneer Energy Services

- Welltec A/S

- Peak Well Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shale-driven well-intervention boom

- 4.2.2 Rig-less CT cost advantage for mature wells

- 4.2.3 Automation & real-time data adoption

- 4.2.4 Geothermal & CCUS retrofit demand (under-reported)

- 4.2.5 Electrified/Hybrid CT units for ESG goals (under-reported)

- 4.3 Market Restraints

- 4.3.1 Crude-oil price volatility

- 4.3.2 Stringent HSE regulations

- 4.3.3 Skilled CT workforce shortage (under-reported)

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service Type

- 5.1.1 Well Cleaning and Stimulation

- 5.1.2 Logging and Perforation

- 5.1.3 Fishing and Milling

- 5.2 By Pipe Diameter

- 5.2.1 Up to 2 in

- 5.2.2 2 to 2.5 in

- 5.2.3 Above 2.5 in

- 5.3 By Application

- 5.3.1 Drilling

- 5.3.2 Completion

- 5.3.3 Well Intervention

- 5.4 By Location of Deployment

- 5.4.1 Onshore

- 5.4.2 Offshore

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Schlumberger Limited

- 6.4.2 Halliburton Company

- 6.4.3 Baker Hughes Company

- 6.4.4 Weatherford International plc

- 6.4.5 National Oilwell Varco Inc.

- 6.4.6 Superior Energy Services

- 6.4.7 Calfrac Well Services Ltd.

- 6.4.8 Trican Well Service Ltd.

- 6.4.9 STEP Energy Services

- 6.4.10 Key Energy Services LLC

- 6.4.11 Essential Energy Services Ltd.

- 6.4.12 Conquest Completion Services LLC

- 6.4.13 Cudd Energy Services

- 6.4.14 Archer Limited

- 6.4.15 Nabors Industries Ltd.

- 6.4.16 Sanjel Energy Services

- 6.4.17 Nine Energy Service

- 6.4.18 Pioneer Energy Services

- 6.4.19 Welltec A/S

- 6.4.20 Peak Well Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

連續油管服務市場 - 全球產業規模、佔有率、趨勢、機會、預測:按應用、部署地點、服務介入、地區和競爭格局分類,2021-2031年

連續油管服務市場 - 全球產業規模、佔有率、趨勢、機會、預測:按應用、部署地點、服務介入、地區和競爭格局分類,2021-2031年 撓曲油管市場:類型、材質、應用和最終用途 - 2026-2032年全球市場預測

撓曲油管市場:類型、材質、應用和最終用途 - 2026-2032年全球市場預測 2026年全球撓曲油管服務市場報告

2026年全球撓曲油管服務市場報告 撓曲油管市場:依產品和地區分類2026年全球盤管市場報告

撓曲油管市場:依產品和地區分類2026年全球盤管市場報告 撓曲油管市場規模、佔有率和趨勢分析報告:按服務、營運、應用、地區和細分市場預測(2026-2033 年)連續油管市場-全球產業規模、佔有率、趨勢、機會、預測:按服務類型、應用、地區和競爭格局分類,2021-2031年

撓曲油管市場規模、佔有率和趨勢分析報告:按服務、營運、應用、地區和細分市場預測(2026-2033 年)連續油管市場-全球產業規模、佔有率、趨勢、機會、預測:按服務類型、應用、地區和競爭格局分類,2021-2031年 全球撓曲油管服務市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考察、未來預測(2026-2034)

全球撓曲油管服務市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考察、未來預測(2026-2034) 撓曲油管市場規模、佔有率和成長分析(按服務、應用、船隊和地區分類)-2026-2033年產業預測

撓曲油管市場規模、佔有率和成長分析(按服務、應用、船隊和地區分類)-2026-2033年產業預測 連續油管鑽井服務市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)

連續油管鑽井服務市場機會、成長促進因素、產業趨勢分析及預測(2025-2034年)