|

市場調查報告書

商品編碼

2063817

Wi-Fi 6E 路由器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Wi-fi 6E Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

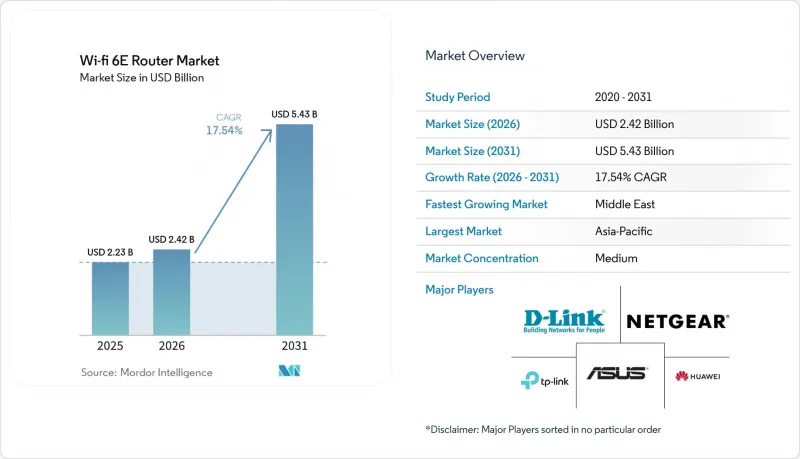

據 Mordor Intelligence 稱,2025 年 Wi-Fi 6E 路由器市值為 22.3 億美元,預計到 2031 年將從 2026 年的 24.2 億美元成長至 54.3 億美元,在預測期(2026-2031 年)內的複合成長率為 17.54%。

本報告頻寬(三頻、雙頻、四頻以上)、產品類型(消費級、企業級、運營商級和ISP閘道器)、最終用戶(住宅、中小企業、企業和園區、公共熱點和智慧城市)、銷售管道(線上零售、實體店、經銷商、OEM直銷)和地區(北美等)進行細分。市場預測以美元計價。

全球Wi-Fi 6E路由器市場趨勢與洞察

Gigabit寬頻用戶激增

到2025年,光纖到府(FTTH)的普及率將突破關鍵閾值。隨著北美、歐洲和亞太地區的通訊業者部署對稱的多Gigabit服務,老舊的Wi-Fi 5路由器正成為瓶頸。預計2025年Wi-Fi 6E設備的出貨量將達到6.269億台,顯示市場需求強勁,消費者正在升級到能夠支援Gigabit連接的硬體。從策略角度來看,關鍵的轉變在於網路服務供應商(ISP)的經營模式。營運商不再將路由器視為普通的家庭設備,而是透過將高階Wi-Fi 6E閘道器與光纖解約率捆綁,來區分不同的服務等級並降低通訊業者流失率。這形成了一個良性循環:更高的寬頻速度促使用戶升級路由器,從而增加附加價值服務(例如家長監護功能和網路安全訂閱)的收入。這對供應商的影響顯而易見。與一級網際網路服務提供商合作可以保證銷量,但除非你通過軟體定義網路 (SDN) 功能脫穎而出,使運營商能夠遠端最佳化性能和排除故障而無需現場訪問,否則利潤率將會受到擠壓。

企業向混合辦公模式轉型

混合辦公模式已成為知識型員工的標準工作模式,迫使企業以以往僅應用於企業園區的同等嚴謹標準來建構在家工作環境的連結性。報告顯示,2025年Wi-Fi 6E網路基地台的出貨量將達到8,160萬個,顯示分散式辦公團隊對低延遲視訊會議和安全VPN隧道的需求強勁。第二個洞見是企業採購趨勢的兩極化。大型企業傾向於採用集中式管理主機的運營商級路由器,而中小企業則傾向於選擇價格親民、卻能提供企業級安全性的消費級硬體。這種兩極化為能夠彌合市場差距的供應商創造了商機,他們可以透過提供具有零接觸配置和基於角色的存取控制的雲端管理平台,同時保持具有競爭力的價格,從而贏得中小企業的訂單。諸如GDPR和新的資料本地化義務等法律規範進一步增加了對內建加密和審計日誌功能的路由器的需求,尤其是在歐洲和亞太市場,因為這些市場對違規的處罰非常嚴厲。

高階晶片組的供應鏈限制

Wi-Fi 6E 路由器依賴少數幾個關鍵供應商(例如博通、高通和聯發科)提供的先進半導體,而這些供應商的生產計劃易受台積電產能限制和東亞地緣政治局勢的影響。分析預測,連接積體電路 (IC) 的複合年成長率將達到 11.6%,但這一成長速度將無法跟上資料中心和汽車對半導體的需求,這意味著 WLAN 市場的供應可能會因晶圓代工廠能分配決策而週期性地受到限制。一個策略風險是,晶片組短缺將擠壓供應商的利潤空間。路由器製造商被迫在接受更長的前置作業時間並冒著市場佔有率被擁有更強供應合約的競爭對手蠶食的風險,或者支付現貨市場價格之間做出選擇。

細分市場分析

到2025年,三頻設備將佔據WiFi 6E路由器市場46.78%的佔有率,成為網狀回程傳輸的首選,其價格也為大多數家庭所接受。在人口密集的都市區公寓中,單一三頻節點即可完全佔用Gigabit光纖線路,因此額外投資購買無線模組的成本並不高。四頻以上型號預計將以18.43%的複合年成長率成長,因為企業、遊戲玩家和內容創作者重視兩個獨立的6 GHz或5 GHz頻段無線電所提供的冗餘性。在印度等僅授權使用較低頻段6 GHz的市場,四頻硬體的實際優勢較為有限,導致其普及速度放緩,但需求不會消失。

強大的設備支援也至關重要。隨著智慧型手機和筆記型電腦擴大採用多無線晶片組,擁有超過 10 個活躍用戶端的家庭開始意識到使用額外的 6 GHz 頻道進行負載平衡的優勢。三頻路由器簡化了零售商和網路服務供應商的庫存管理,而四頻型號則吸引了那些尋求面向未來的 AR、VR 和 8K 串流媒體容量的電力用戶。因此,廠商們正在維護並行的產品線,將三頻型號的價格定位在適合大規模升級週期的水平,並將四頻型號定位為高階產品,以確保即使數十個客戶端同時連接也能保持性能。這種兩極化的策略擴大了 WiFi 6E 路由器市場,提升了入門級和高階市場的規模,並幫助製造商在晶片成本下降的情況下維持利潤率。這種方法還可以透過調整三頻和四頻型號之間的晶片組分配,以符合區域頻率政策,從而降低供應鏈風險。在預測期內,隨著頻段自由化的推進,市場佔有率預計將逐漸向四頻段轉移,但三頻段預計將在 2031 年之前保持其銷售領先地位。

預計到2025年,消費級硬體將佔總銷售額的54.32%,這主要得益於蓬勃發展的電子商務市場以及WiFi 5用戶強勁的更換需求。然而,營運商級閘道器是成長最快的細分市場,複合年成長率高達17.98%,因為通訊業者將WiFi 6E捆綁銷售,以凸顯其多千兆服務的差異化優勢。企業級路由器繼續面向園區市場銷售,但其較長的更新周期限制了短期成長。

與營運商閘道器相關的軟體收入,包括家長監控、安全增強和遠端診斷等功能,正將利潤來源從一次性硬體銷售轉向多年服務合約。能夠確保網路服務供應商 (ISP) 採用其設計方案的供應商,實際上就等於確保了銷量,這不僅支撐了 WiFi 6E 路由器市場的成長,還能透過退休金等多種收入來源來抵消硬體利潤率的下降。

區域分析

受中國、印度和東南亞光纖到府(FTTH)擴張的推動,亞太地區預計到2025年將佔全球銷售額的37.44%。在印度,6GHz低頻段的頻譜許可證將於2026年1月放開,這將開啟一個龐大的住宅和校園市場。同時,中國正利用國內ODM基礎設施,向國內市場和「一帶一路」沿線市場提供價格極具競爭力的硬體。區域風險包括可能擾亂供應鏈和認證體系的貿易摩擦。

北美市場仍然主要由升級需求驅動,但受益於美國聯邦通訊委員會 (FCC) 於 2026 年批准的 Wi-Fi 6E 標準功率。這將使市政 Wi-Fi 和體育場館的室外 Wi-Fi 6E 成為可能,從而擴大其適用範圍。然而,在歐洲,關於與衛星共存的討論正在減緩其普及速度。英國通訊管理局 (Ofcom) 正在進行的談判意味著,6GHz 高頻段的使用在 2027 年之前仍存在不確定性,這迫使供應商提供多種 SKU,並減緩了公共部門的部署速度。

預計中東地區將以20.11%的複合年成長率成長,這主要得益於沙烏地阿拉伯和阿拉伯聯合大公國的「2030願景」計劃,該計劃強調智慧城市互聯互通。儘管南美和非洲的寬頻普及率落後於中東,但主要城市對中價位的三頻路由器的需求已初見端倪。針對不同經濟環境,制定區域性產品線,例如針對海灣國家的高階營運商閘道器和麵向南美的成本績效經濟狀況三頻路由器套裝,將有助於最佳化Wi-Fi 6E路由器的市場滲透率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- Gigabit寬頻用戶數量正在迅速成長。

- 企業向混合辦公模式轉型

- Wi-Fi 6E認證終端設備的快速成長

- 監管機構對 6 GHz 頻段的放鬆管制

- 物聯網中節能目標喚醒時間(TWT)的引入

- 擴展對 WPA3 安全標準的支持

- 市場限制因素

- 高階晶片組的供應鏈限制

- 與Wi-Fi 5路由器相比,平均售價更高

- 對 6 GHz 頻段固定衛星業務的干擾

- 主要已開發國家以外的消費者意識較低

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按樂隊

- 三頻(2.4 GHz、5 GHz、6 GHz)

- 雙頻(2.4 GHz 和 6 GHz)

- 四頻或更高

- 依產品類型

- 消費級路由器

- 企業級路由器

- 營運商級和ISP閘道器

- 最終用戶

- 住宅

- 小型企業

- 大型企業和校園

- 公共熱點與智慧城市

- 按銷售管道

- 線上零售

- 量販店

- 增值轉售商

- 直接OEM/ODM銷售

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ASUSTeK Computer Inc.

- TP-Link Technologies Co., Ltd.

- Netgear, Inc.

- D-Link Corporation

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- Linksys Holdings, Inc.

- Zyxel Communications Corporation

- Ubiquiti Inc.

- EnGenius Technologies, Inc.

- Cambium Networks Corporation

- MikroTikls SIA

- Edimax Technology Co., Ltd.

- Buffalo Inc.

- Cisco Systems, Inc.

- CommScope Holding Company, Inc.(ARRIS)

- Actiontec Electronics, Inc.

- Comtrend Corporation

- NetComm Wireless Pty Ltd.

- Juniper Networks, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the wi-Fi 6E router market size was valued at USD 2.23 billion in 2025 and estimated to grow from USD 2.42 billion in 2026 to reach USD 5.43 billion by 2031, at a CAGR of 17.54% during the forecast period (2026-2031).

This report is Segmented by Band (Tri-Band, Dual-Band, and Quad-Band and Above), Product Type (Consumer, Enterprise, and Carrier-Grade and Isp Gateways), End User (Residential, SMB, Enterprise and Campuses, and Public Hotspots and Smart Cities), Sales Channel (Online Retail, Stores, Resellers, and Direct OEM), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Wi-fi 6E Router Market Trends and Insights

Explosion Of Gigabit Broadband Subscriptions

Fiber-to-the-home penetration crossed critical thresholds in 2025, with operators in North America, Europe, and Asia-Pacific deploying symmetrical multi-gigabit services that render legacy Wi-Fi 5 routers a bottleneck. The projection of 626.9 million Wi-Fi 6E devices shipped in 2025 underscores the demand-side pull as consumers upgrade to hardware capable of saturating gigabit links. What matters strategically is the shift in ISP business models: rather than treating routers as commoditized customer-premises equipment, telcos now bundle premium Wi-Fi 6E gateways with fiber subscriptions to differentiate service tiers and reduce churn. This creates a flywheel effect: higher broadband speeds justify router upgrades, which in turn drive incremental revenue from value-added services such as parental controls and network security subscriptions. The implication for vendors is clear: partnerships with tier-1 ISPs unlock predictable volume, but also compress margins unless differentiated through software-defined networking features that enable operators to remotely optimize performance and troubleshoot issues without truck rolls.

Enterprise Migration Toward Hybrid Work Models

Hybrid work arrangements have entrenched themselves as the default operating model for knowledge workers, compelling enterprises to architect home-office connectivity with the same rigor previously reserved for corporate campuses. The reported 81.6 million Wi-Fi 6E access points shipped in 2025 indicate strong demand from distributed workforces requiring low-latency video conferencing and secure VPN tunneling. The second-order insight involves the bifurcation of enterprise procurement: large corporations are standardizing on carrier-grade routers with centralized management consoles, while small and medium-sized businesses are gravitating toward consumer-grade hardware that offers enterprise-class security at prosumer price points. This bifurcation creates whitespace for vendors that can bridge the gap by offering cloud-managed platforms with zero-touch provisioning and role-based access controls, yet priced competitively enough to win SMB deals. Regulatory frameworks such as GDPR and emerging data-localization mandates further amplify demand for routers with built-in encryption and audit-logging capabilities, particularly in Europe and Asia-Pacific markets where compliance penalties are material.

Supply Chain Constraints of High-end Chipsets

Wi-Fi 6E routers depend on advanced silicon from a concentrated supplier base, Broadcom, Qualcomm, and MediaTek, whose production schedules remain vulnerable to capacity constraints at Taiwan Semiconductor Manufacturing Company and geopolitical tensions in East Asia. Analysis indicates that connectivity integrated circuits are forecast to grow at an 11.6% CAGR, yet this growth lags data-center and automotive semiconductor demand, suggesting that foundry allocation decisions could periodically constrain supply to the WLAN market. The strategic risk is that chipset shortages compress vendor margins. Router manufacturers must either accept longer lead times, thereby risking market-share loss to competitors with stronger supply agreements, or pay spot-market prices.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Growth of Wi-Fi 6E Certified End-Devices

- Spectrum Liberalisation in 6 GHz Band by Regulators

- High Average Selling Price Versus Wi-Fi 5 Routers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tri-band devices held 46.78% WiFi 6E router market share in 2025, validating their position as the default choice for mesh backhaul at a price point most households accept. In dense urban apartments, one tri-band node can fully saturate a gigabit fiber link, so incremental spending on additional radios brings little extra benefit. Quad-band and above models are forecast to expand at an 18.43% CAGR because enterprises, gamers, and content creators value the redundancy that two independent 6 GHz or 5 GHz radios provide. Markets that authorize only the lower 6 GHz block, such as India, narrow the real-world advantage of quad-band hardware, slowing adoption but not eliminating demand.

Strong device support also matters: as smartphones and laptops ship with multi-radio chipsets, households with ten or more active clients begin to notice the load-balancing advantage of an extra 6 GHz channel. Tri-band routers simplify inventory for retailers and ISPs, while quad-band units appeal to power users seeking future-proof capacity for AR, VR, and 8K streaming. Vendors, therefore, keep parallel SKU lines, price tri-band for mass upgrade cycles, and position quad-band as a premium tier that safeguards performance when dozens of clients connect simultaneously. This bifurcated strategy expands the WiFi 6E router market, boosting market size across both value and high-end price bands, helping manufacturers defend margins even as silicon costs fall. The approach also cushions supply-chain risk because chipset allocations can be shifted between tri- and quad-band models to match regional spectrum policies. Over the forecast window, continued spectrum liberalization will gradually tilt share toward quad-band, but tri-band is expected to remain the volume leader through 2031.

Consumer hardware accounted for 54.32% of 2025 revenue, driven by thriving e-commerce and a large base of WiFi 5 replacements. Carrier-grade gateways, however, are the fastest-growing slice at a 17.98% CAGR, as telcos bundle WiFi 6E to differentiate multi-gig services. Enterprise-class routers continue to serve campuses but face longer refresh cycles that temper near-term growth.

Recurring software revenues attached to carrier gateways, including parental controls, security overlays, and remote diagnostics, shift profit pools from one-time hardware sales to multi-year service contracts. Vendors that secure ISP design wins effectively lock in volume, underpinning the trajectory of the WiFi 6E router market while balancing thinner hardware margins with annuity income streams.

Geography Analysis

Asia-Pacific commanded 37.44% revenue in 2025, propelled by fiber-to-the-home expansion in China, India, and Southeast Asia. India's January 2026 de-licensing of the lower 6 GHz band unlocks a vast residential and campus market, while China leverages its ODM base to deliver competitively priced hardware for domestic and Belt-and-Road destinations. Regional risk lies in potential trade friction that may split supply chains and certification regimes.

North America remains a replacement market but benefits from the FCC's 2026 standard-power approval, which enables outdoor WiFi 6E for municipal WiFi and stadiums, broadening the addressable use cases. Satellite coexistence debates temper Europe's adoption; Ofcom's ongoing consultation keeps upper-6 GHz clarity in limbo through 2027, compelling vendors to ship multiple SKUs and slowing public-sector rollouts.

The Middle East, forecast to grow at 20.11% CAGR, leverages Vision 2030 agendas in Saudi Arabia and the United Arab Emirates that mandate smart-city connectivity. South America and Africa trail in broadband penetration, yet tier-1 cities show early demand for mid-priced tri-band models. Tailored regional portfolios, premium carrier gateways in the Gulf, value tri-band kits in South America, optimize the WiFi 6E router market penetration across diverse economic profiles.

- ASUSTeK Computer Inc.

- TP-Link Technologies Co., Ltd.

- Netgear, Inc.

- D-Link Corporation

- Huawei Technologies Co., Ltd.

- Xiaomi Corporation

- Linksys Holdings, Inc.

- Zyxel Communications Corporation

- Ubiquiti Inc.

- EnGenius Technologies, Inc.

- Cambium Networks Corporation

- MikroTikls SIA

- Edimax Technology Co., Ltd.

- Buffalo Inc.

- Cisco Systems, Inc.

- CommScope Holding Company, Inc. (ARRIS)

- Actiontec Electronics, Inc.

- Comtrend Corporation

- NetComm Wireless Pty Ltd.

- Juniper Networks, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosion of Gigabit Broadband Subscriptions

- 4.2.2 Enterprise Migration Toward Hybrid Work Models

- 4.2.3 Rapid Growth of Wi-Fi 6E Certified End-Devices

- 4.2.4 Spectrum Liberalisation in 6 GHz Band by Regulators

- 4.2.5 Energy-Efficient Target Wake Time (TWT) Adoption in IoT

- 4.2.6 Increasing Support for WPA3 Security Standard

- 4.3 Market Restraints

- 4.3.1 Supply Chain Constraints of High-end Chipsets

- 4.3.2 High Average Selling Price Versus Wi-Fi 5 Routers

- 4.3.3 Interference with Fixed Satellite Services in 6 GHz

- 4.3.4 Limited Consumer Awareness Outside Tier-1 Economies

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Comptetive Rivalary

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Band

- 5.1.1 Tri-Band (2.4 GHz, 5 GHz, 6 GHz)

- 5.1.2 Dual-Band (2.4 GHz and 6 GHz)

- 5.1.3 Quad-Band and Above

- 5.2 By Product Type

- 5.2.1 Consumer-Grade Routers

- 5.2.2 Enterprise-Class Routers

- 5.2.3 Carrier-Grade and ISP Gateways

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Small and Medium-Sized Businesses

- 5.3.3 Large Enterprises and Campuses

- 5.3.4 Public Hotspots and Smart Cities

- 5.4 By Sales Channel

- 5.4.1 Online Retail

- 5.4.2 Consumer Electronics Stores

- 5.4.3 Value-Added Resellers

- 5.4.4 Direct OEM / ODM Sales

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ASUSTeK Computer Inc.

- 6.4.2 TP-Link Technologies Co., Ltd.

- 6.4.3 Netgear, Inc.

- 6.4.4 D-Link Corporation

- 6.4.5 Huawei Technologies Co., Ltd.

- 6.4.6 Xiaomi Corporation

- 6.4.7 Linksys Holdings, Inc.

- 6.4.8 Zyxel Communications Corporation

- 6.4.9 Ubiquiti Inc.

- 6.4.10 EnGenius Technologies, Inc.

- 6.4.11 Cambium Networks Corporation

- 6.4.12 MikroTikls SIA

- 6.4.13 Edimax Technology Co., Ltd.

- 6.4.14 Buffalo Inc.

- 6.4.15 Cisco Systems, Inc.

- 6.4.16 CommScope Holding Company, Inc. (ARRIS)

- 6.4.17 Actiontec Electronics, Inc.

- 6.4.18 Comtrend Corporation

- 6.4.19 NetComm Wireless Pty Ltd.

- 6.4.20 Juniper Networks, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Wi-Fi 6 市場 – 2026-2032 年全球市場預測

Wi-Fi 6 市場 – 2026-2032 年全球市場預測 Wi-Fi 6 路由器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

Wi-Fi 6 路由器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) Wi-Fi 6 技術市場:按組件、最終用戶、行業和地區分類

Wi-Fi 6 技術市場:按組件、最終用戶、行業和地區分類 全球Wi-Fi 6路由器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球Wi-Fi 6路由器市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026 年全球 Wi-Fi 6E 設備市場報告2026年Wi-Fi 6全球市場報告

2026 年全球 Wi-Fi 6E 設備市場報告2026年Wi-Fi 6全球市場報告 Wi-Fi 6 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類

Wi-Fi 6 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類 Wi-Fi 6 市場規模、佔有率和成長分析(按產品、類型、應用、垂直產業和地區分類)—2026-2033 年產業預測

Wi-Fi 6 市場規模、佔有率和成長分析(按產品、類型、應用、垂直產業和地區分類)—2026-2033 年產業預測 Wi-Fi 6 設備市場規模、佔有率和成長分析(按交付類型、地點類型、應用、垂直產業和地區分類)—產業預測(2026-2033 年)

Wi-Fi 6 設備市場規模、佔有率和成長分析(按交付類型、地點類型、應用、垂直產業和地區分類)—產業預測(2026-2033 年) Wi-Fi 6市場:產業趨勢·全球預測 (~2035年):提供類型·定位·用途·終端用戶產業·各地區

Wi-Fi 6市場:產業趨勢·全球預測 (~2035年):提供類型·定位·用途·終端用戶產業·各地區