|

市場調查報告書

商品編碼

2063765

Wi-Fi 6 路由器:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Wi-Fi 6 Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

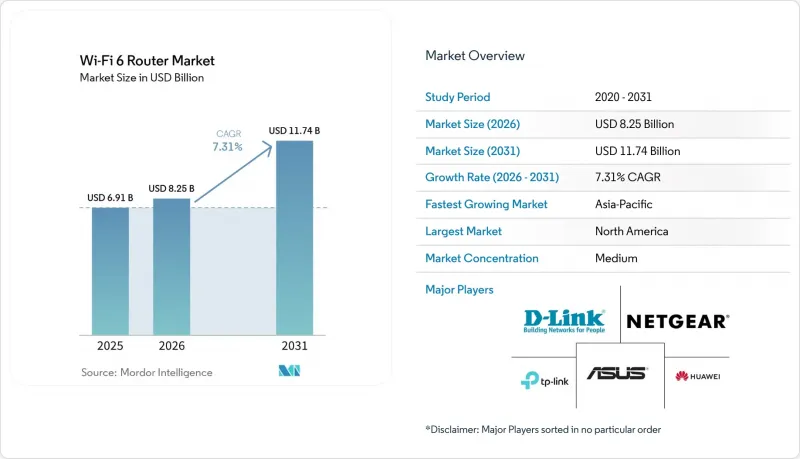

據 Mordor Intelligence 稱,2025 年 Wi-Fi 6 路由器市值為 69.1 億美元,預計到 2031 年將達到 117.4 億美元,而 2026 年為 82.5 億美元,預測期(2026-2031 年)的複合成長率為 7.31%。

本報告按產品類型(雙頻路由器、三頻路由器、四頻路由器)、頻段(2.4 GHz、5 GHz、6 GHz)、最終用戶(住宅、商業、工業)、分銷管道(網路商店、線下零售、B2B 直接採購)和地區進行細分。市場預測以美元計價。

全球Wi-Fi 6路由器市場趨勢與洞察

寬頻升級至Gigabit級服務激增

根據英國通訊管理局(Ofcom)預測,到2025年,英國家庭光纖普及率將達到89.58%,這將加速營運商主導的、老舊VDSL閘道(吞吐量低於Gigabit)的更換進程。 Charter 通訊業者正透過計劃在2024年下半年向美國120萬用戶部署多Gigabit閘道器來推動這一轉型,這表明,老牌有線電視運營商正憑藉下一代Wi-Fi硬體,在光纖競爭中保持領先地位。捆綁式租賃定價模式將路由器升級納入服務費用,從而免除了前期成本並縮短了更換週期。同時,提供DOCSIS和Wi-Fi整合平台的供應商透過簽訂多年供貨契約,對市場需求有了更清晰的了解。隨著對稱千兆Gigabit計畫在歐洲和東亞的擴展,Wi-Fi 6路由器市場正獲得持續的銷售量成長和價格優勢。

2025 年頻率重新分配後,網路服務供應商必須遷移到 Wi-Fi 6 閘道。

2026年1月,美國聯邦通訊委員會(FCC)決定開放6GHz頻譜中的1,200MHz頻寬,迫使通訊業者逐步淘汰無法利用這些頻段的Wi-Fi 5硬體。同時,歐洲電訊標準協會(ETSI)協調了低頻寬法規,使供應商能夠在歐盟主要市場實現三頻平台的標準化。儘管通訊業者在2026年的財務報表中累計了過時庫存的短期減損損失,但他們預計,借助6GHz回程傳輸支援的高速套餐,用戶平均收入(ARPU)將有所提高。印度和韓國類似的監管措施已將產品開發週期縮短至12-18個月,從而加快了晶片組供應商的獲利速度。

Wi-Fi 6E 三頻機型的高階價格區間超過 400 美元。

NETGEAR 的 Orbi 870 三件裝售價 1499.99 美元,與售價低於 200 美元的雙頻系統相比,價格差異顯著。同時,TP-Link 將其中端三頻型號的定價在 333.99 美元左右,通常只有寬頻速度超過 500 Mbps 時,這個價位才算合理。組件成本的上漲反映了額外的射頻鏈路、更大的散熱組件以及覆蓋 2.4GHz、5GHz 和 6GHz 頻段的更複雜的頻段控制韌體。雖然預計到 2027 年底,晶片組的整合將使入門級三頻產品的價格降至 250 美元以下,但目前的高價正在抑制價格敏感型市場(尤其是新興市場)的銷售。

細分市場分析

預計到2031年,三頻硬體將以9.62%的複合年成長率成長,這主要得益於企業願意為專用的6GHz回程傳輸付費,該鏈路能夠將網狀網路流量與客戶端資料流分離,從而提高吞吐量的確定性。Cisco在2026會計年度財報中指出,園區設備升級勢頭強勁,混合辦公環境需要無縫漫遊和穩定的影像質量,這是推動三頻硬體發展的主要因素。儘管如此,雙頻產品在2025年仍保持40.43%的市場佔有率,因為住宅優先考慮網路覆蓋範圍,並將6GHz頻段的採用推遲到Gigabit光纖線路更加普及之後。四頻設備仍然是小眾產品,由於生態系統支援有限,主要局限於遊戲應用場景。

廠商在Wi-Fi 8的研發方面進展迅速,華碩電腦股份有限公司發表了一款符合IEEE 802.11bn草案標準的路由器原型,其峰值速度接近30Gbps。然而,不同地區的偏好仍有差異。北美家庭更傾向於選擇捆綁了訂閱式安全功能的整合設備,而歐洲消費者則傾向於選擇將路由和無線功能分開的模組化系統,以應對結構性干擾的限制。 Wi-Fi聯盟對自動頻率調節的認證,透過確保6GHz頻段內的共存性,並支援三頻架構的持續普及,增強了消費者的信心。

到2031年,6 GHz頻段市場將以9.83%的複合年成長率成長,超過2025年市佔率47.32%的5 GHz頻段。美國聯邦通訊委員會(FCC)透過開放從5.925 GHz到6.875 GHz的連續1200 MHz頻寬,促進了這一轉變,從而創建了七個無干擾的160 MHz頻道,能夠維持多Gigabit的吞吐量。美國通訊部於2024年12月取消了500 MHz頻段的許可,增強了全球經濟活力,並使供應商能夠在關鍵市場實現設計標準化。自動頻率調節架構進一步擴展了6 GHz頻段的應用範圍,使其能夠涵蓋物流場和企業園區等戶外環境,而不會干擾現有的微波系統。

Wi-Fi 6 路由器市場仍依賴 2.4 GHz 頻段來滿足低功耗、遠距離物聯網應用的需求,但其 600 Mbps 的吞吐量限制了需要更高頻寬的應用場景。 5 GHz 頻段雖然會受到雷達探測動態頻率選擇的影響,但它在容量和滲透性牆能力之間取得了平衡,仍然是人口密集住宅環境的實用中間頻寬。相較之下,6 GHz 頻段擴大用於對延遲敏感的企業和工業工作負載,這些工作負載要求抖動保持在 3 毫秒以下以支援確定性網路。這種頻段分類凸顯了清晰的功能層級,每個頻寬都針對不同的效能和部署需求進行了最佳化。

區域分析

預計到2025年,北美將佔全球整體收入的35.43%,這主要得益於有線電視營運商租賃閘道器以應對光纖基礎設施擴張帶來的競爭。這種模式正在將Wi-Fi 6路由器的市場准入從零售轉向通訊業者通路,從而維持較高的平均售價和更短的升級週期。 Charter Communications和Comcast Corporation等公司正是這種模式的典範,他們將先進的閘道器與包含早期Wi-Fi 7部署的服務套餐捆綁銷售,以留住高價值用戶。此外,該地區較高的寬頻普及率和用戶對高效能方案的付費意願正在推動高階市場的成長,加速了下一代標準的普及,領先世界其他地區。

亞太地區預計將在2026年至2031年間以12.43%的複合年成長率實現最高成長,這主要得益於監管協調和成本效益高的製造生態系統。通訊部已對6GHz頻段進行了淘汰,使其頻率政策與美國和歐洲保持一致,並降低了供應商的合規難度。中國製造商,尤其是深圳的製造商,主導著售價低於50美元的雙頻產品的出口,而台灣和韓國的供應商則專注於利潤更高的三頻系統。同時,由於印尼和越南政府主導的光纖網路部署,寬頻存取不斷擴大,路由器出貨量也在成長,但價格敏感度正在減緩單位收入的成長。

南美洲和非洲是新興成長地區,公共資金正將互聯互通的願景轉化為具體的基礎建設項目。 ANATEL已投資32億雷亞爾(約6.4億美元)用於改善農村地區的網路連結。此外,由非洲開發銀行支持的奈及利亞「橋樑計畫」以及由南部非洲開發銀行主導的南非寬頻擴建計畫等舉措,都在擴大「最後一公里」的接入範圍。雖然絕對利潤仍低於成熟市場,但這兩位數的出貨量成長正促使供應商優先考慮能夠適應各種環境條件的堅固耐用、耐高溫的設計。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 寬頻升級至Gigabit級服務激增

- 2025 年頻率重新分配後,網路服務供應商必須遷移到 Wi-Fi 6 閘道。

- 智慧家庭物聯網節點密度爆炸性成長

- 政府主導的南美洲和非洲農村光纖網路部署

- 混合辦公政策下的企業網路更新周期

- 6 GHz 頻段獲得監管部門批准,Wi-Fi 6E 的全部潛力得以釋放。

- 市場限制因素

- Wi-Fi 6E 三頻型號的定價較高,超過 400 美元。

- 6 GHz 頻段法規的分散化導致支援多個 SKU 需要付出合規成本。

- 主要晶片組半導體的前置作業時間超過 30 週。

- 消費者對標準福利的了解有限,阻礙了廣泛普及。

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 雙頻路由器

- 三頻路由器

- 四頻路由器

- 按頻段

- 2.4 GHz

- 5 GHz

- 6 GHz(Wi-Fi 6E)

- 最終用戶

- 住宅

- 商業

- 產業

- 透過分銷管道

- 網路商店

- 線下零售

- 企業直接採購

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- TP-Link Technologies Co., Ltd.

- NETGEAR, Inc.

- ASUSTeK Computer Inc.

- D-Link Corporation

- Huawei Technologies Co., Ltd.

- Belkin International, Inc.

- Cisco Systems, Inc.

- Xiaomi Corporation

- Ubiquiti Inc.

- Zyxel Communications Corporation

- MikroTikls SIA

- Shenzhen Tenda Technology Co., Ltd.

- Shenzhen Mercury Communication Technologies Co., Ltd.

- Zioncom Holdings Limited(TOTOLINK)

- Edimax Technology Co., Ltd.

- TRENDnet, Inc.

- GL Technologies Inc.

- Buffalo Inc.

- AVM Computersysteme Vertriebs GmbH

- DrayTek Corp.

- Synology Inc.

- Cambium Networks Corporation

- Ruijie Networks Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the wi-Fi 6 router market size was valued at USD 6.91 billion in 2025 and is estimated to grow from USD 8.25 billion in 2026 to reach USD 11.74 billion by 2031, at a CAGR of 7.31% during the forecast period (2026-2031).

This report is Segmented by Product Type (Dual-Band Routers, Tri-Band Routers, and Quad-Band Routers), Frequency Band (2. 4 GHz, 5 GHz, and 6 GHz), End User (Residential, Commercial, and Industrial), Distribution Channel (Online Stores, Offline Retail, and Direct Enterprise Procurement), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Wi-Fi 6 Router Market Trends and Insights

Surging Broadband Upgrades To Gigabit-Class Service

Fiber penetration reached 89.58% of United Kingdom premises in 2025, according to Ofcom, accelerating operator-led replacement of legacy VDSL gateways that constrain throughput below gigabit levels. Charter Communications reinforced this shift by deploying multi-gigabit gateways to 1.2 million United States subscribers in late 2024, indicating cable incumbents are pre-empting fiber competition with next-generation Wi-Fi hardware. Bundled lease pricing embeds router upgrades within service fees, eliminating upfront costs and compressing replacement cycles. Concurrently, vendors delivering integrated DOCSIS and Wi-Fi platforms lock in multi-year supply contracts, improving demand visibility. As symmetrical gigabit plans expand across Europe and East Asia, the Wi-Fi 6 router market gains sustained volume momentum and pricing resilience.

Mandatory Transition Of ISPs To Wi-Fi 6 Gateways After 2025 Spectrum Re-allocation

The January 2026 decision by the Federal Communications Commission to release the full 1,200 MHz of 6 GHz spectrum forces operators to phase out Wi-Fi 5 hardware that cannot utilize these channels. In parallel, the European Telecommunications Standards Institute aligned lower-band rules, enabling vendors to standardize tri-band platforms across major EU markets. Operators are absorbing near-term write-offs on legacy inventory in 2026 financials but expect higher ARPU from premium speed tiers supported by 6 GHz backhaul. Similar regulatory actions in India and South Korea are compressing product-development cycles to 12-18 months, accelerating revenue conversion for chipset vendors.

Premium Pricing Of Wi-Fi 6E Tri-Band Models Above USD 400

NETGEAR's Orbi 870 three-pack launched at USD 1,499.99, highlighting a substantial price delta versus sub-USD 200 dual-band systems, while TP-Link positions mid-tier tri-band units around USD 333.99, a threshold typically justified only when broadband speeds exceed 500 Mbps. The elevated bill of materials reflects an additional RF chain, larger thermal assemblies, and more complex band-steering firmware spanning 2.4, 5, and 6 GHz. Although ongoing chipset integration is expected to compress entry-level tri-band pricing below USD 250 by late 2027, the current premium suppresses unit volumes in price-sensitive markets, particularly across emerging economies.

Other drivers and restraints analyzed in the detailed report include:

- Explosive Growth Of Smart-Home IoT Node Density

- Government-Backed Rural Fiber Roll-outs In South America And Africa

- Fragmented 6 GHz Rules Forcing Multi-SKU Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tri-band hardware is projected to expand at a 9.62% CAGR through 2031, driven by enterprise willingness to pay for dedicated 6 GHz backhaul that segregates mesh traffic from client streams and improves throughput determinism. Cisco Systems referenced campus-refresh momentum in its FY 2026 earnings, linking demand to hybrid work environments that require seamless roaming and stable video quality. Despite this, dual-band units retained 40.43% share in 2025 as residential buyers prioritized coverage and delayed 6 GHz adoption until gigabit fiber availability improved. Quad-band devices remain niche, largely confined to gaming use cases with limited ecosystem support.

Vendors are advancing early Wi-Fi 8 development, with ASUSTeK Computer Inc. introducing a prototype router aligned with draft IEEE 802.11bn specifications and peak speeds approaching 30 Gbps. Regional preferences remain differentiated: North American households favor integrated units bundled with subscription-based security, while European consumers opt for modular systems that separate routing and wireless functions to address structural interference constraints. Certification by the Wi-Fi Alliance for automatic frequency coordination strengthens buyer confidence by ensuring coexistence within the 6 GHz band, supporting sustained uptake of tri-band architectures.

The 6 GHz segment is expanding at a 9.83% CAGR through 2031, outpacing the 5 GHz band, which held a 47.32% share in 2025. The Federal Communications Commission enabled this shift by opening a contiguous 1,200 MHz block from 5.925 to 6.875 GHz, creating seven interference-free 160 MHz channels capable of sustaining multi-gigabit throughput. The Department of Telecommunications reinforced global-scale economics by delicensing 500 MHz in December 2024, allowing vendors to standardize designs across key markets. Automated frequency coordination frameworks further extend 6 GHz usability to outdoor environments, including logistics yards and enterprise campuses, without disrupting incumbent microwave systems.

The Wi-Fi 6 router market still depends on 2.4 GHz for low-power, long-range IoT applications, although its throughput ceiling of 600 Mbps limits high-bandwidth use cases. The 5 GHz band remains the practical midpoint in dense residential settings, balancing capacity and wall penetration, despite interruptions from dynamic frequency selection triggered by radar detection. In contrast, 6 GHz is increasingly reserved for latency-sensitive enterprise and industrial workloads, where jitter must remain below 3 milliseconds to support deterministic networking. This segmentation highlights a clear functional stratification, with each band optimized for distinct performance and deployment requirements.

Geography Analysis

North America generated 35.43% of global revenue in 2025, supported by cable operators that lease gateways to defend against fiber overbuild competition. This model shifts entry into the Wi-Fi 6 router market from retail to carrier provisioning, sustaining higher average selling prices and faster upgrade cycles. Charter Communications and Comcast Corporation exemplify this approach by bundling advanced gateways within service plans, including early Wi-Fi 7 deployments to retain high-value subscribers. The region also benefits from higher broadband penetration and willingness to pay for performance tiers, reinforcing premium segment growth and accelerating adoption of next-generation standards ahead of global peers.

Asia-Pacific is expected to record the fastest CAGR of 12.43% between 2026 and 2031, driven by regulatory alignment and cost-efficient manufacturing ecosystems. The Department of Telecommunications enabled 6 GHz delicensing, aligned spectrum policy with the United States and Europe, and reduced compliance complexity for vendors. Chinese manufacturers, particularly those based in Shenzhen, dominate sub-USD 50 dual-band exports, while suppliers in Taiwan and South Korea focus on higher-margin tri-band systems. Concurrently, government-backed fiber rollouts in Indonesia and Vietnam expand broadband access, increasing router volumes even as price sensitivity moderates per-unit revenue growth.

South America and Africa represent emerging growth corridors, where public funding is translating connectivity ambitions into tangible infrastructure deployment. ANATEL is channeling BRL 3.2 billion (USD 640 million) into rural connectivity, while initiatives such as Nigeria's Project BRIDGE, supported by the African Development Bank, and South Africa's broadband expansion led by the Development Bank of Southern Africa are scaling last-mile access. Although absolute revenues remain lower than mature markets, sustained double-digit shipment growth is prompting vendors to pprioritize ruggedized, temperature-resilient designs suited to diverse environmental conditions.

- TP-Link Technologies Co., Ltd.

- NETGEAR, Inc.

- ASUSTeK Computer Inc.

- D-Link Corporation

- Huawei Technologies Co., Ltd.

- Belkin International, Inc.

- Cisco Systems, Inc.

- Xiaomi Corporation

- Ubiquiti Inc.

- Zyxel Communications Corporation

- MikroTikls SIA

- Shenzhen Tenda Technology Co., Ltd.

- Shenzhen Mercury Communication Technologies Co., Ltd.

- Zioncom Holdings Limited (TOTOLINK)

- Edimax Technology Co., Ltd.

- TRENDnet, Inc.

- GL Technologies Inc.

- Buffalo Inc.

- AVM Computersysteme Vertriebs GmbH

- DrayTek Corp.

- Synology Inc.

- Cambium Networks Corporation

- Ruijie Networks Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Broadband Upgrades to Gigabit-Class Services

- 4.2.2 Mandatory Transition of ISPs to Wi-Fi 6 Gateways After 2025 Spectrum Re-allocation

- 4.2.3 Explosive Growth of Smart-Home IoT Node Density

- 4.2.4 Government-Backed Rural Fiber Roll-outs in South America and Africa

- 4.2.5 Enterprise Network Refresh Cycles Driven by Hybrid Work Policies

- 4.2.6 Regulatory Approvals for 6 GHz Band Unleashing Wi-Fi 6E Capacity

- 4.3 Market Restraints

- 4.3.1 Premium Pricing of Wi-Fi 6E Tri-Band Models Above USD 400

- 4.3.2 Fragmented 6 GHz Rules Forcing Multi-SKU Compliance Costs

- 4.3.3 Semiconductor Lead-Times Exceeding 30 Weeks for Key Chipsets

- 4.3.4 Limited Consumer Awareness of Standard Benefits Slowing Adoption

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Dual-Band Routers

- 5.1.2 Tri-Band Routers

- 5.1.3 Quad-Band Routers

- 5.2 By Frequency Band

- 5.2.1 2.4 GHz

- 5.2.2 5 GHz

- 5.2.3 6 GHz (Wi-Fi 6E)

- 5.3 By End User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.4 By Distribution Channel

- 5.4.1 Online Stores

- 5.4.2 Offline Retail

- 5.4.3 Direct Enterprise Procurement

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TP-Link Technologies Co., Ltd.

- 6.4.2 NETGEAR, Inc.

- 6.4.3 ASUSTeK Computer Inc.

- 6.4.4 D-Link Corporation

- 6.4.5 Huawei Technologies Co., Ltd.

- 6.4.6 Belkin International, Inc.

- 6.4.7 Cisco Systems, Inc.

- 6.4.8 Xiaomi Corporation

- 6.4.9 Ubiquiti Inc.

- 6.4.10 Zyxel Communications Corporation

- 6.4.11 MikroTikls SIA

- 6.4.12 Shenzhen Tenda Technology Co., Ltd.

- 6.4.13 Shenzhen Mercury Communication Technologies Co., Ltd.

- 6.4.14 Zioncom Holdings Limited (TOTOLINK)

- 6.4.15 Edimax Technology Co., Ltd.

- 6.4.16 TRENDnet, Inc.

- 6.4.17 GL Technologies Inc.

- 6.4.18 Buffalo Inc.

- 6.4.19 AVM Computersysteme Vertriebs GmbH

- 6.4.20 DrayTek Corp.

- 6.4.21 Synology Inc.

- 6.4.22 Cambium Networks Corporation

- 6.4.23 Ruijie Networks Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

Wi-Fi 6 市場 – 2026-2032 年全球市場預測

Wi-Fi 6 市場 – 2026-2032 年全球市場預測 Wi-Fi 6E 路由器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

Wi-Fi 6E 路由器:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) Wi-Fi 6 技術市場:按組件、最終用戶、行業和地區分類

Wi-Fi 6 技術市場:按組件、最終用戶、行業和地區分類 全球Wi-Fi 6路由器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球Wi-Fi 6路由器市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026 年全球 Wi-Fi 6E 設備市場報告2026年Wi-Fi 6全球市場報告

2026 年全球 Wi-Fi 6E 設備市場報告2026年Wi-Fi 6全球市場報告 Wi-Fi 6 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類

Wi-Fi 6 市場分析及至 2035 年預測:按類型、產品類型、服務、技術、組件、應用、部署類型、最終用戶和解決方案分類 Wi-Fi 6 市場規模、佔有率和成長分析(按產品、類型、應用、垂直產業和地區分類)—2026-2033 年產業預測

Wi-Fi 6 市場規模、佔有率和成長分析(按產品、類型、應用、垂直產業和地區分類)—2026-2033 年產業預測 Wi-Fi 6 設備市場規模、佔有率和成長分析(按交付類型、地點類型、應用、垂直產業和地區分類)—產業預測(2026-2033 年)

Wi-Fi 6 設備市場規模、佔有率和成長分析(按交付類型、地點類型、應用、垂直產業和地區分類)—產業預測(2026-2033 年) Wi-Fi 6市場:產業趨勢·全球預測 (~2035年):提供類型·定位·用途·終端用戶產業·各地區

Wi-Fi 6市場:產業趨勢·全球預測 (~2035年):提供類型·定位·用途·終端用戶產業·各地區