|

市場調查報告書

商品編碼

2063742

南美低密度聚乙烯(LDPE):市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)South America Low-Density Polyethylene (LDPE) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

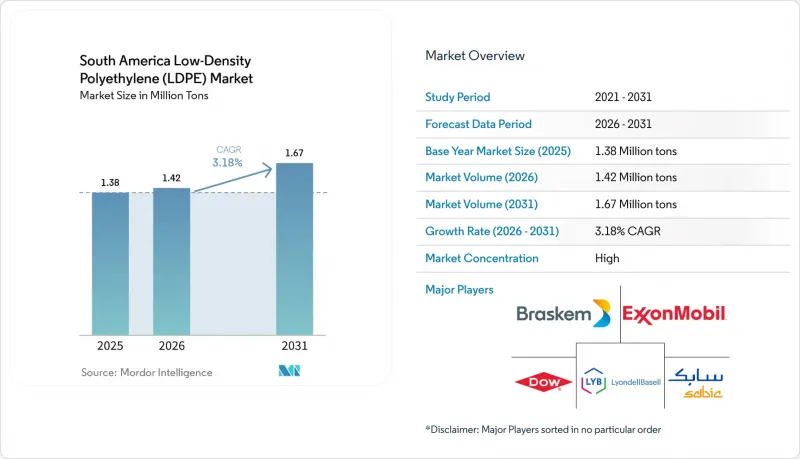

根據 Mordor Intelligence 預測,南美低密度聚乙烯 (LDPE) 市場規模將從 2025 年的 138 萬噸和 2026 年的 142 萬噸成長到 2031 年的 167 萬噸,2026 年至 2031 年的年複合成長率(CAGR)為 3.18%。

本報告按產品類型(片材和薄膜、吹塑成型、射出成型、擠壓塗布等)、終端用戶行業(包裝、農業、汽車、電氣和電子等)以及地區(巴西、阿根廷、哥倫比亞、智利、秘魯和其他南美國家)進行細分。市場預測以噸為單位。

南美低密度聚乙烯(LDPE)市場趨勢與洞察

政府鼓勵汽車業採用輕質塑膠的獎勵

巴西的「Programa Mover」計畫每年投資35億至41億雷亞爾用於降低車輛重量的技術研發,強制執行可回收性標準,並對符合這些標準的車型實施差別課稅。汽車製造商透過以低密度聚乙烯(LDPE)基內裝薄膜取代金屬和玻璃,將車輛重量減輕5%至8%,並將燃油效率提高5%。 2025年3月,Radichi集團開設了一家佔地1.7萬平方公尺的工廠,旨在實現其聚合物化合物向目的地供應商的本地化供應。阿根廷的汽車製造商平台正準備在2027年前達到同等標準,需求正在巴西以外的地區擴展。未來兩到四年的前景取決於汽車平臺的重新設計週期和檢驗流程。

巴西軟性包裝加工商的擴張

巴西加工商正部署高產能生產線,以滿足電子商務和食品宅配領域快速成長的需求。 Bomplastic公司的Comexi F2 MB壓平機每月可生產350噸高阻隔薄膜,而COEXPAN-EMSUR公司位於Jundiay的工廠將於2024年運作,從而加強其在巴西東南部的供應鏈。 Oben集團收購Vitopel公司,透過增加強大的雙向拉伸聚丙烯(BOPP)產品組合,加劇了密封層市場的競爭。片材和薄膜已佔南美低密度聚乙烯(LDPE)產量的近一半,而生產線的快速成長將為南美低密度聚乙烯市場帶來短期利好,因為生產線通常需要12至18個月才能達到額定產能。

LLDPE的替代品和新興的可生物分解薄膜

由於線性低密度聚乙烯 (LLDPE) 具有良好的抗穿刺性和可製成更薄的厚度,薄膜加工商更傾向於使用這種材料。巴西倉庫引入自動化托盤纏繞機後,拉伸套膜中低密度聚乙烯 (LDPE) 的使用量已減少了約 15%。可生物分解的聚乳酸 (PLA) 和聚羥基烷酯(PHA) 結構在高階一次性食品包裝領域,尤其是在智利的零售試點計畫中,正受到越來越多的關注,但由於樹脂價格飆升和缺乏堆肥基礎設施,它們的使用量仍然很低。加工設備升級通常需要兩年時間,這在中期內限制了南美低密度聚乙烯 (LDPE) 市場的發展。

細分市場分析

到2025年,片材和薄膜將佔區域低密度聚乙烯(LDPE)產量的48.37%,預計到2031年將以3.46%的複合年成長率成長。 Bomplastic公司每月350噸的生產線以及COEXPAN-EMSUR公司的產能擴張正在增強對巴西東南部的供應,該地區的履約中心推動了對高透明度重疊薄膜的需求。巴西塞拉多地區和阿根廷潘帕斯地區的農業地膜也為南美低密度聚乙烯(LDPE)市場在該領域的規模做出了貢獻。由於品牌商出於成本考慮轉向擠壓成型(高密度聚苯乙烯) ,吹塑成型瓶的市佔率停滯不前。同時,由於低密度聚乙烯的柔軟性和柔軟觸感,折疊式化妝品軟管仍保持著一定的市場佔有率。

奧本集團收購維托佩爾公司加劇了雙軸延伸聚丙烯(LDPE)密封層市場的競爭,他們看重的是LDPE無與倫比的熱黏性範圍。射出成型級LDPE僅佔市場需求的7%,由於終端用戶的成本削減措施,其市場佔有率正逐漸被聚丙烯取代,但在高階瓶蓋領域,由於需要可靠的防篡改功能,注塑級LDPE仍然佔據主導地位。擠壓塗布在液體紙盒領域仍保持強勁勢頭,而聚對苯二甲酸乙二醇酯(PET)基複合材料在常溫保存乳製品領域則呈現成長趨勢。綜合來看,預計到2031年,這些趨勢將使低密度聚乙烯(LDPE)片材和薄膜在南美洲市場保持強勁的市場佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府鼓勵汽車業採用輕質塑膠的獎勵

- 巴西軟性包裝加工商的擴張

- 基礎設施建設將為管道塗層開闢新的需求領域。

- 電子商務的快速發展正在加速拉伸膜的消耗。

- Braschem Triunfo 綜合設施的生物基低密度聚乙烯產能提升。

- 市場限制因素

- 以LLDPE和新型生物分解薄膜替代

- 由於不同地區石腦油價格的差異,導致原料(乙烯)價格波動。

- 當PCR含量超過20%時,機械性質會下降。

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依產品類型

- 片材和薄膜

- 吹塑成型

- 射出成型

- 擠壓塗布

- 其他產品類型

- 按最終用戶行業分類

- 包裝

- 農業

- 車

- 電氣和電子設備

- 建造

- 衛生保健

- 其他終端用戶產業

- 按地區

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- ALPA Group

- Borealis AG

- Braskem SA

- Chevron Phillips Chemical Company

- Dow

- Exxon Mobil Corporation

- INEOS

- LyondellBasell Industries Holdings BV

- Mitsui Chemicals Inc.

- Osterman Company

- SABIC

- Sasol

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america low-Density polyethylene market size is projected to expand from 1.38 Million tons in 2025 and 1.42 Million tons in 2026 to 1.67 Million tons by 2031, registering a CAGR of 3.18% between 2026 to 2031.

This report is Segmented by Product Type (Sheets and Films, Blow-Molded, Injection-Molded, Extrusion Coating, and Other Product Types), End-User Industry (Packaging, Agriculture, Automotive, Electrical and Electronics, and More), and Geography (Brazil, Argentina, Colombia, Chile, Peru, and Rest of South America). The Market Forecasts are Provided in Terms of Volume (Tons).

South America Low-Density Polyethylene (LDPE) Market Trends and Insights

Implementation of Government Incentives for Lightweight Plastic Adoption in Automotive

Brazil's Programa Mover injects BRL 3.5-4.1 billion each year into technologies that cut vehicle weight, mandating recyclability thresholds and differentiated taxation for compliant models. Automakers are substituting metal and glass with LDPE-based interior films, reducing curb weight by 5%-8% and improving fuel economy by as much as 5%. RadiciGroup's 17,000 m2 plant opened in March 2025 to localize polymer-compound supply for tier-one suppliers. Argentine original equipment manufacturer (OEM) platforms are preparing to align with comparable standards by 2027, extending demand beyond Brazil. The 2-to-4-year horizon reflects vehicle-platform redesign cycles and validation protocols.

Expansion of Flexible-Packaging Converters in Brazil

Brazilian converters are installing high-output lines to preempt demand from rapid e-commerce and food-delivery growth. Bomplastic's Comexi F2 MB press contributes 350 tons per month of high-barrier film, while COEXPAN-EMSUR's Jundiai plant went on-stream in 2024, strengthening supply in the southeast corridor. Oben Group's purchase of Vitopel intensifies contest for sealant-layer business by adding a strong BOPP portfolio. Sheets and films already claim nearly half of South American LDPE volume, and rapid line ramp-ups usually reach nameplate in 12-18 months, underscoring the short-term boost to the South America Low-Density Polyethylene (LDPE) market.

Substitution by LLDPE and Emerging Biodegradable Films

Film processors prefer Linear Low-Density Polyethylene (LLDPE) for puncture resistance and downgauging; automated pallet-wrappers in Brazil's warehouses have already cut LDPE usage in stretch-hood films by about 15%. Biodegradable polylactic acid (PLA) and polyhydroxyalkanoate (PHA) structures are gaining traction in premium single-use food packaging, especially in Chilean retail pilots, but high resin premiums and scarce composting infrastructure keep volumes marginal. Converter re-tooling typically takes two years, explaining the medium-term drag on the South America Low-Density Polyethylene (LDPE) market.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Upgrades Opening New Pipe-Coating Demand Corridors

- E-Commerce Boom Accelerating Stretch-Film Consumption

- Feedstock (Ethylene) Price Volatility Linked to Regional Naphtha Differentials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sheets and films captured 48.37% of regional LDPE volume in 2025 and are forecast to rise at a 3.46% CAGR through 2031. Bomplastic's 350 tons per month line and COEXPAN-EMSUR's ramp-up feed Brazil's southeast, where fulfillment centers dictate demand for high-clarity overwraps. Agricultural mulch films in Brazil's Cerrado and Argentina's Pampas also contribute to the South America Low-Density Polyethylene (LDPE) market size for this segment. Blow-molded bottles trail because brand owners shift squeezable formats to (High-Density Polyethylene) for cost reasons, while collapsible cosmetic tubes keep a foothold for LDPE's flexibility and soft-touch feel.

Oben Group's Vitopel takeover escalates competition as Biaxially Oriented Polypropylene (BOPP) producers pursue LDPE sealant layers given the latter's unmatched hot-tack range. Injection-molding grades, only 7% of demand, face polypropylene substitution amid end-user cost discipline, but still thrive in premium closures that need secure tamper evidence. Extrusion-coating remains steady in liquid cartons, though Polyethylene Terephthalate (PET)-based laminates grow in shelf-stable dairy. Together these dynamics keep the South America Low-Density Polyethylene (LDPE) market share for sheets and films firmly ahead through 2031.

List of Companies Covered in this Report:

- ALPA Group

- Borealis AG

- Braskem SA

- Chevron Phillips Chemical Company

- Dow

- Exxon Mobil Corporation

- INEOS

- LyondellBasell Industries Holdings B.V.

- Mitsui Chemicals Inc.

- Osterman Company

- SABIC

- Sasol

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Implementation of government incentives for lightweight plastic adoption in automotive

- 4.2.2 Expansion of flexible-packaging converters in Brazil

- 4.2.3 Infrastructure upgrades opening new pipe-coating demand corridors

- 4.2.4 E-commerce boom accelerating stretch-film consumption

- 4.2.5 Bio-LDPE capacity build-out at Braskem's Triunfo complex

- 4.3 Market Restraints

- 4.3.1 Substitution by LLDPE and emerging biodegradable films

- 4.3.2 Feed-stock (ethylene) price volatility linked to regional naphtha differentials

- 4.3.3 PCR-content limits above 20% degrading mechanical properties

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Sheets and Films

- 5.1.2 Blow-Molded

- 5.1.3 Injection-Molded

- 5.1.4 Extrusion Coating

- 5.1.5 Other Product Types

- 5.2 By End-user Industry

- 5.2.1 Packaging

- 5.2.2 Agriculture

- 5.2.3 Automotive

- 5.2.4 Electrical and Electronics

- 5.2.5 Construction

- 5.2.6 Healthcare

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Colombia

- 5.3.4 Chile

- 5.3.5 Peru

- 5.3.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ALPA Group

- 6.4.2 Borealis AG

- 6.4.3 Braskem SA

- 6.4.4 Chevron Phillips Chemical Company

- 6.4.5 Dow

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 INEOS

- 6.4.8 LyondellBasell Industries Holdings B.V.

- 6.4.9 Mitsui Chemicals Inc.

- 6.4.10 Osterman Company

- 6.4.11 SABIC

- 6.4.12 Sasol

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

低密度聚乙烯市場分析:按製造流程、原料、應用和地區分類(2026-2034 年)

低密度聚乙烯市場分析:按製造流程、原料、應用和地區分類(2026-2034 年) 低密度聚乙烯市場:按技術、應用和地區分類

低密度聚乙烯市場:按技術、應用和地區分類 低密度聚乙烯市場分析及預測(至2035年):類型、產品、應用、技術、形式、最終用戶、材料類型、製程、功能與組件

低密度聚乙烯市場分析及預測(至2035年):類型、產品、應用、技術、形式、最終用戶、材料類型、製程、功能與組件 2026年全球低密度聚乙烯市場報告

2026年全球低密度聚乙烯市場報告 低密度聚乙烯(LDPE)市場,全球市場,2025-2029年

低密度聚乙烯(LDPE)市場,全球市場,2025-2029年 生質能聚乙烯低密度聚乙烯市場按等級、原料、產品形式、應用和分銷管道分類,全球預測,2026-2032年

生質能聚乙烯低密度聚乙烯市場按等級、原料、產品形式、應用和分銷管道分類,全球預測,2026-2032年 低密度聚乙烯:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

低密度聚乙烯:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 全球低密度聚乙烯市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考察、未來預測(2026-2034)擠壓低密度聚乙烯(LDPE)市場:未來預測(2025-2030)

全球低密度聚乙烯市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的考察、未來預測(2026-2034)擠壓低密度聚乙烯(LDPE)市場:未來預測(2025-2030) 線型低密度聚乙烯(LLDPE)的全球市場:類別,各應用領域,各終端用戶產業,各地區,機會,預測,2018年~2032年

線型低密度聚乙烯(LLDPE)的全球市場:類別,各應用領域,各終端用戶產業,各地區,機會,預測,2018年~2032年