|

市場調查報告書

商品編碼

2063741

南美洲生物炭:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)South America Biochar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

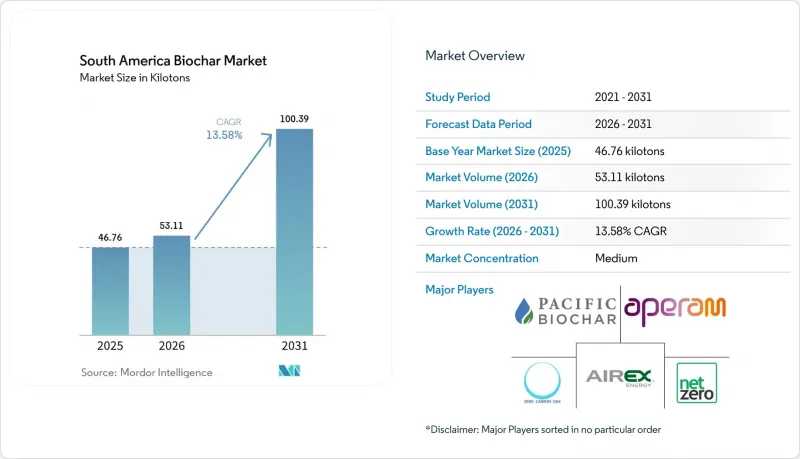

據 Mordor Intelligence 稱,2025 年南美生物炭市場價值為 46.76 千噸,預計到 2031 年將達到 100.39 千噸,而 2026 年為 53.11 千噸,在預測期(2026-2031 年)內複合年成長率為 13.58%。

本報告按技術(熱解、氣化系統及其他技術)、應用(農業、畜牧業、工業應用及其他應用)和地區(巴西、阿根廷、哥倫比亞及其他南美國家)進行細分。市場預測以噸為單位。

南美洲生物炭市場趨勢與洞察

對提高農業土壤肥力的需求

熱帶土壤呈酸性,陽離子交換容量低,阻礙了大豆、玉米和咖啡的養分供應。巴西的田間試驗表明,施用5-10%(體積比)的生物炭可使龍舌蘭生物量增加60%,而甘蔗渣生物炭可使土壤pH值提高0.7個單位,並減少40%的石灰用量。咖啡殼生物炭在沙質土壤中可多保持25%的水分,進而緩解阿拉比卡咖啡品種開花期的乾旱壓力。生物炭的價格在每噸700-1200美元之間,一旦收回三個生長季減少養分用量的成本,其價格就足以與進口的氮磷鉀複合肥競爭。 2024年,巴西發展部成立了第328號研究委員會,負責制定全國熱解生物炭標準,這顯示大規模推廣應用的政策已經準備就緒。

排碳權和新興的自願性碳市場

利用生物炭抵消碳排放可以獲得溢價,因為碳可以穩定保存數千年。根據 Puro.earth 的 CORCHAR 指數,2025 年的碳權價格為每噸 600-1000 雷亞爾(120-200 美元),遠高於歐洲的排放權價格。 Exomad Green 與微軟簽訂的 124 萬噸合約將碳移除價格定在每噸 200-250 美元左右,用於資助玻利維亞產能翻倍。 Altitude 和 Empacar 於 2026 年簽署的 100 萬噸合約證實了企業對可測量、可報告和檢驗(MRV) 碳儲存的需求日益成長。 Verra 向 Aperam BioEnergia (VM0044) 發放的 161,507 個 CORC 表明,工業規模的生物炭項目可以在供應農業市場的同時實現碳貨幣化。

區域產能不足及供應鏈分散

NetZero 和 Exomad Green 兩家公司合計供該地區 60% 的產量,導致方圓 300 公里內的許多地區無法獲得商業產品。哥倫比亞桑坦德省的間歇式窯爐每週僅生產 200-500 公斤生物炭,而阿根廷的稻草生物炭計畫仍處於試驗階段。運輸低密度生物炭會降低利潤,因此很少有距離超過 100 公里的農民採用這種產品。巴西 600 萬噸的木炭產業中,只有不到 2% 的產品符合農業級標準,顯示其市場滲透率緩慢。

細分市場分析

至2025年,熱解將佔生物炭總產量的73.37%,預計到2031年將以15.96%的複合年成長率成長。這將為公司在2031年前保持在南美洲生物炭市場的領先地位奠定基礎。 300-400°C的慢速熱解透過延長停留時間來保留功能基團,從而提高陽離子交換效率;而600-700°C的快速熱解則能增強碳固定,從而產生碳權。 NetZero的第二代裝置以20-40分鐘的循環週期運作,溫度為450-550°C,並回收合成氣作為現場熱源,以降低營業成本。氣化法仍是一種輔助方法,因為其炭產率僅為原料品質的10-20%,而其他方法,例如水熱碳化,仍處於中試階段。 Verra 即將推出的 VM0044 v2 將使 500-2,000 噸模組化系統有資格獲得信貸計劃,從而實現中等規模的部署,並有可能使南美洲的生物炭產業多樣化。

從市政垃圾處理公司到礦業公司,對熱解設備的需求範圍很廣。巴西Eco.Invest提供的貸款現在也用於購買淡季咖啡渣處理反應器。一個大學研究小組正在改進一種低成本的嵌套式滾筒窯,用於處理巴西莓種子,最終將合作社的安裝價格降低到150美元,儘管代價是犧牲了一些MRV(監測、報告和核查)精度。隨著摩托車騎士尋求透過銷售生物炭和電力供應實現雙重收入來源,整合數據記錄器、旋風式氣體洗滌和冷凝水回收功能的設備供應商可能會帶來更高的利潤率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對提高農業土壤肥力的需求

- 排碳權和新興的自願性碳市場

- 將其作為牲畜飼料添加劑,以減少甲烷排放

- 政府對永續廢棄物管理的獎勵

- 利用生物炭混合物回收礦山廢石

- 市場限制因素

- 區域產能短缺和供應鏈分散

- 先進熱解設備的高昂資本投資與營運成本

- 生物炭品質差異導致農業生產結果不均勻

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 透過技術

- 熱解

- 氣化系統

- 其他技術

- 透過使用

- 家畜

- 農業

- 工業應用

- 其他用途

- 按地區

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Airex Energy

- Aperam BioEnergia

- Biochar Solutions Inc.

- Blackwood Technology

- Carbo Culture

- Carbon Gold

- Diacarbon Energy Inc.

- NetZero

- Nova Analytics Biochar

- Pacific Biochar Benefit Corporation

- ZeroCarbon One

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america biochar market size was valued at 46.76 kilotons in 2025 and is estimated to grow from 53.11 kilotons in 2026 to reach 100.39 kilotons by 2031, at a CAGR of 13.58% during the forecast period (2026-2031).

This report is Segmented by Technology (Pyrolysis, Gasification Systems, and Other Technologies), Application (Agriculture, Animal Farming, Industrial Uses, and Other Applications), and Geography (Brazil, Argentina, Colombia, and Rest of South America). The Market Forecasts are Provided in Terms of Volume (Tons).

South America Biochar Market Trends and Insights

Agricultural Soil-Fertility Improvement Demand

Tropical soils are acidic and low in cation-exchange capacity, hampering nutrient availability for soybean, maize, and coffee. Field trials showed that 5-10% biochar by volume raised Agave sisalana biomass by 60% in Brazil, while sugarcane-bagasse biochar lifted soil pH by up to 0.7 units and cut lime use by 40%. Coffee-husk biochar retained 25% more water in sandy soils, easing drought stress during Arabica flowering. With prices of USD 700-1,200 per ton, biochar competes with imported NPK when amortized across three seasons of nutrient-use savings. Brazil's Ministry of Development formed Study Commission 328 in 2024 to draft national pyrogenic-biocarbon standards, signaling policy readiness for scale.

Carbon Credits and Emerging Voluntary Carbon Markets

Biochar offsets command premiums because carbon remains stable for millennia. Puro.earth's CORCHAR index valued credits at R$600-1,000 (USD 120-200) in 2025, far above European allowance prices. Exomad Green's 1.24-million-ton contract with Microsoft priced removals near USD 200-250, financing a doubled Bolivian capacity. Altitude and Empacar's 1-million-ton deal in 2026 confirms rising corporate appetite for measurable, reportable, verifiable (MRV) carbon storage. Verra's VM0044 issuance of 161,507 CORCs to Aperam BioEnergia proves that industrial-scale biochar projects can monetize carbon while supplying agronomic markets.

Insufficient Regional Production Capacity and Fragmented Supply Chain

NetZero and Exomad Green together supply 60% of regional output, leaving many areas without commercial product within 300 km. Batch kilns in Colombia's Santander department turn out just 200-500 kg a week, while Argentina's rice-straw project remains pilot-scale. Transporting low-density biochar erodes margins, so farmers beyond 100 km rarely adopt. Fewer than 2% of Brazil's 6 million-ton charcoal sector meets agronomic-grade standards, delaying penetration.

Other drivers and restraints analyzed in the detailed report include:

- Adoption in Livestock Feed Additives for Methane Reduction

- Government Incentives for Sustainable Waste Management

- High Capital and Operating Costs of Advanced Pyrolysis Units

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pyrolysis supplied 73.37% of 2025 volume and is forecast to grow at a 15.96% CAGR through 2031, underpinning the South America biochar market size leadership through 2031. Slow pyrolysis at 300-400 °C leverages longer residence times to sustain functional groups that improve cation exchange, while fast modes at 600-700 °C increase carbon permanence for credit generation. NetZero's Gen2 units run 20-40-minute cycles at 450-550 °C and capture syngas for onsite heat, lowering cash operating costs. Gasification remains secondary because char yields are just 10-20% of feedstock mass, and other pathways such as hydrothermal carbonization are still pilot level. Verra's forthcoming VM0044 v2 will allow modular 500-2,000 ton systems into credit schemes, potentially unlocking mid-scale adoption and diversifying the South America biochar industry.

Demand for pyrolysis equipment stretches from municipal waste managers to mining firms. Brazil's Eco.Invest loans now cover reactor purchases that process coffee husks during off-season months. University groups adapt low-cost nested-drum kilns for acai seeds, giving cooperatives a USD 150 entry price at the expense of MRV precision. Equipment suppliers that integrate data loggers, cyclone gas cleaning, and condensate recovery may capture higher margins as buyers seek dual revenue from biochar sales and electricity.

List of Companies Covered in this Report:

- Airex Energy

- Aperam BioEnergia

- Biochar Solutions Inc.

- Blackwood Technology

- Carbo Culture

- Carbon Gold

- Diacarbon Energy Inc.

- NetZero

- Nova Analytics Biochar

- Pacific Biochar Benefit Corporation

- ZeroCarbon One

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Agricultural soil-fertility improvement demand

- 4.2.2 Carbon credits and emerging voluntary carbon markets

- 4.2.3 Adoption in livestock feed additives for methane reduction

- 4.2.4 Government incentives for sustainable waste management

- 4.2.5 Mining-tailings rehabilitation using biochar blends

- 4.3 Market Restraints

- 4.3.1 Insufficient regional production capacity and fragmented supply chain

- 4.3.2 High capital and operating costs of advanced pyrolysis units

- 4.3.3 Variable biochar quality causing inconsistent agronomic results

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Technology

- 5.1.1 Pyrolysis

- 5.1.2 Gasification Systems

- 5.1.3 Other Technologies

- 5.2 By Application

- 5.2.1 Animal Farming

- 5.2.2 Agriculture

- 5.2.3 Industrial Uses

- 5.2.4 Others Applications

- 5.3 By Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Colombia

- 5.3.4 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Airex Energy

- 6.4.2 Aperam BioEnergia

- 6.4.3 Biochar Solutions Inc.

- 6.4.4 Blackwood Technology

- 6.4.5 Carbo Culture

- 6.4.6 Carbon Gold

- 6.4.7 Diacarbon Energy Inc.

- 6.4.8 NetZero

- 6.4.9 Nova Analytics Biochar

- 6.4.10 Pacific Biochar Benefit Corporation

- 6.4.11 ZeroCarbon One

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Rapid Urbanization and Industrialization

- 7.3 Rising Demand for Renewable Energy and Carbon-Negative Materials

功能性生物炭市場-全球產業規模、佔有率、趨勢、機會、預測:依技術、應用、區域和競爭格局分類,2021-2031年

功能性生物炭市場-全球產業規模、佔有率、趨勢、機會、預測:依技術、應用、區域和競爭格局分類,2021-2031年 生物炭市場規模、佔有率和成長分析:按原料類型、製造方法、應用、終端用戶產業和地區分類-2026-2033年產業預測

生物炭市場規模、佔有率和成長分析:按原料類型、製造方法、應用、終端用戶產業和地區分類-2026-2033年產業預測 生物炭市場:2026-2032年全球市場預測(依製造技術、原料類型、產品形態、反應器配置、活化類型、應用、通路和最終用戶分類)

生物炭市場:2026-2032年全球市場預測(依製造技術、原料類型、產品形態、反應器配置、活化類型、應用、通路和最終用戶分類) 生物炭市場規模、佔有率和趨勢:按原料類型、技術類型、產品形式、應用和地區分類,並預測2026年至2034年

生物炭市場規模、佔有率和趨勢:按原料類型、技術類型、產品形式、應用和地區分類,並預測2026年至2034年 生物炭生產設備市場:按類型、技術和地區分類

生物炭生產設備市場:按類型、技術和地區分類 全球生物炭市場(2026-2036)

全球生物炭市場(2026-2036) 歐洲生物炭:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)生物炭:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球生物炭市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球生物炭市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)

歐洲生物炭:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)生物炭:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)全球生物炭市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球生物炭市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)