|

市場調查報告書

商品編碼

2063739

南美洲界面活性劑市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)South America Surfactants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

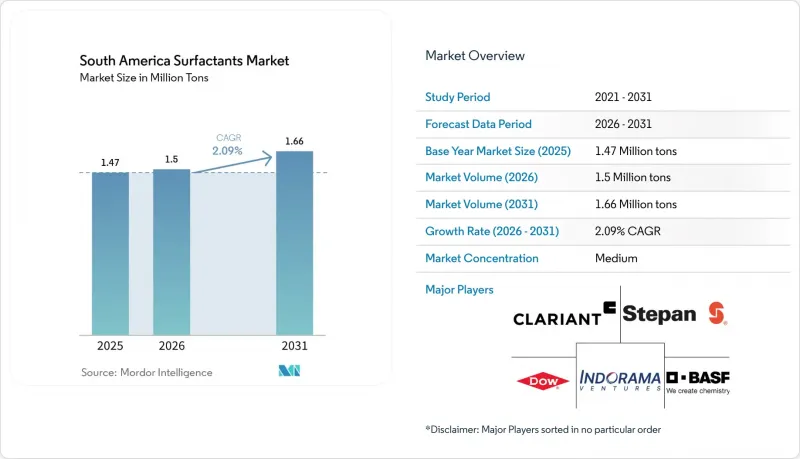

根據 Mordor Intelligence 預測,南美洲界面活性劑市場規模預計在 2025 年達到 147 萬噸,2026 年達到 150 萬噸,到 2031 年達到 166 萬噸,2026 年至 2031 年的複合年成長率為 2.09%。

本報告按類型(陰離子界面活性劑、陽離子界面活性劑等)、原料(合成界面活性劑和生物基界面活性劑)、應用(家用肥皂和清潔劑、個人護理用品、商用和工業清潔劑等)以及地區(巴西、阿根廷、智利、哥倫比亞、秘魯和其他南美國家)進行細分。市場預測以噸為單位。

南美洲表面活性劑市場趨勢與洞察

個人護理和家居護理產品消費激增。

2024年,拉丁美洲化妝品和個人保健產品的銷售額總合247.4億美元,其中巴西佔了98.3億美元。這一成長凸顯了消費者從傳統固態轉向高級產品(如液體沐浴露和洗髮精)的趨勢。溫和的兩性界面活性劑(如椰油醯胺丙基甜菜鹼)的價格比通用型醇類界面活性劑(LAS)高出30%至50%,即使原油衍生原料成本波動,也能確保價格穩定。 2024年,巴西液體清潔劑的零售額達到6.9781億美元,主要得益於都市區滾筒洗衣機的日益普及,而這些洗衣機更傾向於使用醇醚和醇醚硫酸酯(AES)類洗滌劑。在阿根廷,由於高通膨限制了家電的更換,粉狀清潔劑仍然佔據主導地位。在哥倫比亞和秘魯,清潔劑的普及程度在都市區地區存在差異,這給經銷商的庫存管理帶來了挑戰。

加速擴大農藥生產能力

2023年至2024年間,巴西農藥處理的耕地面積增加了6.1%,達到8,500萬公頃。 BRANDT Consolidated公司投資1500萬美元在其位於朗多諾波利斯的輔助工廠生產用於大豆和玉米種植的醇醚組合藥物。由於新投資的延遲,阿根廷製劑生產商依賴進口,但修訂後的噴霧漂移指南正在增加對低發泡、高溫穩定性好的非離子介面活性劑的需求。巴西監管機構計劃在2027年前逐步淘汰農作物保護產品中的烷基酚聚氧乙烯醚,從而將需求轉向符合ISO 14001標準的脂肪胺聚氧乙烯醚和醇醚。

加強APEO和含磷廢水法規

巴西國家環境委員會(CONAMA)通過2024年第498號法令,將工業污水中的烷基酚含量限制在10微克/公升,並將清潔劑中的壬基酚聚氧乙烯醚(NPE)含量限制在0.1%(質量分數),該法令將於2027年1月生效。在阿根廷,全氟烷基和多氟烷基物質(PFAS)將被列入持久性有機污染物(POPs)清單,並將於2026年12月前禁止在消防泡沫中使用含PFAS的界面活性劑。轉向使用醇聚氧乙烯醚和胺氧化物將使原料成本增加8%至12%,這對以競標主導的代理管道構成挑戰。

細分市場分析

2025年,陰離子界面活性劑的銷售量佔比達到46.85%,其中LAS因其在粉狀清潔劑中的廣泛應用而佔據主導地位。 AES和AOS則憑藉其在液體清潔劑和洗髮精中的應用,進一步提升了銷售量。 LAS的價格波動與煤油衍生的直鏈烷基苯密切相關,這促使巴西東北部地區轉向使用MES。在該地區,由於當地油脂化學原料的優勢,MES與LAS的成本差異已縮小至每噸不到100美元。諸如用於鋰浮選的仲磺酸鹽和用於超溫和洗滌劑的磺基琥珀酸鹽等特殊細分市場,雖然規模較小,但盈利豐厚。

預計到2031年,兩性界面活性劑和其他類型的界面活性劑將以3.05%的複合年成長率成長,這主要得益於個人護理品牌對溫和性的重視以及到2027年APEO助表面活性劑的逐步淘汰。非離子界面活性劑主要由醇乙氧基化物組成,其產品正從烷基酚乙氧基化物轉向源自巴西油脂化學工業的線性C12-C14醇乙氧基化物。監管壓力和優質化趨勢正在逐步重塑南美洲表面活性劑市場的類型模式。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 個人護理和家居護理產品消費市場的蓬勃發展

- 農藥生產能力的擴張正在加速。

- 隨著油脂化學原料的成長,生物基界面活性劑正引起人們的注意。

- 鋰礦浮選化學品的需求正在激增。

- 巴西的「綠色化學」稅收優惠政策

- 市場限制因素

- APEO 和加強磷廢水法規

- 原油價格波動正在影響LAB原料。

- 區域宏觀經濟不穩定

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 陰離子活性劑

- 直鏈烷基苯磺酸鹽(LAS 或 LABS)

- 醇乙氧基硫酸鹽(AES)

- α-烯烴磺酸鹽(AOS)

- 二級烷基磺酸鈉(SAS)

- 甲酯磺酸鹽(MES)

- 磺基琥珀酸酯

- 其他陰離子活性劑

- 陽離子界面活性劑

- 季銨化合物

- 其他陽離子界面活性劑

- 非離子界面活性劑

- 醇乙氧基化物

- 乙氧基化烷基酚

- 脂肪酸酯

- 其他非離子表面活性劑

- 雌雄同體和其他類型

- 陰離子活性劑

- 按原產地

- 合成界面活性劑

- 生物基界面活性劑

- 透過使用

- 家用肥皂和清潔劑

- 個人護理

- 公共和工業清潔

- 油田化學品

- 潤滑劑和燃油添加劑

- 殺蟲劑

- 食品加工

- 紡織加工

- 其他用途

- 按地區

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 秘魯

- 其他南美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- BASF

- Braskem SA

- Clariant

- Croda International plc

- Deten Quimica SA

- Dow

- Evonik Industries AG

- Godrej Industries

- Indorama Ventures Public Company Limited

- Innospec

- Kao Corporation

- Lonza

- Nouryon

- P&G Chemicals

- Sasol

- Solvay

- Stepan Company

- TENSAC

- YPF

第7章 市場機會與未來展望

According to Mordor Intelligence, the south america surfactants market size is projected to be 1.47 Million tons in 2025, 1.5 Million tons in 2026, and reach 1.66 Million tons by 2031, growing at a CAGR of 2.09% from 2026 to 2031.

This report is Segmented by Type (Anionic Surfactants, Cationic Surfactants, and More), Origin (Synthetic Surfactants and Bio-Based Surfactants), Application (Household Soaps and Detergents, Personal Care, Institutional and Industrial Cleaning, and More), and Geography (Brazil, Argentina, Chile, Colombia, Peru, and Rest of South America). The Market Forecasts are Provided in Volume (Tons).

South America Surfactants Market Trends and Insights

Growing Personal- and Home-Care Consumption Boom

Latin America's cosmetics and personal-care sales totaled USD 24.74 billion in 2024, with Brazil alone contributing USD 9.83 billion. This growth highlights a shift toward premium products, such as liquid body washes and shampoos, over traditional bar soaps. Mild amphoteric surfactants like cocamidopropyl betaine command a 30-50% price premium over commodity LAS, ensuring price stability even amid fluctuations in crude-derived feedstock costs. Brazil's liquid laundry detergent retail value reached USD 697.81 million in 2024, driven by urban adoption of front-loading washing machines that favor alcohol ethoxylate and Alcohol Ethoxy Sulfate (AES) systems. In Argentina, powder detergents remain dominant due to high inflation limiting appliance upgrades. Colombia and Peru exhibit mixed adoption of detergent formats across urban and rural areas, complicating distributor inventory management.

Accelerating Agrochemical Capacity Additions

Brazil's pesticide-treated cropland expanded by 6.1% between 2023 and 2024, reaching 85 million hectares. BRANDT Consolidated invested USD 15 million in an adjuvant plant in Rondonopolis to supply alcohol-ethoxylate blends for soybean and corn crops. Argentine formulators depend on imports due to delayed greenfield investments, but revised spray-drift guidelines are driving demand for low-foam, high-temperature-stable nonionics. Brazilian regulators plan to phase out alkylphenol ethoxylates in crop-protection products by 2027, shifting demand toward fatty-amine ethoxylates and alcohol ethoxylates that meet ISO 14001 standards.

Tightening APEO and Phosphorus Effluent Laws

Brazil's Conselho Nacional do Meio Ambiente (CONAMA), 498/2024 limits industrial effluent alkylphenol content to 10 µg/L and restricts detergent nonylphenol ethoxylate (NPE) to 0.1% by mass starting January 2027. Argentina has added PFAS compounds to its POPs inventory and will ban PFAS-containing surfactants in firefighting foams by December 2026. Reformulating to alcohol ethoxylates and amine oxides increases raw material costs by 8%-12%, a challenge for tender-driven institutional channels.

Other drivers and restraints analyzed in the detailed report include:

- Bio-Based Surfactants Favored by Oleochemical Feedstock Growth

- Lithium-Ore Flotation Chemicals Demand Spike

- Crude-Oil Price Volatility Hitting LAB Feedstock

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Anionic surfactants accounted for 46.85% of 2025 volume, with LAS dominating due to its prevalence in powder detergents. AES and AOS contributed additional volume through liquid detergent and shampoo applications. LAS price volatility, linked to kerosene-derived linear alkylbenzene, is prompting a shift toward MES in Brazil's Northeast, where localized oleochemical feedstocks narrow cost differences to less than USD 100/t compared to LAS. Specialty sub-segments, such as secondary alkane sulfonates in lithium flotation and sulfosuccinates in ultra-mild cleansers, offer niche but profitable opportunities.

Amphoteric surfactants and other types are projected to grow at a 3.05% CAGR through 2031, driven by personal-care brands emphasizing mildness and the phase-out of APEO co-surfactants by 2027. Nonionics, primarily alcohol ethoxylates, are transitioning from alkylphenol ethoxylates to straight-chain C12-C14 alcohol ethoxylates derived from Brazil's oleochemical industry. Regulatory pressures and premiumization trends are gradually reshaping the South America surfactants market by type.

List of Companies Covered in this Report:

- BASF

- Braskem SA

- Clariant

- Croda International plc

- Deten Quimica S.A.

- Dow

- Evonik Industries AG

- Godrej Industries

- Indorama Ventures Public Company Limited

- Innospec

- Kao Corporation

- Lonza

- Nouryon

- P&G Chemicals

- Sasol

- Solvay

- Stepan Company

- TENSAC

- YPF

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing personal and home-care consumption boom

- 4.2.2 Accelerating agrochemical capacity additions

- 4.2.3 Bio-based surfactants favoured by oleochemical feedstock growth

- 4.2.4 Lithium-ore flotation chemicals demand spike

- 4.2.5 Brazilian "green-chem" tax incentives

- 4.3 Market Restraints

- 4.3.1 Tightening APEO and phosphorus effluent laws

- 4.3.2 Crude-oil price volatility hitting LAB feedstock

- 4.3.3 Regional macro-economic instability

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Anionic Surfactants

- 5.1.1.1 Linear Alkylbenzene Sulfonate (LAS or LABS)

- 5.1.1.2 Alcohol Ethoxy Sulfate (AES)

- 5.1.1.3 Alpha-Olefin Sulfonate (AOS)

- 5.1.1.4 Secondary Alkane Sulfonate (SAS)

- 5.1.1.5 Methyl Ester Sulfonate (MES)

- 5.1.1.6 Sulfosuccinates

- 5.1.1.7 Other Anionic Surfactants

- 5.1.2 Cationic Surfactants

- 5.1.2.1 Quaternary Ammonium Compounds

- 5.1.2.2 Other Cationic Surfactants

- 5.1.3 Non-ionic Surfactants

- 5.1.3.1 Alcohol Ethoxylates

- 5.1.3.2 Ethoxylated Alkyl-phenols

- 5.1.3.3 Fatty Acid Esters

- 5.1.3.4 Other Non-ionic Surfactants

- 5.1.4 Amphoteric and Other Types

- 5.1.1 Anionic Surfactants

- 5.2 By Origin

- 5.2.1 Synthetic Surfactants

- 5.2.2 Bio-based Surfactants

- 5.3 By Application

- 5.3.1 Household Soaps and Detergents

- 5.3.2 Personal Care

- 5.3.3 Institutional and Industrial Cleaning

- 5.3.4 Oilfield Chemicals

- 5.3.5 Lubricants and Fuel Additives

- 5.3.6 Agricultural Chemicals

- 5.3.7 Food Processing

- 5.3.8 Textile Processing

- 5.3.9 Other Applications

- 5.4 By Geography

- 5.4.1 Brazil

- 5.4.2 Argentina

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 BASF

- 6.4.2 Braskem SA

- 6.4.3 Clariant

- 6.4.4 Croda International plc

- 6.4.5 Deten Quimica S.A.

- 6.4.6 Dow

- 6.4.7 Evonik Industries AG

- 6.4.8 Godrej Industries

- 6.4.9 Indorama Ventures Public Company Limited

- 6.4.10 Innospec

- 6.4.11 Kao Corporation

- 6.4.12 Lonza

- 6.4.13 Nouryon

- 6.4.14 P&G Chemicals

- 6.4.15 Sasol

- 6.4.16 Solvay

- 6.4.17 Stepan Company

- 6.4.18 TENSAC

- 6.4.19 YPF

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

界面活性劑市場:依產品、原料、功能及應用分類-2026-2032年全球市場預測界面活性劑提高採收率市場:按類型、來源、技術、分類、功能和應用分類-2026-2032年全球市場預測

界面活性劑市場:依產品、原料、功能及應用分類-2026-2032年全球市場預測界面活性劑提高採收率市場:按類型、來源、技術、分類、功能和應用分類-2026-2032年全球市場預測 肺表面活性劑市場:按類型、藥物類型、適應症、給藥途徑、分銷管道和地區分類

肺表面活性劑市場:按類型、藥物類型、適應症、給藥途徑、分銷管道和地區分類 全球表面活性劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球無 PFAS 陰離子界面活性劑市場(按最終用途產業、產品類型、應用、形態、通路、原料來源和產業鏈長度分類)預測(2026-2032 年)全球無 PFAS 離子界面活性劑市場(按產品類型、物理形態、應用、分銷管道和終端用戶行業分類)預測(2026-2032 年)全球無 PFAS 非離子界面活性劑市場(按類型、形態、應用和分銷管道分類)預測(2026-2032 年)油田水泥防沉劑市場按類型、井型、幾何形狀、技術、壓力等級、應用和終端用戶分類,全球預測,2026-2032年溶劑型無 PFAS 界面活性劑市場按功能、產品等級、包裝、銷售管道和應用分類 - 全球預測,2026-2032 年

全球表面活性劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球無 PFAS 陰離子界面活性劑市場(按最終用途產業、產品類型、應用、形態、通路、原料來源和產業鏈長度分類)預測(2026-2032 年)全球無 PFAS 離子界面活性劑市場(按產品類型、物理形態、應用、分銷管道和終端用戶行業分類)預測(2026-2032 年)全球無 PFAS 非離子界面活性劑市場(按類型、形態、應用和分銷管道分類)預測(2026-2032 年)油田水泥防沉劑市場按類型、井型、幾何形狀、技術、壓力等級、應用和終端用戶分類,全球預測,2026-2032年溶劑型無 PFAS 界面活性劑市場按功能、產品等級、包裝、銷售管道和應用分類 - 全球預測,2026-2032 年 界面活性劑市場分析及預測(至2035年):類型、產品、應用、劑型、材料類型、技術、最終用戶、功能、製程、解決方案

界面活性劑市場分析及預測(至2035年):類型、產品、應用、劑型、材料類型、技術、最終用戶、功能、製程、解決方案