|

市場調查報告書

商品編碼

2071331

2026 年至 2035 年聚合物界面活性劑市場的商業機會、成長要素、產業趨勢與預測。Polymeric Surfactants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

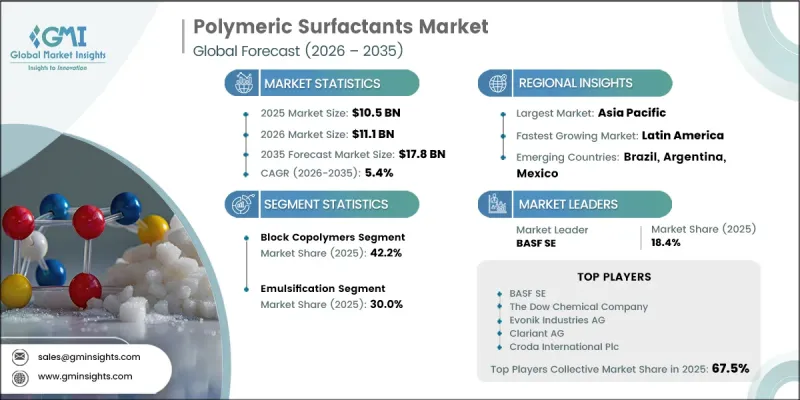

全球聚合物基界面活性劑市場預計到 2025 年將達到 105 億美元,年複合成長率為 5.4%,到 2035 年將達到 178 億美元。

市場成長的驅動力在於各工業領域持續向環保配方技術轉型。在塗料、油漆、個人保健產品和工業應用領域,水性及低揮發性有機化合物(VOC)系統正日益取代傳統的溶劑型配方,從而帶動了對先進聚合物界面活性劑的需求成長。這些材料在提升現代產品系統的配方穩定性、性能和相容性方面發揮著至關重要的作用。需求趨勢日益多元化,高性能聚合物界面活性劑在工業和技術應用領域備受關注,而生物基和永續性配方在消費市場也持續擴張。個人護理和化妝品行業仍然是最具吸引力的成長領域之一,這主要得益於消費者對質地、穩定性和感官特性更佳的高級產品的偏好。此外,聚合物界面活性劑在需要增強介面控制、提高效率和最佳化配方性能的特殊工業流程中也變得越來越重要。隨著監管要求的不斷演變和永續性目標的日益重要,製造商正擴大將聚合物基界面活性劑納入其下一代產品開發策略。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 105億美元 |

| 預測金額 | 178億美元 |

| 複合年成長率 | 5.4% |

預計到2025年,嵌段共聚物將佔據42.2%的市場佔有率,成為領先的產品類型。其強大的市場地位源自於對分子結構和雙親性性質的精確控制,使配方開發人員能夠針對特定應用最佳化性能。由於其多功能性、穩定性以及與多種系統的相容性,這些材料被廣泛應用於塗料、製藥、農業、工業加工和個人保健產品配方中。預計在整個預測期內,對高性能配方的持續需求將支撐該細分市場的持續成長。

預計到2025年,乳化領域將佔據30%的市場。這一主導地位歸功於聚合物界面活性劑在穩定複雜配方和維持產品長期性能方面發揮的關鍵作用。有效的乳化穩定性在眾多行業中至關重要,包括塗料、農產品、個人護理配方和特殊化學品。聚合物界面活性劑形成持久界面結構和增強配方一致性的能力在先進的乳化應用中仍然不可或缺。

預計到2025年,北美聚合物界面活性劑市佔率將達到27.7%。這一強勁的需求主要得益於環保配方日益普及、產品性能要求不斷提高以及排放和化學品使用法規的日益嚴格。該地區的製造商持續投資於低VOC和水性產品的研發,從而持續推動了對先進表面活性劑技術的需求。預計在預測期內,塗料、個人保健產品和工業組合藥物的持續創新將進一步加速該地區的市場成長。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 市場機遇

- 成長潛力分析

- 監理情勢

- 波特的分析

- PESTLE分析

- 價格趨勢

- 按地區

- 按類型

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

- 專利趨勢

- 貿易統計

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- LATAM

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依聚合物結構分類,2022-2035年

- 嵌段共聚物

- 接枝共聚物

- 無規/統計共聚物(聚吸附劑)

- 複合結構

第6章 市場估計與預測:依應用領域分類,2022-2035年

- 乳化

- 分配和穩定

- 潤濕並塗抹

- 發泡抑制

- 打掃

第7章 市場估計與預測:依最終用戶產業分類,2022-2035年

- 油漆和塗料

- 個人護理化妝品

- 居家護理和清潔劑

- 紡織品和皮革

- 農業

- 聚合物和塑膠製造

- 油田化學品

- 製藥

- 其他

第8章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- UAE

- 其他中東和非洲國家

第9章:公司簡介

- ADEKA Corporation

- Akzo Nobel NV

- BASF SE

- Clariant AG

- Colonial Chemical, Inc.

- Croda International Plc

- Evonik Industries AG

- Huntsman International LLC

- Kao Corporation

- Lubrizol Corporation

- Nouryon(formerly AkzoNobel Specialty Chemicals)

- Sasol Limited

- Solvay SA

- Stepan Company

- The Dow Chemical Company

- Wacker Chemie AG

The Global Polymeric Surfactants Market was valued at USD 10.5 billion in 2025 and is estimated to grow at a CAGR of 5.4% to reach USD 17.8 billion by 2035.

Market growth is supported by the ongoing transition toward environmentally responsible formulation technologies across a wide range of industries. Water-based and low-volatile organic compound (VOC) systems are increasingly replacing traditional solvent-based formulations in coatings, paints, personal care products, and industrial applications, creating strong demand for advanced polymeric surfactants. These materials play a critical role in improving formulation stability, performance, and compatibility within modern product systems. Demand patterns are becoming increasingly diversified, with high-performance polymeric surfactants gaining traction in industrial and technical applications, while bio-based and sustainability-focused formulations continue to expand across consumer-oriented markets. The personal care and cosmetics industry remains one of the most attractive growth areas, driven by increasing consumer preference for premium products offering improved texture, stability, and sensory performance. In addition, polymeric surfactants are gaining importance in specialized industrial processes that require enhanced interfacial control, efficiency improvements, and optimized formulation characteristics. As regulatory requirements continue to evolve and sustainability objectives become more prominent, manufacturers are increasingly incorporating polymeric surfactants into next-generation product development strategies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $10.5 Billion |

| Forecast Value | $17.8 Billion |

| CAGR | 5.4% |

Block copolymers accounted for 42.2% share in 2025, making them the leading product category. Their strong market position is attributed to their ability to provide precise control over molecular structure and amphiphilic properties, enabling formulators to tailor performance for specific applications. These materials are widely utilized across coatings, pharmaceuticals, agriculture, industrial processing, and personal care formulations due to their versatility, stability, and compatibility with a broad range of systems. Continued demand for high-performance formulations is expected to support sustained growth within this segment throughout the forecast period.

The emulsification segment held a 30% share in 2025. The segment's leadership is driven by the critical role polymeric surfactants play in stabilizing complex formulations and maintaining long-term product performance. Effective emulsion stability is essential across numerous industries, including coatings, agricultural products, personal care formulations, and specialty chemicals. The ability of polymeric surfactants to create durable interfacial structures and enhance formulation consistency continues to make them indispensable in advanced emulsification applications.

North America Polymeric Surfactants Market accounted for 27.7% share in 2025. Strong demand is supported by increasing adoption of environmentally compliant formulations, evolving product performance requirements, and stringent regulations governing emissions and chemical usage. Manufacturers throughout the region continue to invest in low-VOC and water-based product development, creating sustained demand for advanced surfactant technologies. Ongoing innovation in coatings, personal care products, and industrial formulations is expected to further strengthen regional market growth over the forecast period.

Major companies operating in the global polymeric surfactants market include BASF SE, Clariant AG, Croda International Plc, Evonik Industries AG, Solvay S.A., The Dow Chemical Company, Lubrizol Corporation, Stepan Company, ADEKA Corporation, Akzo Nobel N.V., Colonial Chemical, Inc., Huntsman International LLC, Kao Corporation, Nouryon, Sasol Limited, and Wacker Chemie AG. Companies operating in the polymeric surfactants market are pursuing multiple strategies to strengthen their competitive position and expand their market presence. Product innovation remains a primary focus, with manufacturers investing heavily in research and development to create high-performance, sustainable, and application-specific surfactant solutions. Many companies are expanding their portfolios of bio-based and environmentally friendly products to align with evolving regulatory requirements and customer sustainability goals. Strategic partnerships, acquisitions, and collaborations are also being utilized to enhance technological capabilities and broaden geographic reach. In addition, market participants are increasing investments in advanced manufacturing technologies to improve production efficiency and product consistency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Polymer Architecture

- 2.2.3 Application

- 2.2.4 End user industry

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Polymer Architecture, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Block copolymers

- 5.3 Graft copolymers

- 5.4 Random/statistical copolymers (Polysoaps)

- 5.5 Complex architectures

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Emulsification

- 6.3 Dispersion & stabilization

- 6.4 Wetting & spreading

- 6.5 Foam control

- 6.6 Detergency & cleaning

Chapter 7 Market Estimates and Forecast, By End User Industry, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Paints & coatings

- 7.3 Personal care & cosmetics

- 7.4 Home care & detergents

- 7.5 Textiles & leather

- 7.6 Agriculture

- 7.7 Polymer & plastics manufacturing

- 7.8 Oilfield chemicals

- 7.9 Pharmaceuticals

- 7.10 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 ADEKA Corporation

- 9.2 Akzo Nobel N.V.

- 9.3 BASF SE

- 9.4 Clariant AG

- 9.5 Colonial Chemical, Inc.

- 9.6 Croda International Plc

- 9.7 Evonik Industries AG

- 9.8 Huntsman International LLC

- 9.9 Kao Corporation

- 9.10 Lubrizol Corporation

- 9.11 Nouryon (formerly AkzoNobel Specialty Chemicals)

- 9.12 Sasol Limited

- 9.13 Solvay S.A.

- 9.14 Stepan Company

- 9.15 The Dow Chemical Company

- 9.16 Wacker Chemie AG

南美洲界面活性劑市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)

南美洲界面活性劑市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年) 界面活性劑市場:依產品、原料、功能及應用分類-2026-2032年全球市場預測界面活性劑提高採收率市場:按類型、來源、技術、分類、功能和應用分類-2026-2032年全球市場預測

界面活性劑市場:依產品、原料、功能及應用分類-2026-2032年全球市場預測界面活性劑提高採收率市場:按類型、來源、技術、分類、功能和應用分類-2026-2032年全球市場預測 肺表面活性劑市場:按類型、藥物類型、適應症、給藥途徑、分銷管道和地區分類

肺表面活性劑市場:按類型、藥物類型、適應症、給藥途徑、分銷管道和地區分類 全球表面活性劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球無 PFAS 陰離子界面活性劑市場(按最終用途產業、產品類型、應用、形態、通路、原料來源和產業鏈長度分類)預測(2026-2032 年)全球無 PFAS 離子界面活性劑市場(按產品類型、物理形態、應用、分銷管道和終端用戶行業分類)預測(2026-2032 年)全球無 PFAS 非離子界面活性劑市場(按類型、形態、應用和分銷管道分類)預測(2026-2032 年)油田水泥防沉劑市場按類型、井型、幾何形狀、技術、壓力等級、應用和終端用戶分類,全球預測,2026-2032年溶劑型無 PFAS 界面活性劑市場按功能、產品等級、包裝、銷售管道和應用分類 - 全球預測,2026-2032 年

全球表面活性劑市場規模、佔有率、趨勢和成長分析報告(2026-2034年)全球無 PFAS 陰離子界面活性劑市場(按最終用途產業、產品類型、應用、形態、通路、原料來源和產業鏈長度分類)預測(2026-2032 年)全球無 PFAS 離子界面活性劑市場(按產品類型、物理形態、應用、分銷管道和終端用戶行業分類)預測(2026-2032 年)全球無 PFAS 非離子界面活性劑市場(按類型、形態、應用和分銷管道分類)預測(2026-2032 年)油田水泥防沉劑市場按類型、井型、幾何形狀、技術、壓力等級、應用和終端用戶分類,全球預測,2026-2032年溶劑型無 PFAS 界面活性劑市場按功能、產品等級、包裝、銷售管道和應用分類 - 全球預測,2026-2032 年