|

市場調查報告書

商品編碼

2063635

亞太地區建築和拆除廢棄物管理:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Asia-Pacific Construction And Demolition Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

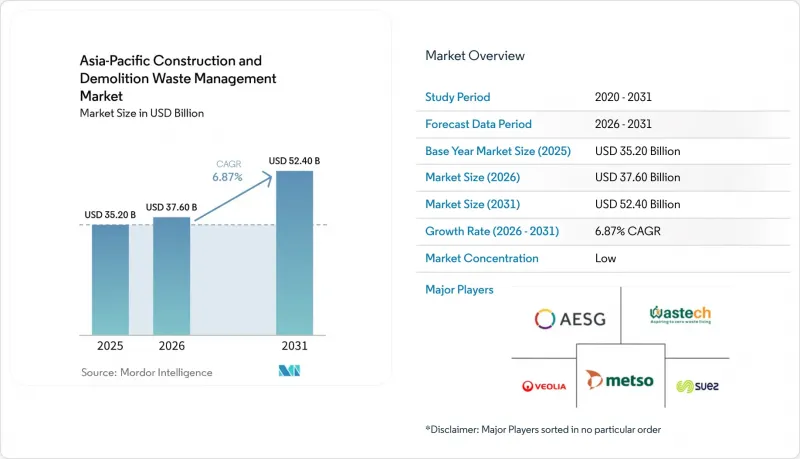

據 Mordor Intelligence 稱,亞太地區建築和拆除廢棄物管理市場在 2025 年的價值為 352 億美元,預計到 2031 年將達到 524 億美元,而 2026 年為 376 億美元,預測期(2026-2031 年)的複合年成長率為 6.87%。

本報告廢棄物廢棄物類型(非危險廢棄物和危險廢棄物)、材料(混凝土、磚塊、瀝青等)、服務(收集和運輸、分類和分離等)以及地區(中國、日本、印度、韓國、東協、澳洲和其他亞太地區)進行分類。預測以美元計價。

亞太地區建築和拆除廢棄物管理市場的趨勢和見解。

快速的都市化和大規模基礎設施建設

隨著亞洲城市的發展,大量的拆除垃圾、挖土和維修廢棄物不斷產生。這種成長推動了亞太地區建築和拆除廢棄物管理市場對專業廢棄物管理服務的需求。主要經濟體的政府正鼓勵廢棄物產生者確保垃圾分類和可追溯運輸,並推行相關政策項目。這一轉變凸顯了數位化工具和現場處理日益重要的角色。在中國,新的建築廢棄物管理法規強調源頭分類和專案期間的材料再利用。這種方法將施工進度與回收目標掛鉤,並透過多部門聯合執法防止非法傾倒。設定再利用目標和監測要求,促使企業擴大採用行動式破碎分類設備和精密分類方法。這些措施減少了長途運輸,並有助於振興再生材料市場。隨著城市化進程的加速和運作中現場准入的受限,模組化設備和分階段物流變得越來越普遍。這些解決方案有助於將材料從現場快速運送到指定的收集中心。這一轉變意味著,中國收集、分類和回收系統的擴展現在與國家和地方平台支援的即時監控聯繫起來。

政府的循環經濟與零廢棄物政策

到2030年,中國中央和地方政府的目標是實現固態廢棄物的綜合利用和建築廢棄物管理的規範化。這些努力將推動對回收、分類和可追溯運輸等服務的長期需求。國務院的《2025年行動計畫》及其操作指南強調建築廢棄物的分類和處理,推廣綠色建築實踐,並強制要求將減少廢棄物的成本納入專案預算。同時,越南的《國家循環經濟行動計畫》旨在提高回收率,並透過在建材產業建立生產者延伸責任制來加強分類和下游加工。在中國,私人企業正與地方政府合作,推出用於監測廢棄物流入和流出並最佳化回收的數位化平台。這些合作正在為再利用和產品轉換率樹立新的標準。在台灣,跨部門合作正在加強無機資源的回收利用,並將其重新用於瀝青骨材和低強度可控材料等用途。這不僅確保了建築業對回收材料的最終利用,還有助於更好地協調監管目標、公共採購和技術應用。這些合作努力正在加強亞太地區的建築和拆除廢棄物管理市場。

開發中國家監管執法方面的不足

在一些新興市場,建築廢棄物法規和許可要求的執行力度不均,可能限制廢棄物分流,並延緩對先進回收生產線的投資。儘管相關部門已開始透過聯合檢查、電子文件和處罰等方式加強監管,但在一些省市,法規的持續有效執行仍然是一項挑戰。中國近期發布的指南正式界定了建築廢棄物的跨部門執法架構,以及監測系統和電子運單的使用,展現了數位化管治如何能夠遏制垃圾傾倒並提高合規性。數位化追蹤不足可能導致收集和運輸初期環節出現漏洞,造成高價值分類材料的回收率降低,並對資源回收業者的獲利能力帶來壓力。隨著監管機構擴大審計範圍並規範報告流程,私人服務供應商將更容易調整其處理能力以適應政策方向,並獲得長期合約。監測和執法工作的持續推進將有助於實現資源回收目標,並降低亞太地區建築和拆除廢棄物管理市場非法傾倒垃圾的風險。

細分市場分析

到2025年,非危險廢棄物將佔據市場主導地位,佔有率高達98.3%。這一主導地位主要由拆除和維修活動產生的混凝土、磚塊、土壤、瀝青和木材等材料推動,並持續影響亞太地區建築和拆除廢棄物管理市場的投資重點。一項針對日本城市的調查顯示,混凝土塊是非危險廢棄物流中佔比最大的部分。此外,系統化的分類技術正在提高骨材、金屬和木材的回收率。擁有專用破碎設施的公共機構案例表明,上游工程中的高品質分類能夠使混凝土和岩石被回收利用,作為基礎設施和掩埋項目的改良路堤材料。然而,這些回收途徑依賴高效的物流管理和品質保證流程,以驗證顆粒大小、污染物和性能標準。現場移動預處理為非危險廢棄物流提供了顯著優勢,縮短了運輸距離,並確保下游工廠原料粒度的一致性。這些效率的提高將促進亞太地區的建築和拆除廢棄物管理市場的發展,使收集、分類和大規模回收與政策主導的利用目標保持一致。

2025年,危險廢棄物僅佔市場佔有率的1.7%,但預計到2031年將以7.1%的複合年成長率穩定成長。這一成長主要得益於亞太地區建築和拆除廢棄物管理市場對石棉、含鉛塗料和污染土壤等材料的監管日益嚴格。區域監管機構正在收緊石棉處理方面的法規,部分地區已全面禁止使用石棉,並要求將其移除、運輸和處置交給持有執照的承包商。印尼衛生部門強調了這個問題,指出含石棉材料的持續使用及其帶來的公共衛生挑戰,並強調未來需要更嚴格的法規和專門的處置設施。在監管嚴格的市場中,清晰的標籤、監管鏈管理以及專用的掩埋場和處理流程等做法已成為標準做法。隨著監管力度加大和執法日益嚴格,危險廢棄物數量的識別和適當處理途徑的指導不斷完善,安全性不斷提高,與非危險廢物處理管線的交叉污染也得到最大限度的減少。這些措施不僅有助於提高合規性,也將為亞太地區建築和拆除廢棄物管理市場的專業服務拓展更多機會。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 快速的都市化和大規模基礎設施建設

- 政府的循環經濟與零廢棄物政策

- 成熟市場中老舊建築的拆除

- 非法傾倒垃圾造成環境污染的擔憂

- 智慧城市中的永續廢棄物整合

- 高密度都市區天然骨材短缺

- 市場限制因素

- 開發中國家監管執法方面的不足

- 低廉的處置費用會促使人們將掩埋掩埋。

- 新興國家缺乏回收基礎設施

- 文化上偏好原生材料

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 澳洲和日本在機器人分類領域的技術領先地位

- 循環經濟與物質流分析

- 移動式回收裝置,可現場使用,以降低運輸成本

- 環境和生命週期評估考慮因素

第5章 市場規模與成長預測

- 廢棄物類型

- 無害廢棄物

- 危險廢棄物

- 材料

- 混凝土磚

- 瀝青

- 金屬

- 木頭

- 沉澱

- 石膏板/乾牆

- 其他材質(塑膠、木材、玻璃)

- 按服務

- 收集和運輸

- 分類和分離

- 回收和資源回收

- 掩埋和廢物處理

- 按地區

- 中國

- 日本

- 印度

- 韓國

- 東協(印尼、泰國、菲律賓、馬來西亞、越南)

- 澳洲

- 其他亞太國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- AESG

- Wastech

- Veolia

- Metso

- SUEZ Asia

- Bingo Industries

- Remondis Australia

- Shanghai Environment Group

- Tapbo Environmental Limited

- Bhangarwala Waste Management Pvt Ltd

- Terreco Resources

- Fieldmans Waste Management

- Ward Demolition

- Cleanaway Waste Management

- China Tianying Inc.(CNTY)

- Advanced Construction Technologies(P)Ltd

- Re Sustainability

- IL&FS Offices

- Saahas Zero Waste

- JM Ecotech Solutions Co.

第7章 市場機會與未來展望

According to Mordor Intelligence, the asia-Pacific construction and demolition waste management market size was valued at USD 35.20 billion in 2025 and is estimated to grow from USD 37.60 billion in 2026 to reach USD 52.40 billion by 2031, at a CAGR of 6.87% during the forecast period (2026-2031).

This report is Segmented by Waste Type (Non-Hazardous Waste, and Hazardous Waste), by Material (Concrete & Bricks, Asphalt, and More), by Service (Collection & Transportation, Sorting & Segregation, and More), and by Geography (China, Japan, India, South Korea, ASEAN, Australia, and Rest of Asia-Pacific). Forecasts are Provided in Terms of Value in USD.

Asia-Pacific Construction And Demolition Waste Management Market Trends and Insights

Rapid Urbanization and Mega Infrastructure Development

Urban growth across Asia is producing large amounts of demolition debris, excavation soil, and renovation waste. This increase is boosting the need for proper waste management services in the Asia-Pacific Construction and Demolition Waste Management market. Governments in major economies are encouraging waste producers to sort materials and ensure traceable transport, driven by policy-backed projects. This shift highlights the rising role of digital tools and on-site processing. In China, new rules for managing construction waste focus on sorting at the source and reusing materials during projects. This approach connects construction progress with recycling goals and uses multi-agency enforcement to prevent illegal dumping. By setting reuse targets and monitoring requirements, businesses are finding more reasons to adopt mobile crushing, screening, and precise sorting methods. These practices cut down on long-distance transport and support markets for recycled materials. As cities grow denser, limited access to active sites is making modular equipment and phased logistics more popular. These solutions help move materials quickly from job sites to approved recovery centers. This shift is aligning the growth of collection, sorting, and recycling systems with real-time monitoring, supported by national and local platforms in China.

Government Circular Economy and Zero Waste Policies

By 2030, Chinese central and municipal authorities aim to comprehensively utilize bulk solid waste and standardize construction waste governance. These initiatives bolster the long-term demand for services like recycling, sorting, and traceable hauling. The State Council's 2025 action plan, along with its operational guidance, emphasizes the classified treatment of construction waste, promotes green construction practices, and mandates the integration of waste reduction costs into project budgets. Meanwhile, Vietnam's national circular economy action plan aims for high collection rates and formalizes extended producer responsibility in sectors linked to building materials, enhancing segregation and downstream processing. In China, corporate operators are collaborating with local governments to launch digital platforms that monitor waste inflows and outflows, optimizing recovery. These collaborations establish new benchmarks for reuse rates and product conversion. Taiwan is witnessing cross-sector initiatives that enhance the recovery of inorganic resources, repurposing them for uses like asphalt aggregates and controlled low-strength material. This not only stabilizes end-use outlets for recycled content in construction but also tightens the alignment between regulatory targets, public procurement, and technology adoption. Such concerted efforts fortify the Asia-Pacific Construction and Demolition Waste Management market.

Weak Regulatory Enforcement in Developing Nations

In several emerging markets, uneven enforcement of construction waste rules and licensing requirements can limit diversion and slow investment in advanced recovery lines. Authorities have started to strengthen oversight through joint inspections, electronic documentation, and penalties, but consistent implementation remains a work in progress in some provinces and municipalities. China's recent guidance formalizes inter-departmental enforcement and the use of surveillance and e-waybills for construction waste, which illustrates how digital governance can curb leakage and improve compliance. Where digital tracking is not fully deployed, gaps may persist in first-mile collection and transfer, which reduces the capture of higher-value fractions and constrains revenues for material recovery operators. As regulators expand audits and standardize reporting, private service providers can better align capacity with policy direction and secure long-term contracts. Continued progress in monitoring and enforcement will support recovery targets and reduce illicit dumping risk in the Asia-Pacific Construction and Demolition Waste Management market.

Other drivers and restraints analyzed in the detailed report include:

- Aging Building Stock Demolition in Mature Markets

- Environmental Pollution Concerns from Illegal Dumping

- Low Tipping Fees Favoring Landfill Disposal

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, non-hazardous waste dominated the scene, capturing a 98.3% share. This dominance, driven by materials like concrete, brick, soil, asphalt, and timber from demolition and renovation activities, continues to shape investment priorities in the Asia-Pacific Construction and Demolition Waste Management market. Assessments in Japanese cities reveal that concrete blocks lead the non-hazardous stream. Moreover, structured separation techniques boost yields for aggregates, metals, and wood. Public agencies with dedicated crushing capacities have shown that, with high-quality upstream sorting, concrete and rock can be recycled into engineered fill for infrastructure and reclamation projects. However, these recycling pathways hinge on efficient logistics management and quality assurance processes that check for gradation, contaminants, and performance standards. Mobile pre-processing at sites offers significant advantages for non-hazardous streams, cutting down haul distances and ensuring a consistent feedstock size for downstream plants. Such efficiencies bolster the Asia-Pacific Construction and Demolition Waste Management market, aligning collection, sorting, and high-volume recycling with policy-driven utilization goals.

While hazardous waste made up a mere 1.7% share in 2025, it's set to grow at a robust 7.1% CAGR through 2031. This growth is largely due to heightened enforcement on materials like asbestos, lead-based coatings, and contaminated soils in the Asia-Pacific Construction and Demolition Waste Management market. Regional regulators have tightened asbestos handling rules, with some areas outright banning it and mandating licensed contractors for its removal, transport, and disposal. Highlighting the issue, health authorities in Indonesia have pointed out the ongoing use of asbestos-containing materials and the resultant public health challenges, bolstering the case for future restrictions and the need for specialized disposal facilities. In markets with stringent compliance, practices like clear labeling, chain-of-custody controls, and dedicated landfill cells or treatment routes have become the norm. As monitoring intensifies and enforcement tightens, the identification and routing of hazardous waste volumes improve, enhancing safety and minimizing cross-contamination with non-hazardous processing lines. Such measures not only boost compliance but also open doors for specialized services in the Asia-Pacific Construction and Demolition Waste Management market.

List of Companies Covered in this Report:

- AESG

- Wastech

- Veolia

- Metso

- SUEZ Asia

- Bingo Industries

- Remondis Australia

- Shanghai Environment Group

- Tapbo Environmental Limited

- Bhangarwala Waste Management Pvt Ltd

- Terreco Resources

- Fieldmans Waste Management

- Ward Demolition

- Cleanaway Waste Management

- China Tianying Inc. (CNTY)

- Advanced Construction Technologies (P) Ltd

- Re Sustainability

- IL&FS Offices

- Saahas Zero Waste

- JM Ecotech Solutions Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Urbanization and Mega Infrastructure Development

- 4.2.2 Government Circular Economy and Zero Waste Policies

- 4.2.3 Aging Building Stock Demolition in Mature Markets

- 4.2.4 Environmental Pollution Concerns from Illegal Dumping

- 4.2.5 Smart City Sustainable Waste Integration

- 4.2.6 Natural Aggregate Shortages in Dense Urban Areas

- 4.3 Market Restraints

- 4.3.1 Weak Regulatory Enforcement in Developing Nations

- 4.3.2 Low Tipping Fees Favoring Landfill Disposal

- 4.3.3 Limited Recycling Infrastructure in Emerging Economies

- 4.3.4 Cultural Preference for Virgin Materials

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Australia-Japan Technology Leadership in Robotic Sorting

- 4.9 Circular Economy & Material Flow Analysis

- 4.10 On-site mobile recycling units reducing transportation costs

- 4.11 Environmental & Life-Cycle Assessment Considerations

5 Market Size & Growth Forecasts (value USD)

- 5.1 By Waste Type

- 5.1.1 Non-Hazardous Waste

- 5.1.2 Hazardous Waste

- 5.2 By Material

- 5.2.1 Concrete & Bricks

- 5.2.2 Asphalt

- 5.2.3 Metal

- 5.2.4 Timber

- 5.2.5 Soil and Sand

- 5.2.6 Gypsum & Drywall

- 5.2.7 Others (Plastic, Wood, Glass)

- 5.3 By Service

- 5.3.1 Collection & Transportation

- 5.3.2 Sorting & Segregation

- 5.3.3 Recycling & Material Recovery

- 5.3.4 Landfilling & Disposal

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 South Korea

- 5.4.5 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.4.6 Australia

- 5.4.7 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 AESG

- 6.4.2 Wastech

- 6.4.3 Veolia

- 6.4.4 Metso

- 6.4.5 SUEZ Asia

- 6.4.6 Bingo Industries

- 6.4.7 Remondis Australia

- 6.4.8 Shanghai Environment Group

- 6.4.9 Tapbo Environmental Limited

- 6.4.10 Bhangarwala Waste Management Pvt Ltd

- 6.4.11 Terreco Resources

- 6.4.12 Fieldmans Waste Management

- 6.4.13 Ward Demolition

- 6.4.14 Cleanaway Waste Management

- 6.4.15 China Tianying Inc. (CNTY)

- 6.4.16 Advanced Construction Technologies (P) Ltd

- 6.4.17 Re Sustainability

- 6.4.18 IL&FS Offices

- 6.4.19 Saahas Zero Waste

- 6.4.20 JM Ecotech Solutions Co.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

建築和拆除廢棄物管理市場-全球產業規模、佔有率、趨勢、機會和預測:按材料、來源、服務、最終用戶、地區和競爭格局分類,2021-2031年

建築和拆除廢棄物管理市場-全球產業規模、佔有率、趨勢、機會和預測:按材料、來源、服務、最終用戶、地區和競爭格局分類,2021-2031年 建築和拆除廢棄物回收市場預測至2034年-按廢棄物類型、來源、服務類型、設備、應用、最終用戶和地區分類的全球分析

建築和拆除廢棄物回收市場預測至2034年-按廢棄物類型、來源、服務類型、設備、應用、最終用戶和地區分類的全球分析 歐洲建築和拆除廢棄物管理:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

歐洲建築和拆除廢棄物管理:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 建築和拆除廢棄物管理市場報告:按行業、服務、廢棄物類型和地區分類(2026-2034 年)

建築和拆除廢棄物管理市場報告:按行業、服務、廢棄物類型和地區分類(2026-2034 年) 建築和拆除廢棄物市場:廢棄物類型、收集方法、處理方法、最終用途和應用分類-2026-2032年全球市場預測

建築和拆除廢棄物市場:廢棄物類型、收集方法、處理方法、最終用途和應用分類-2026-2032年全球市場預測 2026年全球建築與廢棄物廢棄物管理市場報告

2026年全球建築與廢棄物廢棄物管理市場報告 建築與拆除廢棄物管理市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034年)按材料類型、原料來源、加工技術、應用、最終用戶和通路骨材回收市場-2026-2032年全球預測全球挖掘與拆除市場:機會與策略展望(至2034年)

建築與拆除廢棄物管理市場規模、佔有率、成長及全球產業分析:依類型、應用和地區劃分的洞察與預測(2026-2034年)按材料類型、原料來源、加工技術、應用、最終用戶和通路骨材回收市場-2026-2032年全球預測全球挖掘與拆除市場:機會與策略展望(至2034年) 全球建築和拆除廢棄物管理市場

全球建築和拆除廢棄物管理市場