|

市場調查報告書

商品編碼

2063619

印度危險化學品物流:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)India Hazardous Chemical Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

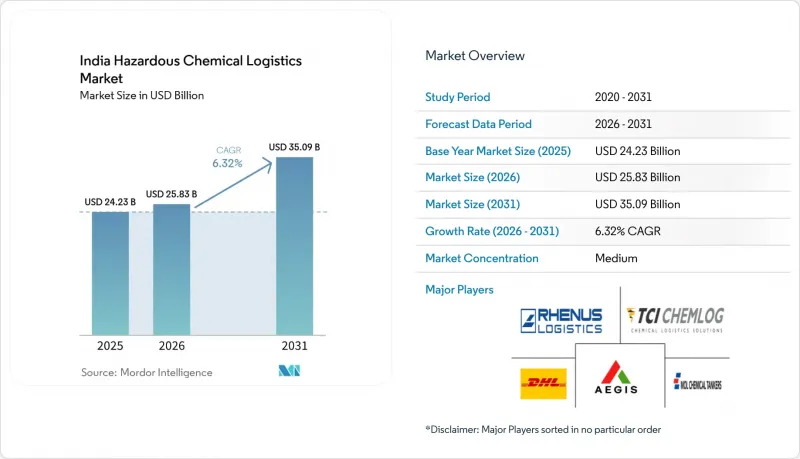

印度危險化學品物流市場預計將從 2025 年的 242.3 億美元成長到 2026 年的 258.3 億美元,到 2031 年達到 350.9 億美元,2026 年至 2031 年的複合年成長率為 6.32%。

這一成長趨勢是由多種因素共同推動的:沿海地區新建石化工廠的運作、外包合規營運需求的成長,以及多模態投資將散裝貨物的運輸方式從公路轉向管道、鐵路和內河航道。本報告按服務類型(運輸、其他)、危險化學品分類(易燃液體、壓縮氣體、腐蝕性物質、其他)、終端用戶行業(石化產品和散裝化學品、其他)以及地區(印度北部、印度南部、印度西部、印度東部、印度中部)進行細分。市場預測以美元計價。

印度危險化學品物流市場趨勢與洞察

印度化學品總產量(大宗化學品和基礎化學品)的擴張

預計到2025年,印度的化學品產量將超過2,200億美元,隨著拉賈斯坦邦和奧裡薩邦新裂解裝置的產能擴張,這一數字也將持續成長。每增加一噸苛性鈉、氯氣和甲醇,就需要使用符合PESO認證標準的油罐車、ISO貨櫃或鐵路罐車進行運輸,這導致對受監管物流服務的需求持續成長。僅印度石油公司營運的帕拉迪普-哈爾迪亞管線預計每年就能取代約1萬輛卡車的運輸量,從而釋放道路運輸能力用於運輸特殊貨物。 Aegis Logistics公司類似的管道和儲罐區擴建項目表明,隨著上游生產的成長,倉儲和運輸資產也在逐步擴張。鑑於印度人均石化產品消費量僅為全球平均的三分之一,預計運輸量的長期成長趨勢將持續下去。

特種化學品和醫藥化學品的生產迅速成長,需要符合合規要求的物流。

特種化學品和醫藥化學品需要小批量生產、更嚴格的溫度控制和即時可追溯性。古吉拉突邦和泰米爾納德邦對含氟化學品的投資,以及烏納和維沙卡帕特南新建的原料藥(API)產業園,正在為溫控運輸、重新包裝和緊急應變計劃創造一個利潤豐厚的業務領域。 Snowman 物流和 Kuehne + Nagel 已運作一座溫度控制在 15-25°C 的倉庫,該倉庫配備氣體檢測功能和批次級條碼管理系統,並因此獲得了一份為期五年的外包合約。隨著運作工廠在 24-36 個月內從試生產過渡到商業化生產,預計中期成長將十分強勁。

用於處理危險物質的車輛和倉庫需要投入大量資金和遵循成本。

符合PESO《2016年靜態和移動壓力容器法規》的不銹鋼化學品罐車造價在6萬至8.5萬美元之間,大約是標準燃料罐車價格的兩倍。此外,每輛車每年還需要6000至1萬美元用於認證、特殊保險和駕駛員培訓,因此對於小規模企業來說,更換車輛是一項資本密集型支出。倉庫自動化同樣成本高昂。 Godley公司在孟買新建的120英尺貨架倉庫需要機器人穿梭車和防爆線路,導致每平方英尺的投資超過500美元。短期來看,高昂的進入門檻限制了新增供給能力,並延緩了對激增需求的回應。

細分市場分析

到2025年,運輸業將佔印度危險化學品物流市場佔有率的64.51%,反映出該國在最後一公里配送方面對公路油輪的依賴。鐵路運輸業正在重新奪回市場佔有率, 物流的ISO罐式列車可將單位成本降低25%,並克服司機短缺的問題。儘管海運和內河航道具有明顯的成本優勢,但其利用率仍然很低。由於4號和5號國家水道的吃水限制,駁船運輸規模仍然很小。從2026年到2031年,附加價值服務,特別是混合、重新貼標和緊急應變計劃,預計將以9.52%的複合年成長率實現最高成長率,因為醫藥和特種貨物運輸公司會將合規方面的挑戰外包出去。 Snowman 在泰米爾納德邦新建的 50,000 平方英尺危險品和冷藏倉庫,以及 Kuehne + Nagel 擴建的 450,000平方公尺合約物流中心,都表明企業正在轉向高利潤的輔助服務,以降低運費波動帶來的風險。

隨著印度危險化學品安全辦公室 (PESO) 收緊倉儲監管,印度危險化學品物流市場的附加價值服務規模預計將穩步擴大。 AIS-140 遠端資訊處理技術可實現地理圍欄、預測性維護和批次級審計追蹤,從而提高了轉換的成本。大型企業正利用其專有技術堆疊整合運輸和倉儲業務,從而提高客戶維繫和單次運輸利潤率。對發泡材填充貨架和電池驅動堆高機的投資為小規模本地承運商設置了很高的進入門檻,表明行業整合正在加劇。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 印度化學品總產量(大宗化學品和基礎化學品)的擴張

- 特種化學品和藥品/化學品的生產迅速成長,需要符合合規要求的物流。

- 擴大沿海叢集的石化和煉油產能

- 對危險物品(PESO、IMDG、DG Shipping)更嚴格的規定正在推動外包需求的成長。

- 石油、化工和石化投資區(PCPIR)開發

- 開發利用內河航道走廊(NW-1、4、5)的低成本化學品運輸路線

- 市場限制因素

- 處理危險物品的車輛和倉庫需要投入高昂的資本投資成本和合規成本。

- 具備危險物品處理資格的駕駛人和搬運工嚴重短缺。

- 各州之間的法規差異正在減緩多模態的發展進程。

- 新建沿海化學品碼頭的海岸管制區審核延誤

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 地緣政治事件的影響

第5章 市場規模與成長預測

- 按服務類型分類

- 運輸

- 路

- 鐵路

- 海事/沿海和內陸水道

- 航空

- 倉儲、物流

- 附加價值服務

- 運輸

- 按類型對危險化學物質進行分類

- 易燃液體

- 壓縮氣體

- 腐蝕性物質

- 危險物質

- 氧化物質

- 放射性物質

- 其他化學品

- 最終用戶行業細分

- 石油化學產品及大宗化學品

- 特種化學品

- 製藥和生命科學

- 殺蟲劑和化肥

- 電動車的電池、電子設備和材料

- 其他行業

- 區域細分

- 印度北部

- 南印度

- 西印度群島

- 東印度

- 印度中部

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Aegis Logistics Ltd

- TCI Chemlog(Transport Corporation of India)

- Allcargo Logistics Ltd

- DHL Supply Chain India

- DSV A/S(including DB Schenker)

- Kuehne+Nagel

- Rhenus Logistics

- Snowman Logistics Ltd

- CMA CGM(Including CEVA Logistics)

- GEODIS

- Den Hartogh Logistics India

- BDP International India

- Hellmann Worldwide Logistics India

- MOL Chemical Tankers India

- Seashell Logistics Pvt. Ltd.

- Bertschi India

- TVS Supply Chain Solutions

- Hazchem Logistics Management LLP

- AWL INDIA

- Milkyway Chem Logistics India

第7章 市場機會與未來展望

According to Mordor Intelligence, india hazardous chemical logistics market size is expected to increase from USD 24.23 billion in 2025 to USD 25.83 billion in 2026 and reach USD 35.09 billion by 2031, growing at a CAGR of 6.32% over 2026-2031.

This trajectory reflects a blend of new petrochemical capacity along the coastline, rising demand for outsourced compliance services, and multimodal investments that shift bulk cargo from roads to pipelines, rail, and inland waterways. This report is Segmented by Service Type (Transportation, and Others), by Hazardous Chemical Class (Flammable Liquids, Compressed Gases, Corrosive Substances, and Others), by End-User Industry (Petrochemicals and Bulk Chemicals, and Others), and by Geography (North India, South India, West India, East India, and Central India). Market Forecasts are Provided in Terms of Value (USD).

India Hazardous Chemical Logistics Market Trends and Insights

Expansion of India's Overall Chemical Output (Bulk & Basic)

India's chemicals output reached more than USD 220 billion in 2025 and is pegged to keep rising as new crackers in Rajasthan and Odisha ramp up capacity. Each additional tonne of caustic soda, chlorine, or methanol must move in PESO-certified tankers, ISO containers, or rail rakes, driving sustained demand for compliant logistics services. Indian Oil's Paradip-Haldia pipeline alone is expected to displace roughly 10,000 annual truck trips, freeing road bandwidth for specialty cargoes. Similar pipeline and tank-farm expansions by Aegis Logistics show how storage and evacuation assets scale line by line with upstream production. The long-term volume uplift persists because India's per capita petrochemical consumption is one-third the world average.

Surge in Specialty & Pharma-Chemical Production Requiring Compliant Logistics

Specialty and pharmaceutical chemicals entail smaller lot sizes, stricter temperature bands, and real-time traceability. New active pharmaceutical ingredient (API) parks in Una and Vizag, plus fluorochemical investments in Gujarat and Tamil Nadu, create high-margin lanes for temperature-controlled trucking, repackaging, and emergency response planning. Snowman Logistics and Kuehne + Nagel are already commissioning 15-25 °C warehouses with gas detection and batch-level barcoding to win five-year outsourcing contracts. Mid-term growth remains solid as commissioned plants ramp from trial to commercial output over 24-36 months.

High CAPEX and Compliance Costs for Hazmat-Graded Fleets & Warehouses

A stainless-steel chemical tanker that meets PESO's Static & Mobile Pressure Vessels Rules 2016 costs USD 60,000-85,000, roughly double a standard fuel tanker. Annual certifications, specialized insurance, and driver training add another USD 6,000-10,000 per vehicle, making fleet renewal a capital-intensive exercise for small operators. Warehouse automation is equally pricey: Godrej's new 120-foot rack-clad store in Mumbai required robotic shuttles and explosion-proof wiring, pushing investment past USD 500 per square foot. In the short run, high entry costs curb fresh capacity and slow response to demand spikes.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Petrochemical and Refining Capacity Across Coastal Clusters

- Stricter Hazardous-Materials Rules (PESO, IMDG, DG Shipping) Raising Outsourcing Demand

- Acute Shortage of HAZMAT-Certified Drivers and Handlers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation accounted for 64.51% of the India hazardous chemical logistics market share in 2025, reflecting the country's reliance on road tankers for last-mile delivery. Rail is regaining ground as AVG Logistics' ISO-tank trains cut unit costs by 25% and bypass driver shortages. Sea and inland waterways remain underpenetrated despite clear cost advantages; draft limits on National Waterways 4 and 5 keep barge sizes small. Over 2026-2031, value-added services, led by blending, relabeling, and emergency-response planning, will post the fastest 9.52% CAGR as pharma and specialty shippers outsource compliance headaches. Snowman's new 50,000 sq ft hazmat-cold store in Tamil Nadu and Kuehne+Nagel's expanded 450,000 m2 contract-logistics footprint show providers pivoting toward high-margin ancillary work that cushions rate volatility.

The India hazardous chemical logistics market size for value-added services is forecast to advance steadily as PESO tightens warehouse rules. AIS-140 telematics unlock geo-fencing, predictive maintenance, and batch-level audit trails, thereby raising switching costs. Bigger players leverage captive tech stacks to bundle transport with warehousing, thus improving retention and margin per load. Investments in foam-suppressed racks and battery-powered forklifts set entry barriers that small regional carriers struggle to cross, signaling ongoing consolidation.

List of Companies Covered in this Report:

- Aegis Logistics Ltd

- TCI Chemlog (Transport Corporation of India)

- Allcargo Logistics Ltd

- DHL Supply Chain India

- DSV A/S (including DB Schenker)

- Kuehne+Nagel

- Rhenus Logistics

- Snowman Logistics Ltd

- CMA CGM (Including CEVA Logistics)

- GEODIS

- Den Hartogh Logistics India

- BDP International India

- Hellmann Worldwide Logistics India

- MOL Chemical Tankers India

- Seashell Logistics Pvt. Ltd.

- Bertschi India

- TVS Supply Chain Solutions

- Hazchem Logistics Management LLP

- AWL INDIA

- Milkyway Chem Logistics India

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of India's Overall Chemical Output (Bulk and Basic)

- 4.2.2 Surge in Specialty and Pharma-Chemical Production Requiring Compliant Logistics

- 4.2.3 Expansion of Petrochemical and Refining Capacity Across Coastal Clusters

- 4.2.4 Stricter Hazardous-Materials Rules (PESO, IMDG, DG Shipping) Raising Outsourcing Demand

- 4.2.5 Development of Petroleum, Chemicals and Petrochemicals Investment Regions (PCPIRs)

- 4.2.6 Inland-Waterway Corridors (NW-1, 4, 5) Opening Low-Cost Chemical Routes

- 4.3 Market Restraints

- 4.3.1 High CAPEX and Compliance Costs for Hazmat-Graded Fleets and Warehouses

- 4.3.2 Acute Shortage of HAZMAT-Certified Drivers and Handlers

- 4.3.3 State-Wise Regulatory Fragmentation Slowing Multimodal Transfers

- 4.3.4 CRZ Clearance Delays for New Coastal Chemical Terminals

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Geo-Political Events

5 Market Size and Growth Forecasts (Value)

- 5.1 Segmentation by Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Rail

- 5.1.1.3 Sea / Coastal and Inland Waterways

- 5.1.1.4 Air

- 5.1.2 Storage, Warehousing and Distribution

- 5.1.3 Value Added Services

- 5.1.1 Transportation

- 5.2 Segmentation by Hazardous Chemical Class

- 5.2.1 Flammable Liquids

- 5.2.2 Compressed Gases

- 5.2.3 Corrosive Substances

- 5.2.4 Toxic Substances

- 5.2.5 Oxidizing Substances

- 5.2.6 Radioactive Materials

- 5.2.7 Other Chemicals

- 5.3 Segmentation by End-User Industry

- 5.3.1 Petrochemicals and Bulk Chemicals

- 5.3.2 Specialty Chemicals

- 5.3.3 Pharmaceuticals and Life Sciences

- 5.3.4 Agrochemicals and Fertilizers

- 5.3.5 Batteries, Electronics and EV Materials

- 5.3.6 Other Industries

- 5.4 Segmentation by Region

- 5.4.1 North India

- 5.4.2 South India

- 5.4.3 West India

- 5.4.4 East India

- 5.4.5 Central India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Aegis Logistics Ltd

- 6.4.2 TCI Chemlog (Transport Corporation of India)

- 6.4.3 Allcargo Logistics Ltd

- 6.4.4 DHL Supply Chain India

- 6.4.5 DSV A/S (including DB Schenker)

- 6.4.6 Kuehne+Nagel

- 6.4.7 Rhenus Logistics

- 6.4.8 Snowman Logistics Ltd

- 6.4.9 CMA CGM (Including CEVA Logistics)

- 6.4.10 GEODIS

- 6.4.11 Den Hartogh Logistics India

- 6.4.12 BDP International India

- 6.4.13 Hellmann Worldwide Logistics India

- 6.4.14 MOL Chemical Tankers India

- 6.4.15 Seashell Logistics Pvt. Ltd.

- 6.4.16 Bertschi India

- 6.4.17 TVS Supply Chain Solutions

- 6.4.18 Hazchem Logistics Management LLP

- 6.4.19 AWL INDIA

- 6.4.20 Milkyway Chem Logistics India

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

化學物質濃度監測儀市場:按類型、測量介質、輸送方式、產品類型、技術、最終用途、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

化學物質濃度監測儀市場:按類型、測量介質、輸送方式、產品類型、技術、最終用途、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 危險品包裝市場規模、佔有率、成長、產業分析和預測:按材料、產品類型、最終用戶和地區分類(至2034年)化學測量儀器市場:依產品類型、技術、組件、最終用途產業、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測

危險品包裝市場規模、佔有率、成長、產業分析和預測:按材料、產品類型、最終用戶和地區分類(至2034年)化學測量儀器市場:依產品類型、技術、組件、最終用途產業、國家及地區分類-產業分析、市場規模、市場佔有率及2026年至2033年預測 2026年全球危險物品物流市場報告

2026年全球危險物品物流市場報告 煙霧密度監測儀市場按產品類型、技術、應用、最終用戶、連接方式和分銷管道分類,全球預測(2026-2032年)2026年全球化學測量儀器市場報告

煙霧密度監測儀市場按產品類型、技術、應用、最終用戶、連接方式和分銷管道分類,全球預測(2026-2032年)2026年全球化學測量儀器市場報告 危險品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

危險品物流:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球化學濃度監測儀市場按介質、產品、技術、終端用戶產業和地區分類-預測至2030年

全球化學濃度監測儀市場按介質、產品、技術、終端用戶產業和地區分類-預測至2030年 全球危險品物流市場

全球危險品物流市場 危險品物流市場-全球產業規模、佔有率、趨勢、機會及預測(按服務、應用、產品類型、地區、競爭細分,2020-2030 年)

危險品物流市場-全球產業規模、佔有率、趨勢、機會及預測(按服務、應用、產品類型、地區、競爭細分,2020-2030 年)