|

市場調查報告書

商品編碼

2063481

翻新實驗室設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Refurbished Laboratory Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

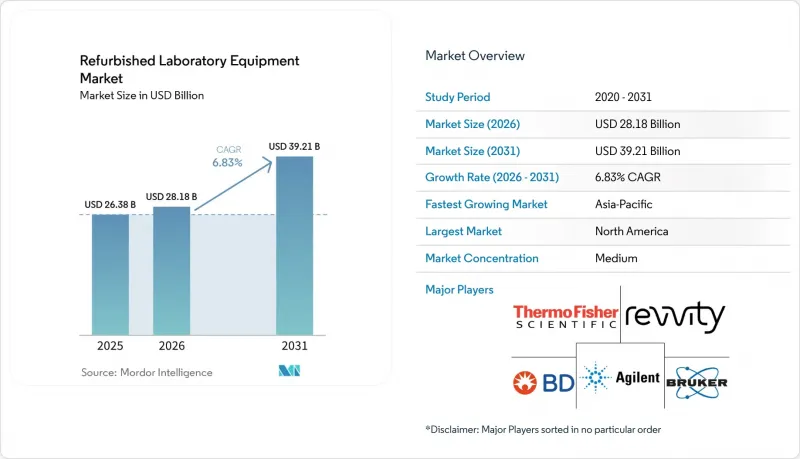

根據 Mordor Intelligence 預測,翻新實驗室設備的市場規模預計將從 2025 年的 263.8 億美元成長到 2026 年的 281.8 億美元,然後從 2026 年到 2031 年以 6.83% 的複合年成長率成長,到 2031 億美元達到 392.1 億美元。

本報告按產品類型(分析儀器、通用實驗室設備等)、最終用戶(製藥和生物技術公司等)、銷售管道(OEM認證二手設備項目等)、翻新等級(OEM工廠認證等)和地區(北美、歐洲等)進行細分。市場規模和預測均以美元計價。

全球翻新實驗室設備市場趨勢及洞察。

為預算有限的研究機構和新創企業提供經濟高效的採購方案。

對預算敏感的買家,例如學術機構、診斷實驗室和合約研究組織,正將資金從新購設備轉向經認證的翻新設備,這些設備能夠以更低的購置成本滿足其處理能力需求,從而使資金可以重新分配到耗材、人員和驗證方面。公共部門和非政府組織的採購負責人正從總體擁有成本 (TCO) 的角度做出決策,強調校準、零件供應、試劑物流和多年期服務獲取,以避免資產閒置和供應商鎖定。由於買家要求可預測的正常運作和可審計的記錄,因此能夠披露校準可追溯性和出貨前驗證的供應商正受到優先考慮。在供應方面,經過工廠檢驗並提供與新系統同等保固的認證翻新項目正在縮小新系統和翻新系統之間性能差異的感知。提供有據可查的環境影響降低和預配置啟動包的市場專家,正日益受到尋求快速運作的培養箱和早期實驗室的青睞。一個典型的例子是供應商計劃,該計劃規定使用原廠配件進行多參數測試,提供全面保障,並支援現場安裝,以支援在受監管的運作流程中合規地啟動營運。此外,注重預算的實驗室會使用可追溯至國家計量機構的校準證書檢驗供應商的說法,以保持隨時可供審計的記錄。

製藥和生物技術領域研發的擴展:對設備的需求增加

隨著生物製藥領域研發投入的活性化,液相層析-質譜聯用儀(LC-MS)、層析法系統和高內涵成像平台等設備的採用率日益提高,使其在後續的設備組合更新中符合以舊換新或認證轉售的條件。併購和設備組合重組加快了設備處置週期,高價值設備正湧入翻新和轉售管道。在許多情況下,拆卸和物流服務以打包形式提供,以減輕買方的負擔。領先的原始設備製造商(OEM)持續投資於端到端能力和夥伴關係,以加強客戶關係,並在資產生命週期內擴大已安裝設備組合的覆蓋範圍。印度的Vigyan Dhara公司正在擴大其區域安裝基礎,並透過增加研發預算和在2025-2026財政年度提供津貼補貼,在後續資金籌措週期中建立更新周期。 OEM的收購和產能擴張與生物製藥行業的需求相符,顯示設備的持續使用,並隨著客戶對其設備進行現代化改造,正在重振二級分銷管道。 ISO 13485 和 FDA 的 QMSR 要求相關的法規的協調統一,進一步規範了校準和文件記錄,提高了對回收商的要求標準,同時也增強了買家對文件記錄完善的產品和服務的信心。

由於複製標準不一致,人們對準確性、可靠性和校準存在擔憂。

校準品質仍然是一個重要問題,尤其是在那些必須滿足FDA、ISO和CLIA要求的實驗室中,這些要求依賴嚴格的測量控制,而翻新標準卻參差不齊。近期聯邦政府發布的不符合項通知經常指出校準缺陷,導致買家更加關注供應商流程中整合的可追溯性、不確定度容差和環境控制。 ISO 13485和ISO/IEC 17025框架要求提供與國家計量局相符的校準鏈記錄、明確的容差範圍,並對超出容差範圍的事件進行調查,以確保產品在整個生命週期內的品質。 FDA品質系統要求也強調了明確的校準週期和將儀器狀態與受檢批次和樣品關聯起來的記錄,要求翻新商從一開始就提供可審核的文件。 CLIA及相關指南強化了定期檢驗的觸發條件,例如試劑批次更換和維護,凸顯了為臨床工作流程中部署的翻新儀器提供可靠服務的重要性。檢查室透過對供應商進行標準化來緩解此限制,這些供應商提供可追溯至 NIST 或 BIPM 的校準證書、檢驗的軟體版本以及校準期間記錄的環境條件。

細分市場分析

2025年,分析儀器在翻新實驗室設備市場銷售額中佔42.17%。這反映了市場對貫穿藥物研發和品管(QC)工作流程的液相層析質譜聯用(LC-MS)、氣相層析(GC)和光譜分析系統的持續需求。採購團隊正擴大將最新一代儀器納入以舊換新計劃,提供經過認證的LC-MS平台,並附帶工廠檢驗記錄、韌體更新和同等保固服務。這增強了受監管應用領域對該類儀器的信心。經銷商提供長達數月的保固、可追溯的校準和安裝服務,從而提升了儀器的殘值;同時,買家也透過服務等級協議和預防性保養計劃來明確其運作預期。符合ISO 13485和ISO/IEC 17025標準的校準文件對於將翻新分析系統部署到製藥品管(QC)和臨床實驗室改進修正案(CLIA)環境中仍然至關重要,這也影響OEM認證設備和未經認證設備之間的價格差異。當實驗室淘汰舊版作業系統和軟體時,經銷商若能在出貨時提供檢驗的軟體狀態,便可減少部署阻力,加快合規性審核流程。這些因素共同鞏固了分析儀器在翻新實驗室設備市場的領先地位。

通用實驗室設備預計將成為成長最快的產品類型,到2031年將以7.43%的複合年成長率成長,這主要得益於其在學術、醫院和工業實驗室的廣泛應用。此細分市場中翻新實驗室設備市場的規模受益於離心機、培養箱、生物安全櫃、天平和液體處理系統等能夠滿足實驗室認證要求的設備快速供應。模組化自動化和永續性設備的普及進一步推動了市場需求,這些設備能夠降低能源和耗材消耗,符合循環採購的目標。經銷商透過提供廣泛的保固服務以及隨附完整的IQ/OQ/PQ測試記錄來脫穎而出,從而能夠在審核環境中快速運作運行。買家擴大選擇包含啟動套件和培訓包的翻新通用設備,以便在有限的預算內建立新的實驗室或擴大現有設施。雖然文件品質和一致性仍然是主要的選擇標準,但校對的可追溯性和清晰的服務流程正在提高決策的速度和信心。這些趨勢正在推動翻新實驗室設備市場中通用設備的持續擴張。

預計到2025年,製藥和生物技術公司將佔銷售額的32.28%,這主要得益於研發投入推動了液相層析質譜聯用(LC-MS)、層析法和高內涵成像平台在研發和品管(QC)各個階段的廣泛應用。隨著新模式的出現,藥物發現和分析領域對儀器的需求不斷成長,積極的以舊換新和升級週期為二手市場提供了大量維護良好的設備。與製藥生產和服務相關的原始設備製造商(OEM)夥伴關係,以及產能的提升,正在強化儀器從初始銷售到最終認證轉售的整個生命週期。對生物製程和分析工作流程的投資持續構成儀器應用的基礎,這些儀器隨後將以品質認證的形式進入二手實驗室儀器市場。與製藥企業買家相關的翻新實驗室儀器的市場佔有率持續受到符合審核和認證要求的等效保證和工廠驗證的支持。這些因素使得翻新儀器的應用成為非GxP環境以及特定GxP環境(需證明其文件齊全、校準可追溯且服務響應迅速)中的可行選擇。

預計到2031年,學術和研究機構將以8.56%的複合年成長率實現最快成長,這主要得益於實驗室容量的提升以及公共項目對實用基礎設施的優先發展。印度的「科學之源」(Vigyan Dhara)基金正在支持這些機構的儀器部署津貼,從而增加了對經認證的翻新系統的短期需求,並為未來的二手設備供應建立了多年更新周期。新成立的國家測量中心和產學研合作中心正在部署代謝體學、分子生物學和表徵能力,並經常使用翻新試劑盒來加速部署和培訓。學術採購團隊優先考慮校準文件、安裝和培訓服務,以最大限度地延長儀器運作,同時確保符合認證標準和津貼報告要求。供應商提供的保固、啟動包和服務合約相結合,支持教育和研究實驗室的快速部署和長期使用。這些因素正在推動翻新實驗室設備市場中學術領域的快速成長。

區域分析

預計到2025年,北美將佔翻新實驗室設備市場收入的36.74%。這主要得益於該地區高度集中的製藥和生物技術中心以及成熟的二手設備分銷管道。聯邦和認證框架推薦符合ISO/IEC 17025標準的校準服務提供商,從而推動了對有據可查的翻新流程和可追溯性標準的需求。原始設備製造商(OEM)持續深化其在美國的製造和服務夥伴關係,以加強全生命週期支持,並在設備更換時提供清晰的認證轉售途徑。由於嚴格的法規和買家對同等保固的需求,以舊換新計畫和製造商認證的二手設備在該地區仍然佔據主導地位。仲介和經銷商憑藉豐富的庫存和靈活的保固服務補充了OEM管道,而學術聯盟則採購預先配置套件以快速推出實驗室。這些因素鞏固了該地區在翻新實驗室設備市場的主導地位和穩步成長的市場佔有率。

預計到2031年,亞太地區翻新實驗室設備市場將以8.90%的複合年成長率成長,成為所有地區中成長最快的市場。大學和國家實驗室的擴建提升了關鍵領域的處理能力,主要國家的公共計畫也加強了對科研基礎設施和人才培養的投資。印度的「Vigyan Dhara」計畫預算撥款便是這一趨勢的例證,該計畫為大學和研究機構對新設備和翻新設備的需求創造了源源不斷的管道。此外,區域中心正在建立先進的儀器中心,為未來的二級供應管道奠定基礎。隨著設備部署的成熟和更新換代週期的開始,預計亞太地區的OEM以舊換新和認證翻新專案將進一步擴展。該地區的買家優先考慮文件、服務管道和軟體驗證支持,以滿足認證和資料完整性要求。這些趨勢支撐了該地區翻新實驗室設備市場持續強勁的成長動能。

在歐洲,嚴格的品質和安全法規對翻新設備的文件要求進行了標準化,使其在翻新實驗室設備市場中保持了顯著的市場佔有率。受監管設備的全面翻新需要CE認證,這提高了合規門檻,但同時也透過統一成員國之間的品質標準降低了買家的不確定性。主要原始設備製造商(OEM)持續投資於歐洲的製造和服務設施,支援報廢設備的生命週期管理和認證的轉售管道。更廣泛的永續發展措施正促使各機構延長資產使用壽命,並採用循環採購規則,強調具有顯著環境效益的翻新和回收方案。這些趨勢共同支撐了符合歐洲監管工作流程和ESG政策的、有據可查的翻新系統的持續需求。

在中東、非洲和南美洲,隨著各國政府和大學研究及測試能力的提升,翻新實驗室設備的市場也不斷擴大。連接數千家機構的跨境數位基礎設施正在推動科學研究計畫對設備的需求,擴大設備使用者群體,並促進未來設備回收。加強科學研究津貼投入和促進設備使用的公私合營合作模式,正在改善設備取得途徑,並支持資源共用模式。由於當地服務選擇有限,這些地區的買家優先考慮設備的可靠性、校準可追溯性和備件供應,以確保設備運作。能夠提供遠端支援、安裝記錄和清晰保固條款的仲介和原始設備製造商(OEM)將更有利於加速設備的普及應用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 為預算有限的研究機構和新創企業提供經濟高效的採購方案。

- 製藥和生物技術領域的研究與開發不斷擴大,對測量儀器的需求也隨之增加。

- 永續發展和循環經濟政策旨在加速再利用

- 新興經濟體學術和研究能力的成長

- 原廠認證的二手設備和以舊換新計畫可降低購買風險。

- 研究機構的關閉、合併和收購以及退役,促進了高品質二手的供應。

- 市場限制因素

- 由於翻新標準不一致,人們對產品的準確性、可靠性和校準存在擔憂。

- 保固範圍有限/售後服務和流程缺乏標準化

- 由於OEM軟體許可/EoL支援方面的限制,搬遷受到限制。

- 受監管工作流程中的組件過時和檢驗成本

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 產品類型

- 分析設備

- 通用實驗室設備

- 生命科學設備

- 臨床診斷設備

- 最終用戶

- 製藥和生物技術公司

- 學術研究機構

- 臨床和診斷檢查室

- 受託研究機構(CRO)

- 醫院和醫療設施

- 按銷售管道

- OEM認證二手設備計劃

- 獨立重整公司/交易商

- 線上市場和競標

- 按等級翻新

- OEM工廠認證

- 第三方修復

- 二手商品,現況出售/附帶保固

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Agilent Technologies, Inc.

- American Laboratory Trading(ALT)

- Becton, Dickinson and Company

- Bruker Corporation

- Cambridge Scientific Products

- Carl Zeiss AG

- Copia Scientific

- EquipNet, Inc.

- GenTech Scientific LLC

- International Equipment Trading Ltd.(IET)

- IRIS Industries

- Marshall Scientific LLC

- Mettler-Toledo International Inc.

- Revvity, Inc.

- Richmond Scientific(UK)

- Sartorius AG

- Siemens Healthineers AG

- Surplus Solutions LLC

- Thermo Fisher Scientific, Inc.

- Waters Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the refurbished laboratory equipment market size is expected to grow from USD 26.38 billion in 2025 to USD 28.18 billion in 2026 and is forecast to reach USD 39.21 billion by 2031 at 6.83% CAGR over 2026-2031.

This report is Segmented by Product Type (Analytical Instruments, General Laboratory Equipment, and More), End User (Pharmaceutical & Biotechnology Companies, and More), Sales Channel (OEM Certified Pre-Owned Programs, and More), Refurbishment Grade (OEM Factory-Certified, and More), and Geography (North America, Europe, and More). The Market and Forecasted in Terms of Value (USD).

Global Refurbished Laboratory Equipment Market Trends and Insights

Cost-Effective Procurement for Budget-Constrained Labs and Startups

Budget-sensitive buyers spanning academia, diagnostics, and contract research redirect capital from new purchases to certified refurbished instruments that meet throughput needs at lower acquisition cost, which allows funds to be reallocated to consumables, personnel, and validation. Public buyers and NGOs frame decisions through total cost of ownership lenses that weigh calibration, parts availability, reagent logistics, and service access over multi-year horizons to avoid idle assets and procurement lock-ins. Vendors that publish calibration traceability and pre-shipment validation gain preference as buyers seek predictable uptime and auditable records. On the supply side, certified refurbishment programs with factory inspection and warranty parity narrow the perceived performance gap compared with new systems. Marketplace specialists that provide documented environmental savings and configured startup bundles strengthen appeal to incubators and early-stage labs seeking rapid commissioning. Case-in-point examples include vendor programs that disclose multi-point inspections with genuine parts, full warranty, and on-site installation to support compliant go-live in regulated workflows. Budget-conscious labs also validate supplier claims against calibration certificates traceable to national metrology bodies to maintain audit-ready records.

Expansion of Pharma and Biotech R&D Increasing Instrument Demand

Rising biopharma R&D intensity increases deployments of LC-MS, chromatography systems, and high-content imaging platforms, which later become candidates for trade-in or certified resale during portfolio upgrades. M&A and portfolio shifts add to decommissioning cycles that release high-value instruments into refurbishment pipelines, often bundled with removal and logistics services to reduce buyer friction. Large OEMs continue to invest in end-to-end capabilities and partnerships that reinforce customer relationships and expand access to installed equipment fleets over the asset lifecycle. India's Vigyan Dhara expanded R&D allocations in 2025-26, supporting equipment grants that add to regional installed bases and set up refresh cycles over subsequent funding windows. OEM acquisitions and capacity expansions that align with biopharma demands signal sustained instrument utilization and repower secondary channels as customers modernize fleets. Regulatory convergence around ISO 13485 and FDA QMSR expectations further codifies calibration and documentation, which raises the bar for refurbishers and increases buyer trust in well-documented offerings.

Accuracy, Reliability, and Calibration Concerns from Non-Uniform Refurb Standards

Calibration quality remains a top concern when refurbishment standards vary, especially where labs must meet FDA, ISO, and CLIA requirements that depend on tight measurement control. Federal letters of nonconformance in recent years have frequently referenced calibration gaps, which elevates buyer scrutiny of traceability, uncertainty budgets, and environmental controls embedded in vendor processes. ISO 13485 and ISO/IEC 17025 frameworks expect documented calibration chains to national metrology bodies, defined tolerances, and investigation of out-of-tolerance events to maintain product quality across the lifecycle. FDA quality system requirements also emphasize defined calibration intervals and records that link instrument status to batches or samples tested, which pushes refurbishers to provide auditable documentation from day one. CLIA and related guidance reinforce periodic verification triggers such as reagent-lot changes and maintenance events, which increase the importance of reliable service access for refurbished units placed in clinical workflows. Labs mitigate this restraint by standardizing on vendors that provide calibration certificates traceable to NIST or BIPM, validated software versions, and environmental conditions documented at the time of calibration.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability and Circular Economy Policies Accelerating Reuse

- Growth of Academic and Research Capacity in Emerging Economies

- Limited Warranty/After-Sales Support and Lack of Process Standardization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Analytical Instruments captured 42.17% of revenue in 2025 within the refurbished laboratory equipment market, reflecting sustained demand for LC-MS, GC, and spectroscopy systems used across discovery and QC workflows. Procurement teams increasingly channel late-generation instruments into trade-in programs that return certified LC-MS platforms with documented factory inspection, firmware updates, and parity warranties, which strengthens trust in this category for regulated uses. Residual value is reinforced by sellers that provide multi-month warranties, traceable calibration, and installation services, while buyers formalize uptime expectations through service tiers and preventive maintenance plans. Calibration documentation aligned to ISO 13485 and ISO/IEC 17025 remains central to placing refurbished analytical systems in pharma QC and CLIA environments, which influences price premiums for OEM-certified units over non-certified alternatives. Where labs retire legacy operating systems or software versions, sellers that provide validated software states at shipment reduce commissioning friction and speed compliance sign-offs. These factors collectively reinforce category leadership for analytical instruments in the refurbished laboratory equipment market.

General Laboratory Equipment is forecast to be the fastest-growing product category at a 7.43% CAGR through 2031, supported by broad applicability across academic, hospital, and industrial labs. The refurbished laboratory equipment market size tied to this segment benefits from quick-turn availability of centrifuges, incubators, biosafety cabinets, balances, and liquid handling systems that can be certified to lab accreditation requirements. Demand is reinforced by modular automation and sustainability-aligned equipment that reduces energy or consumables usage, which aligns with circular procurement objectives. Sellers differentiate through warranty breadth and ability to ship with documented IQ/OQ/PQ test records for rapid go-live in audited environments. Buyers increasingly bundle refurbished general equipment with startup kits and training to stand up new labs or expand existing facilities on constrained budgets. Documentation quality and consistency remain the primary selection criteria, with calibration traceability and defined service routes improving decision speed and confidence. These dynamics support sustained expansion for general equipment in the refurbished laboratory equipment market.

Pharmaceutical & Biotechnology Companies represented 32.28% of 2025 revenue as R&D investment supported high utilization of LC-MS, chromatography, and high-content imaging platforms across development and QC. Active trade-in and upgrade cycles supply secondary channels with well-maintained assets as new modalities expand instrumentation needs in discovery and analytics. OEM partnerships and capacity additions that align to drug-product manufacturing and services strengthen the equipment lifecycle, from primary sale through eventual certified resale. Bioprocess and analytical workflow investments continue to shape installed bases, which later feed the refurbished laboratory equipment market with quality-documented units. The refurbished laboratory equipment market share tied to pharma buyers remains supported by warranty parity and factory validation that satisfy audit and accreditation requirements. These elements keep refurbished placements viable for non-GxP and selected GxP contexts where documentation, calibration traceability, and service response times are proven.

Academic & Research Institutes are projected to grow the fastest at an 8.56% CAGR through 2031 as public programs expand laboratory capacity and prioritize hands-on infrastructure. India's Vigyan Dhara funding supports instrumentation grants across institutions, which increases near-term demand for certified refurbished systems and sets multi-year refresh cycles for future secondary supply. New national instrumentation centers and university-industry hubs bring metabolomics, molecular, and characterization capabilities online, often with refurbished kits that speed commissioning and training. Procurement teams in academia weigh calibration documentation, installation, and training services to comply with accreditation and grant reporting while maximizing instrument uptime. Suppliers that combine warranty coverage, startup bundles, and service agreements support rapid adoption and long-term utilization in teaching and research labs. These drivers sustain the fast-growing academic cohort in the refurbished laboratory equipment market.

Geography Analysis

North America held 36.74% of 2025 revenue for the refurbished laboratory equipment market, supported by dense pharma and biotech clusters and mature secondary-equipment channels. Federal and accreditation frameworks favor ISO/IEC 17025-aligned calibration providers, which reinforces demand for documented refurbishment and traceability standards. OEMs continue to deepen U.S. manufacturing and services partnerships that strengthen lifecycle support and provide clear pathways to certified resale when fleets refresh. Trade-in programs and factory-certified refurbished offerings remain prominent in this region due to regulatory rigor and buyer preferences for warranty parity. Brokers and dealers complement OEM channels through inventory breadth and flexible warranties, while academic consortia source configured kits for rapid lab setups. These elements underpin regional leadership and steady adoption in the refurbished laboratory equipment market.

Asia-Pacific is projected to grow at an 8.90% CAGR through 2031, the fastest among regions in the refurbished laboratory equipment market. University and national lab expansions are adding capacity in priority fields, and public programs in major countries are directing funds toward research infrastructure and training. India's Vigyan Dhara allocation exemplifies this trend, creating a pipeline for both new and refurbished instruments across universities and institutes. Regional hubs are also building advanced instrumentation centers that will generate installed bases aligned to future secondary supply channels. As cohorts mature and upgrade cycles begin, OEM trade-in and certified refurbished programs are expected to scale further into Asia-Pacific. Buyers in the region focus on documentation readiness, service access, and software validation support to align with accreditation and data-integrity requirements. These developments support sustained regional outperformance in the refurbished laboratory equipment market.

Europe maintains a significant share in the refurbished laboratory equipment market as stringent quality and safety regulations normalize documentation expectations for refurbished units. CE marking requirements for substantial refurbishment of regulated devices raise compliance thresholds but also reduce uncertainty for buyers by standardizing quality across member states. Leading OEMs continue to invest in European manufacturing and service footprints, which supports lifecycle management and certified resale pathways for instruments that exit primary service. Broader sustainability initiatives motivate institutions to extend asset life and adopt circular procurement rules that value refurbishment and take-back options with provable environmental benefits. Collectively, these dynamics support durable demand for documented refurbished systems that fit regulated workflows and ESG policies in Europe.

In the Middle East and Africa and in South America, the refurbished laboratory equipment market advances as governments and universities build out research and testing capacity. Cross-border digital infrastructure that connects thousands of institutions is catalyzing equipment demand for scientific programs, which expands installed bases that later recycle into secondary channels. Public-private programs that strengthen research-granting capacity and promote equipment utilization are improving access to instruments and supporting shared resource models. Buyers in these regions prioritize reliability, calibration traceability, and access to replacement parts to sustain uptime with limited local service options. Brokers and OEMs that provide remote support, documented installation, and clear warranty terms are positioned to accelerate adoption.

- Agilent Technologies

- American Laboratory Trading (ALT)

- Beckton Dickinson

- Bruker

- Cambridge Scientific Products

- Carl Zeiss

- Copia Scientific

- EquipNet, Inc.

- GenTech Scientific LLC

- International Equipment Trading Ltd. (IET)

- IRIS Industries

- Marshall Scientific LLC

- Mettler Toledo

- Revvity, Inc.

- Richmond Scientific (UK)

- Sartorius

- Siemens Healthineers

- Surplus Solutions LLC

- Thermo Fisher Scientific

- Waters Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-Effective Procurement for Budget-Constrained Labs and Startups

- 4.2.2 Expansion of Pharma and Biotech R&D Increasing Instrument Demand

- 4.2.3 Sustainability and Circular Economy Policies Accelerating Reuse

- 4.2.4 Growth of Academic and Research Capacity in Emerging Economies

- 4.2.5 OEM Certified Pre-Owned and Trade-In Programs De-Risk Purchases

- 4.2.6 Lab Closures, M&A, and Decommissioning Fueling High-Quality Secondary Supply

- 4.3 Market Restraints

- 4.3.1 Accuracy, Reliability, and Calibration Concerns from Non-Uniform Refurb Standards

- 4.3.2 Limited Warranty/After-Sales Support and Lack of Process Standardization

- 4.3.3 OEM Software Licensing/EoL Support Restrictions Limiting Redeployment

- 4.3.4 Parts Obsolescence and Validation Costs for Regulated Workflows

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 Product Type

- 5.1.1 Analytical Instruments

- 5.1.2 General Laboratory Equipment

- 5.1.3 Life Science Equipment

- 5.1.4 Clinical Diagnostic Equipment

- 5.2 By End User

- 5.2.1 Pharmaceutical & Biotechnology Companies

- 5.2.2 Academic & Research Institutes

- 5.2.3 Clinical & Diagnostic Laboratories

- 5.2.4 Contract Research Organizations (CROs)

- 5.2.5 Hospitals & Healthcare Facilities

- 5.3 By Sales Channel

- 5.3.1 OEM Certified Pre-Owned Programs

- 5.3.2 Independent Refurbishers/Dealers

- 5.3.3 Online Marketplaces & Auctions

- 5.4 By Refurbishment Grade

- 5.4.1 OEM Factory-Certified

- 5.4.2 Third-Party Reconditioned

- 5.4.3 As-Is/Lightly Used with Warranty

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Agilent Technologies, Inc.

- 6.3.2 American Laboratory Trading (ALT)

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Bruker Corporation

- 6.3.5 Cambridge Scientific Products

- 6.3.6 Carl Zeiss AG

- 6.3.7 Copia Scientific

- 6.3.8 EquipNet, Inc.

- 6.3.9 GenTech Scientific LLC

- 6.3.10 International Equipment Trading Ltd. (IET)

- 6.3.11 IRIS Industries

- 6.3.12 Marshall Scientific LLC

- 6.3.13 Mettler-Toledo International Inc.

- 6.3.14 Revvity, Inc.

- 6.3.15 Richmond Scientific (UK)

- 6.3.16 Sartorius AG

- 6.3.17 Siemens Healthineers AG

- 6.3.18 Surplus Solutions LLC

- 6.3.19 Thermo Fisher Scientific, Inc.

- 6.3.20 Waters Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

實驗室培養板處理系統市場:全球市場預測,2026-2032年實驗室瓶蓋分配器市場-2026-2032年全球市場預測實驗室一次性用品市場:2026-2032年全球市場預測(按產品類型、材料、滅菌類型、應用和分銷管道分類)

實驗室培養板處理系統市場:全球市場預測,2026-2032年實驗室瓶蓋分配器市場-2026-2032年全球市場預測實驗室一次性用品市場:2026-2032年全球市場預測(按產品類型、材料、滅菌類型、應用和分銷管道分類) 實驗室設備及服務:市場佔有率分析、產業趨勢及統計、成長預測(2026-2031)

實驗室設備及服務:市場佔有率分析、產業趨勢及統計、成長預測(2026-2031) 實驗室設備市場(2025-2030年):市場概覽實驗室設備及服務市場:2026-2032年全球市場預測(依服務類型、設備類型、定價模式、最終用途及銷售管道)

實驗室設備市場(2025-2030年):市場概覽實驗室設備及服務市場:2026-2032年全球市場預測(依服務類型、設備類型、定價模式、最終用途及銷售管道) 實驗室設備市場規模、佔有率和成長分析:按產品類型、應用、技術、採購方式、最終用戶和地區分類-2026-2033年產業預測

實驗室設備市場規模、佔有率和成長分析:按產品類型、應用、技術、採購方式、最終用戶和地區分類-2026-2033年產業預測 實驗室配件市場:按產品類型、應用、最終用戶和地區分類

實驗室配件市場:按產品類型、應用、最終用戶和地區分類 實驗室設備及耗材市場報告:依產品類型、最終用途及地區分類,2026-2034年實驗室設備市場:全球市場按產品類型、最終用戶、設備類型和應用分類的預測,2026-2032年

實驗室設備及耗材市場報告:依產品類型、最終用途及地區分類,2026-2034年實驗室設備市場:全球市場按產品類型、最終用戶、設備類型和應用分類的預測,2026-2032年