|

市場調查報告書

商品編碼

2063435

Agentic企業軟體:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)Agentic Enterprise Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

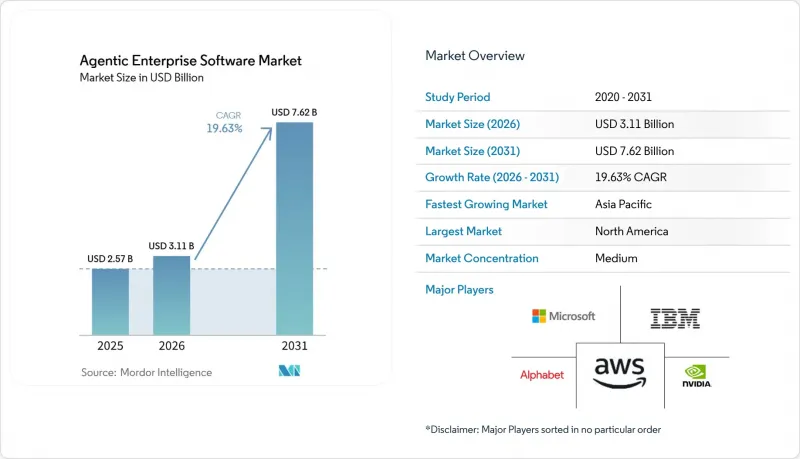

根據 Mordor Intelligence 預測,智慧企業軟體市場將從 2025 年的 25.7 億美元成長到 2026 年的 31.1 億美元,到 2031 年將達到 76.2 億美元,2026 年至 2031 年的複合年成長率為 19.63%。

本報告按部署類型(雲端、本地部署、混合部署)、組件(軟體和服務)、組織規模(大型企業和中小企業)、行業(銀行、金融服務和保險、醫療保健和生命科學、製造業、零售和電子商務等)以及地區進行細分。市場預測以美元計價。

代理企業軟體市場的全球趨勢與洞察

企業對超自動化和成本效益的需求

企業,尤其是金融、人力資源和採購領域的企業,正在將分散的工具整合到整合代理堆疊中,以縮短週期時間並降低人事費用。由於代理即使在使用者介面和資料模式變更時也能保持穩健性,因此避免了以往機器人流程自動化 (RPA) 專案中耗費成本的腳本重寫。在高薪地區,實施的投資回收期不到一年,因此獲得了經營團隊的更多支持。例如,一家銀行的合規團隊已部署代理商來即時監控交易,在保持監管審計追蹤的同時,將誤報率降低了兩位數。不斷上漲的人事費用和持續存在的技能缺口進一步提升了數位化工作的吸引力,預計成熟經濟體和新興經濟體對超自動化的需求都將保持旺盛。

大規模語言模型和工具編配框架的快速發展

LangGraph、AutoGen 和 CrewAI 等框架使開發人員能夠整合專門用於資料收集、程式碼執行和推理的代理,從而建立接近人類分析師績效的一致工作流程。 OpenAI 的 Frontier 平台推出了合約審查、客戶支援分診和供應鏈診斷的即用型模板,將引進週期從幾季縮短到幾週。上下文視窗已從 2025 年初的 32,000 個令牌大幅擴展至超過 200,000 個令牌,使代理商能夠一次處理整個程式碼庫和多年帳簿。這種能力在製造業的根本原因調查中具有極高的價值。具有安全功能的垂直最佳化模型解決了致幻劑問題,從而在需要明確回溯和全面審計追蹤的監管領域中得到了更廣泛的應用。

實施成本高,且難以與舊有系統整合。

將代理程式整合到已運行數十年的企業資源計劃 (ERP) 和客戶管理平台中,需要客製化連接器、資料協調和全面的回歸測試。銀行和保險業仍在運作的大型主機環境由於 COBOL 介面缺乏現代 API,增加了延遲和故障風險,從而進一步增加了複雜性。本地部署還需要專用 GPU叢集,中等規模的環境需要 50 萬至 200 萬美元的資本投資。基於結果的定價模式將部分風險轉移給了供應商,同時壓縮了他們的利潤空間,並縮小了合格整合商的選擇範圍。儘管總體擁有成本 (TCO) 計算結果頗具吸引力,但這些因素導致專案週期延長,並阻礙了短期部署。

細分市場分析

到2031年,混合部署將以每年20.23%的速度成長。這是因為企業將敏感的推理工作負載(例如患者記錄和信用風險模型)卸載到本地節點,同時利用雲端的擴充性進行大量分析和麵向消費者的聊天機器人。由於雲端服務的快速部署和供應商管理的更新,預計到2025年,雲端服務將佔總收入的61.74%,但德國和瑞士的資料居住法規限制了純粹的雲端採用。 Microsoft Azure Stack、AWS Outposts 和類似解決方案在本機硬體上複製雲端控制平面,讓開發人員無論身處何處都能呼叫相同的 API。隨著新的互通性協定減少配置開銷,以及從機器人到零售自助服務終端等各種邊緣用例對亞毫秒響應時間的需求,混合解決方案的代理企業軟體市場規模預計將加速成長。

監管機構要求將高風險推理日誌保存在自身管轄範圍內,從而推動向混合模式的轉變,並透過將關鍵任務資料保留在本地來防止供應商鎖定。企業透過將對延遲敏感的令牌保存在本地,同時將不太重要的作業傳輸到競價型實例上(比按需實例價格便宜高達 80%),從而降低資料傳輸成本。隨著多重雲端管治的日趨成熟,代理將擴大在單一工作流程中編配跨越 AWS、Azure 和 Google Cloud 的任務,從而分散運行時風險並增強彈性。

儘管預計到2025年軟體支出將佔總支出的58.42%,但智慧企業軟體的市佔率組成正在發生變化,服務領域的複合年成長率預計將達到20.03%,這反映出將智慧體整合到異質環境中所面臨的挑戰。資料工程、模式映射和安全測試可能佔第一年預算的30%到50%,在主要大都會地區,專業工程師的收費高達每小時300美元。以結果為導向、承諾明確績效指標的管理服務正在吸引那些缺乏內部機器學習人才的中型買家。

OpenAI 的「前沿聯盟」(Frontier Alliances)與全球顧問公司合作,透過整合建模專業知識和變革管理經驗,系統化了這個生態系統,縮短了高度監管行業的試點部署時間。超大規模資料中心業者中心主導的培訓計畫已認證了數千名從業人員,使其能夠快速開展工程和紅隊演練,進一步促進了服務成長。雖然隨著供應商承擔營運風險,智慧企業軟體的託管服務市場預計將會擴張,但利潤率的壓力可能會導致財務狀況不太穩定的新創公司之間出現整合。

區域分析

北美地區擁有成熟的科技公司和良好的法規環境,預計2025年將佔全球收入的39.68%。該地區的市場主導地位歸功於其對先進技術的早期採用和對創新的大量投資。然而,亞太地區預計到2031年將達到最高的複合年成長率(CAGR),達到20.63%。中國、日本、印度和韓國等國家正在大力投資於自主開發的模型訓練和本地推理叢集,以確保資料主權。這項舉措推動了對本地部署加速器和開放原始碼工具的需求,使該地區成為主要的市場驅動力。同時,由於嚴格的隱私法規,歐洲的採用速度較慢,但這種做法有助於建立長期信任,並可能為該地區的供應商帶來競爭優勢。

在中東和非洲地區,石油收入的激增正被用於發展人工智慧中心。然而,目前人工智慧的應用主要集中在能源和公共服務等領域。這些投資旨在實現區域經濟多元化並增強其技術能力。在拉丁美洲,成長主要集中在巴西和阿根廷,兩國在數位銀行和零售領域的先導計畫已成功展示了人工智慧在詐欺檢測和個人化產品提案的價值。儘管面臨經濟不穩定和基礎設施限制等挑戰,這些進展仍凸顯了人工智慧在該地區應用的巨大潛力。

超大規模資料中心業者資料中心在馬來西亞、泰國和沙烏地阿拉伯等國的區域基地不斷擴張,降低了邊緣運算密集型工作負載的延遲,並進一步加速了先進技術的應用。世界經濟論壇(WEF)的管治框架為這些發展提供了補充,該框架為企業提供了一套標準化的術語,以協調其在多個司法管轄區的部署。該框架尤其有利於在不同的法規環境下運作的組織,能夠實現更順暢的整合和合規。總體而言,這些區域發展凸顯了全球人工智慧應用的強勁勢頭,每個區域的成長軌跡則取決於其政策、投資和技術準備。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 企業對超自動化和成本效益的需求

- 大規模語言模型和工具編配框架的快速發展

- 擴展雲端基礎設施並降低推理成本

- 為實現廠商間互通性,出現了多代理管治標準。

- 產業特定的負責任人工智慧框架:促進受監管產業的採用

- 績效定價模式的日益普及正在加速其在中型企業市場的推廣應用。

- 市場限制因素

- 實施成本高,且難以與舊有系統整合。

- 資料隱私和監管不確定性

- 安全導引型工程人員短缺

- 缺乏企業級代理可靠性基準

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 部署模式

- 基於雲端的

- 現場

- 混合

- 按組件

- 軟體

- 服務

- 按組織規模

- 大公司

- 小型企業

- 按行業分類

- 銀行、金融服務和保險(BFSI)

- 醫療保健和生命科學

- 製造業

- 零售與電子商務

- 資訊科技/通訊

- 政府/公共部門

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- Salesforce Inc

- ServiceNow Inc

- Amazon Web Services Inc

- Google Cloud(Alphabet Inc)

- IBM Corporation

- OpenAI LLC

- Anthropic PBC

- Cohere Inc

- Adept AI Labs

- NVIDIA Corporation

- UiPath Inc

- Aisera Inc

- DataRobot Inc

- Cognigy GmbH

- SAP SE

- Snowflake Inc

- Oracle Corporation

- Baidu Inc

- Automation Anywhere Inc

第7章 市場機會與未來展望

According to Mordor Intelligence, the agentic enterprise software market size is expected to grow from USD 2.57 billion in 2025 to USD 3.11 billion in 2026 and is forecast to reach USD 7.62 billion by 2031 at a 19.63% CAGR over 2026-2031.

This report is Segmented by Deployment Mode (Cloud, On-Premise, and Hybrid), Component (Software and Services), Organization Size (Large Enterprises and Small and Medium Enterprises), Industry Vertical (BFSI, Healthcare and Life Sciences, Manufacturing, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic Enterprise Software Market Trends and Insights

Enterprise Demand for Hyper-Automation and Cost Efficiency

Organizations are consolidating scattered point tools into unified agent stacks that compress cycle times and shrink payroll outlays, especially in finance, human resources, and procurement. Agents remain resilient when user interfaces or data schemas shift, which avoids the costly re-scripting that undermined earlier robotic process automation efforts. In high-wage regions, deployments now attain payback in under one year, strengthening board-level sponsorship. Banking compliance teams, for example, deploy agents that monitor transactions in real time, achieving double-digit reductions in false positives while maintaining regulatory audit trails. Rising labor costs and persistent skills gaps further magnify the appeal of digital labor, ensuring that demand for hyper-automation will stay elevated across both mature and emerging economies.

Rapid Advances in Large Language Models and Tool-Orchestration Frameworks

Frameworks such as LangGraph, AutoGen, and CrewAI allow developers to chain specialized agents for data retrieval, code execution, and reasoning into cohesive workflows that approximate human analyst performance. OpenAI's Frontier platform introduced out-of-the-box templates for contract reviews, customer support triage, and supply chain diagnostics, cutting deployment cycles from quarters to weeks. Context windows have leapt from 32,000 tokens in early 2025 to more than 200,000, enabling agents to process entire code bases or multi-year ledgers in a single pass, a capability prized for root-cause investigations in manufacturing. Vertically tuned models backed by safety guardrails are addressing concerns about hallucinations, which is widening adoption in regulated fields that require deterministic rollback and comprehensive audit trails.

High Implementation Costs and Legacy Integration Challenges

Embedding agents into decades-old enterprise resource planning and customer management platforms demands custom connectors, data harmonization, and exhaustive regression testing. Mainframe environments that still power banking and insurance add another layer of complexity because COBOL interfaces lack modern APIs, which increases latency and failure risk. On-premise rollouts also require specialized GPU clusters, which entail capital expenditures ranging from USD 0.5 million to USD 2 million for mid-sized estates. While outcome-based pricing shifts some risk to vendors, it compresses their margins and restricts the pool of capable integrators. These factors prolong project timelines and temper near-term adoption despite compelling total cost-of-ownership calculations.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Infrastructure Expansion and Lower Inference Costs

- Emergence of Multi-Agent Governance Standards Enabling Cross-Vendor Interoperability

- Data Privacy and Regulatory Uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid deployments are expanding at a 20.23% annual clip through 2031 as firms route sensitive inference workloads, such as patient records or credit-risk models, to on-premise nodes while leveraging cloud elasticity for batch analytics and public-facing chatbots. Cloud offerings accounted for 61.74% of 2025 revenue due to rapid provisioning and vendor-maintained updates, yet data residency statutes in Germany and Switzerland limit pure-cloud penetration. Microsoft Azure Stack, AWS Outposts, and similar solutions replicate cloud control planes on local hardware, enabling developers to invoke identical APIs regardless of location. The agentic enterprise software market size for hybrid solutions is forecast to accelerate as emerging interoperability protocols reduce configuration overhead and as edge use cases, from robotics to retail kiosks, demand sub-100-millisecond response times.

Regulators are nudging adoption toward hybrid models by requiring that high-risk inference logs remain within sovereign borders, thereby guarding against vendor lock-in by keeping mission-critical data onsite. Enterprises cut egress bills by keeping latency-sensitive tokens local while bursting non-critical jobs to spot instances priced up to 80% below on-demand rates. As multi-cloud governance matures, agents will increasingly orchestrate tasks across AWS, Azure, and Google Cloud within a single workflow, thereby diversifying runtime risk and amplifying resilience.

Software accounted for 58.42% of 2025 spending, yet the agentic enterprise software market share mix is shifting as services register a 20.03% CAGR, mirroring the difficulty of stitching agents into heterogeneous estates. Data engineering, schema mapping, and safety testing can swallow 30% to 50% of first-year budgets, while hourly rates for specialized engineers reach USD 300 in major hubs. Outcome-based managed services that commit to definitive performance benchmarks are attracting mid-market buyers that lack in-house machine-learning talent.

OpenAI's Frontier Alliances with global consultancies formalize this ecosystem by pooling model expertise with change-management playbooks, shrinking pilot timelines in heavily regulated verticals. Training programs from hyperscalers certify thousands of practitioners in prompt engineering and red-teaming, further fueling services growth. The agentic enterprise software market size for managed offerings is set to expand as vendors assume operational risk, though margin pressures may induce consolidation among undercapitalized startups.

Geography Analysis

North America accounted for 39.68% of 2025 revenue, driven by the presence of established technology incumbents and a favorable regulatory environment. The region's market stronghold is attributed to its early adoption of advanced technologies and significant investments in innovation. However, the Asia-Pacific is expected to achieve the highest regional CAGR of 20.63% through 2031. Countries such as China, Japan, India, and South Korea are heavily investing in indigenous model training and local inference clusters to ensure data sovereignty. This focus has led to increased demand for on-premise accelerators and open-source tools, positioning the region as a key growth driver in the market. Meanwhile, Europe faces slower rollouts due to its stringent privacy regulations, but this approach fosters long-term trust, which could serve as a competitive advantage for vendors in the region.

The Middle East and Africa are channeling oil windfall revenues into the development of AI hubs, though current use remains concentrated in sectors such as energy and public services. These investments aim to diversify regional economies and enhance technological capabilities. In Latin America, growth is primarily centered around Brazil and Argentina, where digital banking and retail pilots are successfully demonstrating the value of AI in fraud detection and personalized merchandising. These advancements highlight the region's potential for AI adoption, despite challenges such as economic instability and infrastructure limitations.

Hyperscaler region build-outs in countries like Malaysia, Thailand, and Saudi Arabia are reducing latency for edge-heavy workloads, further enabling the adoption of advanced technologies. These developments are complemented by the World Economic Forum's governance framework, which provides a standardized vocabulary for enterprises to harmonize multi-jurisdiction deployments. This framework is particularly beneficial for organizations operating across diverse regulatory environments, ensuring smoother integration and compliance. Collectively, these regional dynamics underscore the global momentum toward AI adoption, with varying growth trajectories influenced by local policies, investments, and technological readiness.

- Microsoft Corporation

- Salesforce Inc

- ServiceNow Inc

- Amazon Web Services Inc

- Google Cloud (Alphabet Inc)

- IBM Corporation

- OpenAI LLC

- Anthropic PBC

- Cohere Inc

- Adept AI Labs

- NVIDIA Corporation

- UiPath Inc

- Aisera Inc

- DataRobot Inc

- Cognigy GmbH

- SAP SE

- Snowflake Inc

- Oracle Corporation

- Baidu Inc

- Automation Anywhere Inc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Enterprise Demand for Hyper-Automation and Cost Efficiency

- 4.2.2 Rapid Advances in Large Language Models and Tool-Orchestration Frameworks

- 4.2.3 Cloud Infrastructure Expansion and Lower Inference Costs

- 4.2.4 Emergence of Multi-Agent Governance Standards Enabling Cross-Vendor Interoperability

- 4.2.5 Sector-Specific Responsible AI Frameworks Unlocking Regulated Industry Adoption

- 4.2.6 Availability of Outcome-Based Pricing Models Accelerating Mid-Market Uptake

- 4.3 Market Restraints

- 4.3.1 High Implementation Costs and Legacy Integration Challenges

- 4.3.2 Data Privacy and Regulatory Uncertainty

- 4.3.3 Scarcity of Safety-Alignment Engineering Talent

- 4.3.4 Absence of Enterprise-Grade Agent Reliability Benchmarks

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Industry Vertical

- 5.4.1 Banking Financial Services and Insurance BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Manufacturing

- 5.4.4 Retail and E-Commerce

- 5.4.5 Information Technology and Telecom

- 5.4.6 Government and Public Sector

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Salesforce Inc

- 6.4.3 ServiceNow Inc

- 6.4.4 Amazon Web Services Inc

- 6.4.5 Google Cloud (Alphabet Inc)

- 6.4.6 IBM Corporation

- 6.4.7 OpenAI LLC

- 6.4.8 Anthropic PBC

- 6.4.9 Cohere Inc

- 6.4.10 Adept AI Labs

- 6.4.11 NVIDIA Corporation

- 6.4.12 UiPath Inc

- 6.4.13 Aisera Inc

- 6.4.14 DataRobot Inc

- 6.4.15 Cognigy GmbH

- 6.4.16 SAP SE

- 6.4.17 Snowflake Inc

- 6.4.18 Oracle Corporation

- 6.4.19 Baidu Inc

- 6.4.20 Automation Anywhere Inc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

基於代理的人工智慧自動化市場預測至2034年-按部署模式、企業規模、技術水平、功能應用、最終用戶和地區分類的全球分析

基於代理的人工智慧自動化市場預測至2034年-按部署模式、企業規模、技術水平、功能應用、最終用戶和地區分類的全球分析 基於代理商的商業、人工智慧編配和自主支付市場:2026 年

基於代理商的商業、人工智慧編配和自主支付市場:2026 年 基於代理的人工智慧開發平台:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)醫療保健領域的智慧體人工智慧:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

基於代理的人工智慧開發平台:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)醫療保健領域的智慧體人工智慧:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 基於代理的人工智慧市場:按組件、部署類型、企業規模、最終用戶、國家和地區分類-行業分析、市場規模、市場佔有率及2026年至2033年預測無障礙學習技術市場預測至2034年-全球分析(按組件、殘疾類型、部署模式、技術、應用、最終用戶和地區分類)

基於代理的人工智慧市場:按組件、部署類型、企業規模、最終用戶、國家和地區分類-行業分析、市場規模、市場佔有率及2026年至2033年預測無障礙學習技術市場預測至2034年-全球分析(按組件、殘疾類型、部署模式、技術、應用、最終用戶和地區分類) 全球基於代理的人工智慧安全市場(至 2032 年):按安全功能和工具(即時安全工具、防護框架、人工智慧穿透測試和紅隊工具)和部署層級分類

全球基於代理的人工智慧安全市場(至 2032 年):按安全功能和工具(即時安全工具、防護框架、人工智慧穿透測試和紅隊工具)和部署層級分類 全球基於代理的人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球人工智慧購物代理和基於代理的商務(2026):部署趨勢和實施限制基於代理的人工智慧市場預測至2034年:按部署類型、功能、最終用戶和地區分類的全球分析

全球基於代理的人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球人工智慧購物代理和基於代理的商務(2026):部署趨勢和實施限制基於代理的人工智慧市場預測至2034年:按部署類型、功能、最終用戶和地區分類的全球分析