|

市場調查報告書

商品編碼

2061959

醫療保健領域的智慧體人工智慧:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Healthcare Agentic AI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

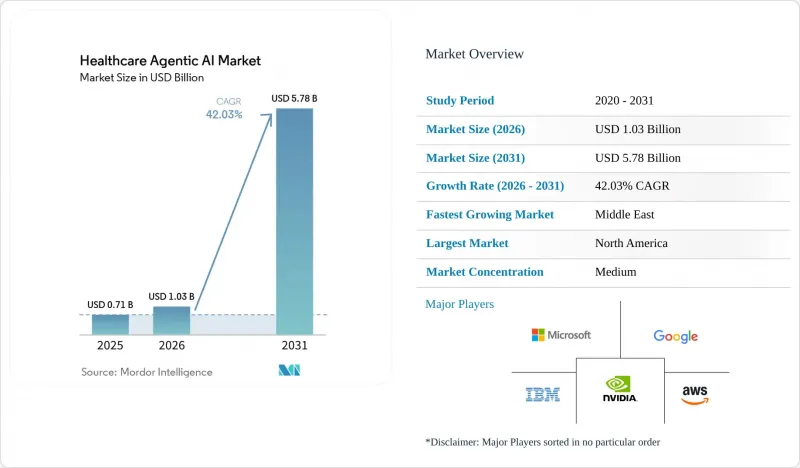

預計醫療保健領域智慧人工智慧的市場規模將從 2025 年的 7.1 億美元成長到 2026 年的 10.3 億美元,然後從 2026 年到 2031 年以 42.03% 的複合年成長率成長,到 2031 年達到 57.8 億美元。

本報告按交付方式(例如,平台)、部署方式(例如,本地部署)、應用領域(例如,臨床決策支援和診斷)、最終用戶(例如,醫院和醫療保健系統)、技術(例如,大規模語言模型代理、多模態自主代理、強化學習代理)和地區進行細分。市場預測以美元計價。

全球醫療保健領域智慧體人工智慧市場趨勢及洞察

擴大基於LLM的臨床ChatGPT工具的應用。

2026年,醫療保健系統開始將基於LLM的臨床工具整合到日常工作流程中,而不再局限於試點環境。 2026年1月,OpenAI與八家美國領先的醫療保健機構合作推出了“OpenAI for Healthcare”,該平台採用了GPT-5.2模型,該模型是在收集了來自60個國家260位醫生的反饋後開發的。 2026年4月發布的「ChatGPT for Clinicians」擴展了醫療保健專業人員的認證存取權限,並透過HealthBench Professional引入了臨床基準測試。微軟等領先供應商正在將醫療保健代理商編配納入其核心產品藍圖。到2025年底,微軟已在Microsoft Foundry中推出了醫療保健專用AI模型“Healthcare Agent Orchestrator”,並建立了一個醫療保健AI市場。隨著檢驗的AI工具被廣泛接受,醫療保健領域基於代理的AI正從創新預算轉向營運成本。

護理人員短缺日益嚴重,推動了對護理助理的需求。

勞動力短缺的壓力正在推動對虛擬護理和輔助人員的需求。一項利用美國勞動力數據的研究預測,到2033年,註冊護理師的年需求量將達到194,500個,到2038年,非大都會圈的勞動力缺口將達到11%。許多可以自動化的任務,例如建立病患摘要和協調推廣,都與護理工作流程密切相關。梅奧診所透過在其住院病房和急診科為超過9,600名護士部署人工智慧驅動的“護士虛擬助理”,展示了其擴充性,該計劃於2025年9月完成。這種務實的方法使醫療系統能夠在不大幅改變護理模式的情況下解放員工時間,從而使醫院即使在預算緊張的情況下也能繼續投資於基於代理的人工智慧。

資料隱私和 HIPAA 合規性的複雜性。

儘管需求不斷成長,但隱私要求仍然阻礙著技術的普及。處理敏感醫療資訊的基於代理的系統會產生多個控制點,從而增加複雜性,尤其是在必須遵守 HIPAA 和各州隱私法的跨州醫療保健系統中。隨著資料交換範圍的擴大,全國互通性基礎設施的擴展進一步凸顯了管治的必要性,因為安全存取控制和可審計性變得至關重要。因此,在醫療保健領域基於代理的人工智慧市場中,擁有清晰的資料處理規則、安全整合和對第三方模型層進行有效監管的供應商更具優勢。

細分市場分析

到2025年,軟體代理平台將佔據醫療保健代理人工智慧市場41.82%的佔有率。這主要是由於與電子健康記錄(EHR)工作流程整合後,轉換成本增加所致。微軟和Oracle正在推進其企業級技術堆疊中醫療保健人工智慧的編配,從而在無需更換硬體的情況下持續增加軟體收入。由於許多醫療服務提供者網路同時使用EHR和影像系統,因此整合服務仍然至關重要。

邊緣設備和專用硬體預計將成為醫療代理人工智慧市場中成長最快的細分領域,其成長動力主要來自影像診斷和監測中對本地推理的需求,因為雲端延遲會影響臨床回應。預計到2031年,其複合年成長率將達到42.63%。飛利浦和英偉達在2025年5月合作開發了一款利用英偉達基礎設施(包括MAISI和VISTA-3D)進行掃描規劃和自動檢測的MRI模型,凸顯了這一趨勢。這項合作在醫療設備和雲端軟體訂閱之間建立了一個清晰的硬體層。

到2025年,基於雲端的部署將佔據醫療保健領域的智慧體人工智慧市場52.38%。這一主導地位反映出,當醫療保健系統無需將大規模本地基礎設施作為初始投資時,它們可以更快地擴展新的人工智慧功能。雲端優先部署也符合領先供應商的商業策略,這些供應商致力於將人工智慧服務融入現有公司間的數據、生產力和臨床系統關係中。在資料主權規則和內部管治標準過於嚴格,難以僅透過雲端配置滿足的市場和機構中,本地部署模式仍然至關重要。

混合邊緣雲端部署預計到2031年將以42.58%的複合年成長率成長,在即時本地推理(用於分診和監控)與集中式模型更新之間取得平衡。蒙彼利埃大學醫院(CHU de Montpellier)的「2026 Alliance Sante IA」計畫是一項耗資1490萬歐元(1680萬美元)的計劃,利用自主本地計算技術為16000名醫療保健專業人員部署人工智慧。全國範圍內互通性的擴展進一步推動了混合模式的發展,實現了跨站點的數據協調,而無需集中所有推理,這使得混合架構成為主動式人工智慧醫療保健市場的關鍵設計轉折點。

區域分析

到2025年,北美將佔據醫療保健領域智慧體人工智慧市場的44.74%。這主要得益於電子健康記錄(EHR)的廣泛應用、強大的雲端基礎設施以及充滿活力的醫療保健軟體生態系統。聯邦政府的政策,例如縮短預核准週期和透過醫療保險和醫療補助服務中心(CMS)提高互通性,將進一步加速其應用。到2026年初,美國衛生與公眾服務部(HHS)將報告稱,《電子健康資訊共享法案》(TEFCA)已促成近5億份醫療記錄的交換,並增強了智慧體工作流程的數據傳輸。隨著應用範圍的擴大,該地區面臨的主要挑戰將是解決隱私、管治和更新管理等方面的問題。

歐洲在2025年排名第二。這得益於其對高風險臨床人工智慧採取合規主導的方法,強調資料管治、透明度和自主部署。歐盟委員會於2025年10月啟動的COMPASS-AI舉措旨在支援在腫瘤學和遠端醫療等領域安全部署該技術。例如,蒙彼利埃大學醫院(CHU de Montpellier)正在開發自主人工智慧基礎設施,並已吸引了其他15家醫院的關注。在歐洲市場,預計本地管理且可審計的架構將比僅透過雲端快速部署更受歡迎。

預計到2031年,中東地區的複合年成長率將達到42.89%,在所有地區中位居榜首。這主要得益於一項由政府主導的醫療轉型計劃,該計劃整合了由人工智慧驅動的醫療服務。亞太地區也正在崛起為關鍵區域,中國國家醫療保障局將於2026年3月推出「個人健康保險雲」舉措,該計劃旨在整合13.3億參保人員的數據。人才短缺、遠端醫療的擴展以及大規模的公共數位化計畫正在推動這兩個地區人工智慧技術的應用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 基於LLM的臨床ChatGPT工具的廣泛應用

- 護理人員短缺問題日益嚴重,導致對護理助理的需求不斷成長。

- 支付機構在預核准流程自動化方面的義務

- 將多模態感測技術整合到遠端監控設備中

- 向價值導向型醫療保健的轉變正在推動自動化。

- 醫療保健領域代理型新創企業的創業投資激增。

- 市場限制因素

- 資料隱私和 HIPAA 合規性的複雜性。

- 演算法偏見的風險會招致監管機構的監督。

- 缺乏標準化的互通性框架

- 缺乏自主代理的臨床檢驗證據

- 宏觀經濟因素對市場的影響

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 報價

- 軟體代理平台

- 整合和客製化服務

- 邊緣設備和專用硬體

- 部署模式

- 基於雲端的

- 現場

- 混合

- 透過使用

- 臨床決策支援與診斷

- 病人參與和虛擬護理

- 業務流程和管理自動化

- 藥物發現與研究

- 遠端監測和遠端醫療

- 最終用戶

- 醫院和醫療系統

- 門診/專科診所

- 付款人和保險

- 製藥和生物技術公司

- 病人(直接面對消費者)

- 透過技術

- 大規模語言模型代理

- 多模態自主代理

- 強化學習代理

- 基於規則的/專家代理

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Microsoft Corporation

- Google LLC

- Amazon.com, Inc.

- IBM Corporation

- NVIDIA Corporation

- Oracle Corporation

- GE HealthCare Technologies Inc.

- Siemens Healthineers AG

- Koninklijke Philips NV

- Epic Systems Corporation

- Cerner Corporation

- Nuance Communications, Inc.

- Medtronic plc

- Intuitive Surgical, Inc.

- Tempus Labs, Inc.

- PathAI, Inc.

- Butterfly Network, Inc.

- Viz.ai, Inc.

- Insilico Medicine, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the healthcare agentic AI market size is expected to grow from USD 0.71 billion in 2025 to USD 1.03 billion in 2026 and is forecast to reach USD 5.78 billion by 2031 at 42.03% CAGR over 2026-2031.

This report is Segmented by Offering (Platforms, and More), Deployment (On-Premise, and More), Application (Clinical Decision Support and Diagnostics, and More), End-User (Hospitals and Health Systems, and More), Technology (Large-Language-Model Agents, Multi-Modal Autonomous Agents, Reinforcement-Learning Agents, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Healthcare Agentic AI Market Trends and Insights

Rising Adoption of LLM-Based Clinical ChatGPT Tools

In 2026, health systems began integrating LLM-based clinical tools into daily workflows instead of limiting them to pilot settings. OpenAI launched OpenAI for Healthcare in January 2026, partnering with 8 leading U.S. health institutions and using GPT-5.2 models developed with input from 260 physicians across 60 countries. The April 2026 release of ChatGPT for Clinicians expanded verified access for medical users and introduced a clinical benchmark through HealthBench Professional. Major vendors, such as Microsoft, are incorporating healthcare agent orchestration into their core product roadmaps. By late 2025, Microsoft introduced healthcare-specific AI models, a Healthcare Agent Orchestrator in Microsoft Foundry, and a healthcare AI marketplace. As verified AI tools gain acceptance, agentic AI in healthcare is transitioning from innovation budgets to operational spending.

Increasing Shortage of Nursing Staff Driving Agent Assistants

Workforce pressure is driving demand for virtual nursing and task-support agents. A study using U.S. labor data projects 194,500 annual registered nurse job openings through 2033, with non-metropolitan areas potentially facing an 11% shortage by 2038. Many automated tasks, such as patient summaries and outreach coordination, are tied to nurse workflows. Mayo Clinic demonstrated scalability by deploying its AI-powered Nurse Virtual Assistant to over 9,600 nurses in inpatient and emergency units by September 2025. This practical approach allows health systems to reclaim staff time without overhauling care models, keeping hospitals invested in agentic AI despite tight capital budgets.

Data Privacy and HIPAA Compliance Complexities

Privacy requirements continue to hinder deployment despite rising demand. Agentic systems handling protected health information create multiple control points, increasing complexity, especially for multi-state health systems navigating HIPAA and state privacy laws. The growth of national interoperability infrastructure further underscores the need for governance, as broader data exchange underscores the importance of secure access controls and auditability. Consequently, the agentic AI in the healthcare market favors vendors with clear data handling rules, secure integration, and robust oversight of third-party model layers.

Other drivers and restraints analyzed in the detailed report include:

- Payer Mandates for Prior Authorization Automation

- Integration of Multi-Modal Sensing in Remote Monitoring Devices

- Algorithmic Bias Risks Leading to Regulatory Scrutiny

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software agent platforms accounted for 41.82% of the healthcare agentic AI market share in 2025, driven by their integration into EHR-linked workflows, which increases switching costs. Microsoft and Oracle have advanced healthcare AI orchestration within their enterprise stacks, boosting recurring software revenue without requiring hardware replacement. Integration services remain vital as many provider networks operate mixed EHR and imaging systems.

Edge devices and specialized hardware are expected to grow fastest in the agentic AI healthcare market, with a 42.63% CAGR through 2031, driven by the need for local inference in imaging and monitoring where cloud latency affects clinical response. Philips and NVIDIA highlighted this trend in May 2025 by collaborating on an MRI model that leveraged NVIDIA infrastructure, including MAISI and VISTA-3D, for scan planning and automated detection. This development establishes a distinct hardware layer between medical equipment and cloud software subscriptions.

Cloud-based deployment accounted for 52.38% of the healthcare agentic artificial intelligence market in 2025. That lead reflects the fact that health systems can scale new AI functions faster when they do not need heavy upfront local infrastructure. Cloud-first deployment also aligns with the commercial strategy of major platform vendors, which aim to have AI services sit within existing enterprise relationships across data, productivity, and clinical systems. On-premise models still matter in markets and institutions where data sovereignty rules and internal governance standards remain stricter than what a cloud-only setup can easily satisfy.

Hybrid edge-cloud deployments are projected to grow at a 42.58% CAGR through 2031, balancing real-time local inference for triage and monitoring with centralized model updates. CHU de Montpellier's 2026 Alliance Sante IA program, a EUR 14.9 million (USD 16.8 million) initiative, used sovereign local computing for AI deployment across 16,000 hospital professionals. National interoperability growth further supports hybrid models by enabling data coordination across sites without centralizing all inference, making hybrid architecture a key design shift in the agentic AI healthcare market.

Geography Analysis

North America accounted for 44.74% of the agentic AI market share in healthcare in 2025, driven by widespread EHR adoption, robust cloud infrastructure, and a dynamic healthcare software ecosystem. Federal policies, such as CMS's tightened prior authorization timelines and expanded interoperability, further accelerated adoption. By early 2026, HHS reported TEFCA had facilitated nearly 500 million health record exchanges, strengthening data movement for agent workflows. The region's primary challenge lies in addressing privacy, governance, and update control concerns as adoption scales.

Europe ranked second in 2025, following a compliance-driven approach emphasizing data governance, transparency, and sovereign deployment for high-risk clinical AI. The European Commission's COMPASS-AI initiative, launched in October 2025, supports the safe adoption of technologies in areas such as oncology and remote care. For instance, CHU de Montpellier is developing sovereign AI infrastructure, attracting interest from 15 additional hospital centers. Europe's market is expected to prioritize local control and audit-compliant architectures over rapid cloud-only rollouts.

The Middle East is projected to grow at a 42.89% CAGR through 2031, the fastest regional growth rate, fueled by state-backed health transformation programs integrating AI-enabled care delivery. Asia-Pacific is also emerging as a key region, with China's National Healthcare Security Administration launching the Personal Medical Insurance Cloud initiative in March 2026 to integrate data for 1.33 billion insured individuals. Workforce pressures, telehealth expansion, and large public digital programs are driving adoption in both regions.

- Microsoft Corporation

- Google LLC

- Amazon.com, Inc.

- IBM Corporation

- NVIDIA Corporation

- Oracle Corporation

- GE HealthCare Technologies Inc.

- Siemens Healthineers AG

- Koninklijke Philips N.V.

- Epic Systems Corporation

- Cerner Corporation

- Nuance Communications, Inc.

- Medtronic plc

- Intuitive Surgical, Inc.

- Tempus Labs, Inc.

- PathAI, Inc.

- Butterfly Network, Inc.

- Viz.ai, Inc.

- Insilico Medicine, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of LLM-Based Clinical ChatGPT Tools

- 4.2.2 Increasing Shortage of Nursing Staff Driving Agent Assistants

- 4.2.3 Payer Mandates for Prior Authorization Automation

- 4.2.4 Integration of Multi-Modal Sensing in Remote Monitoring Devices

- 4.2.5 Shift Toward Value-Based Care Incentivizing Automation

- 4.2.6 Venture Capital Funding Surge in Healthcare Agentic Start-ups

- 4.3 Market Restraints

- 4.3.1 Data Privacy and HIPAA Compliance Complexities

- 4.3.2 Algorithmic Bias Risks Leading to Regulatory Scrutiny

- 4.3.3 Lack of Standardized Interoperability Frameworks

- 4.3.4 Limited Clinical Validation Evidence for Autonomous Agents

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software Agent Platforms

- 5.1.2 Integration and Customization Services

- 5.1.3 Edge Devices and Specialized Hardware

- 5.2 By Deployment Mode

- 5.2.1 Cloud-based

- 5.2.2 On-premise

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Clinical Decision Support and Diagnostics

- 5.3.2 Patient Engagement and Virtual Nursing

- 5.3.3 Operational and Administrative Automation

- 5.3.4 Drug Discovery and Research

- 5.3.5 Remote Monitoring and Tele-health

- 5.4 By End-User

- 5.4.1 Hospitals and Health Systems

- 5.4.2 Ambulatory / Specialty Clinics

- 5.4.3 Payers and Insurance

- 5.4.4 Pharmaceutical and Biotech Companies

- 5.4.5 Patients (Direct-to-Consumer)

- 5.5 By Technology

- 5.5.1 Large-Language-Model Agents

- 5.5.2 Multi-Modal Autonomous Agents

- 5.5.3 Reinforcement-Learning Agents

- 5.5.4 Rule-based / Expert Agents

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Google LLC

- 6.4.3 Amazon.com, Inc.

- 6.4.4 IBM Corporation

- 6.4.5 NVIDIA Corporation

- 6.4.6 Oracle Corporation

- 6.4.7 GE HealthCare Technologies Inc.

- 6.4.8 Siemens Healthineers AG

- 6.4.9 Koninklijke Philips N.V.

- 6.4.10 Epic Systems Corporation

- 6.4.11 Cerner Corporation

- 6.4.12 Nuance Communications, Inc.

- 6.4.13 Medtronic plc

- 6.4.14 Intuitive Surgical, Inc.

- 6.4.15 Tempus Labs, Inc.

- 6.4.16 PathAI, Inc.

- 6.4.17 Butterfly Network, Inc.

- 6.4.18 Viz.ai, Inc.

- 6.4.19 Insilico Medicine, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

基於代理的人工智慧自動化市場預測至2034年-按部署模式、企業規模、技術水平、功能應用、最終用戶和地區分類的全球分析

基於代理的人工智慧自動化市場預測至2034年-按部署模式、企業規模、技術水平、功能應用、最終用戶和地區分類的全球分析 基於代理商的商業、人工智慧編配和自主支付市場:2026 年

基於代理商的商業、人工智慧編配和自主支付市場:2026 年 基於代理的人工智慧開發平台:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

基於代理的人工智慧開發平台:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 基於代理的人工智慧市場:按組件、部署類型、企業規模、最終用戶、國家和地區分類-行業分析、市場規模、市場佔有率及2026年至2033年預測無障礙學習技術市場預測至2034年-全球分析(按組件、殘疾類型、部署模式、技術、應用、最終用戶和地區分類)

基於代理的人工智慧市場:按組件、部署類型、企業規模、最終用戶、國家和地區分類-行業分析、市場規模、市場佔有率及2026年至2033年預測無障礙學習技術市場預測至2034年-全球分析(按組件、殘疾類型、部署模式、技術、應用、最終用戶和地區分類) 全球基於代理的人工智慧安全市場(至 2032 年):按安全功能和工具(即時安全工具、防護框架、人工智慧穿透測試和紅隊工具)和部署層級分類

全球基於代理的人工智慧安全市場(至 2032 年):按安全功能和工具(即時安全工具、防護框架、人工智慧穿透測試和紅隊工具)和部署層級分類 全球基於代理的人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球人工智慧購物代理和基於代理的商務(2026):部署趨勢和實施限制基於代理的人工智慧市場預測至2034年:按部署類型、功能、最終用戶和地區分類的全球分析Agentic企業軟體:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)

全球基於代理的人工智慧市場規模、佔有率、趨勢和成長分析報告(2026-2034)全球人工智慧購物代理和基於代理的商務(2026):部署趨勢和實施限制基於代理的人工智慧市場預測至2034年:按部署類型、功能、最終用戶和地區分類的全球分析Agentic企業軟體:市佔率分析、產業趨勢與統計、成長預測(2026-2031年)