|

市場調查報告書

商品編碼

2063426

紅外線(IR)LED晶片:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031年)Infrared (IR) LED Chip - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

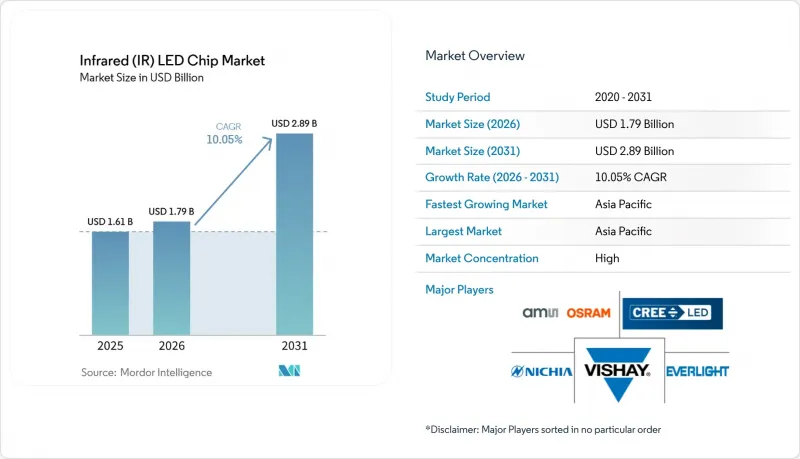

根據 Mordor Intelligence 預測,紅外線 (IR) LED 晶片市場將從 2025 年的 16.1 億美元成長到 2026 年的 17.9 億美元,到 2031 年達到 28.9 億美元,2026 年至 2031 年的複合年成長率為 10.1%。

本報告按波長範圍(近紅外線、短波紅外線和擴展紅外線)、功率輸出(低功率、中功率、高功率)、應用領域(家用電子電器、汽車、工業和機器視覺、安防監控、醫療保健)以及地區進行細分。市場預測以美元計價。

全球紅外線(IR)LED晶片市場趨勢及洞察

家用電子電器的普及率不斷提高

智慧型手機製造商正在重新定位有機發光二極體顯示器背面的紅外線發送器,以實現螢幕下人臉部認證。這種設計變更有利於能夠穿過吸收層並提供高輻射通量的小型晶片。 850奈米陣列正被應用於行動電話、平板電腦、智慧音箱和擴增實境(AR)頭顯,以及手勢姿態辨識和深度映射。在消費級穿戴裝置領域,使用830-850奈米LED刺激膠原蛋白產生的FDA核准的治療面膜正變得越來越普及,擴大了潛在市場規模(TAM)。向美容和健康領域的多元化發展減少了對定期更換智慧型手機的依賴,並支撐了對小型高效能晶片的持續需求。因此,隨著設備製造商需要更薄的封裝和更窄的波長範圍以保持生物識別精度,紅外線LED晶片市場需求穩定。

汽車駕駛監控和ADAS系統的擴展

歐洲新車安全評鑑協會 (Euro NCAP) 2026 年的評測協議將為眼動追蹤駕駛監控系統授予最高 25 分的安全加分,這實際上意味著乘用車必須配備近紅外線照明。美國和中國的監管機構也制定了類似的法規,推動了全球對符合 AEC-Q102 認證、可在 -40 度C至 125 度C溫度範圍內保持波長穩定性的近發送器的需求。供應商正積極響應,推出五結雷射二極體,以提高峰值光輸出,同時降低電流消耗和發熱量,使雷射雷達模組能夠探測 200 公尺以外的物體。一級整合商已開始進行量產認證,並與主要代工廠簽署多年供貨協議,以確保市場佔有率。這些要求正在加速近紅外線 LED 晶片的普及應用,並鞏固其在安全電子產品發展藍圖中的關鍵地位。

激烈的競爭給利潤率帶來了壓力。

為因應原物料成本飆升,中國製造商計劃到2025年將平均售價提高5%至10%,但全球LED構裝銷售仍下降4%,顯示通用型LED封裝存在供應過剩。垂直整合提供了一定的保護,台灣和歐洲的成熟企業專注於微型LED和雷射架構,以避免價格競爭。三安光電正在收購Lumileds,此舉有望產生成本協同效應效應,並對歐洲汽車LED價格構成壓力。缺乏自主智慧財產權的中小型供應商面臨利潤率下降和被擠出市場的風險,這一趨勢正在加速紅外線LED晶片產業的產業重組。

細分市場分析

到2025年,波長為850-950奈米的近紅外線頻寬將佔據紅外線(IR)LED晶片市場銷售額的一半以上,這反映出該波段能夠與低成本的矽光電檢測器無縫整合,並在智慧型手機、汽車駕駛員監控和安防攝影機等領域得到廣泛應用。波段為1000-1700奈米的短波紅外線裝置預計將在2031年之前保持最高的年成長率,達到10.68%,因為食品加工商和回收商正在採用高光譜遙測分類機來識別可見光系統無法檢測到的聚合物和水分含量。

Cimbria 的 SEA.HY分類機和 Imec 的簡介成像器展示了精確的波長控制如何提高即時處理生產線的分類精度。歐盟的回收義務和北美的食品安全法規正在推動要素對頻譜範圍更窄的晶片的需求,並推高其價格。波長超過 1700 奈米的長波紅外線解決方案適用於航太領域,但銦鎵砷 (IGAr)檢測器的高成本限制了其銷售量。外延片均勻性和封裝散熱器技術的不斷創新,正在增強短波解決方案在廣闊的紅外線 (IR) LED 晶片市場中的價值提案。

區域分析

預計到2025年,亞太地區將佔紅外線(IR)LED晶片市場銷售額的49.53%,年複合成長率(CAGR)為11.22%,主要得益於中國大陸、台灣和韓國廠商擴大其外延和封裝產能。三安光電累計2025年上半年銷售額達89.87億元人民幣(約12.4億美元),年增17.03%,反映其產品在豪華汽車和消費性電子領域的滲透率進一步提高。台灣的恩諾斯達(Ennostar)正轉向微型LED和垂直共振腔面射型雷射(VCSEL)以避免因產品同質化而導致的價格下跌,而日本供應商則專注於符合汽車品質標準的分立式功率裝置。區域產業園區的垂直整合正在縮短週期,並為紅外線LED晶片市場建立具有競爭力的成本基礎。

北美和歐洲的進展較為緩慢,但它們在汽車認證和國防項目中發揮著至關重要的作用。 ams OSRAM 已成功從歐盟資金籌措,用於在奧地利建設一座價值 14 億歐元(15.8 億美元)的後端工廠,該工廠將作為對沖亞洲供應風險的戰略屏障。 ams OSRAM 與日亞化學工業株式會社之間的專利交叉授權解決了訴訟糾紛,並促進了對下一代發送器的投資。這些地區也是光生物安全性和電磁相容性一致性測試的中心,確保全球汽車和醫療設備製造商能夠採納相關設計。

儘管南美和中東/非洲的市場佔有率較小,但它們正受益於需要夜視監控和交通分析的基礎設施項目。在中東,保護關鍵資產是重中之重,推動了940奈米隱蔽攝影機的大規模部署。歐洲的隱私法規可能會減緩生物識別技術的普及,但能夠成功應對這些分散法規的供應商正在實現地理均衡成長。因此,區域趨勢正在推動紅外線LED晶片市場的發展,亞太地區保持著供應優勢,而其他地區也擁有高階細分市場。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 家用電子電器的擴張

- 具備夜視功能的安防監視錄影機的需求正在成長。

- 汽車駕駛監控和ADAS系統的擴展

- 在醫療診斷和穿戴式裝置領域的應用日益廣泛

- 將短波紅外線(SWIR)高光譜影像技術應用於食品和回收物分類。

- 採用低功耗紅外線LED陣列的非接觸式智慧零售貨架

- 市場限制因素

- 激烈的競爭給利潤率帶來了壓力。

- 高輻射通量下溫度控管面臨的挑戰

- 鎵和砷監管對供應鏈的脆弱性

- 隱私權問題限制了生物識別技術的大規模部署。

- 產業供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

- 宏觀經濟因素對市場的影響

第5章 市場規模與成長預測

- 按波長範圍

- 近紅外線

- 短波紅外線

- 擴展紅外線

- 依輸出類型

- 低功率

- 中功率

- 高功率

- 透過使用

- 家用電子產品

- 車

- 工業和機器視覺

- 安全監控

- 醫療保健

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 印度

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- ams OSRAM AG

- Nichia Corporation

- Everlight Electronics Co., Ltd.

- Cree LED

- Vishay Intertechnology, Inc.

- Epistar Corporation

- Lite-On Technology Corporation

- Lextar Electronics Corporation

- Kingbright Company, LLC

- Lumileds Holding BV

- High Power Lighting Corporation

- EPILEDS Technologies Inc.

- ROHM Co., Ltd.

- ON Semiconductor Corporation

- Ushio Inc.

- Marktech Optoelectronics

- Excelitas Technologies Corp.

- Toyoda Gosei Co., Ltd.

- Samsung Electronics Co., Ltd.

- Stanley Electric Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the infrared (IR) LED chip market size is expected to increase from USD 1.61 billion in 2025 to USD 1.79 billion in 2026 and reach USD 2.89 billion by 2031, growing at a CAGR of 10.1% over 2026-2031.

This report is Segmented by Wavelength Range (Near Infrared, Short-Wave Infrared, and Extended Infrared), Power Output (Low Power, Medium Power, and High Power), Application (Consumer Electronics, Automotive, Industrial and Machine Vision, Security and Surveillance, and Healthcare and Medical), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Infrared (IR) LED Chip Market Trends and Insights

Rising Adoption In Consumer Electronics

Smartphone makers are repositioning infrared emitters behind organic light-emitting diode displays to enable under-screen facial recognition, a redesign that favors miniaturized chips that deliver high radiant flux through absorptive stack layers. Beyond handsets, tablets, smart speakers, and augmented-reality headsets, 850-nanometer arrays are embedded for gesture recognition and depth mapping. Consumer wearables benefit from FDA-cleared therapy masks that use 830-850-nanometer LEDs to stimulate collagen, widening the total addressable market. Diversification into beauty and wellness reduces dependence on cyclical phone refreshes and supports recurring demand for compact, high-efficiency chips. The result is steady pull-through for the infrared LED chip market as device makers seek thinner packages and tighter wavelength bins to maintain biometric accuracy.

Expansion Of Automotive Driver Monitoring And ADAS Systems

Euro NCAP's 2026 protocol awards up to 25 safety points for eye-tracking driver monitoring, effectively making near-infrared illumination mandatory in passenger cars. U.S. and Chinese regulators are drafting similar language, synchronizing global demand for AEC-Q102 qualified emitters that remain wavelength-stable from -40 °C to 125 °C. Suppliers respond with five-junction laser diodes that lift peak optical power while easing current draw and heat generation, enabling LiDAR modules to detect objects beyond 200 meters. Tier-one integrators have begun high-volume qualification, anchoring multiyear supply agreements that lock in share for leading foundries. These mandates accelerate adoption curves and reinforce the pivotal role of the infrared LED chip market in the safety electronics roadmap.

Intense Price Competition Compressing Margins

Chinese producers lifted average selling prices 5-10% in 2025 to offset raw material inflation, yet global LED packaging revenue still slipped 4%, signaling oversupply in commodity grades. Vertical integration offers partial insulation, with Taiwanese and European incumbents focusing on microLED and laser architectures to escape price wars. Sanan's pending acquisition of Lumileds adds cost synergy that could pressure European automotive LED pricing. Smaller suppliers without differentiated intellectual property face margin squeeze and potential exit, a dynamic that keeps consolidation high throughout the infrared LED chip industry.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand For Night-Vision Security And Surveillance Cameras

- Increasing Use In Healthcare Diagnostics And Wearable Devices

- Supply-Chain Vulnerability To Gallium And Arsenic Restrictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The near-infrared band between 850-950 nanometers accounted for more than half of the infrared (IR) LED chip market 2025 revenue, reflecting its seamless pairing with low-cost silicon photodetectors and entrenched position in smartphones, automotive driver monitoring, and security cameras. Short-wave infrared devices spanning 1,000-1,700 nanometers are projected to register the fastest growth at 10.68% annually through 2031 as food processors and recyclers adopt hyperspectral sorters that identify polymers and moisture levels invisible to visible-light systems.

Cimbria's SEA.HY sorter and Imec's snapshot imager demonstrate how precise wavelength control improves classification accuracy in real-time processing lines. European Union recycling mandates and North American food-safety regulations act as pull factors, supporting premium pricing for chips with tighter spectral bins. Although extended-infrared solutions beyond 1,700 nanometers cater to aerospace, the higher cost of indium gallium arsenide detectors constrains volume. Continuous innovation in epi-wafer uniformity and packaging heatsinks strengthens the value proposition of short-wave solutions within the broader infrared (IR) LED chip market.

Geography Analysis

Asia-Pacific generated 49.53% of the infrared (IR) LED chip market's 2025 revenue and is on track for an 11.22% CAGR as Chinese, Taiwanese, and South Korean vendors expand epitaxial and packaging capacity. Sanan Optoelectronics posted RMB 8.987 billion (USD 1.24 billion) first-half-2025 revenue, up 17.03%, reflecting deeper penetration into premium automotive and consumer segments. Taiwan's Ennostar shifts toward microLED and vertical-cavity surface-emitting lasers to escape commodity pricing, while Japanese suppliers focus on discrete power devices supporting automotive quality standards. Vertical integration within regional industrial parks compresses cycle times and underpins the infrared LED chip market's competitive cost base.

North America and Europe advance more slowly but play a pivotal role in automotive qualification and defense programs. ams OSRAM secured EUR 227 million (USD 256 million) of EU funding to build a EUR 1.4 billion (USD 1.58 billion) back-end facility in Austria, a strategic hedge against Asian supply risk. Patent cross-licensing between ams OSRAM and Nichia resolves litigation distraction and channels investment into next-generation emitters. These regions also anchor compliance testing for photobiological safety and electromagnetic compatibility, locking in design-wins from global carmakers and medical device firms.

South America, the Middle East, and Africa hold smaller shares but benefit from infrastructure projects that require night-vision surveillance and traffic analytics. The Middle East prioritizes critical-asset protection, supporting large-scale deployments of covert 940 nanometer cameras. European privacy legislation may slow biometric roll-outs, but suppliers able to navigate fragmented regulations capture geographically balanced growth. Consequently, regional dynamics preserve Asia-Pacific's supply dominance while sustaining premium niches elsewhere within the infrared LED chip market.

- ams OSRAM AG

- Nichia Corporation

- Everlight Electronics Co., Ltd.

- Cree LED

- Vishay Intertechnology, Inc.

- Epistar Corporation

- Lite-On Technology Corporation

- Lextar Electronics Corporation

- Kingbright Company, LLC

- Lumileds Holding B.V.

- High Power Lighting Corporation

- EPILEDS Technologies Inc.

- ROHM Co., Ltd.

- ON Semiconductor Corporation

- Ushio Inc.

- Marktech Optoelectronics

- Excelitas Technologies Corp.

- Toyoda Gosei Co., Ltd.

- Samsung Electronics Co., Ltd.

- Stanley Electric Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption in Consumer Electronics

- 4.2.2 Growing Demand for Night-Vision Security and Surveillance Cameras

- 4.2.3 Expansion of Automotive Driver Monitoring and ADAS Systems

- 4.2.4 Increasing Use in Healthcare Diagnostics and Wearable Devices

- 4.2.5 Integration with SWIR Hyperspectral Imaging for Food and Recycling Sorting

- 4.2.6 Contactless Smart-Retail Shelves Using Low-Power IR LED Arrays

- 4.3 Market Restraints

- 4.3.1 Intense Price Competition Compressing Margins

- 4.3.2 Thermal Management Challenges at High Radiant Flux

- 4.3.3 Supply-Chain Vulnerability to Gallium and Arsenic Restrictions

- 4.3.4 Privacy Concerns Limiting Large-Scale Biometric Deployments

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Wavelength Range

- 5.1.1 Near Infrared

- 5.1.2 Short-Wave Infrared

- 5.1.3 Extended Infrared

- 5.2 By Power Output

- 5.2.1 Low Power

- 5.2.2 Medium Power

- 5.2.3 High Power

- 5.3 By Application

- 5.3.1 Consumer Electronics

- 5.3.2 Automotive

- 5.3.3 Industrial and Machine Vision

- 5.3.4 Security and Surveillance

- 5.3.5 Healthcare and Medical

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 South Korea

- 5.4.3.4 India

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ams OSRAM AG

- 6.4.2 Nichia Corporation

- 6.4.3 Everlight Electronics Co., Ltd.

- 6.4.4 Cree LED

- 6.4.5 Vishay Intertechnology, Inc.

- 6.4.6 Epistar Corporation

- 6.4.7 Lite-On Technology Corporation

- 6.4.8 Lextar Electronics Corporation

- 6.4.9 Kingbright Company, LLC

- 6.4.10 Lumileds Holding B.V.

- 6.4.11 High Power Lighting Corporation

- 6.4.12 EPILEDS Technologies Inc.

- 6.4.13 ROHM Co., Ltd.

- 6.4.14 ON Semiconductor Corporation

- 6.4.15 Ushio Inc.

- 6.4.16 Marktech Optoelectronics

- 6.4.17 Excelitas Technologies Corp.

- 6.4.18 Toyoda Gosei Co., Ltd.

- 6.4.19 Samsung Electronics Co., Ltd.

- 6.4.20 Stanley Electric Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment