|

市場調查報告書

商品編碼

1959577

紅外線LED市場機會、成長要素、產業趨勢分析及2026年至2035年預測Infrared (IR) LED Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

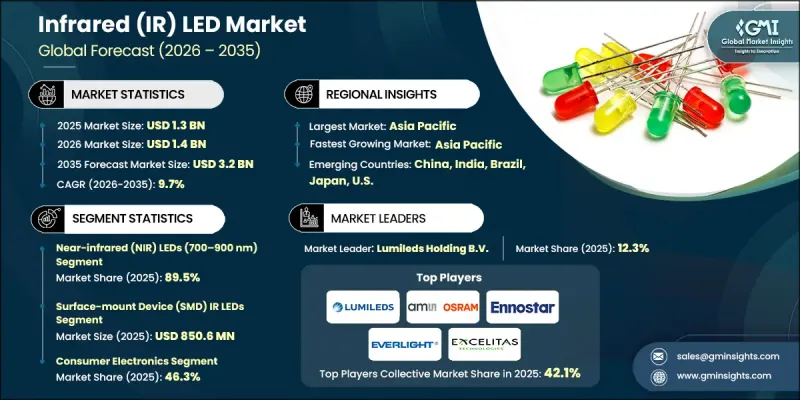

2025 年全球紅外線 (IR) LED 市場價值為 13 億美元,預計到 2035 年將達到 32 億美元,年複合成長率為 9.7%。

市場擴張的驅動力來自消費科技領域的日益融合、汽車感測和安全平台的廣泛應用、工廠自動化和視覺系統的加速普及、生物識別和醫療解決方案的日益廣泛應用,以及安防監控基礎設施的持續需求。紅外線LED設計的進步著重於系統級效率的提升,而非單一組件性能的增強,從而在降低熱應力的同時實現更高的輻射輸出。這些性能的提升簡化了封裝要求,延長了使用壽命,並實現了更緊湊的外形規格。短期內,效率的逐步提升將持續累積;而中期來看,發展趨勢表明,原始設備製造商(OEM)正朝著直接調整其產品架構以適應這些改進的紅外線性能特性的方向發展。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 13億美元 |

| 預測金額 | 32億美元 |

| 複合年成長率 | 9.7% |

消費性電子產品仍是整體需求的最大貢獻者,這主要得益於感測精度、能源效率和小型化技術的不斷提升。製造商正從傳統的材料結構轉向更先進的異質結構設計,以抑制高電流下的效率下降並提高光提取效率。這種轉變使得晶粒尺寸更小、亮度更高,從而支援更薄的模組和更佳的散熱控制。對系統級效能的日益重視,使整合商能夠實現更長的運作週期和更大的設計柔軟性。

預計2026年至2035年間,短波紅外線LED市場將以11.8%的複合年成長率成長。對短波紅外線(SWIR)技術的需求主要來自於需要更長波長性能的應用,這些應用能夠提供更強的滲透性、更高的探測精度和更可靠的成像效果。儘管該細分市場目前在總出貨量中所佔比例較小,但由於其在高價值環境中的應用,其收入成長仍然強勁,在這些環境中,性能比成本更為重要。技術的不斷進步以及在專業工業、醫療和國防相關系統中的日益普及,支撐了SWIR產品的高價位結構和持續的研發投入。

預計2026年至2035年間,汽車和交通運輸業將以13.5%的複合年成長率成長,成為成長最快的終端用戶產業之一。這一成長與高級駕駛輔助系統(ADAS)架構、車載監控平台以及半自動駕駛和自動駕駛系統的日益普及密切相關。電動車產量的成長和全球安全標準的日益嚴格正在加速紅外線LED在乘員檢測、車載感知和弱光輔助功能方面的應用。這些應用對產品的可靠性和使用壽命提出了更高的要求,從而為高利潤產品創造了機遇,並促進了汽車供應鏈中供應商之間深厚合作關係的建立。

預計到2025年,北美紅外線(IR)LED市場佔有率將達到20.7%。該地區作為主要需求中心的地位依然穩固,這得益於汽車製造、工業自動化和國防相關項目的強勁需求。智慧感測技術的快速普及,以及成熟的製造業基礎,正在推動全部區域的持續成長。美國和加拿大仍然是先進感測器整合、微機電系統(MEMS)和高性能光電元件投資的重點,所有這些都為紅外線LED的穩定長期需求做出了貢獻。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 家用電子電器的普及率不斷提高

- 在汽車感測和安全系統中得到更廣泛的應用

- 工業自動化和機器視覺的擴展

- 對生物識別和醫療保健應用的需求日益成長

- 安全和監控系統的發展

- 產業潛在風險與挑戰

- 高功率長波長紅外線LED的技術局限性

- 對零件供應鏈的依賴和半導體短缺

- 市場機遇

- 穿戴式和攜帶式醫療設備的成長

- 智慧家庭和物聯網設備的應用日益普及

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格趨勢

- 按地區

- 依產品

- 定價策略

- 新興經營模式

- 合規要求

- 專利和智慧財產權分析

- 地緣政治和貿易趨勢

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 市場集中度分析

- 按地區

- 主要企業的競爭標竿分析

- 財務績效比較

- 收入

- 利潤率

- 研究與開發

- 產品系列比較

- 產品線的廣度

- 科技

- 創新

- 地理位置比較

- 全球擴張分析

- 服務網路覆蓋

- 按地區分類的市場滲透率

- 競爭定位矩陣

- 領導企業

- 受讓人

- 追蹤者

- 小眾玩家

- 戰略展望矩陣

- 財務績效比較

- 主要進展

- 併購

- 夥伴關係與合作

- 技術進步

- 擴張和投資策略

- 數位轉型計劃

- 新興/Start-Ups競爭對手的發展趨勢

第5章 市場估計與預測:依波長範圍分類,2022-2035年

- 近紅外線(NIR)LED(700-900奈米)

- 短波長紅外線(SWIR)LED(900-1000+nm)

第6章 市場估計與預測:依產量分類,2022-2035年

- 低功率紅外線LED(≤100毫瓦)

- 中功率紅外線LED(100毫瓦至1瓦)

- 高功率紅外線LED(超過1瓦)

第7章 市場估價與預測:依包裝類型分類,2022-2035年

- 通孔紅外線發光二極體

- 表面黏著技術(SMD)紅外線LED

- 其他

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 感測和接近檢測

- 生物識別

- 用於成像和夜視的紅外線照明

- 遠端控制和人機介面(HMI)

- 光纖通訊和數據傳輸

- 其他

第9章 市場估計與預測:依最終用途產業分類,2022-2035年

- 家用電子電器

- 醫療及醫療設備

- 汽車/運輸設備

- 安全、國防和執法機關

- 工業製造

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第11章:公司簡介

- 主要企業

- Lumileds Holding BV

- ams-OSRAM AG

- Ennostar Inc.

- Everlight Electronics Co., Ltd.

- Excelitas Technologies Corp.

- 按地區分類的主要企業

- 北美洲

- Broadcom

- Luminus, Inc.

- Vishay Intertechnology, Inc.

- 亞太地區

- Kingbright

- DOWA Electronics Materials Co., Ltd.

- Stanley Electric Co., Ltd.

- Hamamatsu Photonics KK

- 歐洲

- Wurth Elektronik eiSos GmbH &Co. KG

- Dialight

- 北美洲

- 特殊玩家/干擾者

- Boston Electronics

- Marktech Optoelectronics Inc.

The Global Infrared (IR) LED Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 9.7% to reach USD 3.2 billion by 2035.

Market expansion is fueled by rising integration across consumer-focused technologies, stronger deployment within automotive sensing and safety platforms, accelerating adoption in factory automation and vision-based systems, increasing utilization in biometric identification and healthcare solutions, and sustained demand from security and monitoring infrastructures. Advancements in infrared LED design are focused on improving system-level efficiency rather than isolated component gains, allowing higher radiant output with reduced thermal stress. These performance improvements simplify packaging requirements, extend operational lifecycles, and enable more compact form factors. In the near term, gradual efficiency enhancements continue to accumulate, while mid-term development trends show original equipment manufacturers aligning product architectures directly with these improved infrared performance characteristics.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 9.7% |

Consumer-oriented electronics remain the largest contributor to overall demand, driven by continuous upgrades in sensing accuracy, power efficiency, and miniaturization. Manufacturers are transitioning away from traditional material structures toward more advanced heterostructure designs that limit efficiency degradation at elevated current levels and improve light extraction. This shift enables smaller die sizes with higher brightness output, supporting thinner modules and improved thermal control. The emphasis is increasingly placed on achieving higher performance at the system level, which allows longer operating cycles and greater design flexibility for integrators.

The short-wave infrared LED segment is forecast to register a CAGR of 11.8% during 2026-2035. Demand for SWIR technology is being driven by applications that require longer wavelength performance to achieve enhanced penetration, higher detection accuracy, and improved imaging reliability. Although this segment currently accounts for a smaller share of total shipments, revenue growth remains strong due to its use in high-value environments where performance outweighs cost sensitivity. Ongoing technical refinement and expanding acceptance across specialized industrial, medical, and defense-related systems are supporting premium pricing structures and sustained investment in SWIR development.

The automotive and transportation segment is expected to grow at a CAGR of 13.5% during 2026-2035, making it one of the fastest-growing end-use segments. Growth is linked to the rising deployment of advanced driver-assistance architectures, in-cabin monitoring platforms, and semi-autonomous and autonomous mobility systems. Increased production of electric vehicles and stricter global safety mandates are accelerating the integration of infrared LEDs for occupant detection, interior sensing, and low-light assistance functions. These applications demand high reliability and long operational life, creating opportunities for higher-margin products and deeper supplier relationships within the automotive supply chain.

North America Infrared (IR) LED Market accounted for 20.7% share in 2025. The region continues to serve as a key demand center, supported by strong activity across automotive manufacturing, industrial automation, and defense-related programs. Rapid adoption of smart sensing technologies, combined with a well-established manufacturing base, underpins consistent regional growth. The United States and Canada remain focal points for investment in advanced sensor integration, microelectromechanical systems, and performance-driven optoelectronic components, all of which contribute to stable long-term demand for infrared LEDs.

Key participants operating in the Global Infrared (IR) LED Market include ams-OSRAM AG, Vishay Intertechnology, Inc., Everlight Electronics Co., Ltd., Stanley Electric Co., Ltd., Broadcom, Lumileds Holding B.V., Wurth Elektronik eiSos GmbH & Co. KG, Hamamatsu Photonics K.K., Ennostar Inc., Luminus, Inc., Marktech Optoelectronics Inc., Dialight, Excelitas Technologies Corp., Kingbright, DOWA Electronics Materials Co., Ltd., and Boston Electronics. Companies operating in the Global Infrared (IR) LED Market are actively strengthening their market position through a combination of technology innovation, portfolio diversification, and strategic partnerships. A strong focus is placed on developing higher-efficiency emitters with improved thermal performance and longer operating lifespans to meet evolving system-level requirements. Many players are investing in advanced packaging techniques and wafer-level optimization to reduce form factors while enhancing output consistency. Expansion into high-growth application segments such as automotive sensing, industrial automation, and medical diagnostics is another key strategy, often supported by long-term supply agreements.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Wavelength range trends

- 2.2.2 Power output trends

- 2.2.3 Packaging type trends

- 2.2.4 Application trends

- 2.2.5 End-use industry trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption in consumer electronics

- 3.2.1.2 Increasing use in automotive sensing & safety systems

- 3.2.1.3 Expansion of industrial automation & machine vision

- 3.2.1.4 Growing demand for biometric and healthcare applications

- 3.2.1.5 Growth in security & surveillance systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Technical limitations in high-power and long-wavelength IR LEDs

- 3.2.2.2 Dependence on component supply chain and semiconductor shortages

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in wearable and portable healthcare devices

- 3.2.3.2 Increasing adoption in smart homes and IoT devices

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Wavelength Range, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Near-infrared (NIR) LEDs (700-900 nm)

- 5.3 Short-wave infrared (SWIR) LEDs (900-1,000+ nm)

Chapter 6 Market Estimates and Forecast, By Power Output, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Low-power IR LEDs (≤100 mW)

- 6.3 Medium-power IR LEDs (100 mW-1 W)

- 6.4 High-power IR LEDs (>1 W)

Chapter 7 Market Estimates and Forecast, By Packaging Type, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Through-hole IR LEDs

- 7.3 Surface-mount device (SMD) IR LEDs

- 7.4 Others

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Sensing & proximity detection

- 8.3 Biometric identification

- 8.4 IR illumination for imaging & night vision

- 8.5 Remote control & human-machine interface (HMI)

- 8.6 Optical communication & data transmission

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 Consumer electronics

- 9.3 Healthcare & medical devices

- 9.4 Automotive & transportation

- 9.5 Security, defense & law enforcement

- 9.6 Industrial manufacturing

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Lumileds Holding B.V.

- 11.1.2 ams-OSRAM AG

- 11.1.3 Ennostar Inc.

- 11.1.4 Everlight Electronics Co., Ltd.

- 11.1.5 Excelitas Technologies Corp.

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Broadcom

- 11.2.1.2 Luminus, Inc.

- 11.2.1.3 Vishay Intertechnology, Inc.

- 11.2.2 Asia Pacific

- 11.2.2.1 Kingbright

- 11.2.2.2 DOWA Electronics Materials Co., Ltd.

- 11.2.2.3 Stanley Electric Co., Ltd.

- 11.2.2.4 Hamamatsu Photonics K.K.

- 11.2.3 Europe

- 11.2.3.1 Wurth Elektronik eiSos GmbH & Co. KG

- 11.2.3.2 Dialight

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 Boston Electronics

- 11.3.2 Marktech Optoelectronics Inc.