|

市場調查報告書

商品編碼

2063386

石油和天然氣行業閥門:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Valves In Oil And Gas Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

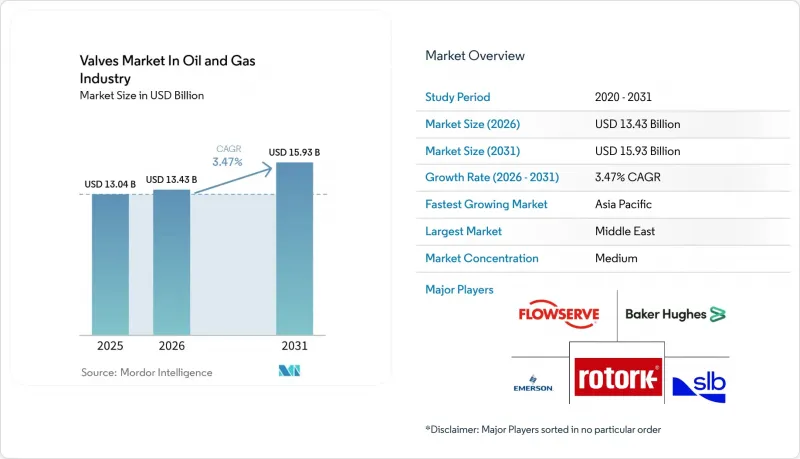

根據 Mordor Intelligence 預測,石油和天然氣產業的閥門市場規模將從 2025 年的 130.4 億美元成長到 2026 年的 134.3 億美元,到 2031 年達到 159.3 億美元,複合年成長率為 3.47%。

本報告按閥門類型(球閥、閘閥、截止閥及其他)、材質(鑄鋼、鍛鋼、不銹鋼及其他)、應用領域(上游、中游及其他)、操作方式(手動、氣動及其他)、尺寸(6英寸及以下、6-12英寸、12-24英寸及其他)和地區進行分類。市場預測以美元計價。

石油和天然氣行業閥門市場的趨勢和發展

擴大上游和中游管道項目

儘管年減4%,但預計2025年上游支出將回升至5,700億美元,分析師預測2030年將增至7,380億美元。巴西深海開發案和沙烏地阿拉伯非常規天然氣開發案已簽署多年期契約,採購適用於酸性天然氣的高壓閘閥和球閥。中游領域的成長情況類似,Enbridge公司已批准一項價值14億美元的天然氣管道項目,該項目計劃於2024年完工;ADNOC公司也投資24億美元建設海水注入網路,該網路需要耐腐蝕止回閥。中國國家電網公司正在建造48吋主幹管道,這將推高對24吋以上尺寸閥門的需求。符合API 6D和ISO 15848標準現已成為採購的標配要求。

LNG接收站建設快速成長

到2030年,預計每年將新增約3000億立方米液化產能,其中一項已批准的800億立方米項目將於2025年投產,將引領這一成長。卡達能源公司投資300億美元的北方氣田擴建計畫將使年產能提升至1.26億噸,這將需要數千個低溫球閥和三偏心蝶閥,這些閥門的設計能夠承受-196 度C環境。印度、越南和菲律賓的進口碼頭將優先選擇擁有本地庫存並獲得貝克休斯API 6FA耐火認證的供應商。合金鋼和雙相鋼的年複合成長率將達到4.72%,它們將有助於抵消液化天然氣設施特有的熱循環損害。 EPC合約中的本地售後服務條款對遠距離供應商構成了准入障礙。

原油價格波動抑制了資本投資。

2024年至2025年間,布蘭特原油價格在每桶70至90美元之間波動,最終投資決策停滯不前,獲利能力較弱的項目的閥門訂單減少。由於頁岩油業者優先考慮自由現金流而非成長,2025年上游支出較去年同期下降4%至5,700億美元。二疊紀盆地的生產商推遲了管道連接,導致井口閥門需求放緩。同時,北海和墨西哥灣的資產選擇退役而非更換昂貴的海底設備。由於業者不願持有儲備庫存,累積訂單在景氣衰退衰退期間的減少速度比復甦時期更快。因此,供應商面臨收入的周期性波動,使生產計畫更加複雜。

細分市場分析

借助數位雙胞胎技術,控制閥預計將以5.12%的複合年成長率成長,超過石油和天然氣行業閥門市場的整體成長速度。到2025年,球閥將在開關應用中保持33.53%的市場佔有率,而閘閥將在高壓鑽井和海底採油樹領域佔據主導地位。旋塞閥和蝶閥正在磨蝕性漿料和大直徑低壓管線等領域開拓利基市場。隨著預測分析驅動的產能最佳化不斷推進,石油和天然氣控制閥市場預計將持續成長。

預測性維護可確保控制閥的運轉率保持在高水平,操作員除了需要進行 API 607 防火檢查外,還必須進行 ISO 15848 洩漏排放評估。電動執行機構提高了分切精度,並促進了控制閥的發展。每項新標準的推出都會提高進入門檻,從而保護那些擁有全球檢測設施和數位化服務體系的現有企業。

預計到2025年,鑄鋼的市場佔有率將達到27.31%,而合金鋼和雙相鋼的市場佔有率預計將以每年4.72%的速度成長,這主要得益於酸性氣體和氫氣混合氣體使用過程中對耐腐蝕性能要求的不斷提高。目前,卡達擴建的諾斯菲爾德製程生產線採用的是雙相鋼,而艾默生公司的HV-7000氫氣穩壓器則採用鎳合金。隨著NACE MR0175標準的普及,合金鋼閥門在石油和天然氣行業的市佔率預計將會擴大。

鍛鋼仍是10,000 psi井口設備必不可少的材料,而複合材料則用於低壓、高腐蝕性的胺裝置。強制性的材料識別和鋼廠檢驗報告增加了管理成本,這使得擁有整合冶金實驗室的現有供應商更具優勢。

區域分析

預計到2025年,亞太地區將佔全球銷售額的41.09%,這主要得益於中國管道和電網的一體化以及印度城市燃氣管網的發展。印度國家管網公司正在鋪設48吋主幹管道,這將推動對雙相鋼蝶閥的需求。同時,印度監管機構強制要求符合API 6D標準,並將低規格進口產品排除在市場之外。日本和韓國正在推進氫氣試點項目,從而催生了對鎳合金閥芯的利基需求。東南亞液化天然氣進口終端正在提高其再氣化能力,但由於資金籌措障礙,進展緩慢。

預計到2031年,中東地區的複合年成長率將達到4.76%。卡達能源公司的北部油田擴建項目需要數千個能夠承受低至-196°C低溫的低溫閥門;沙烏地阿拉伯的傑夫拉緻密氣開發項目需要耐硫化氫的雙相不銹鋼閥芯;阿布達比國家石油公司(ADNOC)的海水注入網路則需要用於高鹽度流體的耐腐蝕止回閥。該地區國有石油公司的資金支持使這些項目免受原油價格波動的影響,並維持了訂單的穩定來源。

在北美,墨西哥灣沿岸的液化天然氣出口工廠和從二疊紀盆地延伸的輸氣管道備受關注。美國已批准到2025年每年新增800億立方公尺液化產能,這將刺激對大口徑截止閥的需求。同時,墨西哥灣沿岸老舊平台的退役也持續推動對海底截止閥維修的需求。歐洲市場因油氣產量下降而萎縮,但正將重心轉向需要高壓二氧化碳閥的氫氣混合氣和碳捕集計畫。南美洲依賴巴西的鹽層下氣田和阿根廷的瓦卡穆埃爾塔(Vaca Muerta)基礎設施,而非洲的成長則依賴奈及利亞的天然氣貨幣化和莫三比克的液化天然氣,但政治風險阻礙了其發展勢頭。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 上游及中游管道工程擴建

- 加速推廣智慧燈泡

- 加強全球安全和排放氣體法規

- LNG接收站建設快速成長

- 用於能量轉換的氫氣相容閥門設計

- 老化的海上資產需要進行閥門維修

- 市場限制因素

- 原油價格波動抑制了資本投資。

- 向可再生能源轉型正在加速。

- 貿易關稅導致合金和不銹鋼價格大幅上漲。

- 互聯閥門網路面臨的網路安全風險日益增加。

- 工業價值、供應鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按閥門類型

- 球閥

- 閘閥

- 球閥

- 蝶閥

- 單向閥

- 塞閥

- 控制閥

- 材料

- 鑄鋼

- 鍛鋼

- 防鏽的

- 合金鋼和雙相鋼

- 非金屬/複合材料

- 透過使用

- 上游(開挖、隧道入口、人工抽水)

- 中游(管道、碼頭、儲槽)

- 下游(煉油、石化)

- 液化天然氣(LNG)設施

- 透過操作方法

- 手動的

- 氣動型

- 電的

- 液壓式、電液式

- 尺寸

- 6吋或更小

- 6-12英寸

- 12-24英寸

- 超過 24 英寸

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲地區

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Emerson Electric Co.

- Flowserve Corporation

- Schlumberger NV

- Baker Hughes Company

- Rotork plc

- Alfa Laval AB

- Crane Co.

- Metso Corporation

- KITZ Corporation

- IMI plc

- Samson AG

- Valmet Oyj

- Velan Inc.

- Honeywell International Inc.

- Parker Hannifin Corporation

- AVK Holding A/S

- CIRCOR International, Inc.

- The Weir Group plc

- Pentair plc

- Neway Valve(Suzhou)Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the valves market in oil and gas industry size is expected to grow from USD 13.04 billion in 2025 to USD 13.43 billion in 2026 and is forecast to reach USD 15.93 billion by 2031, advancing at a 3.47% CAGR.

This report is Segmented by Valve Type (Ball Valve, Gate Valve, Globe Valve, and More), Material (Cast Steel, Forged Steel, Stainless Steel, and More), Application (Upstream, Midstream, and More), Actuation Type (Manual, Pneumatic, and More), Size (Less Than 6 Inch, 6 To12 Inch, 12 To 24 Inch, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Insights and Trends of Valves Market In Oil And Gas Industry

Growing Upstream And Midstream Pipeline Projects

Upstream spending rebounded to USD 570 billion in 2025 despite a 4% year-over-year dip, and analysts see an upswing to USD 738 billion by 2030. Deepwater programs in Brazil and unconventional gas in Saudi Arabia are locking in multi-year contracts for high-pressure gate and ball valves rated for sour service.Midstream growth is similar, as Enbridge approved a USD 1.4 billion gas line in 2024 while ADNOC funded a USD 2.4 billion seawater-injection network that requires corrosion-resistant check valves. China's national grid is adding 48-inch trunk lines, boosting demand for valves above 24 inches. Compliance with API 6D and ISO 15848 is now standard procurement language.

Surge In LNG Terminal Constructions

Roughly 300 billion m3 per year of new liquefaction capacity is scheduled for completion by 2030, led by 80 billion m3 sanctioned in the United States during 2025. QatarEnergy's USD 30 billion North Field expansion raises capacity to 126 million tpa and needs thousands of cryogenic ball and triple-offset butterfly valves engineered for -196 °C duty. Import terminals across India, Vietnam, and the Philippines prefer suppliers with local inventory and API 6FA fire-testing certification from Baker Hughes. Alloy and duplex steels, growing at a 4.72% CAGR, counter thermal-cycling damage inherent in LNG service. Local after-sales clauses in EPC contracts raise barriers for distant vendors.

Crude Oil Price Volatility Dampening CAPEX

Brent fluctuated between USD 70 and USD 90 per barrel in 2024-2025, stalling final investment decisions and trimming valve orders for marginal projects. Upstream spending slipped 4% year over year to USD 570 billion in 2025, as shale operators favored free cash flow over growth. Permian producers deferred tie-ins, softening demand for wellhead valves, while North Sea and Gulf of Mexico assets leaned toward decommissioning rather than costly subsea replacements. Downturns shrink order books faster than recoveries expand them because operators hesitate to carry spare inventory. Suppliers thus face cyclic revenue swings that complicate production planning.

Other drivers and restraints analyzed in the detailed report include:

- Accelerating Adoption Of Digital And Smart Valves

- Stringent Global Safety And Emission Regulations

- Intensifying Shift Toward Renewable Energy

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Control valves, aided by digital twins, are expected to advance at a 5.12% CAGR, outpacing the overall valves market in oil and gas industry. Ball valves retained a 33.53% share in 2025 for on-off isolation, while gate valves dominate in high-pressure drilling and subsea trees. Plug and butterfly valves carve out niches in abrasive slurries and large-diameter low-pressure lines. The oil and gas industry's control valve market is projected to expand as predictive analytics sharpen throughput optimization.

Predictive maintenance keeps control-valve uptime high, compelling operators to specify ISO 15848 fugitive-emission ratings alongside API 607 fire testing. Electric actuation improves throttling accuracy, reinforcing the growth of control valves. Competitive entry barriers rise with each new standard, safeguarding incumbents that boast global test facilities and digital-service suites.

Cast steel held a 27.31% share in 2025, but alloy and duplex steels are forecast to grow 4.72% annually as sour-gas and hydrogen blends require enhanced corrosion resistance. Duplex grades now line Qatar's expanded North Field process trains, while nickel alloys equip Emerson's HV-7000 hydrogen regulator. The oil and gas industry's alloy steel valve market share is set to increase as NACE MR0175 compliance becomes routine.

Forged steel remains vital for 10,000 psi wellheads, whereas composite bodies are used for low-pressure, highly corrosive amine units. Positive material identification and mill test reports are mandatory, adding administrative cost that favors established suppliers with integrated metallurgy labs.

Geography Analysis

Asia-Pacific generated 41.09% of 2025 revenue, anchored by China's pipeline-grid integration and India's city-gas buildout. National Pipeline Network Company deploys 48-inch mains, raising the need for duplex-steel butterfly valves, while India's regulator demands API 6D compliance, shutting out low-spec imports. Japan and South Korea pursue hydrogen pilots, creating niche orders for nickel-alloy trim. Southeast Asian LNG import terminals are adding regas capacity but advancing slowly due to financing hurdles.

The Middle East is projected to have a 4.76% CAGR to 2031. QatarEnergy's North Field expansion specifies thousands of cryogenic valves engineered for minus 196 °C, and Saudi Arabia's Jafurah tight-gas development calls for hydrogen-sulfide-resistant duplex-steel trim. ADNOC's seawater-injection network demands corrosion-proof check valves for high-salinity fluids. Regional national-oil-company funding shields projects from crude swings, sustaining predictable order flows.

North America focuses on LNG export trains along the Gulf Coast and takeaway pipelines leaving the Permian Basin. The United States sanctioned 80 billion m3 per year of liquefaction capacity in 2025, triggering demand for large-diameter isolation valves. Meanwhile, the decommissioning of aging Gulf of Mexico platforms sustains retrofit activity for subsea isolation valves. Europe's market contracts amid declining hydrocarbon volumes, yet pivots to hydrogen blends and carbon-capture projects that require high-pressure CO2 valves. South America depends on Brazil's pre-salt fields and Argentina's Vaca Muerta infrastructure, while Africa's growth hinges on Nigerian gas monetization and Mozambique LNG, tempered by political risk.

- Emerson Electric Co.

- Flowserve Corporation

- Schlumberger N.V.

- Baker Hughes Company

- Rotork plc

- Alfa Laval AB

- Crane Co.

- Metso Corporation

- KITZ Corporation

- IMI plc

- Samson AG

- Valmet Oyj

- Velan Inc.

- Honeywell International Inc.

- Parker Hannifin Corporation

- AVK Holding A/S

- CIRCOR International, Inc.

- The Weir Group plc

- Pentair plc

- Neway Valve (Suzhou) Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Upstream and Midstream Pipeline Projects

- 4.2.2 Accelerating Adoption of Digital and Smart Valves

- 4.2.3 Stringent Global Safety and Emission Regulations

- 4.2.4 Surge in LNG Terminal Constructions

- 4.2.5 Hydrogen-Ready Valve Designs for Energy Transition

- 4.2.6 Aging Offshore Assets Requiring Valve Retrofits

- 4.3 Market Restraints

- 4.3.1 Crude Oil Price Volatility Dampening CAPEX

- 4.3.2 Intensifying Shift Toward Renewable Energy

- 4.3.3 Alloy and Stainless-Steel Cost Spikes from Trade Tariffs

- 4.3.4 Rising Cybersecurity Risks in Connected Valve Networks

- 4.4 Industry Value, Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Intensity of Competitive Rivalry

- 4.8.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Valve Type

- 5.1.1 Ball Valve

- 5.1.2 Gate Valve

- 5.1.3 Globe Valve

- 5.1.4 Butterfly Valve

- 5.1.5 Check Valve

- 5.1.6 Plug Valve

- 5.1.7 Control Valve

- 5.2 By Material

- 5.2.1 Cast Steel

- 5.2.2 Forged Steel

- 5.2.3 Stainless Steel

- 5.2.4 Alloy and Duplex Steels

- 5.2.5 Non-Metallic, Composite

- 5.3 By Application

- 5.3.1 Upstream (Drilling, Wellhead, Artificial Lift)

- 5.3.2 Midstream (Pipelines, Terminals, Storage)

- 5.3.3 Downstream (Refining, Petrochemical)

- 5.3.4 Liquefied Natural Gas (LNG) Facilities

- 5.4 By Actuation Type

- 5.4.1 Manual

- 5.4.2 Pneumatic

- 5.4.3 Electric

- 5.4.4 Hydraulic, Electro-Hydraulic

- 5.5 By Size

- 5.5.1 Less than 6 inch

- 5.5.2 6 to 12 inch

- 5.5.3 12 to 24 inch

- 5.5.4 More than 24 inch

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Australia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Kenya

- 5.6.6.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Emerson Electric Co.

- 6.4.2 Flowserve Corporation

- 6.4.3 Schlumberger N.V.

- 6.4.4 Baker Hughes Company

- 6.4.5 Rotork plc

- 6.4.6 Alfa Laval AB

- 6.4.7 Crane Co.

- 6.4.8 Metso Corporation

- 6.4.9 KITZ Corporation

- 6.4.10 IMI plc

- 6.4.11 Samson AG

- 6.4.12 Valmet Oyj

- 6.4.13 Velan Inc.

- 6.4.14 Honeywell International Inc.

- 6.4.15 Parker Hannifin Corporation

- 6.4.16 AVK Holding A/S

- 6.4.17 CIRCOR International, Inc.

- 6.4.18 The Weir Group plc

- 6.4.19 Pentair plc

- 6.4.20 Neway Valve (Suzhou) Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

工業閥門市場:依產品類型、材料、尺寸、驅動方式、最終用途產業和銷售管道-全球預測,2026-2032年

工業閥門市場:依產品類型、材料、尺寸、驅動方式、最終用途產業和銷售管道-全球預測,2026-2032年 全球工業閥門市場(至 2032 年):依閥門類型(截止閥、球閥、蝶閥、電磁閥、旋塞閥、彈簧閥、儲槽排氣閥、夾管閥、閘閥、隔膜閥、先導閥、止回閥、安全閥、針閥、洩壓閥)、尺寸(小於 1 英吋、先導閥、止回閥、安全閥、針閥、洩壓閥)、尺寸(小於 1 英吋、1-6 英吋、25 英吋大於英吋)和介質(液體、氣體、漿料)分類

全球工業閥門市場(至 2032 年):依閥門類型(截止閥、球閥、蝶閥、電磁閥、旋塞閥、彈簧閥、儲槽排氣閥、夾管閥、閘閥、隔膜閥、先導閥、止回閥、安全閥、針閥、洩壓閥)、尺寸(小於 1 英吋、先導閥、止回閥、安全閥、針閥、洩壓閥)、尺寸(小於 1 英吋、1-6 英吋、25 英吋大於英吋)和介質(液體、氣體、漿料)分類 工業閥門市場分析及預測(至2035年):類型、產品類型、技術、應用、材質、製程、最終用戶、功能、安裝配置、解決方案

工業閥門市場分析及預測(至2035年):類型、產品類型、技術、應用、材質、製程、最終用戶、功能、安裝配置、解決方案 工業閥門市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按類型、尺寸、等級和行業分類

工業閥門市場規模及預測(2021-2034),全球及區域佔有率、趨勢和成長機會分析報告:按類型、尺寸、等級和行業分類 工業閥門市場規模、佔有率、趨勢和預測:按產品類型、功能、材質、尺寸、最終用途行業和地區分類(2026-2034 年)拍擊閥市場:材質、尺寸、壓力等級、驅動方式、應用及通路分類-2026-2032年全球市場預測

工業閥門市場規模、佔有率、趨勢和預測:按產品類型、功能、材質、尺寸、最終用途行業和地區分類(2026-2034 年)拍擊閥市場:材質、尺寸、壓力等級、驅動方式、應用及通路分類-2026-2032年全球市場預測 工業閥門市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年)工業噴霧閥市場:2026-2032年全球市場預測(依產品類型、操作機構、材質、噴霧模式、應用及最終用戶產業分類)

工業閥門市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年)工業噴霧閥市場:2026-2032年全球市場預測(依產品類型、操作機構、材質、噴霧模式、應用及最終用戶產業分類) 2026-2030年全球石油天然氣工業閥門市場

2026-2030年全球石油天然氣工業閥門市場 工業閥門市場機會、成長要素、產業趨勢分析及2026-2035年預測

工業閥門市場機會、成長要素、產業趨勢分析及2026-2035年預測