|

市場調查報告書

商品編碼

2063379

無人駕駛計程車:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Robo Taxi - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

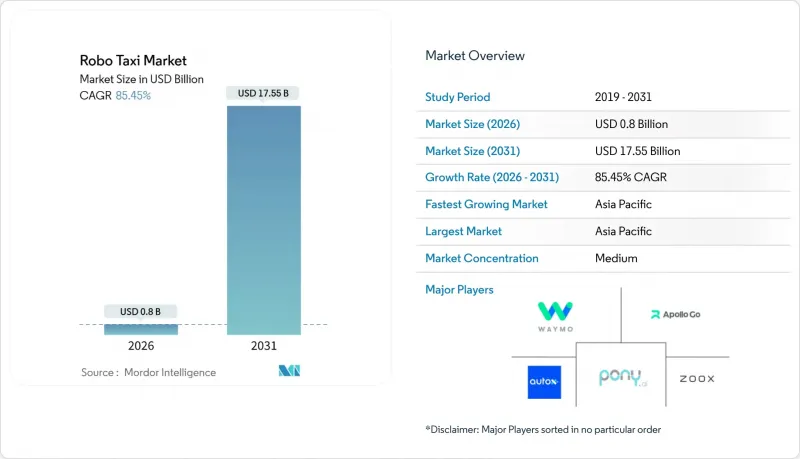

根據 Mordor Intelligence 預測,到 2026 年,無人駕駛計程車市場規模將達到 8 億美元,到 2031 年將達到 175.5 億美元,在預測期內複合年成長率將達到 85.45%。

本報告按自動駕駛等級(L4 和 L5)、動力系統(純電動車、混合動力汽車等)、車輛類型(乘用車和廂型車/接駁車)、應用領域(客運和貨運/小包裹運輸)、服務類型、經營模式、車輛所有權、營運環境和地區進行細分。市場預測以價值(美元)和數量(輛)兩種單位呈現。

全球無人駕駛計程車市場趨勢及洞察

政府主導的自動駕駛車輛示範實驗和監管沙箱

有條件豁免允許使用真實世界數據而非理論模型,從而縮短無人駕駛計程車市場的檢驗週期。 2025年8月,Zoox成為第一家根據美國國家公路交通安全管理局(NHTSA)的自動駕駛車輛豁免計畫(AVEP)獲得示範豁免的公司。這項里程碑式的成就使得Zoox在美國製造的客製化自動駕駛車輛能夠在滿足特定條件的情況下無需傳統的人工操控即可運行。自2024年中期以來,中國交通運輸部已批准在多個主要城市進行全自動駕駛車輛的公共試驗,實現了數百萬英里的載客運輸里程。 2025年11月,阿布達比批准了無人駕駛駕駛人的商業運營,為該地區的快速擴張奠定了基礎。營運商正利用這些早期授權來建立安全記錄,從而更容易進入更保守的市場。

2025 年 8 月 6 日,美國國家公路交通安全管理局 (NHTSA) 根據其自動駕駛車輛豁免計劃 (AVEP) 向 Zoox 授予了首個美國製造的專用自動駕駛車輛的演示豁免,使其能夠在某些情況下無需傳統的手動控制即可運行。

創紀錄的資金流入自動駕駛出行領域。

2024年10月,Waymo完成了由Alphabet主導、外部投資者跟投的56億美元資金籌措。此舉凸顯了投資人對無人駕駛計程車市場商業化前景日益成長的信心。同時,Waabi也籌集了大量資金,用於增強其人工智慧驅動的模擬平台,從而大幅減少了大規模道路測試的需求。在眾多大型IPO和策略性分拆的浪潮中,資源正集中在少數幾家領導企業,進一步鞏固了現有的規模經濟優勢。

前期資本投入高,投資回收期不確定。

在自動駕駛計程車市場,專用車輛和感測器套件的高昂成本顯著延長了大多數城市的損益平衡點。 2024年12月,通用汽車(GM)因累積虧損不斷增加而退出自動駕駛叫車業務。即使是像百度RT6這樣高度最佳化的設計,在車輛投入運作前也需要大量的預付資金。一個主要挑戰依然存在:非尖峰時段的運轉率顯著降低,從而拉低了整體盈利。

細分市場分析

2025年,L4級自動駕駛系統佔總部署車輛數量的62.05%。然而,隨著安全駕駛人的薪資預計將從營運成本中消失,預計到2031年,L5級自動駕駛系統的年複合成長率將達到88.02%,超過L4級。 Waymo在2025年下半年於高速公路上的部署表明,高速併入匝道和變換車道仍在當前感知和規劃能力的範圍內。

擴展營運設計範圍將使機場航線、區域覆蓋和城際走廊成為可能,從而提高每輛車的收益。 Zoox 已獲得美國國家公路交通安全管理局 (NHTSA) 的無方向盤豁免,這意味著如果冗餘的煞車、轉向和感知層達到安全等效性,監管機構將認證其 L5 級自動駕駛能力。由於遠端營運中心可以監控每個營運商的 50 多輛車,人事費用將低於維持車載安全員的成本,從而推動經濟轉型為完全自動駕駛。

預計到2025年,電池式電動車平台將佔據72.13%的市場。這主要得益於零排放區的獎勵以及每英里更低的能源成本。混合動力汽車需要維護兩套動力傳動系統,並且在許多主要城市無法享受堵塞費豁免。預計到2031年,電池式電動車在無人駕駛計程車市場佔有率的複合年成長率將達到87.14%,這主要受電池組價格下降和市政當局更嚴格的排放氣體法規的推動。

百度專門設計的RT6透過取消面向駕駛員的硬體來最佳化能源效率,從而實現了驚人的續航里程。這種方法在降低能源成本的同時,保持了與混合動力轎車相媲美的性能。 Zoox聲稱其專門設計的車輛配備了133kWh的電池,單次充電即可運行超過16小時。這將使其能夠在指定充電間隔下實現全天候服務。然而,燃料電池原型車面臨氫氣基礎設施不足和相關成本高等挑戰。

到2025年,受舒適性標準和現有轎車供應鏈的推動,乘用車將佔所有營運的68.22%。同時,受小包裹遞送合約和校園內固定線路服務的推動,廂型車和接駁車預計將以86.03%的複合年成長率成長。 Nuro的第三代貨運艙營運於郊區雜貨配送路線,與常集中在尖峰時段的乘用車相比,其白天運轉率更高,資產生產力也更高。

EasyMile的EZ10和Navya的Autonom Shuttle已在機場和商務園區累計行駛超過一百萬公里,證明低速自動駕駛是加速法規核准的有效途徑。可重構的內裝支援日夜模式切換,從而最大限度地提高單車收益。

區域分析

預計到2025年,亞太地區將以46.09%的市佔率引領自動駕駛計程車市場,並在2031年之前維持85.79%的複合年成長率。中國交通運輸部已在多個主要城市批准了全自動駕駛服務,使得Apollo Go在2025年1月前累積行駛里程突破900萬次。 Pony.ai在深圳獲得的全市範圍許可涵蓋了大量自動駕駛車輛,展現了該地區監管方面的強勁勢頭。日本和韓國正利用其國內製造能力推進區域試點項目,而印度儘管政策進展較為緩慢,但由於人們對緩解交通堵塞的預期,也正吸引著越來越多的關注。

北美排名第二,這主要得益於Waymo在多個城市的運作。該公司目前已將業務拓展至高速公路路段。儘管各州的保險要求有所不同,但美國國家公路交通安全管理局(NHTSA)已表示有意豁免無方向盤專用車輛的監管,這表明聯邦政府對此表示支持。加拿大在多倫多和溫哥華進行的試點計畫正著重進行寒冷天氣檢驗,以擴大營運設計區域(ODD)。

由於歐洲保守的型式認證流程和分散的責任標準,其在規模上落後於其他國家。儘管如此,德國的L4級自動法規明確了製造商的責任,並且德國正在從多家本土汽車製造商收集測試車輛。 EasyMile和Navya的校園自動駕駛班車已行駛超過100萬公里,這表明低速行駛是自動駕駛的入門階段。中東地區正在崛起為一個快速發展的地區。阿布達比推出了全球首個全自動駕駛商業服務,而杜拜計劃大幅增加其車隊規模,政府將提供激勵措施,與營運商分享利潤。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府主導的自動駕駛車輛示範實驗和監管沙箱

- 創紀錄的資金流入自動駕駛和出行領域。

- AD感測器和運算成本

- 透過整合出行即服務 (MaaS) 平台來提高車輛運轉率

- 專為最後一公里物流設計的自動駕駛貨車架構

- 都市區擁塞收費系統、引導機制和共用自動駕駛

- 市場限制因素

- 前期資本投入高,且投資回收期不確定性。

- 大眾根深蒂固的信任與安全感之間的差距。

- 世界各國在責任和安全認證體系方面存在不一致之處。

- V2X網路安全漏洞

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按自動駕駛級別

- 4級

- 5級

- 透過推進力

- 電池式電動車

- 油電混合車

- 燃料電池汽車

- 車輛類型

- 搭乘用車

- 麵包車/接駁車

- 透過使用

- 客運

- 貨物/小包裹運輸

- 按服務類型

- 租賃類型(自由浮動)

- 站點基座(樞紐站之間)

- 按經營模式

- B2C(直接銷售給騎士)

- B2B(企業和物流合約)

- 與公共交通的合作

- 依所有權類型

- 原廠所有

- 企業所有(跨國公司和新創企業)

- 公有

- 透過操作環境

- 市中心

- 郊區/校園

- 高速公路/城際公路

- 混合用途區

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東和非洲

- 土耳其

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Waymo LLC

- Apollo Go

- AutoX Inc.

- Pony.ai

- Zoox, Inc.

- Tesla, Inc.

- DiDi Autonomous Driving

- Avride Inc.(Yandex Self-Driving Group)

- EasyMile SAS

- Navya Mobility SAS

- Nuro Inc.

- Motional, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the robo taxi market size reached USD 0.80 billion in 2026 and is projected to touch USD 17.55 billion by 2031, advancing at an 85.45% CAGR over the forecast period.

This report is Segmented by Level of Autonomy (Level 4 and Level 5), Propulsion (Battery-Electric, Hybrid-Electric, and More), Vehicle Type (Car and Van/Shuttle), Application (Passenger Transportation and Goods/Parcel Transportation), Service Type, Business Model, Fleet Ownership, Operating Environment, and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Robo Taxi Market Trends and Insights

Government AV Pilots and Regulatory Sandboxes

Conditional exemptions enable the use of real-world data to substitute for theoretical models, thereby reducing validation timelines in the Robo Taxi Market. In August 2025, Zoox became the first recipient of a demonstration exemption from the National Highway Traffic Safety Administration under the Automated Vehicle Exemption Program (AVEP). This milestone enables Zoox's American-built, purpose-designed automated vehicle to operate without conventional manual controls, provided that certain specified conditions are met China's Ministry of Transport has permitted fully driverless public trials across multiple tier-1 cities since mid-2024, enabling millions of passenger-carrying miles. Abu Dhabi authorized commercial operations without safety drivers in November 2025, setting the stage for regional leapfrog adoption. Operators use early approvals to accrue safety records that ease expansion into more conservative markets.

On August 6, 2025, NHTSA granted Zoox the first-ever demonstration exemption under the Automated Vehicle Exemption Program (AVEP) for an American-built purpose-built automated vehicle, enabling operation without traditional manual controls under specified conditions."

Record Capital Inflows into Autonomous-Mobility Ventures

In October 2024, Waymo secured a USD 5.6 billion funding round, spearheaded by Alphabet and bolstered by external investors. This move highlighted the escalating investor confidence in the imminent commercialization of the Robo Taxi Market. Meanwhile, Waabi raised substantial capital to enhance its AI-driven simulation platform, significantly reducing the need for extensive on-road testing. As major IPOs and strategic spin-outs emerge, they're centralizing resources among a select few leaders, intensifying the prevailing scale advantages.

High Upfront CAPEX and Uncertain Payback

In most cities, breakeven periods for purpose-built vehicles and sensor suites are significantly long due to their high costs in the Robo Taxi Market. In December 2024, General Motors discontinued its autonomous ride-hailing venture after incurring substantial cumulative losses. Even with highly optimized designs, like Baidu's RT6, considerable upfront investment is required before these vehicles can enter service. A persistent challenge remains: off-peak hours experience significant underutilization, which dampens overall returns.

Other drivers and restraints analyzed in the detailed report include:

- Declining AD-Sensor and Computing Costs

- Maas Platform Integration Unlocking Fleet Utilization

- Persistent Public-Trust and Safety-Perception Gap

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Level 4 systems accounted for 62.05% of 2025 deployments; however, Level 5 is projected to outpace this with an 88.02% CAGR to 2031, as safety-driver wages are expected to disappear from operating ledgers. Waymo's expansion to freeway routes in late 2025 showed that on-ramp merging and high-speed lane changes are within current perception-and-planning capabilities.

Wider operational design domains will unlock airport runs, rural coverage, and inter-city corridors, raising revenue miles per vehicle. Zoox has obtained a steering-wheel-free exemption from the NHTSA, indicating that regulators will certify Level 5 once redundant braking, steering, and perception layers achieve safety equivalency. As remote operations centers supervise 50-plus vehicles per human, labor overhead falls below the cost of retaining in-car safety operators, tipping economics toward full autonomy.

Battery-electric platforms held a 72.13% share in 2025, reflecting the influence of zero-emission zone incentives and low per-mile energy costs. Hybrid alternatives carry dual-powertrain maintenance and fail to qualify for congestion-pricing exemptions in multiple capitals. The robo taxi market share for battery-electric vehicles is forecast to expand with a 87.14% CAGR through 2031 as pack prices decrease and city councils tighten emissions regulations.

Baidu's RT6, designed for a purpose, achieves an impressive range by optimizing energy efficiency through the removal of driver-centric hardware. This approach aligns its performance with hybrid sedans while reducing energy costs. Zoox claims that its purpose-built vehicle, equipped with a 133 kWh battery, can go over 16 hours on a single charge. This enables full-day service with designated charging intervals. However, fuel-cell prototypes face challenges due to the limited availability of hydrogen infrastructure and higher associated costs.

Passenger cars accounted for 68.22% of rides in 2025, driven by comfort benchmarks and existing sedan supply chains. Vans and shuttles, however, are forecast to grow at 86.03% CAGR, propelled by parcel contracts and fixed-route campus services. Nuro's third-generation cargo pod runs suburban grocery loops with notable daytime utilization, demonstrating higher asset productivity than peak-biased passenger use cases.

EasyMile's EZ10 and Navya's Autonom Shuttle log over 1 million commercial kilometers across airports and business parks, validating low-speed autonomy as a fast-track regulatory entry point. Reconfigurable interiors permit day-night mode switching, maximizing revenue per chassis.

Geography Analysis

The Asia-Pacific region led the robo taxi market with a 46.09% share in 2025 and is projected to grow at an 85.79% CAGR through 2031. China's Ministry of Transport has authorized fully driverless services in multiple tier-1 cities, accelerating cumulative ride counts beyond nine million for Apollo Go by January 2025 . Pony.ai's city-wide permit in Shenzhen covers a significant number of autonomous cars, demonstrating the region's regulatory momentum. Japan and South Korea leverage domestic manufacturing strength to push local pilots, while India attracts interest for congestion relief despite slower policy progress.

North America ranks second, led by Waymo's multi-city operations, which now include freeway segments. NHTSA's willingness to exempt purpose-built vehicles without steering wheels signals federal support, even as state-level insurance requirements remain uneven. Canadian pilots in Toronto and Vancouver concentrate on cold-weather validation to expand operational design domains.

Europe trails in volume due to conservative type-approval processes and fragmented liability norms. Nevertheless, Germany's Level 4 statute clarifies manufacturer responsibility, drawing pilot fleets from domestic OEMs. Autonomous campus shuttles from EasyMile and Navya have logged over 1 million kilometers, highlighting lower-speed niches as entry points. The Middle East emerges as a leapfrog region: Abu Dhabi hosts the first fully driverless commercial service, and Dubai plans to significantly expand its fleets, backed by government concessions that share revenue with operators.

- Waymo LLC

- Apollo Go

- AutoX Inc.

- Pony.ai

- Zoox, Inc.

- Tesla, Inc.

- DiDi Autonomous Driving

- Avride Inc. (Yandex Self-Driving Group)

- EasyMile SAS

- Navya Mobility SAS

- Nuro Inc.

- Motional, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government AV Pilots and Regulatory Sandboxes

- 4.2.2 Record Capital Inflows into Autonomous-Mobility Ventures

- 4.2.3 Declining AD-Sensor and Computing Costs

- 4.2.4 MaaS Platform Integration Unlocking Fleet Utilization

- 4.2.5 Purpose-Built Autonomous Van Architectures for Last-Mile Logistics

- 4.2.6 Urban Congestion Pricing Nudging Shared Autonomy

- 4.3 Market Restraints

- 4.3.1 High Upfront CAPEX and Uncertain Pay-Back

- 4.3.2 Persistent Public Trust and Safety-Perception Gap

- 4.3.3 Patchy Global Liability and Safety Certification Regimes

- 4.3.4 V2X Cybersecurity Vulnerabilities

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Level of Autonomy

- 5.1.1 Level 4

- 5.1.2 Level 5

- 5.2 By Propulsion

- 5.2.1 Battery-Electric Vehicles

- 5.2.2 Hybrid-Electric Vehicles

- 5.2.3 Fuel-Cell Electric Vehicles

- 5.3 By Vehicle Type

- 5.3.1 Car

- 5.3.2 Van / Shuttle

- 5.4 By Application

- 5.4.1 Passenger Transportation

- 5.4.2 Goods / Parcel Transportation

- 5.5 By Service Type

- 5.5.1 Rental-Based (free-floating)

- 5.5.2 Station-Based (hub-to-hub)

- 5.6 By Business Model

- 5.6.1 B2C (direct to riders)

- 5.6.2 B2B (corporate / logistics contracts)

- 5.6.3 Public-Transit Integration

- 5.7 By Fleet Ownership

- 5.7.1 OEM-Owned

- 5.7.2 Operator-Owned (TNCs and start-ups)

- 5.7.3 Public-Agency-Owned

- 5.8 By Operating Environment

- 5.8.1 Urban Core

- 5.8.2 Sub-Urban / Campus

- 5.8.3 Highway / Inter-city

- 5.8.4 Mixed-Use Zones

- 5.9 By Geography

- 5.9.1 North America

- 5.9.1.1 United States

- 5.9.1.2 Canada

- 5.9.1.3 Rest of North America

- 5.9.2 South America

- 5.9.2.1 Brazil

- 5.9.2.2 Argentina

- 5.9.2.3 Rest of South America

- 5.9.3 Europe

- 5.9.3.1 Germany

- 5.9.3.2 United Kingdom

- 5.9.3.3 France

- 5.9.3.4 Italy

- 5.9.3.5 Spain

- 5.9.3.6 Russia

- 5.9.3.7 Rest of Europe

- 5.9.4 Asia-Pacific

- 5.9.4.1 China

- 5.9.4.2 Japan

- 5.9.4.3 India

- 5.9.4.4 South Korea

- 5.9.4.5 Rest of Asia-Pacific

- 5.9.5 Middle East and Africa

- 5.9.5.1 Turkey

- 5.9.5.2 Saudi Arabia

- 5.9.5.3 United Arab Emirates

- 5.9.5.4 South Africa

- 5.9.5.5 Nigeria

- 5.9.5.6 Rest of the Middle East and Africa

- 5.9.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Waymo LLC

- 6.4.2 Apollo Go

- 6.4.3 AutoX Inc.

- 6.4.4 Pony.ai

- 6.4.5 Zoox, Inc.

- 6.4.6 Tesla, Inc.

- 6.4.7 DiDi Autonomous Driving

- 6.4.8 Avride Inc. (Yandex Self-Driving Group)

- 6.4.9 EasyMile SAS

- 6.4.10 Navya Mobility SAS

- 6.4.11 Nuro Inc.

- 6.4.12 Motional, Inc.

7 Market Opportunities & Future Outlook

- 7.1 Autonomous Ride-Hailing Integration into City MaaS Platforms

- 7.2 Dedicated Robo-Van Networks for Last-Mile Parcel Delivery

- 7.3 Subscription-Based Robo-Taxi Services for Senior Mobility

- 7.4 Cross-Border Robo-Taxi Corridors (e.g., EU Schengen Pilot)

- 7.5 Carbon-Credit Monetization for Zero-Emission Robo-Taxi Fleets

自動駕駛計程車市場:2026-2032年全球市場預測(依車輛類型、自動駕駛等級、技術堆疊和應用分類)

自動駕駛計程車市場:2026-2032年全球市場預測(依車輛類型、自動駕駛等級、技術堆疊和應用分類) 自動駕駛計程車市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、部署模式、最終用戶、功能

自動駕駛計程車市場分析及預測(至2035年):類型、產品、服務、技術、組件、應用、部署模式、最終用戶、功能 全球20個城市的無人駕駛計程車市場:基準分析(2026-2035年)機器人計程車市場規模、佔有率、成長、全球產業分析、區域趨勢以及 2026 年至 2034 年的預測。

全球20個城市的無人駕駛計程車市場:基準分析(2026-2035年)機器人計程車市場規模、佔有率、成長、全球產業分析、區域趨勢以及 2026 年至 2034 年的預測。 自動駕駛計程車市場報告:按應用、自主程度、車輛類型、服務、推進方式和地區分類(2026-2034 年)

自動駕駛計程車市場報告:按應用、自主程度、車輛類型、服務、推進方式和地區分類(2026-2034 年) 2034年自動駕駛計程車市場預測:按組件、車輛類型、服務類型、推進方式、應用和區域分類的全球分析

2034年自動駕駛計程車市場預測:按組件、車輛類型、服務類型、推進方式、應用和區域分類的全球分析 2026年全球機器人計程車市場報告

2026年全球機器人計程車市場報告 無人駕駛計程車市場:按應用、車輛類型、組件類型和地區分類自動駕駛計程車服務市場:按服務模式、車輛推進系統、所有權模式、自動駕駛水平、最終用戶和應用分類——2026-2032年全球預測

無人駕駛計程車市場:按應用、車輛類型、組件類型和地區分類自動駕駛計程車服務市場:按服務模式、車輛推進系統、所有權模式、自動駕駛水平、最終用戶和應用分類——2026-2032年全球預測 自動駕駛計程車市場規模、佔有率和趨勢分析報告:按推進方式、組件類型、自動駕駛等級、車輛類型、服務類型、應用、地區和細分市場預測(2026-2033 年)

自動駕駛計程車市場規模、佔有率和趨勢分析報告:按推進方式、組件類型、自動駕駛等級、車輛類型、服務類型、應用、地區和細分市場預測(2026-2033 年)