|

市場調查報告書

商品編碼

2063373

汽車虛擬機器管理程序:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Automotive Hypervisor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

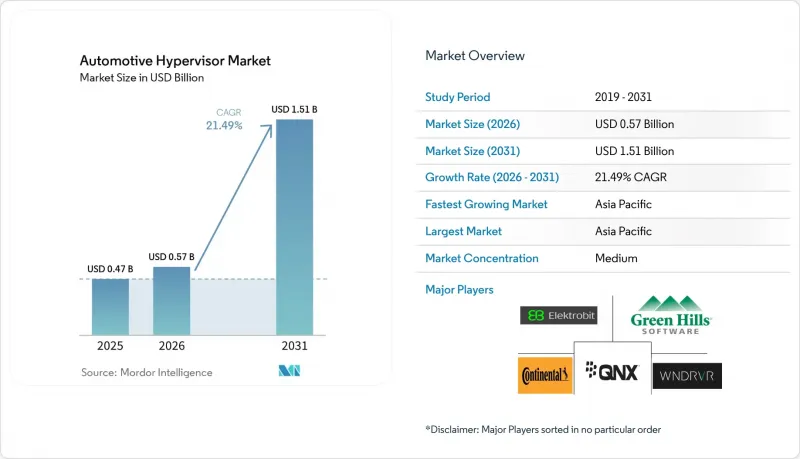

根據 Mordor Intelligence 預測,汽車虛擬機器管理程式市場將從 2025 年的 4.7 億美元成長到 2026 年的 5.7 億美元,到 2031 年達到 15.1 億美元,2026 年至 2031 年的複合年成長率為 21.49%。

本報告按類型(1 型:裸機管理程序;2 型:主機型管理程序)、車輛類型(乘用車、輕型商用車、其他)、運行模式(自動駕駛車輛、其他)、應用(高級駕駛輔助系統 (ADAS)、其他)、需求類型(OEM、替換)和地區(北美、其他)進行分類。市場預測以美元計價。

全球汽車虛擬機器管理程式市場趨勢及洞察

網域控制器型電子/電氣架構的普及

汽車產業從分散式ECU架構向集中式網域控制器的轉變,從根本上重塑了車輛電氣和電子(E/E)系統,其中虛擬機管理程式在將100多個獨立的ECU整合到不到10個高效能運算單元中發揮著至關重要的作用。這種架構轉型可使車輛重量減輕約15-20公斤,線束複雜度降低高達40%,直接影響電動車的續航里程和製造成本。這種整合也為汽車虛擬機器管理程式市場帶來了巨大的機遇,因為每個網域控制器都需要先進的虛擬化軟體來管理不同嚴重程度的工作負載,涵蓋ASIL-D安全功能和非安全應用。為了滿足不斷變化的軟體需求並建立面向未來的汽車平臺,原始設備製造商(OEM)正擴大採用基於虛擬機器管理程式的架構,其中特斯拉、寶馬和大眾汽車在向軟體定義汽車轉型方面主導。

強制性網路安全合規性(ISO/SAE 21434、UNECE R155/R156)

汽車網路安全監管要求正在推動汽車虛擬機器管理程式市場實現合規主導成長。聯合國歐洲經濟委員會R155號法規規定,自2024年7月起,歐盟成員國、日本和韓國的車輛類型認證必須以網路安全管理系統(CSMS)認證為前提。由於該法規強調組織層面的網路安全流程以及定期的威脅分析和風險評估(TARA)活動,原始設備製造商(OEM)被迫採用基於虛擬機器管理程序的架構,以實現安全關鍵域和連接域之間的硬體隔離。 ISO/SAE 21434合規性要求在混合嚴重性系統中特別嚴格,要求虛擬機器管理程序證明在共用硬體資源上運行的不同ASIL等級的應用程式之間不會相互干擾。

一級供應商對傳統ECU的投資日益鞏固

汽車產業對傳統ECU架構的大量投資仍是汽車虛擬機器管理程式市場成長的一大挑戰。這是因為一級供應商可能累計數十億美元的資產減損損失,這些損失涉及現有的工具鏈、製造設施以及針對分散式控制系統最佳化的工程技術。許多傳統供應商已經開發了自己的AUTOSAR Classic實現方案和安全認證的軟體棧,這些方案和軟體堆疊需要進行大規模的重新設計才能在虛擬機器管理程式環境下運行,從而構成了快速遷移的經濟障礙。漫長的汽車開發週期進一步加劇了這個挑戰。 2022-2023年完成設計的ECU將繼續安裝在量產車上,直至2028-2030年,這將限制預測期內虛擬機管理程序解決方案的潛在市場規模。

細分市場分析

到2025年,第一類裸機虛擬機管理程式將佔據62.04%的市場。這反映了其卓越的性能和直接硬體存取能力,而這些對於安全至關重要的汽車應用至關重要。這些虛擬機器管理程式無需底層作業系統即可直接在車輛硬體上運行,從而提供確定性的即時性能和極低的延遲開銷,這對於高級駕駛輔助系統(ADAS)和動力傳動系統控制系統至關重要。雖然第二類託管虛擬機器管理程式的市佔率較小,但預計到2031年,其複合年成長率將達到16.82%,這主要得益於其開發環境的柔軟性以及與現有基於Linux的資訊娛樂平台的易於整合。

裸機架構的效能優勢在混合優先權場景中特別顯著,在這些場景中,ASIL-D 等級安全功能必須與非安全應用程式在共用硬體資源上共存。諸如 Green Hills 的 INTEGRITY Multivisor 和 Wind River 的 Helix Virtualization Platform 等 1 型虛擬機器管理程序,提供了硬體輔助虛擬化功能,能夠實現功能安全合規性所需的嚴格時間和空間分類。然而,對於軟體開發、測試和非安全資訊娛樂應用程式等特定用例,2 型解決方案正日益普及,因為其簡化的部署模式彌補了效能方面的不足。市場趨勢表明,未來市場格局將呈現兩極化:1 型虛擬機管理程序將主導量產車輛的部署,而 2 型解決方案將佔據開發工具和售後市場領域。

預計到2025年,乘用車將佔汽車虛擬化部署的58.28%。這主要歸功於該細分市場的大規模生產,以及受益於域整合的先進資訊娛樂和ADAS功能的日益普及。乘用車市場的主導地位反映了OEM廠商致力於透過軟體定義功能和空中升級來打造差異化乘用車,而這需要強大的虛擬化平台。輕型商用車(LCV)和重型商用車(HCV)合計佔據剩餘的市場佔有率,其中商用車領域對利用虛擬化技術的車隊管理和遠端資訊處理應用的需求日益成長。

輕型商用車 (LCV) 細分市場是汽車虛擬化管理程式市場中成長最快的領域,這主要得益於車隊營運的快速數位化以及連網軟體主導架構的普及。物流和最後一公里配送車隊對即時遠端資訊處理、駕駛輔助和空中升級的需求不斷成長,正在加速 LCV 平台與虛擬化管理程序的整合。汽車製造商正在將資訊娛樂系統、高級駕駛輔助系統 (ADAS)和動力傳動系統等多個控制域整合到虛擬化 ECU 中,以降低硬體成本並提高系統效率。此外,遵守網路安全法規以及向電動化 LCV 轉型也需要安全且可擴展的虛擬化框架。因此,在預測期內,LCV 細分市場對汽車虛擬化管理程序而言具有最大的部署潛力。

區域分析

預計到2025年,亞太地區將以37.81%的市佔率佔據全球領先地位,年複合成長率將達到14.79%,主要得益於中國OEM廠商加速晶片在地化和軟體定義架構的採用。到2025年,中國生產的車型中約有三分之一將配備網域控制器,每個網域控制器至少整合一個虛擬機器管理程式實例。目前,國內晶片製造商已開始出貨早期RISC-V汽車SoC,加速開發針對中國安全演算法客製化的在地化虛擬化協定堆疊。

北美也正效仿這一做法,這主要得益於38個州開展的大規模自動駕駛測試,以及美國國家公路交通安全管理局(NHTSA)新訂定的數據共用要求,該要求強制執行安全日誌記錄(這是虛擬機管理程序特有的用例)。美國供應鏈風險規避措施限制使用中國產車載資訊系統組件,促使原始設備製造商(OEM)轉向國內及盟友的軟體供應商。

歐洲仍然是嚴格功能安全標準的市場。 UNECE R156 更新流程要求每三年進行一次重新認證,這為提供合規性監控的虛擬機器管理程式供應商帶來了持續的收入。德國的 Level 4 Regulation 2024 和法國的 Black Box Regulation 2025 為能夠確保資料隔離防崩潰的解決方案創造了獨特的機會。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 網域控制器型電子/電氣架構的普及

- 強制性網路安全合規性(ISO/SAE 21434、UNECE R155/R156)

- 將資訊娛樂系統、ADAS系統和動力傳動系統整合到單一SoC中。

- 「車輛即服務」訂閱模式的興起

- 採用區域架構以支援混合優先權工作負載

- 原始設備製造商 (OEM) 正在推動軟體定義汽車 (SDV) 的普及。

- 市場限制因素

- 一級供應商對傳統ECU的投資日益鞏固

- 符合 ASIL-D 標準的虛擬機器管理程序認證費用

- 即時效能開銷和延遲抖動

- 缺乏汽車級虛擬化技能

- 價值/供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 類型 1(裸機虛擬機器管理程式)

- 類型 2(基於主機的虛擬機器管理程式)

- 按車輛類型

- 搭乘用車

- 輕型商用車(LCV)

- 中型和重型商用車輛(HCV)

- 透過操作模式

- 自動駕駛汽車

- 半自動駕駛汽車

- 透過使用

- ADAS(進階駕駛輔助系統)

- 資訊娛樂系統

- 互聯互通和遠端資訊處理

- 動力傳動系統和引擎控制系統

- 其他

- 依需求類型

- OEM

- 用於替換

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 西班牙

- 義大利

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BlackBerry QNX

- Green Hills Software

- Wind River

- Continental AG

- Elektrobit

- Vector Informatik

- Renesas Electronics

- Siemens Digital Industries(Embedded Mentor)

- NXP Semiconductors

- LYNX Software Technologies

- Real-Time Systems(RTX)

- Bosch ETAS

- Aptiv

- Harman(Samsung)

- Denso

- Qualcomm

- KPIT Technologies

- TTTech Auto

- SYSGO

第7章 市場機會與未來展望

According to Mordor Intelligence, the automotive hypervisor market size is expected to increase from USD 0.47 billion in 2025 to USD 0.57 billion in 2026 and reach USD 1.51 billion by 2031, growing at a CAGR of 21.49% over 2026-2031.

This report is Segmented by Type (Type 1 Bare-Metal Hypervisor, Type 2 Hosted Hypervisor), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Mode of Operation (Autonomous Vehicles, and More), Application (Advanced Driver Assistance Systems, and More), Demand Type (OEM, Replacement), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive Hypervisor Market Trends and Insights

Proliferation of Domain-Controller E/E Architectures

The automotive industry's transition from distributed ECU architectures to centralized domain controllers fundamentally reshapes vehicle electrical/electronic (E/E) systems, with hypervisors as the critical enabler for consolidating 100+ individual ECUs onto fewer than 10 high-performance computing units. This architectural shift reduces vehicle weight by approximately 15-20 kilograms while cutting wiring harness complexity by up to 40%, directly impacting electric vehicle range and manufacturing costs. The consolidation is also creating significant opportunities in the automotive hypervisor market, as each domain controller requires advanced virtualization software to manage mixed-criticality workloads across ASIL-D safety functions and non-safety applications. OEMs are increasingly adopting hypervisor-based architectures to future-proof vehicle platforms against evolving software demands, with Tesla, BMW, and Volkswagen leading the move toward software-defined vehicles.

Mandatory Cybersecurity Compliance (ISO/SAE 21434, UNECE R155/R156)

Regulatory mandates for automotive cybersecurity are driving compliance-led growth in the automotive hypervisor market. UNECE R155 requires Cybersecurity Management Systems (CSMS) certification as a precondition for vehicle type approval in EU member countries, Japan, and South Korea since July 2024. The regulation's emphasis on organizational-level cybersecurity processes and regular threat analysis and risk assessment (TARA) activities drives OEMs to adopt hypervisor-based architectures that provide hardware-backed isolation between safety-critical and connectivity domains. ISO/SAE 21434 compliance requirements are particularly stringent for mixed-criticality systems, where hypervisors must demonstrate freedom from interference between different ASIL-rated applications running on shared hardware resources.

Legacy ECU Investment Lock-ins at Tier-1s

The automotive industry's heavy investment in legacy ECU architectures remains a major challenge for growth in the automotive hypervisor market, as Tier-1 suppliers face potential write-offs of billions of dollars in existing toolchains, manufacturing equipment, and engineering expertise optimized for distributed control systems. Many established suppliers have developed proprietary AUTOSAR Classic implementations and safety-certified software stacks requiring extensive re-engineering to operate within hypervisor environments, creating financial disincentives for rapid migration. The challenge is compounded by long automotive development cycles. ECU designs frozen in 2022-2023 will continue shipping in production vehicles through 2028-2030, limiting the addressable market for hypervisor solutions during the forecast period.

Other drivers and restraints analyzed in the detailed report include:

- Consolidation of Infotainment, ADAS and Powertrain on Single SoCs

- OEM Push Toward Software-Defined Vehicles (SDVs)

- Hypervisor Certification Costs for ASIL-D Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Type 1 bare-metal hypervisors hold 62.04% market share in 2025, reflecting their superior performance and direct hardware access capabilities, which are essential for safety-critical automotive applications. These hypervisors operate directly on vehicle hardware without an underlying operating system, providing deterministic real-time performance and minimal latency overhead crucial for ADAS and powertrain control systems. Type 2 hosted hypervisors, despite a smaller market share, are experiencing rapid growth at a 16.82% CAGR through 2031, driven by their flexibility in development environments and ease of integration with existing Linux-based infotainment platforms.

The performance advantages of bare-metal architectures become particularly pronounced in mixed-criticality scenarios, where ASIL-D safety functions must coexist with non-safety applications on shared hardware resources. Type 1 hypervisors, such as Green Hills' INTEGRITY Multivisor and Wind River's Helix Virtualization Platform, provide hardware-assisted virtualization features that enable strict temporal and spatial partitioning required for functional safety compliance. However, Type 2 solutions are gaining traction in specific use cases such as software development, testing, and non-safety infotainment applications where their simplified deployment model outweighs performance considerations. The market evolution suggests a bifurcated future, with Type 1 hypervisors dominating production vehicle deployments while Type 2 solutions capture development tool and aftermarket segments.

Passenger cars account for 58.28% of automotive hypervisor deployments in 2025, driven by the segment's high-volume production and the increasing integration of advanced infotainment and ADAS features that benefit from domain consolidation. The passenger car segment's dominance reflects OEMs' focus on differentiating consumer vehicles through software-defined features and over-the-air updates, which require robust virtualization platforms. Light Commercial Vehicles (LCVs) and Medium/Heavy Commercial Vehicles (HCVs) collectively account for the remaining market share, with commercial segments showing growing interest in hypervisor-enabled fleet management and telematics applications.

The LCV (Light Commercial Vehicle) segment is the fastest-growing category in the automotive hypervisor market, owing to the rapid digitalization of fleet operations and the adoption of connected, software-driven architectures. Rising demand for real-time telematics, driver assistance, and over-the-air updates in logistics and last-mile delivery fleets is accelerating the integration of hypervisors across LCV platforms. Automakers are consolidating multiple control domains-infotainment, ADAS, and powertrain-into virtualized ECUs to reduce hardware costs and enhance system efficiency. Furthermore, compliance with cybersecurity regulations and the shift toward electrified LCVs require secure and scalable virtualization frameworks. As a result, the LCV segment offers the highest deployment potential for automotive hypervisors during the forecast period.

Geography Analysis

Asia-Pacific led with 37.81% share in 2025 and is advancing at a 14.79% CAGR as Chinese OEMs race to localize silicon and adopt software-defined architectures. Roughly one-third of vehicles built in China for the 2025 model year will feature domain controllers, each of which embeds at least one hypervisor instance. Domestic chipmakers are now shipping early RISC-V automotive SoCs, prompting the development of localized virtualization stacks tuned for Chinese security algorithms.

North America follows, buoyed by widespread autonomous testing across 38 states and emerging NHTSA data-sharing mandates that require secure logging-an inherent hypervisor use case. U.S. supply-chain de-risking policies curtailing the use of Chinese telematics components are pushing OEMs toward domestic and allied software vendors.

Europe remains the reference market for rigorous functional safety. UNECE R156 update processes call for three-year re-certification cycles, generating recurring revenue for hypervisor suppliers offering compliance monitoring. Germany's 2024 Level 4 ordinance and France's 2025 black-box rules create unique opportunities for solutions that guarantee crash-proof data isolation.

- BlackBerry QNX

- Green Hills Software

- Wind River

- Continental AG

- Elektrobit

- Vector Informatik

- Renesas Electronics

- Siemens Digital Industries (Embedded Mentor)

- NXP Semiconductors

- LYNX Software Technologies

- Real-Time Systems (RTX)

- Bosch ETAS

- Aptiv

- Harman (Samsung)

- Denso

- Qualcomm

- KPIT Technologies

- TTTech Auto

- SYSGO

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Domain-Controller E/E Architectures

- 4.2.2 Mandatory Cybersecurity Compliance (ISO/SAE 21434, UNECE R155/R156)

- 4.2.3 Consolidation of Infotainment, ADAS, and Powertrain on Single SoCs

- 4.2.4 Rise of "Vehicle-as-a-Service" Subscription Models

- 4.2.5 Adoption of Zonal Architecture Enabling Mixed-Criticality Workloads

- 4.2.6 OEM Push Toward Software-Defined Vehicles (SDVs)

- 4.3 Market Restraints

- 4.3.1 Legacy ECU Investment Lock-Ins at Tier-1s

- 4.3.2 Hypervisor Certification Costs for ASIL-D Compliance

- 4.3.3 Real-Time Performance Overhead and Latency Jitter

- 4.3.4 Scarcity of Automotive-Grade Virtualization Skillsets

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Threat of Substitutes

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Bargaining Power of Suppliers

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Type

- 5.1.1 Type 1 (Bare-Metal Hypervisor)

- 5.1.2 Type 2 (Hosted Hypervisor)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles (LCVs)

- 5.2.3 Medium and Heavy Commercial Vehicles (HCVs)

- 5.3 By Mode of Operation

- 5.3.1 Autonomous Vehicles

- 5.3.2 Semi-Autonomous Vehicles

- 5.4 By Application

- 5.4.1 Advanced Driver Assistance Systems (ADAS)

- 5.4.2 Infotainment Systems

- 5.4.3 Connectivity and Telematics

- 5.4.4 Powertrain and Engine Control Systems

- 5.4.5 Others

- 5.5 By Demand Type

- 5.5.1 OEM

- 5.5.2 Replacement

- 5.6 By Region

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 Spain

- 5.6.3.4 Italy

- 5.6.3.5 France

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 India

- 5.6.4.2 China

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 BlackBerry QNX

- 6.4.2 Green Hills Software

- 6.4.3 Wind River

- 6.4.4 Continental AG

- 6.4.5 Elektrobit

- 6.4.6 Vector Informatik

- 6.4.7 Renesas Electronics

- 6.4.8 Siemens Digital Industries (Embedded Mentor)

- 6.4.9 NXP Semiconductors

- 6.4.10 LYNX Software Technologies

- 6.4.11 Real-Time Systems (RTX)

- 6.4.12 Bosch ETAS

- 6.4.13 Aptiv

- 6.4.14 Harman (Samsung)

- 6.4.15 Denso

- 6.4.16 Qualcomm

- 6.4.17 KPIT Technologies

- 6.4.18 TTTech Auto

- 6.4.19 SYSGO

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

汽車虛擬機器管理程序和混合重要性作業系統全球市場規模、佔有率、趨勢和成長分析報告(2026-2034)

汽車虛擬機器管理程序和混合重要性作業系統全球市場規模、佔有率、趨勢和成長分析報告(2026-2034) 汽車虛擬機器管理程式市場:按組件、應用、車輛類型、部署模式和最終用戶分類-2026-2032年全球市場預測

汽車虛擬機器管理程式市場:按組件、應用、車輛類型、部署模式和最終用戶分類-2026-2032年全球市場預測 汽車虛擬機管理程式市場分析與預測(至2035年):類型、產品、服務、技術、組件、應用、部署、最終用戶、功能、解決方案

汽車虛擬機管理程式市場分析與預測(至2035年):類型、產品、服務、技術、組件、應用、部署、最終用戶、功能、解決方案 汽車虛擬機器管理程序及混合重要性作業系統市場機會、成長要素、產業趨勢分析及2026-2035年預測

汽車虛擬機器管理程序及混合重要性作業系統市場機會、成長要素、產業趨勢分析及2026-2035年預測 2026年全球汽車虛擬機器管理程式市場報告嵌入式虛擬機器管理程式市場分析與預測(至2035年):類型、產品類型、服務、技術、元件、應用、部署模式、最終用戶、功能

2026年全球汽車虛擬機器管理程式市場報告嵌入式虛擬機器管理程式市場分析與預測(至2035年):類型、產品類型、服務、技術、元件、應用、部署模式、最終用戶、功能 2026-2030年全球虛擬機器管理程式市場汽車虛擬管理程式市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測汽車虛擬機器管理程序市場機會、成長要素、產業趨勢分析及預測(2026-2035年)

2026-2030年全球虛擬機器管理程式市場汽車虛擬管理程式市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測汽車虛擬機器管理程序市場機會、成長要素、產業趨勢分析及預測(2026-2035年) 嵌入式虛擬機器管理程式市場,按組件、按類型、按技術、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測

嵌入式虛擬機器管理程式市場,按組件、按類型、按技術、按最終用戶、按國家和地區 - 2025 年至 2032 年全球行業分析、市場規模、市場佔有率和預測