|

市場調查報告書

商品編碼

2063346

北美精密農業:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)North America Precision Agriculture - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

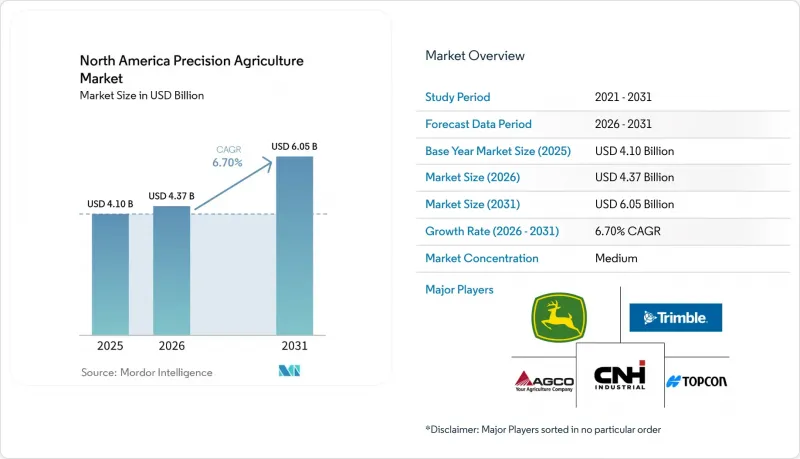

根據 Mordor Intelligence 預測,北美精密農業市場規模將從 2025 年的 41 億美元和 2026 年的 43.7 億美元成長到 2031 年的 60.5 億美元,2026 年至 2031 年的複合年成長率為 6.7%。

本報告按組件(硬體、軟體等)、技術(導航(GPS/GNSS等)、應用(產量監測等)、農場規模(大型農場(1000英畝或以上)等)和地區(美國、加拿大、墨西哥、北美及其他地區)進行細分。市場預測以美元(USD)為單位。

北美精密農業市場趨勢與洞察

透過最佳化可變費率投入降低成本

可變施肥技術使種植者能夠在特定的微區內調整種子、肥料和農藥的施用量,從而減少10-15%的浪費,並即時帶來現金流收益。約翰迪爾的ExactApply噴嘴系統在2025年於內布拉斯加州和堪薩斯州進行的試驗中,除草劑用量減少了高達77%。這項技術在土壤變異性高且已在使用GPS導航曳引機的地區,尤其是在愛荷華州、伊利諾州和薩斯喀徹爾溫省,推廣速度最為迅速。經銷商報告稱,可安裝在現有播種機上的附加控制器銷售強勁,其成本僅為更換整機價格的三分之一。

補貼以促進智慧設備的使用

在北美,成本分攤獎勵在促進精密農業技術的應用方面繼續發揮至關重要的作用。在美國,農業部將包括環境品質獎勵計畫(EQIP)在內的保護性資助計畫從2021年延長至2023年。此次延期加強了精密農業工具和氣候友善耕作方式的財政支持。同樣,在加拿大,加拿大農業及農業食品部於2021年啟動了乾淨科技計劃,為精密農業設備、感測器和節能技術提供成本分攤支持,資金支持將持續到2026年。

先進技術的實施成本很高

包含RTK接收器、無人機平台和可變應用控制器的標準套裝成本仍然很高。對於收入淨額有限的小規模糧食種植者來說,這筆費用構成了一項重大挑戰,他們難以償還此類投資。高昂的初始投資仍是北美地區精密農業技術普及的主要障礙。 GPS導航系統、感測器和數據平台等先進設備的巨額前期成本尤其令資金籌措有限的中小型農場望而卻步。除了硬體成本外,長期經濟效益的不確定性以及這些技術的操作複雜性也使得農民難以評估投資報酬率(ROI)。

細分市場分析

2025年,硬體在北美精密農業市場佔據最大佔有率,達到68.0%,這主要得益於GPS接收器和無人機平台的成熟基礎。然而,預計2026年至2031年間,軟體市場將以9.8%的複合年成長率(CAGR)實現最高成長。氣候公司(The Climate Corporation)新增了FieldView用戶,其中相當一部分用戶選擇支付額外費用,用於可變施肥腳本編寫和排碳權記錄。 2023年,天寶公司(Trimble)宣布透過與AGCO成立合資企業,推出精密農業策略,重點在於整合不同品牌設備及數據系統,實現不同製造商設備的混合使用。到2024年,該策略已擴展為更廣泛的多品牌連接和數據整合平台,實現了迪爾公司(Deere & Company)、凱斯紐荷蘭工業公司(CNH Industrial NV)和AGCO公司之間的遙測互通性。

為了應對日益複雜的營運環境,基於服務的產品和服務正在不斷擴展,供應商也更加注重整合化的數位平台和遠端支持,以最大限度地減少對現場干預的依賴。設備製造商正在將遠端資訊處理、互聯互通和農業諮詢服務整合到其產品中,將收入模式與績效結果掛鉤,並促進與客戶參與。此外,高光譜影像和土壤分析工具等先進感測技術正被整合到更廣泛的數位生態系統中。專有分析技術在將原始數據轉化為可執行的洞察方面發揮著至關重要的作用,從而實現高效的農場管理。

截至2025年,導航(GPS/GNSS)將佔北美精密農業市場佔有率的37.5%,這反映了過去20年間改造升級和工廠標準化帶來的成果。預計2026年至2031年間,可變應用技術的市場規模將以10.4%的複合年成長率(CAGR)實現最高成長。這一成長主要歸功於播種、施肥和農藥施用處方管理功能的加入,從而提高了現有自動轉向平台的盈利。 2025年5月,約翰迪爾收購Sentera,將高高光譜遙測功能直接整合到其營運中心,取消了訂閱模式,並加速了互聯機械的普及。

遙感探測和分析服務提供者正在增強邊緣運算和即時處理能力,從而加快決策速度並降低田間評估的延遲。互通性解決方案和改裝技術使老舊設備能夠連接到最新的精密農業系統,加速了注重成本的營運商採用這些系統。同時,人工智慧 (AI) 分析在作物監測和產量最佳化等應用領域日益受到關注,但由於其數據需求高且實施複雜,目前仍僅限於技術嫻熟的用戶。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 透過最佳化投入材料,實現變異性管理,進而降低成本。

- 補貼以促進智慧設備的使用

- 物聯網感測器、無人機和分析技術的普及。

- 透過精準利用氮肥獲得排碳權

- 大型農場的專用 5G 網路

- 土壤微生物組分析能夠實現適應性施肥。

- 市場限制因素

- 尖端技術的高昂資本成本

- 資料互通性和隱私方面的挑戰

- 農村地區農業技術工程師短缺

- 農村地區頻段分散導致連接差異

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 硬體

- 軟體

- 服務

- 透過技術

- 導航(GPS(全球定位系統)/GNSS(全球導航衛星系統))

- 遙感探測

- 可變利率技術

- 人工智慧驅動的分析

- 透過使用

- 產量監測

- 實地測繪

- 作物調查

- 氣象追蹤與預報

- 灌溉管理

- 庫存和勞動力管理

- 按農場規模

- 大型農場(1000英畝或以上)

- 中型農場(250-999英畝)

- 小規模農場(少於250英畝)

- 按地區

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deere & Company

- Trimble Inc.

- CNH Industrial NV

- AGCO Corporation

- Topcon Corporation

- Farmers Edge Inc.

- Hexagon AB

- Lindsay Corporation

- Valmont Industries, Inc

- TeeJet Technologies(Spraying Systems Co.)

- Ag Leader Technology, Inc.

- DroneDeploy, Inc.

- Kubota Corporation

- Sentera, Inc.

- The Climate Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the north america precision agriculture market is projected to grow from USD 4.10 billion in 2025 and USD 4.37 billion in 2026 to USD 6.05 billion by 2031, registering a CAGR of 6.7% between 2026 and 2031.

This report is Segmented by Component (Hardware, Software, and More), by Technology (Guidance (GPS/GNSS) and More), by Application (Yield Monitoring and More), by Farm Size (Large Farms (More Than 1, 000 Acres), and More), and by Geography (United States, Canada, Mexico, and Rest of North America). The Market Forecasts are Provided in Terms of Value (USD).

North America Precision Agriculture Market Trends and Insights

Optimized Variable-Rate Inputs Lowering Costs

Variable-rate technology enables growers to adjust seed, fertilizer, and pesticide application rates within specific micro-zones, reducing waste by 10%-15% and providing immediate cash-flow benefits . John Deere's ExactApply nozzle system achieved herbicide savings of up to 77% during trials conducted in Nebraska and Kansas in 2025 . Adoption of this technology is advancing most rapidly in areas with high soil variability and existing GPS-guided tractors, particularly in regions such as Iowa, Illinois, and Saskatchewan. Dealers have reported strong sales of retrofit controllers, which can be installed on existing planters at one-third the cost of full replacements.

Subsidies Promoting Smart Equipment Use

Cost-share incentives remain significant in promoting the adoption of precision agriculture technologies across North America. In the United States, the Department of Agriculture enhanced conservation funding programs, including the Environmental Quality Incentives Program, during 2021-2023. This expansion increased financial support for precision farming tools and climate-smart practices. Similarly, in Canada, Agriculture and Agri-Food Canada launched the Agricultural Clean Technology Program in 2021, providing cost-sharing assistance for precision equipment, sensors, and energy-efficient technologies, with funding available through 2026.

High Capital Costs for Advanced Technologies

Equipment costs remain high for a standard package comprising RTK receivers, drone platforms, and variable-rate controllers. This expense poses a significant challenge for small grain farms, which struggle to amortize such investments when net returns are limited. High initial investment requirements continue to be a significant barrier to the adoption of precision agriculture technologies in North America. The substantial upfront costs of advanced equipment, including GPS-guided systems, sensors, and data platforms, discourage adoption, particularly among small and mid-sized farms with limited capital access. Beyond hardware expenses, farmers also face difficulties in assessing the return on investment due to uncertainties regarding long-term economic benefits and the operational complexity of these technologies.

Other drivers and restraints analyzed in the detailed report include:

- Increased Adoption of IoT Sensors, Drones, and Analytics

- Carbon-Credit Gains from Precise Nitrogen Use

- Data Interoperability and Privacy Issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware captured the largest 68.0% of the North America precision agriculture market share in 2025, owing to the entrenched base of GPS receivers and drone platforms. Even so, the software market size is projected to grow at the fastest 9.8% CAGR from 2026 to 2031. The Climate Corporation gained new FieldView subscribers, with a significant portion opting to pay additional fees for variable-rate scripting and carbon-credit documentation. In 2023, Trimble announced its mixed-fleet precision agriculture strategy through a joint venture with AGCO, emphasizing integration across equipment brands and data systems. By 2024, this initiative expanded into broader multi-brand connectivity and data integration platforms, enabling telemetry interoperability across the Deere & Company, CNH Industrial N.V., and AGCO Corporation .

Service-based offerings are expanding in response to increasing operational complexity, with vendors emphasizing integrated digital platforms and remote support to minimize reliance on on-site interventions. Equipment manufacturers are incorporating telematics, connectivity, and agronomic advisory services into their offerings, aligning revenue models with performance outcomes and fostering long-term customer engagement. Additionally, advanced sensing technologies, such as hyperspectral imaging and soil analysis tools, are being integrated into broader digital ecosystems. Proprietary analytics play a key role in transforming raw data into actionable insights for effective farm management.

Guidance (GPS/GNSS) held the largest 37.5% of the North America precision agriculture market share in 2025, reflecting two decades of retrofits and factory installs. The variable-rate technology market size is projected to grow at the fastest 10.4% CAGR from 2026 to 2031. This growth is driven by the addition of prescription control over seeding, fertilization, and chemical application, which enhances returns on existing autosteer platforms. In May 2025, John Deere's acquisition of Sentera integrated hyperspectral analytics directly into its Operations Center, eliminating a subscription layer and facilitating adoption for connected machines.

Remote sensing and analytics providers are enhancing edge computing and real-time processing capabilities, enabling quicker decision-making and reducing delays in field assessments. Interoperability solutions and retrofit technologies are improving accessibility by allowing older machinery to connect with modern precision systems, facilitating broader adoption among cost-conscious operators. While artificial intelligence-driven analytics are gaining traction for applications like crop monitoring and yield optimization, adoption remains limited to technologically advanced users due to high data requirements and implementation complexities.

List of Companies Covered in this Report:

- Deere & Company

- Trimble Inc.

- CNH Industrial N.V.

- AGCO Corporation

- Topcon Corporation

- Farmers Edge Inc.

- Hexagon AB

- Lindsay Corporation

- Valmont Industries, Inc

- TeeJet Technologies (Spraying Systems Co.)

- Ag Leader Technology, Inc.

- DroneDeploy, Inc.

- Kubota Corporation

- Sentera, Inc.

- The Climate Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Optimized variable-rate inputs lowering costs

- 4.2.2 Subsidies promoting smart equipment use

- 4.2.3 Increased adoption of IoT sensors, drones, and analytics

- 4.2.4 Carbon-credit gains from precise nitrogen use

- 4.2.5 Private 5G networks on large farms

- 4.2.6 Soil-microbiome analytics enabling adaptive fertility

- 4.3 Market Restraints

- 4.3.1 High capital costs for advanced technologies

- 4.3.2 Data interoperability and privacy issues

- 4.3.3 Lack of ag-tech technicians in rural areas

- 4.3.4 Connectivity gaps due to fragmented rural spectrum

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software

- 5.1.3 Services

- 5.2 By Technology

- 5.2.1 Guidance (GPS (Global Positioning System)/GNSS (Global Navigation Satellite System))

- 5.2.2 Remote Sensing

- 5.2.3 Variable-rate Technology

- 5.2.4 AI-enabled Analytics

- 5.3 By Application

- 5.3.1 Yield Monitoring

- 5.3.2 Field Mapping

- 5.3.3 Crop Scouting

- 5.3.4 Weather Tracking and Forecasting

- 5.3.5 Irrigation Management

- 5.3.6 Inventory and Labor Management

- 5.4 By Farm Size

- 5.4.1 Large Farms (more than 1,000 acres)

- 5.4.2 Medium Farms (250-999 acres)

- 5.4.3 Small Farms (less than 250 acres)

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

- 5.5.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 Trimble Inc.

- 6.4.3 CNH Industrial N.V.

- 6.4.4 AGCO Corporation

- 6.4.5 Topcon Corporation

- 6.4.6 Farmers Edge Inc.

- 6.4.7 Hexagon AB

- 6.4.8 Lindsay Corporation

- 6.4.9 Valmont Industries, Inc

- 6.4.10 TeeJet Technologies (Spraying Systems Co.)

- 6.4.11 Ag Leader Technology, Inc.

- 6.4.12 DroneDeploy, Inc.

- 6.4.13 Kubota Corporation

- 6.4.14 Sentera, Inc.

- 6.4.15 The Climate Corporation

7 Market Opportunities and Future Outlook

精密農業成像技術市場:全球市場按技術類型、平台、頻譜範圍、組件和應用分類的預測,2026-2032年

精密農業成像技術市場:全球市場按技術類型、平台、頻譜範圍、組件和應用分類的預測,2026-2032年 高精度自主機器人市場:按類型、運作模式、電源、最終用途、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

高精度自主機器人市場:按類型、運作模式、電源、最終用途、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 下一代精密農業:趨勢與市場展望(2025-2035)

下一代精密農業:趨勢與市場展望(2025-2035) 精密農業市場規模、佔有率、成長、全球產業分析、區域趨勢及2026年至2034年預測。

精密農業市場規模、佔有率、成長、全球產業分析、區域趨勢及2026年至2034年預測。 精密農業成像技術市場規模、佔有率及成長分析:依成像技術類型、平台、資料處理方法、應用、最終用戶和地區分類-2026年至2033年產業預測

精密農業成像技術市場規模、佔有率及成長分析:依成像技術類型、平台、資料處理方法、應用、最終用戶和地區分類-2026年至2033年產業預測 2026年全球精密農業市場報告種子檢測設備市場:2026-2032年全球市場預測(按感測器類型、連接方式、銷售管道、最終用戶和應用分類)2026年全球精密農業物聯網市場報告2026年全球農業遙感探測技術市場報告

2026年全球精密農業市場報告種子檢測設備市場:2026-2032年全球市場預測(按感測器類型、連接方式、銷售管道、最終用戶和應用分類)2026年全球精密農業物聯網市場報告2026年全球農業遙感探測技術市場報告 精密農業市場規模、佔有率、趨勢和預測:按技術、類型、組件、應用和地區分類(2026-2034 年)

精密農業市場規模、佔有率、趨勢和預測:按技術、類型、組件、應用和地區分類(2026-2034 年)