|

市場調查報告書

商品編碼

2063296

底部填充式點膠機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Underfill Dispenser - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

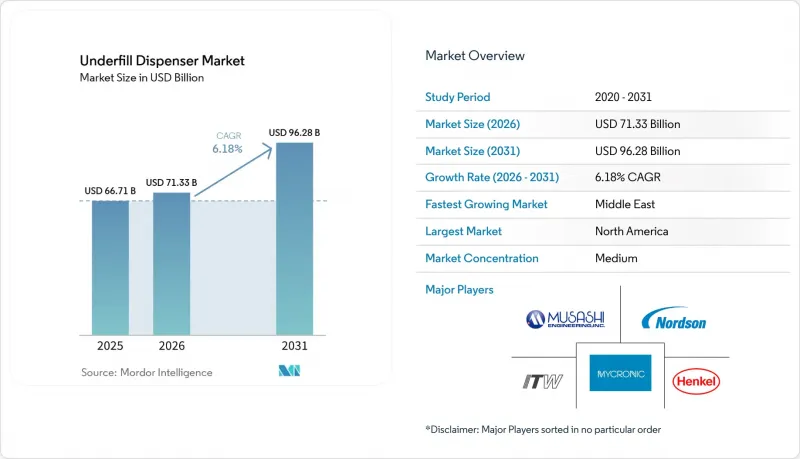

據 Mordor Intelligence 稱,2025 年底部填充分配器市值為 667.1 億美元,預計到 2031 年將達到 962.8 億美元,而 2026 年為 713.3 億美元,預測期(2026-2031 年)的複合年成長率為 6.18%。

本報告按產品類型(例如,毛細管流動式底部填充點膠機)、技術(例如,壓電噴射、氣動針頭)、應用(例如,覆晶構裝)、最終用戶(例如,半導體組裝和測試服務提供者 (OSAT))、點膠容量範圍(例如,小於 5 奈升)和地區進行細分。市場預測以美元 (USD) 為單位。

全球底部灌裝分配器市場趨勢及洞察

人工智慧最佳化的點膠路徑規劃可縮短週期時間。

整合到視覺系統中的機器學習演算法產生的點膠軌跡,與基於規則的程式設計相比,可將底部填充製程時間縮短 15% 至 25%。這是 Coherix 於 2025 年引進台積電 CoWoS 封裝生產線的 3D 視覺偵測系統中的一項功能。這些模型能夠評估表面幾何形狀、基板翹曲和回流焊接溫度歷史,並即時調整噴嘴接近角度和壓力。據採用該技術的領先組裝稱,配方開發時間已從 50 小時縮短至不到 10 小時,使工程資源能夠重新投入到新的封裝認證工作中。可靠性的提昇在碳化矽 (SiC) 功率模組中尤其明顯,因為傳統的基於規則的控制器無法維持非牛頓流體底部填充材料所需的壓力曲線。更快的路徑規劃也提高了關鍵指標:設備運轉率,因為頂級噴射系統的資本成本超過 100 萬美元。

採用高密度異構整合封裝

晶片級拓樸結構廣泛應用於人工智慧加速器和高效能CPU,使得晶片間凸塊間距縮小至40微米以下。為了避免焊點間出現橋接,底部填充材料必須包含小於2微米的填充顆粒,並且點膠機需要以±1微米的精度分配1至4納升的點。雙閥噴射平台現在可以在毛細管流動和模塑底部填充材料之間即時切換,將生產線切換時間從90分鐘縮短至15分鐘。在同一班次內處理多種基板佈局的組裝製造商報告稱,生產效率提高了20-25%,這充分展現了精密噴射技術在底部填充點膠機市場的競爭優勢。

先進噴射平台需要高額資本投資

新一代壓電點膠機整合了線上視覺系統、雙閥配置和100級防護等級外殼,單價在80萬至120萬美元之間。目前利潤率較低的中小型組裝製造商,由於採用傳統的球柵陣列(BGA)封裝,如果沒有外部資金支持,根本無法承擔這些成本。儘管預計到2026年半導體製造設備產業的總資本投資將達到2,000億美元,但底部填充點膠機的運轉率仍將維持在65%至70%左右。這是因為組裝線需要在覆晶、球柵陣列和晶圓層次電子構裝等不同製程之間切換。每種工藝都需要不同的點膠配方,每次切換需要2至4小時。在平均65%至70%的運轉率下,工人每個班次都需要多次更換配方,這使得投資報酬率(ROI)的計算更加困難。因此,許多二線供應商繼續選擇價格低於 25 萬美元的氣動針頭分配器,儘管它們無法滿足汽車和航太項目的缺口目標。

細分市場分析

預計到2025年,噴射點膠機將佔據最大的銷售佔有率,而噴射平台底部填充點膠機市場預計將在2026年至2031年間以6.77%的複合年成長率成長。其非接觸式操作可防止基板損壞,並實現小於5奈升的液滴形成。這些特性對於間距為25微米或更小的晶片至關重要。將毛細管流動和噴射點膠頭整合到單一機架中的混合型設備可減少40%的面積,使工廠能夠將多個傳統製程整合到一條生產線上。

儘管在黏度超過 50,000 cP 的高黏度封裝領域,針頭式系統仍然佔據主導地位,但隨著材料供應商不斷改進配方以匹配壓電噴射器的剪切特性,人們對針頭式系統的興趣正在減弱。在家用電子電器產業,由於成本方面的考慮,3-5% 的空隙率是可以接受的,因此毛細管流動式點膠機仍然發揮著重要作用。然而,人工智慧驅動的路徑規劃已將噴射平台的運轉率提升至近 80%,從而縮小了整體擁有成本 (TCO) 的差距。因此,無論是跨國公司還是本地的 OSAT(外包半導體組裝公司),底部填充點膠機市場的採購預算都在顯著地轉向噴射系統。

預計到2025年,壓電噴射技術將佔銷售額的34.54%,其在底部填充點膠機市場的佔有率預計將以6.94%的複合年成長率成長。目前,擁有超過1500個噴嘴的列印頭以20kHz的頻率驅動,在保持±2微米定位精度的同時,每小時可實現超過9萬個點的列印量。雖然氣動針頭工具在東南亞處理0.5毫米間距BGA的生產線上仍佔據一定的市場佔有率,但關鍵的先進封裝技術藍圖已明確指出,對於間距小於20微米的晶片,壓電技術的應用前景廣闊。

容積式泵浦和螺旋推進器在晶圓層次電子構裝佔據了一席之地,它們能夠滿足持續流速超過 10 mL/min 的需求,而壓電堆難以應對此流速範圍。薄膜轉移技術已在高度小於 200 μm 的超薄 MEMS 模組領域站穩腳跟,但缺乏廣泛的化學支持限制了其目前的成長。總體而言,機器視覺和即時點膠檢驗技術的日益融合,正在鞏固壓電技術在主流異構整合方案中,尤其是在底部填充點膠機市場中的領先地位。

區域分析

到2025年,亞太地區將佔全球銷售額的53.73%,其核心是台灣的先進封裝工廠,這些總合將運作超過500台高精度點膠機。在韓國,隨著耗資129億美元的HBM綜合體破土動工,預計2026年韓國市場將加速成長,該項目至少獲得了40台頂級噴射點膠機的訂單。在中國當地,儘管出口限制限制了EUV晶圓的產能,但在本土GPU新創企業引領的2.5D舉措推動下,本地需求仍實現了兩位數成長。日本市場保持穩定,但主要依賴國內供應商提供的分階段升級方案,這些方案更受重視保守認證計畫的汽車產業客戶的青睞。

中東地區預計將以6.57%的複合年成長率成長,成為成長最快的地區。主權財富基金正在支持阿拉伯聯合大公國和沙烏地阿拉伯的多家晶圓廠,其中包括一條價值160億美元的邏輯晶片生產線,該生產線具備晶片組裝能力。該地區的政策目標是到2028年培育50家本土半導體企業,採購文件中已明確要求使用與台灣地區類似的窄間隙底部填充劑分配器。

儘管《晶片封裝和晶片保護法案》(CHIPS Act)提供了支持國內封裝的獎勵,北美和歐洲的封裝市場仍保持著個位數的中段成長率,因為它們面臨著工程人才短缺的困境。雖然精密噴射分配器已在亞利桑那州和薩克森州的試點生產線上投入使用,但全球只有幾百名工程師專門從事晶圓級底部填充技術,導致操作員培訓週期過長。南美洲和非洲市場仍在發展中,但一家巴西汽車零件供應商已開始對用於軟性燃料控制器的無空隙封裝進行認證,這表明該地區底部填充分配器市場訂單可能增加。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 利用人工智慧最佳化配料路線,縮短週期時間。

- 採用高密度異構整合封裝

- 在 3D 晶片堆疊的過渡需要無空隙的底部填充材料。

- 汽車功率半導體需求不斷成長

- 矽光電和共封裝光學組件的成長

- 窄間距晶片基板的出現

- 市場限制因素

- 先進噴射平台需要高額資本投資

- 面板級包裝生產線的分配能力限制

- 減小晶片間距會增加助焊劑洩漏和污染的風險。

- 晶圓級底部填充程式工程工程師短缺。

- 產業價值鏈分析

- 監理情勢

- 宏觀經濟因素對市場的影響

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 毛細管流動式底部填充分配器

- 噴射式分配系統

- 組合/混合系統

- 針頭分發系統

- 透過技術

- 壓電噴射

- 氣動針

- 螺旋鑽

- 容積式泵

- 底片轉印系統

- 透過使用

- 覆晶封裝

- 球柵陣列(BGA)封裝

- 晶圓級封裝(WLP)

- MEMS和感測器封裝

- 光電和光電封裝

- 功率半導體封裝

- 最終用戶

- 半導體組裝和測試外包公司(OSAT)

- 垂直整合設備製造商(IDM)

- 鑄造廠

- 電子製造服務 (EMS) 供應商

- 光電裝置製造商

- 研究與發展機構/研究機構

- 排放體積範圍

- 少於5納升

- 5-30納升

- 30納升或更多

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nordson Corporation

- Musashi Engineering, Inc.

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc.(Camalot Systems)

- Fisnar Inc.

- GPD Global

- Essemtec AG

- Mycronic AB

- MKS Instruments, Inc.

- Scheugenpflug GmbH

- Techcon Systems, Inc.

- SMART VISION Co., Ltd.

- bdtronic GmbH

- Shenzhen Second Intelligent Equipment Co., Ltd.

- Dispensing Technology Corporation

- PVA(Precision Valve & Automation, Inc.)

- ViscoTec Pumpen-u. Dosiertechnik GmbH

- Universal Instruments Corporation

- Fuji Corporation

- Panasonic Holdings Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the underfill dispenser market size was valued at USD 66.71 billion in 2025 and estimated to grow from USD 71.33 billion in 2026 to reach USD 96.28 billion by 2031, at a CAGR of 6.18% during the forecast period (2026-2031).

This report is Segmented by Product Type (Capillary Flow Underfill Dispensers, and More), Technology (Piezoelectric Jetting, Pneumatic Needle, and More), Application (Flip Chip Packaging, and More), End-User (Outsourced Semiconductor Assembly and Test (OSAT) Companies, and More), Dispensing Volume Range (Less Than 5 Nanolitres, and More), and Geography. The Market Forecasts are Provided in Value (USD).

Global Underfill Dispenser Market Trends and Insights

AI-Optimized Dispense Path Planning Reduces Cycle Time

Machine-learning algorithms embedded in vision systems now generate dispense trajectories that cut underfill cycle time by 15-25%, compared to rule-based programming, a capability that Coherix introduced in its 3D vision inspection systems deployed at TSMC's CoWoS packaging lines in 2025. These models assess the topography, substrate warpage, and reflow temperature history, then adjust nozzle approach angles and pressure in real time. Major assembly houses deploying the technology report that recipe development time has fallen from 50 hours to less than 10, freeing engineering resources for new package qualifications. Reliability gains are notable in silicon carbide power modules, where non-Newtonian underfill chemistries demand pressure profiles that legacy rule-based controllers cannot sustain. Faster path planning also raises equipment utilization, a key metric, as capital costs for top-tier jetting systems exceed USD 1 million.

Adoption of High-Density Heterogeneous Integration Packages

Chiplet topologies permeate artificial-intelligence accelerators and high-performance CPUs, driving die-to-die bump pitch below 40 micrometers. Underfill materials must carry filler particles no larger than 2 micrometers to avoid bridging between solder joints, pushing dispensers to deliver 1-4 nanoliter dots with +-1 micrometer accuracy. Dual-valve jetting platforms now switch instantly between capillary-flow and molded underfill chemistries, reducing line changeover from 90 minutes to 15 minutes. Assembly houses handling multiple substrate layouts inside the same shift report throughput lifts of 20-25%, reinforcing the competitive case for precision jetting in the underfill dispenser market.

High Capex of Advanced Jetting Platforms

Next-generation piezoelectric jetting dispensers bundled with inline vision, dual-valve setups, and Class-100 enclosures command USD 800,000-1,200,000 per unit. Small and mid-size assembly houses that process legacy ball-grid-array packages at modest margins cannot absorb these costs without external financing. The semiconductor equipment industry's aggregate capital expenditure reached USD 200 billion in 2026, yet equipment utilization rates for underfill dispensers averaged 65-70% as assembly lines cycled between flip chip, ball grid array, and wafer-level packaging processes that require different dispense recipes and material changeovers consuming 2-4 hours per transition. The ROI equation becomes more challenging when line utilization averages 65-70%, since crews change recipes several times per shift. Consequently, many second-tier providers still opt for pneumatic needle dispensers priced below USD 250,000, even though those tools cannot meet void targets for automotive or aerospace programs.

Other drivers and restraints analyzed in the detailed report include:

- Transition to 3D Chip-Stacking Demands Void-Free Underfill

- Increasing Demand for Automotive-Grade Power Semiconductors

- Limited Dispensing Throughput for Panel-Level Packaging Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Jet dispensers accounted for the largest share of 2025 revenue, and the underfill dispenser market for jet platforms is forecast to grow at a 6.77% CAGR over 2026-2031. Their non-contact operation eliminates substrate scratches and allows sub-5-nanoliter dots, attributes crucial for chiplets separated by 25 micrometers or less. Hybrid machines that combine capillary-flow and jetting heads in a single frame now cut floor space by 40% and help factories consolidate multiple legacy processes onto a single line.

Needle systems still dominate high-viscosity encapsulants above 50,000 cP, but interest is waning as material suppliers reformulate chemistries to match the shear profiles of piezoelectric ejectors. Cost sensitivity keeps capillary-flow dispensers relevant in consumer electronics, where 3-5% void levels remain acceptable. Even so, AI-driven path planning lifts utilization for jetting platforms to nearly 80%, narrowing the total cost of ownership gap. As a result, the underfill dispenser market is seeing procurement budgets tilt decisively toward jet systems at both multinational and regional OSATs.

Piezoelectric jetting captured 34.54% of the revenue share in 2025, and its share of the underfill dispenser market is on track to widen, with a 6.94% CAGR projection. Printheads packing more than 1,500 nozzles now fire at 20 kHz, pushing hourly dot counts beyond 90,000 while holding +-2 micrometer positional tolerance. Pneumatic needle tools keep a share in Southeast Asian lines running 0.5 mm-pitch BGAs, but every major advanced-package roadmap specifies piezoelectric capability for die gaps below 20 micrometers.

Positive-displacement pumps and auger screws fill a niche for wafer-level packaging that requires sustained flow above 10 mL/min, volumes outside the comfort zone of piezo stacks. Film transfer has gained a foothold among ultra-thin MEMS modules under 200 μm tall, yet the lack of broad chemical support limits growth today. Overall, expanded machine vision integration and real-time dispense verification consolidate piezoelectric technology's leadership across mainstream heterogeneous integration programs in the underfill dispenser market.

Geography Analysis

Asia-Pacific generated 53.73% of 2025 revenue, anchored by Taiwan's cluster of advanced packaging plants that together consume more than 500 high-precision dispensers. South Korea added momentum in 2026 as a USD 12.9 billion HBM complex broke ground, underwriting orders for at least 40 top-tier jetting tools. Mainland China's 2.5D initiatives, driven by domestic GPU startups, lifted local demand by double digits even as export controls constrained EUV wafer capacity. Japan remains steady but leans on domestic suppliers that deliver incremental upgrades favored by automotive customers with conservative qualification schedules.

The Middle East is poised for a 6.57% CAGR and is the fastest regional climber. Sovereign wealth funds back multiple fabs in the United Arab Emirates and Saudi Arabia, including a USD 16 billion logic line bundled with chiplet assembly capability. Regional policy targets 50 homegrown semiconductor firms by 2028, and procurement documents already specify narrow-gap underfill dispensers matching those used in Taiwan.

North America and Europe progress at mid-single-digit rates as CHIPS Act incentives subsidize domestic packaging but struggle with engineering talent shortages. Pilot lines in Arizona and Saxony have installed precision jetters yet report extended operator-training times because only a few hundred engineers worldwide specialize in wafer-level underfill. South America and Africa remain nascent, although Brazilian automotive suppliers have begun qualifying void-free encapsulants for flex-fuel controllers, hinting at future uptick in regional orders for the underfill dispenser market.

- Nordson Corporation

- Musashi Engineering, Inc.

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc. (Camalot Systems)

- Fisnar Inc.

- GPD Global

- Essemtec AG

- Mycronic AB

- MKS Instruments, Inc.

- Scheugenpflug GmbH

- Techcon Systems, Inc.

- SMART VISION Co., Ltd.

- bdtronic GmbH

- Shenzhen Second Intelligent Equipment Co., Ltd.

- Dispensing Technology Corporation

- PVA (Precision Valve & Automation, Inc.)

- ViscoTec Pumpen- u. Dosiertechnik GmbH

- Universal Instruments Corporation

- Fuji Corporation

- Panasonic Holdings Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI-optimised Dispense Path Planning Reduces Cycle Time

- 4.2.2 Adoption of High-Density Heterogeneous Integration Packages

- 4.2.3 Transition to 3D Chip-Stacking Demands Void-Free Underfill

- 4.2.4 Increasing Demand for Automotive-Grade Power Semiconductors

- 4.2.5 Growth of Silicon Photonics and Co-Packaged Optics Assemblies

- 4.2.6 Emergence of Chiplet-Based Substrates with Narrow Gap Spacing

- 4.3 Market Restraints

- 4.3.1 High Capex of Advanced Jetting Platforms

- 4.3.2 Limited Dispensing Throughput for Panel-Level Packaging Lines

- 4.3.3 Shrinking Die Gaps Intensify Flux/Contamination Risk

- 4.3.4 Talent Shortage in Process Engineering for Wafer-Level Underfill

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Capillary Flow Underfill Dispensers

- 5.1.2 Jet Dispensing Systems

- 5.1.3 Combination / Hybrid Systems

- 5.1.4 Needle Dispensing Systems

- 5.2 By Technology

- 5.2.1 Piezoelectric Jetting

- 5.2.2 Pneumatic Needle

- 5.2.3 Auger Screw

- 5.2.4 Positive Displacement Pump

- 5.2.5 Film Transfer Systems

- 5.3 By Application

- 5.3.1 Flip Chip Packaging

- 5.3.2 Ball Grid Array (BGA) Packaging

- 5.3.3 Wafer Level Packaging (WLP)

- 5.3.4 MEMS and Sensor Packaging

- 5.3.5 Photonics and Optoelectronic Packaging

- 5.3.6 Power Semiconductor Packaging

- 5.4 By End-User

- 5.4.1 Outsourced Semiconductor Assembly and Test (OSAT) Companies

- 5.4.2 Integrated Device Manufacturers (IDMs)

- 5.4.3 Foundries

- 5.4.4 Electronics Manufacturing Services (EMS) Providers

- 5.4.5 Photonics Device Manufacturers

- 5.4.6 Research and Development Institutions / Labs

- 5.5 By Dispensing Volume Range

- 5.5.1 Less than 5 Nanolitres

- 5.5.2 5-30 Nanolitres

- 5.5.3 More than 30 Nanolitres

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East

- 5.6.4.1 Saudi Arabia

- 5.6.4.2 United Arab Emirates

- 5.6.4.3 Rest of Middle East

- 5.6.5 Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Egypt

- 5.6.5.3 Rest of Africa

- 5.6.6 South America

- 5.6.6.1 Brazil

- 5.6.6.2 Argentina

- 5.6.6.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nordson Corporation

- 6.4.2 Musashi Engineering, Inc.

- 6.4.3 Henkel AG & Co. KGaA

- 6.4.4 Illinois Tool Works Inc. (Camalot Systems)

- 6.4.5 Fisnar Inc.

- 6.4.6 GPD Global

- 6.4.7 Essemtec AG

- 6.4.8 Mycronic AB

- 6.4.9 MKS Instruments, Inc.

- 6.4.10 Scheugenpflug GmbH

- 6.4.11 Techcon Systems, Inc.

- 6.4.12 SMART VISION Co., Ltd.

- 6.4.13 bdtronic GmbH

- 6.4.14 Shenzhen Second Intelligent Equipment Co., Ltd.

- 6.4.15 Dispensing Technology Corporation

- 6.4.16 PVA (Precision Valve & Automation, Inc.)

- 6.4.17 ViscoTec Pumpen- u. Dosiertechnik GmbH

- 6.4.18 Universal Instruments Corporation

- 6.4.19 Fuji Corporation

- 6.4.20 Panasonic Holdings Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment