|

市場調查報告書

商品編碼

2063289

日本輪胎製造設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Japan Tire Manufacturing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

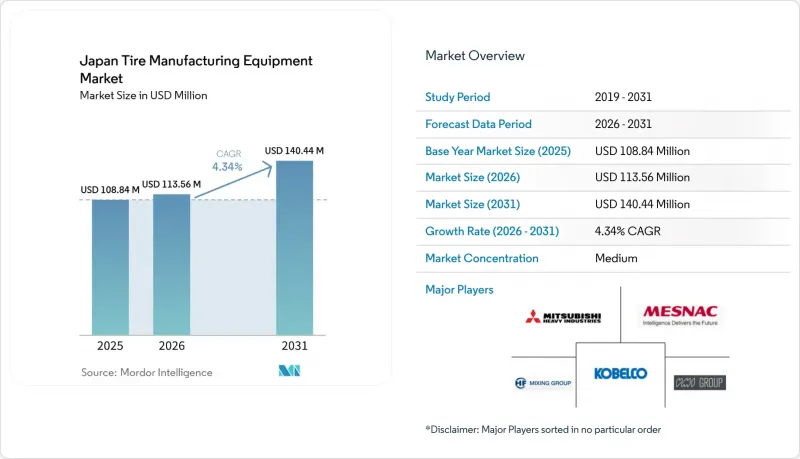

根據 Mordor Intelligence 預測,日本輪胎製造設備市場規模將從 2025 年的 1.0884 億美元和 2026 年的 1.1356 億美元成長到 2031 年的 1.4044 億美元,2026 年至 2031 年的複合年成長率為 4.34%。

本報告按設備類型(上游工程、成型工藝、硫化工藝和檢測工藝)、輪胎結構(斜交輪胎和子午線輪胎)、車輛類型(二輪車、三輪車等)、輪圈尺寸(12英寸及以下、12-18英寸、18英寸及以上)以及最終用戶(OEM和售後/替換市場)進行細分。市場預測以美元計價。

日本輪胎製造設備市場的趨勢與洞察

節能、高性能輪胎的需求日益成長

電動和混合動力汽車輪胎必須在低滾動阻力和高承載能力之間取得平衡。這項需求促使製造商採用富含二氧化矽的胎面配方,並保持壓延製程的公差。Bridgestone的「ENLITEN」配方象徵著產業的這項變革,它需要共擠出機頭來控制胎面層之間的硬度差異。與此同時,Yokohama Rubber正在投資賽車輪胎生產線以擴大產能。這項擴張凸顯了對精密硫化機日益成長的需求。專為電動車設計的輪胎現在整合了RFID晶片和用於胎壓監測系統的感測器插槽。這些創新不僅提高了車輛性能,還延長了傳統成型和切割設備的更換週期。為此,設備供應商正在推出先進的工具,例如雷射引導斜切機和伺服驅動胎面擠出機,所有這些工具都具有微米等級的精度。此外,目前處於試生產階段的生物基硫共聚物正在進一步降低滾動阻力。然而,這些共聚物改變了硫化反應的速率,需要對混合器進行升級,以適應低溫加工,以防止燒焦。

日本輪胎工廠的自動化與工業4.0實施

住友橡膠工業株式會社在其白川工廠安裝了日立PTC製造執行系統(MES)。該系統可即時匯總來自混煉機、擠出機、成型機和壓平機的即時數據,顯著減少意外停機時間。Bridgestone的BCMA模組進一步提升了效率,並大幅縮短了換模時間,無需手動更換滾筒,即可使用單台成型機實現不同SKU之間的無縫切換。神戶製鋼正在推廣一款即插即用的物聯網感測器套件,該套件可將扭力、黏度和溫度資料傳輸到基於雲端的AI控制面板。這些數位化最佳化的循環已顯著降低了每批次的能耗。雖然新機器都配備了感測器,但日本現有的大部分設備都是先前安裝的,這為改造升級提供了巨大的機會。尤其值得一提的是,資金籌措來源不斷增加,經濟產業省(METI)的補貼涵蓋了部分節能設備。這項支持顯著縮短了投資回收期。

硬化壓機投資成本高,投資回收期長

在日本,配備RFID標籤功能的最新型液壓淬火機價格昂貴。加上安裝費用,價格更是水漲船高。中型企業難以承受漫長的投資回收期,這不僅超過了標準貸款期限,而且幾乎與技術過時的時間線重疊。租賃模式在日本雖然存在,但仍然很少見。這主要是由於供應商和會計人員的共同推動,企業更傾向於完全擁有設備。因此,大型OEM廠商利用這種情況,大量訂購多台壓平機以獲得批量折扣。

相較之下,小規模的製造商則舉步維艱,他們推遲升級,並透過第三方維護合約延長老舊沖壓機的使用壽命。這種截然不同的做法抑制了新沖壓機的短期需求。然而,同時,人們對感測器改造套件、預測性維護軟體以及液壓系統的部分升級越來越感興趣。

細分市場分析

至2025年,上游工程混煉和配製設備將佔日本輪胎製造設備市場42.21%的佔有率。如此巨大的市場佔有率表明,隨著電動車(EV)輪胎逐漸成為主流,市場對精確配方控制的需求將大幅成長。目前,日本輪胎製造設備市場正在進行多個項目,旨在將再生填料和生物聚合物整合到混煉生產線中,同時確保批次間的一致性。供應商也在積極應用扭矩分析和自動送料斗等技術,這些技術對於保持低滾動阻力胎面所需的黏度一致性至關重要。

預計到2031年,切割和檢測系統將以6.21%的複合年成長率成長,超過所有其他類別。這一成長主要得益於攝影機引導的切割工作站、X光胎面掃描儀和人工智慧驅動的缺陷分類系統,尤其是在原始設備製造商(OEM)日益追求自動駕駛汽車輪胎零缺陷標準的情況下。此外,將可攜式智慧感測器改裝到傳統滾筒上,使工廠能夠在不更換舊設備的情況下收集預測性維護數據。這項功能對於空間有限的工廠尤其具有吸引力。

預計到2025年,子午線輪胎技術將佔日本輪胎製造設備市場89.22%的佔有率,並在2031年之前以6.39%的複合年成長率成長,確保日本輪胎製造設備市場能夠跟上全球汽車生產向子午線輪胎轉型的步伐。伺服驅動皮帶施布機透過即時監測張力,確保簾線角度保持在90度的最小公差範圍內。這種精度對於滿足原始設備製造商(OEM)規定的滾動阻力標準至關重要。

斜交輪胎設備佔據相當大的市場佔有率,主要服務於農業、建築和摩托車等特殊領域,出口市場主要集中在東南亞。儘管由於產量有限,成長緩慢,但像川田工程這樣的日本製造商透過出口價格遠低於子午線輪胎設備的緊湊型斜交輪胎切割機,確保了盈利。針對斜交輪胎硫化這項高能耗製程的國內永續性法規可能會阻礙未來的投資,而隨著新興市場逐步轉向子午線輪胎,過渡性需求仍在持續。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 節能、高性能輪胎的需求日益成長

- 日本輪胎工廠的自動化與工業4.0實施

- Bridgestone、住友、Yokohama Rubber等公司的產能擴張計劃

- 用於客製化電動車/自動駕駛汽車輪胎的靈活模組化設備

- 政府對用節能型機器取代老舊機器提供補助。

- 用於永續橡膠混合物的新型混合技術

- 市場限制因素

- 硬化壓平機的投資報酬率高,投資回收期長

- 原料成本波動給設備預算帶來了壓力。

- 老舊國內工廠的空間限制

- 經濟產業省對進口機械的認證流程出現延誤。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 依設備類型

- 上游工程(混合和組分製備)

- 攪拌機/橡膠攪拌機

- 日曆機

- 擠出機

- 切割機

- 其他(冷卻設備等)

- 結構工程

- 輪胎邊緣珠機

- 輪胎成型機

- 其他(例如,帶材繞線機)

- 固化和檢驗(測試區)

- 壓力成型機

- 輪胎噴漆機

- 其他(檢測設備等)

- 上游工程(混合和組分製備)

- 輪胎設計

- 偏見

- 徑向

- 車輛類型

- 摩托車

- 三輪車

- 搭乘用車

- 輕型商用車

- 中型和大型商用車輛

- 越野車

- 按輪圈尺寸

- 12英吋或更小

- 12-18英寸

- 18 英吋或更大

- 最終用戶

- 目的地設備製造商(OEM)

- 替換件/售後市場

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Kobe Steel Ltd.

- Mitsubishi Heavy Industries Machinery Systems, Ltd.

- Sanyo Machine Works, Ltd.

- Kawata Mfg. Co., Ltd.

- Fukui Rubber Industry Co., Ltd.

- Ishikawa Machinery Co., Ltd.

- Kurimoto Ltd.

- HF Mixing Group

- VMI Holland BV

- Mesnac Co., Ltd.

- Comerio Ercole SpA

- Zeppelin Systems GmbH

- L&T Rubber Processing Machinery

- Himile Mechanical Science & Technology Co., Ltd.

- Guilin Rubber Machinery Co., Ltd.

- Safe-Run Machinery(Suzhou)Co., Ltd.

- Steelastic Company LLC

- Pelmar Engineering Ltd.

- Uzer Makina

- Yingkou JinDing Machinery Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the japanese tire manufacturing equipment market size is projected to expand from USD 108.84 million in 2025 and USD 113.56 million in 2026 to USD 140.44 million by 2031, registering a CAGR of 4.34% between 2026 and 2031.

This report is Segmented by Equipment Type (Upstream, Building Area, and Curing & Inspection), Tire Design (Bias and Radial), Vehicle Type (Two-Wheelers, Three-Wheelers, and More), Rim Size (Up To 12 Inches, 12 To 18 Inches, and Above 18 Inches), and End-User (Original Equipment Manufacturers and Replacement/Aftermarket). The Market Forecasts are Provided in Terms of Value (USD).

Japan Tire Manufacturing Equipment Market Trends and Insights

Rising Demand for Fuel-Efficient, High-Performance Tires

Tires for electric and hybrid vehicles must balance low rolling resistance with higher load ratings. This need pushes manufacturers to adopt silica-rich treads and maintain calendering tolerances. Bridgestone's ENLITEN compound showcases this industry shift, necessitating co-extrusion heads to manage durometer variance across tread layers . Meanwhile, Yokohama Rubber is investing in a motorsports line to boost capacity. This expansion highlights the growing demand for precision curing presses. Tires tailored for EVs now feature sensor pockets for RFID chips and tire-pressure monitoring. These innovations not only enhance vehicle performance but also extend replacement cycles for traditional building and cutting machines. In response, equipment suppliers are rolling out advanced tools like laser-guided bias cutters and servo-driven tread extruders, both boasting micron-level accuracy. Additionally, pilot-produced bio-based sulfur copolymers are achieving a reduction in rolling resistance. However, these copolymers modify cure kinetics, necessitating upgrades to mixers for lower-temperature processing to prevent scorching.

Automation and Industry 4.0 Adoption in Japanese Tire Plants

Sumitomo Rubber deployed a Hitachi-PTC manufacturing execution system (MES) at its Shirakawa facility. This system aggregates live data from mixers, extruders, builders, and presses, leading to a significant reduction in unplanned downtime. Bridgestone's BCMA module further enhances efficiency, cutting changeover time substantially. This allows a single building machine to seamlessly switch between SKUs without manual drum changes. Kobe Steel is promoting bolt-on IoT sensor kits that transmit data on torque, viscosity, and temperature to cloud-based AI dashboards. These digitally optimized cycles have already achieved notable energy savings per mixing batch. While new machines come equipped with embedded sensors, a large portion of Japan's existing machines were installed earlier, presenting a significant retrofit opportunity. Financing options are becoming more accessible, especially with METI subsidies covering a portion of qualifying energy-efficient equipment. This support has significantly shortened the payback period.

High CAPEX and Long Payback Period for Curing Presses

In Japan, a modern hydraulic curing press equipped with RFID tagging comes with a high price tag. When installation is factored in, costs rise further. Mid-sized firms grapple with extended payback horizons. This duration not only surpasses standard financing tenors but also inches perilously close to the timelines for technological obsolescence. While leasing models are available, they remain a rarity in Japan. This is largely due to a prevailing preference for outright ownership, championed by both suppliers and accountants. As a result, larger OEMs capitalize on this landscape, placing multi-press orders to secure volume discounts.

In contrast, smaller producers find themselves in a bind, delaying replacements and extending the life of their older presses through third-party service contracts. This pronounced divergence in approach dampens immediate demand for new presses. However, it simultaneously amplifies interest in sensor-retrofit kits, predictive-maintenance software, and partial hydraulic upgrades.

Other drivers and restraints analyzed in the detailed report include:

- Flexible Modular Equipment for EV/AV Tire Customization

- Capacity-Expansion Programs by Leading OEMs

- Raw-Material Cost Volatility Squeezing Equipment Budgets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, upstream mixing and preparation assets accounted for 42.21% of the Japanese tire manufacturing equipment market. This dominance underscores the surging demand for precise compound control, especially as electric vehicle (EV) tires become increasingly mainstream. Projects in Japan's tire manufacturing equipment market are now integrating recycled fillers and bio-polymers into mixing lines, all while ensuring batch uniformity. Suppliers are also adopting torque analytics and automated feed hoppers, crucial for maintaining the consistent viscosity needed in low-rolling-resistance treads.

Systems for cutting and inspection are projected to expand at a 6.21% CAGR through 2031, outpacing all other categories. This growth is driven by camera-guided knife stations, X-ray tread scanners, and AI-driven defect classifiers, especially as OEMs enforce zero-defect standards for tires in autonomous vehicles. Additionally, portable smart sensors are being retrofitted onto legacy drums, enabling plants to gather predictive maintenance data without replacing older equipment. This capability is particularly appealing for shops with limited space.

Radial-tire technology commanded 89.22% of the Japanese tire manufacturing equipment market in 2025 and is expected to grow at a 6.39% CAGR through 2031, keeping the Japanese tire manufacturing equipment market firmly aligned with global radially-skewed automotive production. Servo-driven belt applicators now ensure the 90-degree cord angle remains within a minimal margin by monitoring tension in real-time. This precision is crucial for meeting OEM-specified rolling resistance metrics.

Holding a notable market share, the bias-tire gear caters to specialty farm, construction, and two-wheeler segments, with exports primarily directed to Southeast Asia. While growth remains modest due to limited unit volumes, Japanese manufacturers like Kawata Engineering find profitability by exporting compact bias cutters, priced significantly lower than their radial counterparts. Although national sustainability regulations target energy-intensive bias curing, potentially stifling future investments, a transitional demand endures as emerging markets gradually shift towards radial adoption.

List of Companies Covered in this Report:

- Kobe Steel Ltd.

- Mitsubishi Heavy Industries Machinery Systems, Ltd.

- Sanyo Machine Works, Ltd.

- Kawata Mfg. Co., Ltd.

- Fukui Rubber Industry Co., Ltd.

- Ishikawa Machinery Co., Ltd.

- Kurimoto Ltd.

- HF Mixing Group

- VMI Holland B.V.

- Mesnac Co., Ltd.

- Comerio Ercole S.p.A.

- Zeppelin Systems GmbH

- L&T Rubber Processing Machinery

- Himile Mechanical Science & Technology Co., Ltd.

- Guilin Rubber Machinery Co., Ltd.

- Safe-Run Machinery (Suzhou) Co., Ltd.

- Steelastic Company LLC

- Pelmar Engineering Ltd.

- Uzer Makina

- Yingkou JinDing Machinery Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Fuel-Efficient, High-Performance Tires

- 4.2.2 Automation and Industry 4.0 Adoption in Japanese Tire Plants

- 4.2.3 Capacity-Expansion Programs by Bridgestone, Sumitomo, Yokohama and Others

- 4.2.4 Flexible Modular Equipment for EV / AV Tire Customization

- 4.2.5 Government Subsidies for Energy-Efficient Machinery Upgrades

- 4.2.6 Novel Mixing Tech for Sustainable Rubber Blends

- 4.3 Market Restraints

- 4.3.1 High CAPEX and Long Payback Period for Curing Presses

- 4.3.2 Raw-Material Cost Volatility Squeezing Equipment Budgets

- 4.3.3 Space Constraints in Aging Domestic Plants

- 4.3.4 Slow METI Certification for Imported Machinery

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Equipment Type

- 5.1.1 Upstream (Mixer & Component Preparation)

- 5.1.1.1 Mixing Machines / Rubber Mixers

- 5.1.1.2 Calendaring Machines

- 5.1.1.3 Extrusion Machines

- 5.1.1.4 Cutting Machines

- 5.1.1.5 Others (Cooling Units, etc.)

- 5.1.2 Building Area

- 5.1.2.1 Bead Winding Machine

- 5.1.2.2 Tire Building Machine

- 5.1.2.3 Others (Strip Winding Machine, etc.)

- 5.1.3 Curing & Inspection (Testing Area)

- 5.1.3.1 Curing Press Machines

- 5.1.3.2 Tire Painting Machines

- 5.1.3.3 Others (Inspection Machines, etc.)

- 5.1.1 Upstream (Mixer & Component Preparation)

- 5.2 By Tire Design

- 5.2.1 Bias

- 5.2.2 Radial

- 5.3 By Vehicle Type

- 5.3.1 Two-wheelers

- 5.3.2 Three-wheelers

- 5.3.3 Passenger Cars

- 5.3.4 Light Commercial Vehicles

- 5.3.5 Medium & Heavy Commercial Vehicles

- 5.3.6 Off-Road Vehicles

- 5.4 By Rim Size

- 5.4.1 Up to 12 inches

- 5.4.2 12 to 18 inches

- 5.4.3 Above 18 inches

- 5.5 By End-User

- 5.5.1 Original Equipment Manufacturers (OEMs)

- 5.5.2 Replacement / Aftermarket

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Kobe Steel Ltd.

- 6.4.2 Mitsubishi Heavy Industries Machinery Systems, Ltd.

- 6.4.3 Sanyo Machine Works, Ltd.

- 6.4.4 Kawata Mfg. Co., Ltd.

- 6.4.5 Fukui Rubber Industry Co., Ltd.

- 6.4.6 Ishikawa Machinery Co., Ltd.

- 6.4.7 Kurimoto Ltd.

- 6.4.8 HF Mixing Group

- 6.4.9 VMI Holland B.V.

- 6.4.10 Mesnac Co., Ltd.

- 6.4.11 Comerio Ercole S.p.A.

- 6.4.12 Zeppelin Systems GmbH

- 6.4.13 L&T Rubber Processing Machinery

- 6.4.14 Himile Mechanical Science & Technology Co., Ltd.

- 6.4.15 Guilin Rubber Machinery Co., Ltd.

- 6.4.16 Safe-Run Machinery (Suzhou) Co., Ltd.

- 6.4.17 Steelastic Company LLC

- 6.4.18 Pelmar Engineering Ltd.

- 6.4.19 Uzer Makina

- 6.4.20 Yingkou JinDing Machinery Co., Ltd.

7 Market Opportunities & Future Outlook

無內胎輪胎市場:2026-2032年全球市場預測(依輪胎結構、車輛類型、材料、應用及銷售管道)汽車輪胎市場:2026-2032年全球市場預測(依輪胎類型、規格、輪胎寬度、輪圈尺寸、材質、季節、應用、車輛類型、最終用戶和銷售管道)

無內胎輪胎市場:2026-2032年全球市場預測(依輪胎結構、車輛類型、材料、應用及銷售管道)汽車輪胎市場:2026-2032年全球市場預測(依輪胎類型、規格、輪胎寬度、輪圈尺寸、材質、季節、應用、車輛類型、最終用戶和銷售管道) 2026-2030年全球汽車輪胎市場

2026-2030年全球汽車輪胎市場 充氣輪胎:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

充氣輪胎:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 日本輪胎市場規模、佔有率、趨勢和預測:按車輛類型、OEM和替換市場、進出口、子午線輪胎和斜交輪胎、有內胎和無內胎輪胎分類,2026-2034年

日本輪胎市場規模、佔有率、趨勢和預測:按車輛類型、OEM和替換市場、進出口、子午線輪胎和斜交輪胎、有內胎和無內胎輪胎分類,2026-2034年 無內胎輪胎市場:依設計、車輛類型、輪圈尺寸和地區分類。輪胎零售市場:按車輛類型、輪胎類型、分銷管道和地區分類。

無內胎輪胎市場:依設計、車輛類型、輪圈尺寸和地區分類。輪胎零售市場:按車輛類型、輪胎類型、分銷管道和地區分類。 2026年全球汽車輪胎OEM市場報告2026年全球輪胎平衡市場報告2026年全球汽車輪胎市場報告

2026年全球汽車輪胎OEM市場報告2026年全球輪胎平衡市場報告2026年全球汽車輪胎市場報告