|

市場調查報告書

商品編碼

2062381

充氣輪胎:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Pneumatic Tire - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

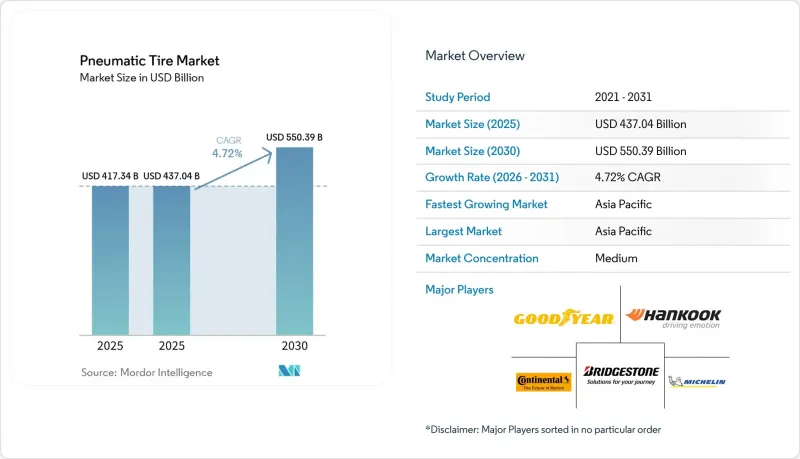

根據 Mordor Intelligence 預測,充氣輪胎市場規模將從 2025 年的 4,370.4 億美元成長到 2030 年的 5,503.9 億美元,2025 年至 2030 年的複合年成長率為 4.72%。

本報告按輪胎類型(子午線輪胎和斜交輪胎)、配銷通路(原廠配套和售後市場)、車輛類型(乘用車、輕型商用車、重型商用車、摩托車和越野車)以及地區(亞太地區、北美地區、歐洲地區、南美地區以及中東和非洲地區)進行細分。市場預測以美元計價。

全球充氣輪胎市場趨勢及洞察

節能、高性能輪胎的需求日益成長

為了符合自2027年車型年起實施的更為嚴格的企業平均燃油經濟性(CAFE)標準,車隊營運商正致力於降低滾動阻力。正如美國國家公路交通安全管理局(NHTSA)所指出的,這促使人們更多地使用富含二氧化矽的胎面配方和生物基油,以在不影響濕地抓地力的前提下降低滯後效應。例如,大陸集團的EcoContact和米其林的e.Primacy等產品已獲得歐盟燃油經濟性標籤的A級評級,這表明高性能和安全要求可以兼得。此外,電動車(EV)扭力的增加導致輪胎損耗率上升了約20%,促使原始設備製造商(OEM)要求加強胎側並最佳化胎面花紋以延長輪胎壽命。這些進步使供應商能夠在充氣輪胎市場中保持價格溢價。技術創新持續推動高性能輪胎領域的成長,其成長速度超過了整體替換輪胎市場。

電子商務和物流車輛的擴張

美國郵政服務公司 (USPS) 計劃在 2028 年部署 106,000 輛新一代送貨車輛,其中 66,000 輛將是電池式電動車。這一轉變凸顯了都市區送貨里程的不斷成長。固特異公司投資 3.2 億美元升級位於勞頓的工廠,旨在提高專為住宅送貨路線設計的低噪音、加固胎側輪胎的產能。在印度和印尼等市場,網路購物的快速成長正推動輕型商用車車隊從斜交輪胎轉向子午線輪胎。子午線輪胎較適合在頻繁啟動停止的情況下進行溫度控管。隨著小包裹量的增加,車隊管理人員正在採用可與遠端資訊處理系統配合使用的數據驅動型輪胎,這增加了輪胎更換的成本。這些趨勢共同推動了充氣輪胎市場收入的逐步成長。

加強有關廢棄物和微塑膠的環境法規

歐盟7排放標準收緊了顆粒物排放標準,預計到2032年還將進一步收緊。此外,美國已有24個州實施了生產者延伸責任制(EPR),將廢棄物處置成本轉嫁給製造商。為提高輪胎耐久性而採用的硬質胎面配方可能會影響濕地抓地力,因此需要對二氧化矽分散和聚合物交聯技術進行新的投資,以維持安全標準。皮尤慈善信託基金預測,到2050年,輪胎和煞車磨損將佔道路運輸顆粒物排放量的90%,將導致監管力道加大。據估計,遵守這些法規將使單位成本增加2%至4%,從而影響價格競爭力,尤其對於充氣輪胎市場利潤率較低的供應商更是如此。

細分市場分析

預計到2025年,子午線輪胎將佔市場佔有率的77.12%,這主要得益於人們對燃油效率和高速行駛安全性的日益重視。斜交輪胎預計到2031年將以5.15%的複合年成長率成長,超過充氣輪胎市場的整體複合年成長率。在擁有超過2.2億輛摩托車的印度,斜交輪胎因其防刺穿性和價格優勢,仍然廣受歡迎,尤其是在農村地區。同樣,在撒哈拉以南非洲,斜交輪胎也更受在非鋪路面上行駛的輕型卡車和三輪車的青睞。子午線輪胎的銷量仍佔很大佔有率,尤其是在電動車領域。普利司通已在日本投資270億日圓(約1.7億美元),用於擴大其專為重型電動車電池組設計的高剛性子午線輪胎的產能。

斜交輪胎製造商也在進行現代化轉型。像中策橡膠和三角輪胎這樣的公司正在加強其工程輪胎產品線,以滿足礦業和建築行業的需求,因為在這些行業中,子午線輪胎的優勢並不那麼明顯。同時,大陸集團的泰國工廠正專注於生產用於摩托車和電動車的子午線輪胎,以提高乘坐舒適性和扭矩控制。為了平衡性能和永續性,製造商正在豐富產品系列,以滿足充氣輪胎市場多樣化的應用情境。

區域分析

預計到2025年,亞太地區將佔全球輪胎市場佔有率的44.15%,並在2031年之前以5.49%的複合年成長率成長。這一成長主要得益於中國每年8.4億條輪胎的產量、印度向子午線輪胎的轉型以及東協(東南亞國家聯盟)國家商用車市場的擴張。玲瓏輪胎在安徽工廠投資7.5億美元,將使其產能增加1400萬條;中芯橡膠杭州工廠採用5G技術,將使其乘用車子午線輪胎產量翻倍至2000萬條。這些發展將滿足區域需求,增強出口能力,鞏固亞太地區在充氣輪胎市場的地位。

儘管北美地區的銷售成長放緩,但由於高階電動車輪胎的普及,單價上漲,固特異輪胎公司從中受益。美國輪胎製造商協會(USTMA)預測,2025年固特異輪胎出貨量將達3.404億條,銷售量僅成長0.9%。然而,價格結構的改善預計將提振營收。固特異正致力於生產配備感測器、低噪音的電動車輪胎,為此,固特異在勞頓投資3.2億美元進行擴建,並在加拿大投資5.75億加元(約4.1516億美元)進行現代化改造。同時,歐洲市場面臨成本挑戰,預計2024年德國的產量將下降4.3%。此外,大陸集團關閉了位於馬來西亞亞羅士打的工廠,以降低高成本產能。

南美洲、中東和非洲市場規模雖小規模,但戰略地位舉足輕重。玲瓏輪胎在巴西的合資企業規避了反傾銷稅,並向南方共同市場成員國的組裝商供應輪胎。在中東,沙烏地阿拉伯和阿拉伯聯合大公國的基礎建設推動了需求成長,但外匯波動抑制了投資意願。在非洲,仿冒品佔替換輪胎銷量的40%之多,對合法充氣輪胎製造商構成了挑戰。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 節能、高性能輪胎的需求日益成長

- 電子商務和物流車輛的擴張

- 車輛老化導致售後市場需求加速成長

- 對輪胎效率和標籤有嚴格的規定。

- 整合式智慧輪胎感測器進行預測性維護

- 市場限制因素

- 加強有關廢棄物和微塑膠的環境法規

- 假冒偽劣輪胎湧入新興市場

- 無氣輪胎和實心輪胎在小眾應用領域的興起

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按輪胎類型

- 子午線輪胎

- 斜交輪胎

- 透過分銷管道

- OEM

- 售後市場

- 車輛類型

- 搭乘用車

- 輕型商用車

- 大型商用車輛

- 摩托車

- 越野車

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 澳洲和紐西蘭

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 南非

- 埃及

- 奈及利亞

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Apollo Tyres Ltd

- Bridgestone

- Continental AG

- Giti Tire

- Hankook Tire & Technology

- Kumho Tire Co., Inc.

- Linglong Tire

- Maxxis International

- Michelin

- MRF Tyres

- Nokian Tyres plc

- Pirelli & CSpA

- Sailun Group Co., Ltd

- Sumitomo Rubber Industries, Ltd

- The Goodyear Tire & Rubber Company

- The Yokohama Rubber Co., Ltd

- Toyo Tire Corporation

- Zhongce Rubber Group Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the pneumatic tire market size is projected to expand from USD 417.34 billion in 2025 and USD 437.04 billion in 2025 to USD 550.39 billion by 2030, registering a CAGR of 4.72% between 2025 to 2030.

This report is Segmented by Tire Type (Radial Tires and Bias Tires), Distribution Channel (OEM and Aftermarket), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Two-Wheelers, and Off-The-Road Vehicles), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Pneumatic Tire Market Trends and Insights

Rising Demand for Fuel-Efficient and High-Performance Tires

Fleet operators are focusing on reducing rolling resistance to comply with the Corporate Average Fuel Economy (CAFE) standards, which will become stricter starting with model-year 2027. This has led to the use of silica-rich tread compounds and bio-based oils that lower hysteresis without affecting wet grip, as noted by the National Highway Traffic Safety Administration (NHTSA). Products such as Continental EcoContact and Michelin e.Primacy, which holds A-ratings for European Union (EU) fuel-efficiency labels, demonstrates that high performance can align with safety requirements. Additionally, the increased torque of electric vehicles (EVs) raises tire wear rates by approximately 20%, prompting original equipment manufacturers (OEMs) to require reinforced sidewalls and optimized tread patterns to extend tire service life. These advancements enable suppliers to maintain price premiums in the pneumatic tire market. Technological innovation continues to drive growth in high-performance tire segments, outpacing overall replacement market growth.

Expansion of E-Commerce and Logistics Fleets

The United States Postal Service (USPS) plans to deploy 106,000 next-generation delivery vehicles by 2028, with 66,000 of these being battery-electric vehicles. This shift highlights the increasing urban delivery mileage. Goodyear's USD 320 million upgrade to its Lawton facility aims to expand production capacity for low-noise tires with reinforced sidewalls, specifically designed for residential delivery routes. In markets like India and Indonesia, the rapid growth of online shopping is driving light-commercial fleets to transition from bias-ply to radial tires, which are better suited for managing heat during frequent stop-start cycles. As parcel volumes increase, fleet managers are adopting data-enabled tires that integrate with telematics systems, thereby increasing switching costs. These trends collectively contribute to incremental revenue growth in the pneumatic tire market.

Tighter Environmental Rules on Disposal and Micro-Plastics

Euro 7 regulations introduce stricter particulate limits, with further tightening expected by 2032. Additionally, 24 United States (U.S.) states have implemented Extended Producer Responsibility (EPR) laws, transferring disposal costs to manufacturers. The use of harder tread compounds, while addressing durability, can affect wet-grip performance, necessitating new investments in silica dispersion and polymer cross-linking technologies to maintain safety standards. According to the Pew Charitable Trusts, tire and brake wear is projected to account for 90% of road-transport particulates by 2050, leading to increased regulatory scrutiny. Compliance with these regulations is estimated to raise unit costs by 2%-4%, impacting price competitiveness, particularly for low-margin suppliers in the pneumatic tire market.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Aftermarket Demand from Ageing Vehicle Parc

- Stringent Tire-Efficiency and Labeling Regulations

- Counterfeit and Low-Quality Tire Influx in Developing Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Radial tires accounted for 77.12% of market value in 2025, driven by regulatory emphasis on fuel efficiency and high-speed safety. Bias tires are projected to grow at a compound annual growth rate (CAGR) of 5.15% through 2031, surpassing the overall pneumatic tire market CAGR. In India, with a two-wheeler base exceeding 220 million units, bias tires remain popular due to their puncture resistance and affordability, particularly among rural users. Similarly, in Sub-Saharan Africa, bias tires are preferred for light trucks and three-wheelers operating on unpaved roads. Radial tires continue to dominate revenue generation, especially in electric vehicles. Bridgestone's JPY 27 billion (USD 0.17 billion) investment in Japan has expanded capacity for high-rigidity radial tires designed for heavier electric vehicle (EV) battery packs.

Bias tire manufacturers are also modernizing. Companies like Zhongce Rubber and Triangle Tire are enhancing their engineering tire lines to cater to the mining and construction sectors, where radial advantages are less pronounced. Meanwhile, Continental's plant in Thailand focuses on motorcycle and EV radial tires, which improve ride quality and torque management. As manufacturers aim to balance performance and sustainability, they are diversifying their product portfolios to address varied use cases across the pneumatic tire market.

Geography Analysis

Asia-Pacific accounted for 44.15% of the market value in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 5.49% through 2031. This growth is supported by China's annual output of 840 million units, India's transition to radial tires, and the expansion of commercial vehicle markets in ASEAN (Association of Southeast Asian Nations) countries. Linglong's USD 750 million Anhui plant adds 14 million units to its capacity, while ZC Rubber's 5G-enabled Hangzhou facility doubles its output to 20 million passenger radials. These developments address regional demand and enhance export capabilities, reinforcing Asia-Pacific's role in the pneumatic tire market.

North America shows slower volume growth but benefits from higher per-unit values due to the increasing adoption of premium electric vehicle (EV) tires. The United States Tire Manufacturers Association (USTMA) projects 340.4 million shipments in 2025, reflecting a modest 0.9% volume growth. However, an improved price mix is expected to drive revenue. Goodyear's USD 320 million expansion in Lawton and a CAD 575 million (USD 415.16 million) modernization project in Canada focus on producing sensor-ready, low-noise EV tires. Meanwhile, Europe faces cost challenges, with German production declining by 4.3% in 2024. Additionally, Continental closed its Malaysian Alor Setar plant to reduce high-cost capacity.

South America and the Middle East & Africa remain smaller markets but hold strategic importance. Linglong's joint venture in Brazil circumvents anti-dumping tariffs and supplies tires to Mercosur assemblers. In the Middle East, infrastructure development in Saudi Arabia and the United Arab Emirates (UAE) drives demand, although currency volatility dampens investment enthusiasm. In Africa, counterfeit products account for up to 40% of replacement tire sales, posing challenges for legitimate players in the pneumatic tire market.

- Apollo Tyres Ltd

- Bridgestone

- Continental AG

- Giti Tire

- Hankook Tire & Technology

- Kumho Tire Co., Inc.

- Linglong Tire

- Maxxis International

- Michelin

- MRF Tyres

- Nokian Tyres plc

- Pirelli & C. S.p.A.

- Sailun Group Co., Ltd

- Sumitomo Rubber Industries, Ltd

- The Goodyear Tire & Rubber Company

- The Yokohama Rubber Co., Ltd

- Toyo Tire Corporation

- Zhongce Rubber Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Fuel-Efficient and High-Performance Tires

- 4.2.2 Expansion of E-Commerce and Logistics Fleets

- 4.2.3 Accelerated Aftermarket Demand from Ageing Vehicle Parc

- 4.2.4 Stringent Tire-Efficiency and Labelling Regulations

- 4.2.5 Integration of Smart-Tire Sensors for Predictive Maintenance

- 4.3 Market Restraints

- 4.3.1 Tighter Environmental Rules on Disposal and Micro-Plastics

- 4.3.2 Counterfeit and Low-Quality Tire Influx in Developing Markets

- 4.3.3 Emergence of Airless and Solid Tires in Niche Uses

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Tire Type

- 5.1.1 Radial Tires

- 5.1.2 Bias Tires

- 5.2 By Distribution Channel

- 5.2.1 OEM

- 5.2.2 Aftermarket

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.3.4 Two-Wheelers

- 5.3.5 Off-the-Road Vehicles

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Australia and New Zealand

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Egypt

- 5.4.5.6 Nigeria

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Apollo Tyres Ltd

- 6.4.2 Bridgestone

- 6.4.3 Continental AG

- 6.4.4 Giti Tire

- 6.4.5 Hankook Tire & Technology

- 6.4.6 Kumho Tire Co., Inc.

- 6.4.7 Linglong Tire

- 6.4.8 Maxxis International

- 6.4.9 Michelin

- 6.4.10 MRF Tyres

- 6.4.11 Nokian Tyres plc

- 6.4.12 Pirelli & C. S.p.A.

- 6.4.13 Sailun Group Co., Ltd

- 6.4.14 Sumitomo Rubber Industries, Ltd

- 6.4.15 The Goodyear Tire & Rubber Company

- 6.4.16 The Yokohama Rubber Co., Ltd

- 6.4.17 Toyo Tire Corporation

- 6.4.18 Zhongce Rubber Group Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

2026-2030年全球汽車輪胎市場

2026-2030年全球汽車輪胎市場 日本輪胎製造設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

日本輪胎製造設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 無內胎輪胎市場:依結構、車輛類型及銷售管道分類-2026-2032年全球市場預測汽車輪胎市場:2026-2032年全球市場預測(按輪胎類型、型號、寬度、輪圈尺寸、材料、季節、應用、車輛類型、最終用戶和銷售管道)

無內胎輪胎市場:依結構、車輛類型及銷售管道分類-2026-2032年全球市場預測汽車輪胎市場:2026-2032年全球市場預測(按輪胎類型、型號、寬度、輪圈尺寸、材料、季節、應用、車輛類型、最終用戶和銷售管道) 日本輪胎市場規模、佔有率、趨勢和預測:按車輛類型、OEM和替換市場、進出口、子午線輪胎和斜交輪胎、有內胎和無內胎輪胎分類,2026-2034年

日本輪胎市場規模、佔有率、趨勢和預測:按車輛類型、OEM和替換市場、進出口、子午線輪胎和斜交輪胎、有內胎和無內胎輪胎分類,2026-2034年 無內胎輪胎市場:依設計、車輛類型、輪圈尺寸和地區分類。輪胎零售市場:按車輛類型、輪胎類型、分銷管道和地區分類。

無內胎輪胎市場:依設計、車輛類型、輪圈尺寸和地區分類。輪胎零售市場:按車輛類型、輪胎類型、分銷管道和地區分類。 2026年全球汽車輪胎OEM市場報告2026年全球輪胎平衡市場報告2026年全球汽車輪胎市場報告

2026年全球汽車輪胎OEM市場報告2026年全球輪胎平衡市場報告2026年全球汽車輪胎市場報告