|

市場調查報告書

商品編碼

2063259

太陽能板清潔:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Solar Panel Cleaning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

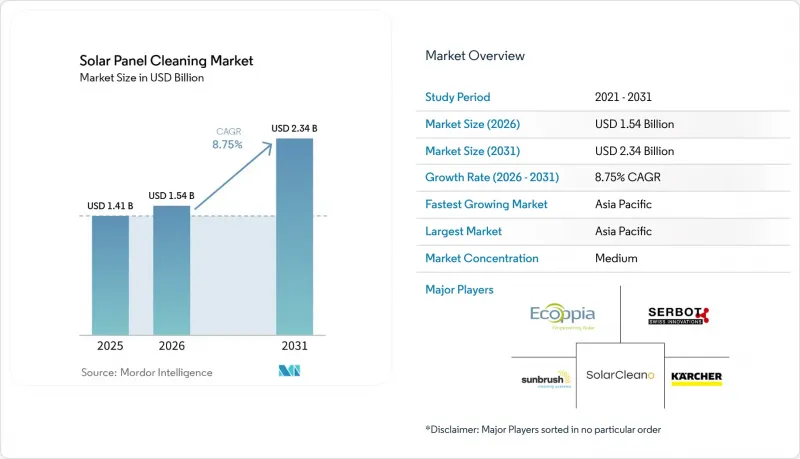

根據 Mordor Intelligence 預測,太陽能板清潔市場規模將從 2025 年的 14.1 億美元和 2026 年的 15.4 億美元成長到 2031 年的 23.4 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 8.75%。

本報告按清潔方法(濕式、乾式、靜電式、塗層式)、技術水準(手動、半自動、自主機器人、無人機)、部署類型(住宅、商業/工業、公用事業規模、浮體式太陽能發電)、服務模式(自主運營、第三方提供、機器人即服務)以及地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球太陽能板清潔市場趨勢及洞察

在乾旱地區快速興建大型太陽能發電廠

在沙烏地阿拉伯的舒艾巴和蘇代爾太陽能發電廠,污垢導致高達70%的電力損失,因此頻繁的清潔循環在經濟上至關重要。為此,位於拉賈斯坦邦的1吉瓦普加爾太陽能發電廠已在合約中規定,如果營運商未能達到清潔標準,將處以每千瓦時6印度盧比的罰款。昆士蘭州和新南威爾斯州的大規模太陽能發電廠仍在與沙塵暴作鬥爭,如今,配備磷酸鐵鋰電池、能夠攀爬20度斜坡的機器人全天候運作,已成為必然之選。國際能源總署(IEA)估計,污垢造成的損失佔全球太陽能發電量的4%至7%,相當於每年50億歐元的收入損失。供應商正在透過使用地形適應性履帶式機器人和輕質複合材料來降低偏遠沙漠地區的運輸成本。這些創新技術正在透過自動化清潔來加強電力購買協議(PPA)的保護生態系統,並為吉瓦級建設項目提供資金籌措支援。

更嚴格的運維和績效比率合約

西孟加拉邦10兆瓦屋頂光電競標和智利ENGIE 181.25兆瓦交流電專案均納入了發電量閾值,迫使服務供應商承擔污染風險,從而推動了對能夠拍攝並傳輸每次清潔週期照片證據的機器人的需求。印度太陽能公司(SECI)的標準化維運模板規定,在季風季節和收割後粉塵濃度高峰期,每兩週進行一次清潔,以確保印度的實踐符合歐盟可再生能源指令的標準。西班牙和義大利的資產所有者將獎勵支付與即時車隊數據掛鉤,迫使供應商整合基於雲端的儀表板和預測性維護分析。結果是,採購環境以績效為導向,合約的成功不僅取決於設備價格,還取決於清潔頻率。

對全自動機器人的高資本投入

在美國,一套10千瓦的屋頂光電系統,每套售價5萬至15萬美元,投資回收期超過10年,而年收入僅4,500美元。 Serbot的操縱桿控制PV Eco STANDARD系統降低了成本門檻,但仍需要人工操作,減緩了50千瓦以下小型系統的普及。 BladeRanger公司佔據了該細分市場18%的收入,專注於兆瓦級契約,透過規模經濟分攤部署機器人的成本。利率上升和淨計量獎勵的減少預計到2024年,美國住宅太陽能裝置將下降31%至32%,這將抑制對昂貴自動化系統的需求。雖然租賃模式和機器人即服務(RaaS)可以將資本支出(Capex)轉化為營運支出(OpEx),但對於分散的屋頂用戶來說,訂閱費用在經濟上仍然不可行。

細分市場分析

預計到2025年,濕式清洗將佔太陽能板清洗市場60.0%的佔有率,而乾刷機器人的市佔率也不斷擴大。高壓噴射系統在西班牙、義大利和阿拉伯聯合大公國等沿海地區佔據主導地位,這些地區由於鹽膜的存在,需要定期清洗。但Solaris Hydrobotics公司的液壓馬達機器人每個電池板僅需0.5至1.5公升水,使其成為水資源豐富但缺乏電網覆蓋地區的理想選擇。

Ecoppia公司3900兆瓦的無水清潔裝置表明,在沙漠地區消除油輪可以降低30-40%的營運成本。 Bluesky和Nomadd公司測試的一種摩擦驅動電磁篩可在7分鐘內去除90%的灰塵,展現了未來無刷解決方案的發展方向。 Chemitek公司的可生物分解化學品可用於農光互補設施的行間無人機噴灑,從而打造出一套結合濕式和空中噴灑技術的混合工具包。在中東和北非地區,水價已超過每立方公尺5美元,乾式平台正逐漸取代濕式方法的主導地位,太陽能板清潔產業的採購政策也開始將無水清潔方案作為2026年後運作電廠的預設選項。

在太陽能板清潔市場,到2025年,手動設備仍將佔50.2%的銷售額,這主要是因為在住宅和1兆瓦以下屋頂設施中,低廉的人事費用超過了效率提升帶來的收益。在印度和東南亞等屋頂坡度不均勻的商業和工業設施中,半自動手推車正在填補成本缺口。

全自動機器人正以11.4%的複合年成長率快速成長,這得益於精度高達±10公分的GPS定位、機器視覺以及可避免熱衝擊的夜間運作。隨著美國聯邦航空管理局(FAA)批准多架無人機於2025年用於太陽能發電作業,預計空中系統將與地面履帶式機器人配合,並在崎嶇地形上進行作業。 EAUAV公司的無人機每天可清潔8000至10000平方公尺,從而擴大了高海拔地區太陽能板的清潔範圍。同時,Infosys-Kaynes公司的「Kleinbot」機器人則專注於清潔被空調設備遮擋的緊湊型屋頂。整個太陽能板清潔產業正朝著地面機器人和無人機結合的整合車隊發展,加速淘汰純人工清潔系統。

區域分析

預計到2025年,亞太地區將佔全球銷售額的45.1%,並在2031年之前維持10.0%的年均成長率。中國289吉瓦的組件產量和印度每兩週一次的清潔義務構成了市場需求的基礎。同時,天合光能的行間清潔系統已使阿爾巴尼亞152兆瓦和馬來西亞100兆瓦太陽能電站的發電量提高了8%至15%。 2022年,日本、韓國和東南亞國協新增太陽能發電裝置容量41.4吉瓦,推動了適用於人口密集都市區屋頂的可攜式機器人的普及。

在北美,受《通膨抑制法案》的推動,2021年至2024年間,大型太陽能發電廠的建設量激增73%。然而,利率上升導致2024年住宅裝置量下降了31%至32%。在亞利桑那州和索諾拉州等沙漠地區,人們依靠機器人系統清理乾燥的林地,以避免使用成本超過1000美元的水罐車。在加拿大安大略省和亞伯達,兼具除雪功能的半自動化平台正廣受歡迎,而且不會影響組件的保固。

2022年,歐洲新增太陽能發電裝置容量41.4吉瓦,根據「REPowerEU」計劃,目標是達到450吉瓦交流電。但在西班牙,季節性沙塵在旱季會使發電量減少高達15%。目前,西班牙和葡萄牙的標準配置是採用混合系統,該系統使用乾燥機器人進行日常維護,並使用濕式系統進行徹底清潔。北歐的太陽能發電廠更傾向於使用軟輥式除雪解決方案,而德國的上網電價補貼(FIT)政策鼓勵屋頂太陽能發電的推廣,因此需要輕鬆易攜的設備。

中東和非洲的污染率位居世界前列,日污染率高達0.9%,因此引進無水清潔機器人勢在必行。在沙烏地阿拉伯的「2030願景」綜合體中,Ecoppia機器人無需用水即可實現99.92%的清潔效率。南非和埃及也正在效仿,水資源短缺加上雄心勃勃的太陽能發電項目,正鞏固該地區作為乾旱地區創新先鋒的地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在乾旱地區快速興建大型太陽能發電廠

- 更嚴格的運維績效比率合約

- 降低乾刷機器人系統的平準化能源成本

- 在光伏組件保固中增加了防污性能KPI。

- 以ESG主導的零用水營運維護要求

- 市場限制因素

- 全自動機器人需要高資本投入

- 屋頂安裝的投資報酬率僅限於50千瓦以下的系統。

- 關於刷子磨損產生的微塑膠,監管方面存在灰色地帶。

- 機器人維護領域技術純熟勞工短缺

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過清洗方法

- 濕式(供水刷、高壓噴射)

- 乾式(旋轉刷、氣流)

- 靜電/離子

- 自清潔塗層(防水、防污)

- 按技術水準

- 手動工具

- 半自動(手推車式、曳引機式)

- 全自動機器人

- 基於無人機的系統

- 不同的發展

- 住宅屋頂光電發電系統(20kW 或以下)

- 商業和工業用途(20千瓦至1兆瓦)

- 公用事業規模(1兆瓦或以上)

- 浮體式太陽能發電陣列

- 按服務模式

- 內部維運團隊

- 外部清潔服務提供者

- 機器人即服務 (RaaS) 訂閱

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和市場佔有率)

- 公司簡介

- Ecoppia

- SunBrush mobil GmbH

- Karcher

- Serbot AG

- SolarCleano

- RST CleanTech

- Heliotex

- Sunpure Technology

- IPC Eagle

- PV Clean Mobile(USA)

- Clean Solar Industries

- KP Group

- TrinaRobot

- ChemiTek

- IFBOT Robotics

- Exosun

- Energy Robotics

- Aqua Solar Cleaners

- Limpeza Solar(Brazil)

- Muller Solar Services

第7章 市場機會與未來展望

According to Mordor Intelligence, the solar panel cleaning market size is projected to expand from USD 1.41 billion in 2025 and USD 1.54 billion in 2026 to USD 2.34 billion by 2031, registering a CAGR of 8.75% between 2026 to 2031.

This report is Segmented by Cleaning Method (Wet, Dry, Electrostatic, Coating-Based), Technology Level (Manual, Semi-Automatic, Autonomous Robots, Drones), Deployment (Residential, Commercial & Industrial, Utility-Scale, Floating PV), Service Model (In-House, Third-Party, Raas), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are in Value (USD).

Global Solar Panel Cleaning Market Trends and Insights

Rapid Utility-Scale PV Build-Outs in Arid Zones

Soiling losses of up to 70% in Saudi Arabia's Shuaibah and Sudair complexes have made frequent cleaning cycles financially critical, triggering contractual mandates in Rajasthan's 1 GW Pugal park that fine operators INR 6 per kWh for under-performance. Large arrays in Queensland and New South Wales battle dust storms that now justify 24/7 robotic fleets equipped with LiFePO4 batteries capable of climbing 20-degree slopes. The IEA estimates soiling erodes 4-7% of global PV output, equal to EUR 5 billion in lost revenue each year . Suppliers respond with terrain-adaptive tracks and lightweight composites that lower transport costs to remote desert sites. These innovations reinforce an ecosystem where automated cleaning protects power-purchase guarantees and underpins bankability for gigawatt-scale builds.

Stricter O&M Performance-Ratio Contracts

Generation thresholds embedded in West Bengal's 10 MW rooftop tender and Chile's 181.25 MWac ENGIE project force service providers to shoulder soiling risk, catalyzing demand for robots that capture and transmit photographic proof of every cleaning cycle. SECIs standardized O&M template now requires biweekly cleaning during monsoon and post-harvest dust peaks, aligning Indian practice with EU Renewable Energy Directive standards. Asset owners in Spain and Italy link incentive payments to real-time fleet data, compelling vendors to integrate cloud-based dashboards and predictive maintenance analytics. The net result is a performance-driven procurement environment where cleaning cadence, not just equipment price, determines contract awards.

High Capex of Fully-Autonomous Robots

Price tags of USD 50,000-150,000 per unit impose decade-long paybacks on 10 kW U.S. rooftops earning only USD 4,500 annually. Serbot's joystick-controlled PV Eco STANDARD eases cost barriers but still demands human presence, slowing adoption below the 50 kW threshold. BladeRanger, holding 18% segment revenue, focuses on multi-MW contracts where fleets amortize cost over scale. Rising interest rates and declining net-metering incentives kept U.S. residential solar installations down 31-32% in 2024, dampening demand for expensive automation. Leasing models and Robot-as-a-Service convert capex to opex, yet subscription fees remain uneconomic for scattered rooftop owners.

Other drivers and restraints analyzed in the detailed report include:

- Falling LCOE of Dry-Brush Robotic Systems

- PV Module Warranties Adding Anti-Soiling KPIs

- Skilled-Labor Shortages for Robot Fleet Servicing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dry-brush robots captured a growing share as wet cleaning retained 60.0% of the solar panel cleaning market size in 2025. High-pressure jet systems dominate coastal Spain, Italy, and the UAE, where salt films demand periodic rinsing, while Solaris Hydrobotics' water-motor robots consume only 0.5-1.5 liters per panel and thrive where water is plentiful yet grid power is absent .

Ecoppia's 3,900 MW of water-free deployments illustrate how eliminating tanker-truck logistics cuts operating expenses 30-40% in deserts. Triboelectric electrodynamic screens tested by Bluesky and Nomadd remove 90% of dust in seven minutes, offering a future zero-brush solution. Biodegradable agents from Chemitek enable drone spraying over agrivoltaic rows, blending wet and aerial techniques into a hybrid toolkit. As water prices surpass USD 5 per m3 in MENA, dry platforms are steadily eroding wet dominance, and the solar panel cleaning industry is witnessing procurement policies that now default to zero-water options for plants entering service after 2026.

Manual equipment still holds 50.2% of 2025 revenue in the solar panel cleaning market share, chiefly across residential and sub-MW rooftops where low labor costs outweigh efficiency gains . Semi-automatic trolleys bridge affordability gaps for Indian and Southeast Asian C&I sites with mixed roof angles.

Fully autonomous robots are scaling at an 11.4% CAGR, aided by GPS positioning accurate to +-10 cm, machine vision, and night-time operation that avoids thermal shock. FAA approval for multi-drone solar missions in 2025 positions aerial systems to complement ground crawlers on irregular terrain. EAUAV drones cleaning 8,000-10,000 m2 daily expand access to high-elevation arrays, while Infosys-Kaynes' Kleinbot targets compact roofs shaded by HVAC units. The solar panel cleaning industry as a whole is moving toward integrated fleets mixing ground robots and drones, accelerating the retirement of purely manual regimes.

Geography Analysis

Asia-Pacific accounted for 45.1% of global revenue in 2025 and is forecast to grow at 10.0% annually through 2031. China's module output of 289 GW and India's biweekly cleaning mandates anchor demand, while TrinaRobot's cross-row systems improved generation 8-15% across 152 MW in Albania and 100 MW in Malaysia. Japan, South Korea, and ASEAN nations added 41.4 GW of solar capacity in 2022, driving the uptake of portable robots suited to dense urban rooftops.

North America's utility-scale buildout surged 73% from 2021 to 2024 on the back of the Inflation Reduction Act, but residential installations fell 31-32% in 2024 as interest rates climbed. Desert states like Arizona and Sonora rely on dry-brush fleets to avoid USD 1,000-plus water-truck runs. Canada's Ontario and Alberta favor semi-automatic platforms that can double as snow-removal tools without violating module warranties.

Europe added 41.4 GW in 2022 and aims for 450 GWac under REPowerEU, with Spain's seasonal dust curtailing output up to 15% during dry spells. Hybrid regimes using dry robots for routine cycles and wet systems for deep cleans are now standard in Spain and Portugal. Nordic arrays prioritize soft-roller snow solutions, while Germany's feed-in tariffs spur rooftop growth, demanding lightweight portable equipment.

The Middle East and Africa experience the planet's worst soiling rates up to 0.9% per day,y making water-free robots essential. Saudi Arabia's Vision 2030 complexes employ Ecoppia fleets that reach 99.92% cleaning efficiency without a single liter of water. South Africa and Egypt follow suit as water scarcity converges with ambitious solar pipelines, reinforcing the region's status as a bellwether for dry-brush innovation.

- Ecoppia

- SunBrush mobil GmbH

- Karcher

- Serbot AG

- SolarCleano

- RST CleanTech

- Heliotex

- Sunpure Technology

- IPC Eagle

- PV Clean Mobile (USA)

- Clean Solar Industries

- KP Group

- TrinaRobot

- ChemiTek

- IFBOT Robotics

- Exosun

- Energy Robotics

- Aqua Solar Cleaners

- Limpeza Solar (Brazil)

- Muller Solar Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid utility-scale PV build-outs in arid zones

- 4.2.2 Stricter O&M performance-ratio contracts

- 4.2.3 Falling LCOE of dry-brush robotic systems

- 4.2.4 PV module warranties adding anti-soiling KPIs

- 4.2.5 ESG-driven water-neutral O&M mandates

- 4.3 Market Restraints

- 4.3.1 High capex of fully-autonomous robots

- 4.3.2 Limited ROI for rooftops <50 kW

- 4.3.3 Regulatory gray-zones on micro-plastics from brush wear

- 4.3.4 Skilled-labor shortages for robot fleet servicing

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Cleaning Method

- 5.1.1 Wet (Water-Fed Brush, High-Pressure Jet)

- 5.1.2 Dry (Rotary Brush, Air-Blast)

- 5.1.3 Electrostatic / Ionic

- 5.1.4 Coating-Based Self-Cleaning (Hydrophobic, Anti-Soiling)

- 5.2 By Technology Level

- 5.2.1 Manual Tools

- 5.2.2 Semi-Automatic (Trolley, Tractor-Mounted)

- 5.2.3 Fully-Autonomous Robots

- 5.2.4 Drone-Based Systems

- 5.3 By Deployment

- 5.3.1 Residential Rooftop (Up to 20 kW)

- 5.3.2 Commercial and Industrial (20 kW to 1 MW)

- 5.3.3 Utility-Scale (Above 1 MW)

- 5.3.4 Floating PV Arrays

- 5.4 By Service Model

- 5.4.1 In-House O&M Teams

- 5.4.2 Third-Party Cleaning Service Providers

- 5.4.3 Robot-as-a-Service (RaaS) Subscriptions

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Ecoppia

- 6.4.2 SunBrush mobil GmbH

- 6.4.3 Karcher

- 6.4.4 Serbot AG

- 6.4.5 SolarCleano

- 6.4.6 RST CleanTech

- 6.4.7 Heliotex

- 6.4.8 Sunpure Technology

- 6.4.9 IPC Eagle

- 6.4.10 PV Clean Mobile (USA)

- 6.4.11 Clean Solar Industries

- 6.4.12 KP Group

- 6.4.13 TrinaRobot

- 6.4.14 ChemiTek

- 6.4.15 IFBOT Robotics

- 6.4.16 Exosun

- 6.4.17 Energy Robotics

- 6.4.18 Aqua Solar Cleaners

- 6.4.19 Limpeza Solar (Brazil)

- 6.4.20 Muller Solar Services

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

太陽能板清潔市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、工藝、應用、運作模式、地區和競爭格局分類,2021-2031年

太陽能板清潔市場-全球產業規模、佔有率、趨勢、機會、預測:按技術、工藝、應用、運作模式、地區和競爭格局分類,2021-2031年 太陽能板清潔系統市場:依自動化程度、清潔方法、電源、最終用戶和分銷管道分類-2026-2032年全球市場預測

太陽能板清潔系統市場:依自動化程度、清潔方法、電源、最終用戶和分銷管道分類-2026-2032年全球市場預測 全球乾式自動太陽能板清洗市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球乾式自動太陽能板清洗市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 太陽能板清潔市場機會、成長要素、產業趨勢分析及2026年至2035年預測智慧太陽能清潔機器人市場按類型、電源、清潔模式、應用、最終用戶和分銷管道分類-全球預測(2026-2032 年)

太陽能板清潔市場機會、成長要素、產業趨勢分析及2026年至2035年預測智慧太陽能清潔機器人市場按類型、電源、清潔模式、應用、最終用戶和分銷管道分類-全球預測(2026-2032 年) 太陽能板清洗市場規模、佔有率和成長分析(按操作方式、類型、製程、應用和地區分類)—產業預測(2026-2033 年)

太陽能板清洗市場規模、佔有率和成長分析(按操作方式、類型、製程、應用和地區分類)—產業預測(2026-2033 年) 全球太陽能板自動乾式清洗市場全球太陽能板自動清潔市場

全球太陽能板自動乾式清洗市場全球太陽能板自動清潔市場 太陽能板清洗系統市場 - 成長、未來展望、競爭分析,2025 年至 2033 年

太陽能板清洗系統市場 - 成長、未來展望、競爭分析,2025 年至 2033 年 全球自動太陽能板清潔市場:成長、未來展望與競爭分析(2024-2032 年)

全球自動太陽能板清潔市場:成長、未來展望與競爭分析(2024-2032 年)