|

市場調查報告書

商品編碼

2063258

複閉器:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Recloser - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

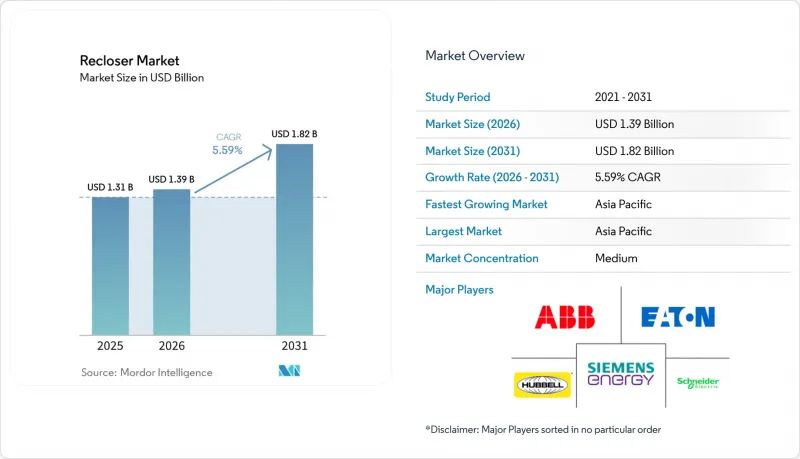

根據 Mordor Intelligence 預測,複閉器市場規模將從 2025 年的 13.1 億美元和 2026 年的 13.9 億美元成長到 2031 年的 18.2 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 5.59%。

本報告按中斷介質(例如,油浸絕緣)、相數(例如,單相)、控制方式(例如,液壓)、電壓等級(例如,15 kV 或以下)、安裝位置(例如,電線杆安裝)、最終用戶(公共產業、其他)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球複閉器市場趨勢與洞察

電力傳輸和分配網路現代化改造計畫激增,電力傳輸和分配自動化方面的支出增加。

電力公司已撥款4,800億美元用於2025年輸電網升級,並計畫在2035年投資5.8兆美元,其中約三分之一將用於配電自動化,包括高速複閉器。 EverSource公司已在其2025-2029年資本計畫中撥款162億美元,用於在其位於新英格蘭地區的整個線路上建造智慧電網,服務140萬用戶。中國國家電網公司正在為其西部省份建設13.75萬公里長的饋線,並由此獲得了27千伏和38千伏真空斷路開關的突破性訂單。亞伯達省一項為期20年、耗資51億美元的計劃,將三分之二的支出用於可再生能源主導的饋線自動化。同時,美國GRIP計畫已提供76億美元的津貼,用於野火預防項目,強制要求在沿海易洪地區使用地面安裝式複閉器。

加速中壓可再生能源併網。

截至2026年初,併網等待名單上的太陽能、風能和儲能容量總合將達到2600吉瓦,中位等待時間超過36個月,這迫使電力公司部署符合IEEE 1547-2018標準、能夠管理雙向電流的重合閘裝置。印度450吉瓦的可再生能源目標將需要210億美元的電網升級改造,其中大部分將用於33千伏特和11千伏系統,而複閉器將構成第一道保護屏障。杜克能源佛羅裡達公司指出,等待名單上有17吉瓦的資料中心負荷,這正在推動整個24千伏迴路中智慧複閉器裝置的加速部署。到2040年,東南亞國協將面臨3,000億美元的電網投資,以支持跨境電力交易,這將加劇對15-38千伏設備的持續需求。馬薩諸塞州的一家電力公司透過將 ADMS 軟體(可在 30 秒內重新路由電力)與複閉器結合,到 2025 年將故障恢復時間縮短了 60%。

對資本密集、過時的液壓設備維修

油壓設備每3至5年需要更換一次潤滑油,每次更換的維修費用在600至1000美元之間;而新的真空設備價格昂貴,售價在15000至40000美元之間,且需要10年才能收回投資。伊頓的Form 7維修套件透過重複利用電線電線杆結構,可將安裝成本降低40%,但歐洲工程需要額外支付2000至5000美元用於PCB(多氯聯苯)的處置,並且會延長工程工期。 ABB的Eagle單相無電池型號專為液壓設備的直接替換而設計,並可為現場工作人員加密Wi-Fi試運行通訊。

細分市場分析

真空斷路器以 8.0% 的複合年成長率推動市場成長,而氣體斷路器和無 SF6固體斷路器在 2025 年仍將佔據複閉器市場 60.3% 的最大佔有率。隨著歐洲電力公司開始更換 SF6 設備(SF6 設備將於 2026 年 1 月起被禁用),採用真空技術的複閉器市場規模預計將迅速擴大。

已轉型採用真空技術的電力公司表示,由於新型真空瓶無需補充氣體即可運作10,000次,因此維護成本降低。 ABB的SafePlus Air和Schneider Electric的GM AirSeT展示了維修現有安裝空間的案例,從而簡化了法規核准流程。在極寒和地震多發地區的配電室中,仍然使用充油式裝置,但能夠承受低至-50 度C溫度的新型密封真空瓶正在縮小其市場佔有率。

2025年,三相斷路器在複閉器市場佔據48.9%的佔有率,但預計到2031年,三相單線斷路器將以6.5%的複合年成長率超越三相斷路器。在處理灌溉和油田負載的農村電路中,僅切斷故障相即可將用戶的停電次數減少30%至40%。

Hubbell 的「LineDefender」和 ABB 的「Eagle」均配備可視故障指示器和自供電運作功能,電力線路工人無需起重機即可進行安裝。由於微處理器邏輯能夠同步獨立極點,電力公司預計即使在 27kV 主幹線路上,三極單極系統也將得到更廣泛的應用,以最佳化分散式能源 (DER) 的容量。

區域分析

預計到2025年,亞太地區將佔全球銷售額的42.8%,並以6.2%的複合年成長率成長,這主要得益於中國5740億美元的電網擴建項目和印度930億美元的變電站項目(該項目旨在實現500吉瓦的非石化燃料發電)。國家電網計畫鋪設13.75萬公里的新輸電線路,主要為35千伏線路,將直接刺激區域複閉器市場的發展。在太平洋島嶼地區,政府已根據「REnew Pacific」計畫投資建造了一個5兆瓦的微電網,該計畫展示了單相機組的有效性,即使在颶風爆發期間也能確保島嶼的無縫運作。

在北美,美國GRIP計畫正在全美50州投資76億美元用於野火預防和電力線路地下化。 EverSource公司162億美元的配電計畫以及加拿大自然資源部(NRCan)的津貼,都為電力公司持續投入資金提供了支持。維吉尼亞、佛羅裡達州和德克薩斯州的資料中心叢集指定使用符合IEC 61850 2.1版網路安全標準的34.5千伏基座安裝式式複閉器,並要求供應商實施MACsec和基於角色的存取控制。

在歐洲,SF6的禁用導致5萬至7萬台中壓設備需要維修。 ABB已提前向德國E.ON公司交付了SafeRing Air開關設備。Schneider Electric也已投資960萬美元用於其利茲工廠生產Ringmaster AirSeT開關設備。北歐配電業者(DSO),例如Landsnet,率先引進了透過光纖複閉器PMU的全數位化變電站,這種模式正在波羅的海國家和中歐地區推廣。

南美洲的成長主要得益於巴西國家電力監管局 (ANEEL) 強制推行的損耗降低舉措,以及智利阿塔卡馬地區對採礦設備的投資增加。專為海拔高達 4500 公尺的環境設計的基座安裝式複閉器,目前正用於礦井入口附近的電網,為電動運輸卡車提供支援。

在中東和非洲地區,隨著沙烏地阿拉伯電力公司為其NEOM和紅海可再生能源專案訂購5000至7000套真空開關設備,以及杜拜水電局(DEWA)在其穆罕默德·本·拉希德·阿勒馬克圖姆太陽能發電廠安裝自動複閉器,市場預計將會擴張。南非電力公司(Eskom)積壓了2萬套老舊設備,這可能成為潛在的替換需求來源,取決於財政改革的進展。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電力系統現代化專案和輸配電自動化領域的投資激增。

- 加速中壓可再生能源併網。

- 基於IEEE 1366(北美)的SAIDI/SAIFI可靠性要求

- 透過人工智慧驅動的預測性維護降低資產全生命週期總成本。

- 微電網在孤立系統和偏遠地區的部署正在迅速擴大。

- 市場限制因素

- 對老舊液壓車輛進行資本密集改造

- 公共產業認證週期過長以及未處理的類型測試案例積壓。

- 基於IEC 61850的複閉器控制中的網路安全合規成本

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 透過中斷介質

- 油絕緣

- 真空

- 無氣體/SF6固體

- 按階段

- 單相

- 三相

- 三單

- 控制方法

- 油壓

- 電的

- 微處理器/簡易爆炸裝置

- 電壓等級

- 15千伏或以下

- 16~27 kV

- 28~38 kV

- 按安裝位置

- 電線杆架空型

- 基座安裝式式

- 地下盒子

- 最終用戶

- 公用事業(電力傳輸和分配)

- 工業(製造業、採礦業、石油和天然氣業)

- 適用於商業和機構用途

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- ABB Ltd

- Eaton Corporation plc

- Siemens Energy AG

- Schneider Electric SE

- Hubbell Power Systems

- S&C Electric Company

- NOJA Power Switchgear

- G&W Electric Company

- Tavrida Electric

- GE Grid Solutions

- Schweitzer Engineering Laboratories(SEL)

- Arteche Group

- ERMCO Inc.

- Ningbo Tianan(Group)Co.

- Zhejiang Zhegui Electric

- CG Power & Industrial Solutions

- Myers Power Products

- Brush Group

- Mitsubishi Electric Power Products

- Powell Industries

第7章 市場機會與未來展望

According to Mordor Intelligence, the recloser market size is projected to expand from USD 1.31 billion in 2025 and USD 1.39 billion in 2026 to USD 1.82 billion by 2031, registering a CAGR of 5.59% between 2026 to 2031.

This report is Segmented by Interruption Medium (Oil-Insulated, and More), Phase (Single-Phase, and More), Control Type (Hydraulic, and More), Voltage Class (Up To 15 KV, and More), Installation Location (Pole-Mounted, and More), End-User (Utilities, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Recloser Market Trends and Insights

Grid-Modernization Programs and T&D Automation Spending Surge

Utilities allocated USD 480 billion to grid upgrades in 2025 and plan to invest USD 5.8 trillion through 2035, funneling roughly one-third toward distribution automation that includes high-speed reclosers . Eversource earmarked USD 16.2 billion of its 2025-2029 capital plan for smart-grid overlays across New England circuits serving 1.4 million customers . China State Grid is funding 137,500 circuit-kilometers of feeders in western provinces, creating landmark orders for vacuum units rated at 27 kV and 38 kV. Alberta's 20-year USD 5.1 billion blueprint dedicates two-thirds of spending to renewable-driven feeder automation, while the U.S. GRIP program has awarded USD 7.6 billion to wildfire-hardening projects that specify pad-mounted reclosers in coastal flood zones.

Accelerated Renewable Energy Interconnections at Medium-Voltage Levels

Interconnection queues held 2,600 GW of solar, wind, and storage in early 2026, stretching median wait times beyond 36 months and pushing utilities to adopt IEEE 1547-2018-compliant reclosers able to manage bidirectional flows. India's 450 GW renewables target demands USD 21 billion in transmission upgrades, much at 33 kV and 11 kV, where reclosers form the first protection layer. Duke Energy Florida cites 17 GW of queued data-center load that now dictates accelerated deployment of intelligent reclosers across 24 kV loops. ASEAN nations face USD 300 billion in grid investment by 2040 to support cross-border power trade, reinforcing sustained demand for 15-38 kV devices. Massachusetts utilities cut fault-restoration times 60% in 2025 by pairing reclosers with ADMS software that reroutes power within 30 seconds.

Capital-Intensive Retrofit of Legacy Hydraulic Fleets

Hydraulic devices need oil changes every 3-5 years and cost USD 600-1,000 per repair, yet new vacuum units range USD 15,000-40,000, stretching payback to a decade. Eaton's Form 7 retrofit kit slashes install cost 40% by re-using the pole structure, but European projects bear extra USD 2,000-5,000 PCB disposal fees that extend timelines . ABB's battery-free Eagle single-phase model targets one-to-one hydraulic swaps and encrypts Wi-Fi commissioning traffic for field crews.

Other drivers and restraints analyzed in the detailed report include:

- Reliability Mandates Under IEEE 1366 SAIDI/SAIFI Tightening (North America)

- AI-Enabled Predictive Maintenance Lowering Total Asset Lifecycle Cost

- Lengthy Utility Qualification Cycles and Type-Test Backlogs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vacuum interrupters dominated growth with an 8.0% CAGR, while gas and SF6-free solids retained the largest 60.3% 2025 recloser market share. The recloser market size for vacuum technology is set to expand rapidly as utilities in Europe replace banned SF6 equipment starting January 2026.

Utilities that migrated to vacuum report maintenance savings because the design delivers 10,000 operations without gas top-ups. ABB's SafePlus Air and Schneider's GM AirSeT illustrate retrofits that fit existing footprints, easing regulatory approval. Oil-filled units persist in arctic and seismic vaults, but new hermetic vacuum bottles rated -50 °C are narrowing that niche.

Three-phase devices held 48.9% of the 2025 recloser market share, yet triple-single models will outpace at a 6.5% CAGR through 2031. Rural circuits carrying irrigation and oil-field loads gain 30-40% fewer customer interruptions when only the faulted phase is opened.

Hubbell's LineDefender and ABB's Eagle demonstrate visible fault indication and self-powered operation that linemen can install without cranes. As micro-processor logic synchronizes independent poles, utilities foresee triple-single adoption even on 27 kV backbone laterals to optimize DER hosting capacity.

Geography Analysis

Asia-Pacific secured 42.8% of 2025 revenue and is forecast to grow at 6.2% CAGR, buoyed by China's USD 574 billion distribution expansion and India's USD 93 billion substation program targeting 500 GW of non-fossil power. State Grid aims to wire 137,500 circuit-kilometers of new lines, most at 35 kV, directly lifting the regional recloser market. Pacific Islands funded 5 MW of mini-grids under the REnew Pacific scheme, validating single-phase units that enable seamless islanding during cyclones.

In North America, the U.S. GRIP program injects USD 7.6 billion into wildfire mitigation and undergrounding across 50 states. Eversource's USD 16.2 billion distribution plan and Canada's NRCan grants underscore stable utility spending. Data-center clusters in Virginia, Florida, and Texas are specifying 34.5 kV pad-mounted reclosers with IEC 61850 Edition 2.1 cybersecurity, pushing suppliers to add MACsec and role-based access control.

In Europe, the SF6 ban forces the retrofit of 50,000-70,000 medium-voltage devices. ABB shipped SafeRing Air switchgear to E.ON Germany ahead of the deadline, and Schneider invested USD 9.6 million in its Leeds plant for Ringmaster AirSeT production. Nordic DSOs such as Landsnet pioneered fully digital substations that integrate recloser PMUs over fiber, a blueprint spreading to the Baltics and Central Europe.

Growth in South America is driven by ANEEL-mandated loss reduction initiatives in Brazil and increased mining capital expenditure in Chile's Atacama region. Pad-mounted reclosers, designed for altitudes of up to 4,500 meters, are now being utilized in pit-rim networks to support electric haul trucks.

The Middle East and Africa will grow as Saudi Electricity Company orders 5,000-7,000 vacuum units for NEOM and Red Sea renewables, and DEWA deploys automated reclosers across the Mohammed bin Rashid Al Maktoum solar park. South Africa's Eskom backlog of 20,000 aging units remains a latent replacement pool, contingent on fiscal reform.

- ABB Ltd

- Eaton Corporation plc

- Siemens Energy AG

- Schneider Electric SE

- Hubbell Power Systems

- S&C Electric Company

- NOJA Power Switchgear

- G&W Electric Company

- Tavrida Electric

- GE Grid Solutions

- Schweitzer Engineering Laboratories (SEL)

- Arteche Group

- ERMCO Inc.

- Ningbo Tianan (Group) Co.

- Zhejiang Zhegui Electric

- CG Power & Industrial Solutions

- Myers Power Products

- Brush Group

- Mitsubishi Electric Power Products

- Powell Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Grid-modernization programs & T&D automation spending surge

- 4.2.2 Accelerated renewable energy interconnections at medium-voltage levels

- 4.2.3 Reliability mandates under IEEE 1366 SAIDI/SAIFI tightening (North America)

- 4.2.4 AI-enabled predictive maintenance lowering total asset lifecycle cost (under-the-radar)

- 4.2.5 Fast-rising micro-grid deployments in islanded & remote grids (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Capital-intensive retrofit of legacy hydraulic fleets

- 4.3.2 Lengthy utility qualification cycles & type-test backlogs

- 4.3.3 Cyber-security compliance costs for IEC 61850-based recloser controls (under-the-radar)

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Interruption Medium

- 5.1.1 Oil-insulated

- 5.1.2 Vacuum

- 5.1.3 Gas/SF6-free Solid

- 5.2 By Phase

- 5.2.1 Single-Phase

- 5.2.2 Three-Phase

- 5.2.3 Triple-Single

- 5.3 By Control Type

- 5.3.1 Hydraulic

- 5.3.2 Electric

- 5.3.3 Microprocessor/IED

- 5.4 By Voltage Class

- 5.4.1 Up to 15 kV

- 5.4.2 16 to 27 kV

- 5.4.3 28 to 38 kV

- 5.5 By Installation Location

- 5.5.1 Pole-Mounted Overhead

- 5.5.2 Pad-Mounted

- 5.5.3 Underground Vault

- 5.6 By End-User

- 5.6.1 Utilities (T&D)

- 5.6.2 Industrial (Manufacturing, Mining, Oil & Gas)

- 5.6.3 Commercial and Institutional

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 NORDIC Countries

- 5.7.2.6 Russia

- 5.7.2.7 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 ASEAN Countries

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Argentina

- 5.7.4.3 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 South Africa

- 5.7.5.4 Egypt

- 5.7.5.5 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 Eaton Corporation plc

- 6.4.3 Siemens Energy AG

- 6.4.4 Schneider Electric SE

- 6.4.5 Hubbell Power Systems

- 6.4.6 S&C Electric Company

- 6.4.7 NOJA Power Switchgear

- 6.4.8 G&W Electric Company

- 6.4.9 Tavrida Electric

- 6.4.10 GE Grid Solutions

- 6.4.11 Schweitzer Engineering Laboratories (SEL)

- 6.4.12 Arteche Group

- 6.4.13 ERMCO Inc.

- 6.4.14 Ningbo Tianan (Group) Co.

- 6.4.15 Zhejiang Zhegui Electric

- 6.4.16 CG Power & Industrial Solutions

- 6.4.17 Myers Power Products

- 6.4.18 Brush Group

- 6.4.19 Mitsubishi Electric Power Products

- 6.4.20 Powell Industries

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

重合閘市場機會、成長要素、產業趨勢分析及2026-2035年預測

重合閘市場機會、成長要素、產業趨勢分析及2026-2035年預測 重合閘市場:按相位、控制方式、應用和地區分類

重合閘市場:按相位、控制方式、應用和地區分類 全球重合器市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球重合器市場規模、佔有率、趨勢和成長分析報告(2026-2034) 重合閘市場:依機構類型、額定電壓、相數、最終用戶和應用分類-2026-2032年全球市場預測全球三相重合器市場規模、佔有率、趨勢和成長分析報告(2026-2034)桿式重合閘裝置市場:按類型、控制方式、額定電壓、隔離介質和最終用戶分類 - 全球預測 2026-2032

重合閘市場:依機構類型、額定電壓、相數、最終用戶和應用分類-2026-2032年全球市場預測全球三相重合器市場規模、佔有率、趨勢和成長分析報告(2026-2034)桿式重合閘裝置市場:按類型、控制方式、額定電壓、隔離介質和最終用戶分類 - 全球預測 2026-2032 全球複閉器市場:機會與策略展望(至2034年)

全球複閉器市場:機會與策略展望(至2034年) 重合閘市場規模、佔有率和成長分析(按重合閘類型、最終用戶、應用、安裝類型、控制機制和地區分類)-2026-2033年產業預測

重合閘市場規模、佔有率和成長分析(按重合閘類型、最終用戶、應用、安裝類型、控制機制和地區分類)-2026-2033年產業預測 複閉器市場 - 全球產業規模、佔有率、趨勢、機會與預測:階段類型、控制類型、額定電壓、分段器控制類型、區域和競爭格局,2021-2031年單相重合器市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)

複閉器市場 - 全球產業規模、佔有率、趨勢、機會與預測:階段類型、控制類型、額定電壓、分段器控制類型、區域和競爭格局,2021-2031年單相重合器市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)