|

市場調查報告書

商品編碼

2063249

中國豬飼料市場:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031年)China Swine Feed - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

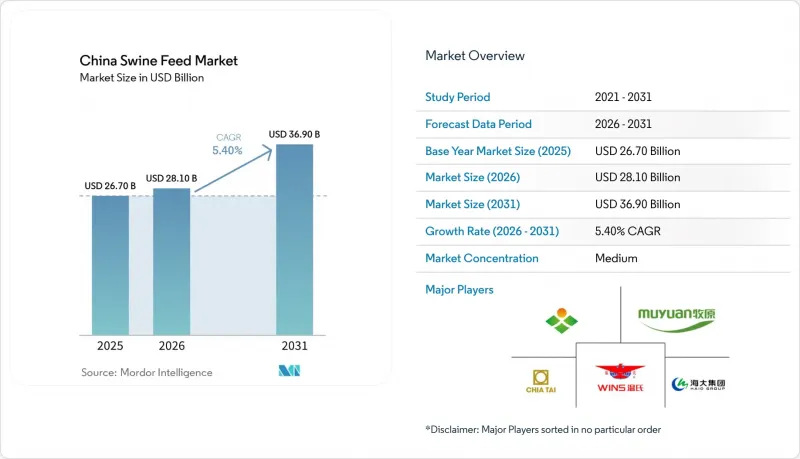

根據 Mordor Intelligence 預測,中國豬飼料市場規模將從 2025 年的 267 億美元成長到 2026 年的 281 億美元,到 2031 年將進一步成長到 369 億美元,2026 年至 2031 年的複合年成長率為 5.4%。

本報告按產品類型(幼畜飼料、育成雞飼料、育肥雞飼料、種雞飼料)、形態(顆粒狀、粉狀、碎粒狀)和原料類型(玉米、豆粕、氨基酸添加劑、維生素和礦物質、酵素以及其他穀物和油脂)進行細分。市場預測以美元計價。

中國豬飼料市場趨勢與洞察

大型養豬場的快速整合

大型養豬場的快速整合正將採購權轉移到垂直一體化的企業手中,這些企業直接與飼料供應商談判,並要求根據每個生長階段客製化飼料配方。牧源食品公司報告稱,截至2025年3月,其完全分攤的育種成本為每公斤12元人民幣(約1.65美元)。這種規模的營運使一體化企業能夠自建飼料廠,實施嚴格的生物安全措施,並將節省的成本再投資於營養研究,從而進一步拉大了大規模一體化企業與小規模農戶之間的差距。

非洲豬瘟疫情引發了對具備生物安全措施的商業飼料的需求激增。

為因應非洲豬瘟疫情,養豬戶正在加強生物安全措施,並轉向更安全的飼料來源。根據聯合國糧食及農業組織(糧農組織)預測,越南的非洲豬瘟病例數預計將從2024年的1,600多例激增至2025年的約2,495例,導致約127萬頭豬被撲殺。這一成長凸顯了傳統養殖系統中日益嚴重的污染風險。由於非洲豬瘟可透過飼料和農業投入品傳播,養豬戶正轉而使用來自生物安全設施的經熱處理認證的商業飼料。這種轉變推動了可追溯、符合HACCP標準的複合飼料產品的需求成長。

國內玉米價格波動

2026年2月,國內玉米價格為每公斤2.320元人民幣(約每公斤0.32美元),較2022年底的每公斤3元人民幣大幅下跌。這次價格暴跌凸顯了玉米市場的波動性,為生產者和貿易商都帶來了挑戰。價格波動導致期貨合約存在不確定性,生產者難以取得穩定的價格,也難以有效制定產業計畫。此外,價格不穩定可能導致生產者出於預防目的而減少庫存,進而可能降低飼料需求,進一步影響市場動態。

細分市場分析

2025年,生長飼料將佔中國豬飼料市場38%的最大佔有率。這是因為生長期(30至70公斤)是飼料採食量最高的時期,也是每頭豬複合飼料用量最高的時期。預計2026年至2031年,幼畜飼料市場將呈現最高的成長率,複合年成長率將達到5.9%。這一成長反映了該行業日益重視早期腸道健康計劃,旨在降低死亡率並縮短育肥期,從而應對養豬生產中的關鍵挑戰。育肥飼料將繼續注重成本效益以最佳化生產成本,而種豬飼料的供應則與母豬數量的趨勢密切相關。

生產者正致力於提高斷奶期營養管理的精準度,以最大限度地減少壓力反應,改善腸道健康,並提升生長性能。因此,易消化蛋白質、有機酸以及促進免疫力和飼料吸收的功能性成分的使用日益增多。對抗生素和氧化鋅使用的監管也進一步推動了先進合規型幼畜飼料解決方案的研發。此外,大型農場和合約養殖系統的擴張,以及旨在提高飼料轉換率和降低死亡率的綜合生產模式,也推動了對高品質幼畜飼料的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 大型養豬場的快速整合

- 非洲豬瘟疫情引發了對生物安全型商業飼料的需求激增。

- 政府指令減少豆粕用量

- 部署精準餵料物聯網平台

- 採用重組耐熱植酸酶

- 零售商的碳中和豬肉採購目標

- 市場限制因素

- 國內玉米價格波動

- 非洲豬瘟後重組豬群的延誤

- 加強對抗生素使用的限制

- 提高飼料中昆蟲來源和發酵蛋白質的比例

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 起始飼料

- 種植者的飼料

- 飼料

- 種畜飼料

- 按形式

- 顆粒

- 搗碎

- 崩潰

- 依成分類型

- 玉米

- 豆粉

- 胺基酸添加劑

- 維生素和礦物質

- 酵素(例如植酸酶)

- 其他穀物、油脂

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- New Hope Liuhe Co., Ltd.

- Chia Tai Investment Co., Ltd.(Charoen Pokphand Group)

- Wens Foodstuff Group Co., Ltd.

- Guangdong Haid Group Co., Ltd.

- Muyuan Foods Co., Ltd.

- Beijing Dabeinong Technology Group Co., Ltd.(DBN Group)

- Tongwei Co., Ltd.

- Liaoning Wellhope Agri-Tech Co., Ltd.

- Cargill, Incorporated

- Archer-Daniels-Midland Company

- DSM-Firmenich AG

- Evonik Industries AG

第7章 市場機會與未來展望

According to Mordor Intelligence, the china swine feed market size is projected to grow from USD 26.7 billion in 2025 to USD 28.1 billion in 2026, and further to USD 36.9 billion by 2031, with a CAGR of 5.4% from 2026 to 2031.

This report is Segmented by Product Type (Starter Feed, Grower Feed, Finisher Feed, Breeder Feed), by Form (Pellet, Mash, Crumbles), and by Ingredient Type (Corn, Soybean Meal, Amino-Acid Additives, Vitamins and Minerals, Enzymes, Other Cereals and Fats). The Market Forecasts are Provided in Terms of Value (USD).

China Swine Feed Market Trends and Insights

Rapid Consolidation of Large-Scale Pig Farms

The rapid consolidation of large-scale pig farms is shifting procurement power toward vertically integrated companies that negotiate directly with grain suppliers and require stage-specific feed rations. Muyuan Foods reported a fully allocated breeding cost of CNY 12 per kilogram (USD 1.65 per kilogram) in March 2025 . The scale of operations enables integrators to operate on-site feed mills, implement stringent biosecurity measures, and reinvest cost savings into nutrition research, further widening the gap between large integrators and smallholders.

African Swine Fever (ASF)-Triggered Surge in Biosecure Commercial Feed

In response to the African Swine Fever (ASF) outbreak, swine producers are tightening biosecurity measures and pivoting towards safer feed sourcing. The Food and Agriculture Organization reported a jump in ASF cases in Vietnam, rising from over 1,600 in 2024 to about 2,495 in 2025, leading to the culling of roughly 1.27 million pigs . This uptick underscores heightened contamination risks in conventional systems. Given that ASF can be transmitted via feed and farm inputs, producers are turning to heat-treated, certified commercial feed sourced from biosecure mills. This shift is propelling the demand for traceable, HACCP-compliant compound feed products.

Domestic Corn-Price Volatility

In February 2026, domestic corn was traded at 2.320 RMB per kilogram (USD 0.32 per kilogram), marking a significant decline from 3.000 RMB per kilogram in late 2022 . This sharp price drop highlights the volatility in the corn market, which poses challenges for producers and traders alike. Such fluctuations create uncertainty in forward contracting, making it difficult for producers to secure stable pricing and plan their operations effectively. Additionally, this price instability may prompt producers to reduce their inventory levels as a precautionary measure, potentially leading to a decline in feed demand and further impacting market dynamics.

Other drivers and restraints analyzed in the detailed report include:

- Swill-Feeding Ban Spurs Commercial Feed Uptake

- Roll-Out of Precision-Feeding IoT Platforms

- Slow Herd-Rebuilding Pace post ASF

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grower feed accounted for the largest 38% of the China swine feed market share in 2025, driven by the high feed consumption during the 30 to 70 kilogram growth phase, which requires the largest ration volume per animal. The starter feed market size is projected to register the fastest CAGR of 5.9% from 2026 to 2031. This growth reflects the industry's increasing focus on early-life gut-health programs designed to reduce mortality rates and shorten finishing periods, addressing key challenges in swine production. Finisher Feed remains focused on cost efficiency to optimize production expenses, while Breeder Feed volumes are closely tied to sow inventory trends.

Producers are focusing on nutritional precision during the weaning phase to minimize stress, improve gut health, and enhance growth performance. This has resulted in increased use of functional ingredients, including easily digestible proteins, organic acids, and feed additives that promote immunity and nutrient absorption. Regulatory restrictions on the use of antibiotics and zinc oxide are further driving the development of advanced, compliant starter feed solutions. Additionally, the expansion of large-scale farms and contract rearing systems is boosting the demand for high-quality starter feed, supported by integrated production models aimed at improving feed efficiency and reducing mortality rates.

List of Companies Covered in this Report:

- New Hope Liuhe Co., Ltd.

- Chia Tai Investment Co., Ltd. (Charoen Pokphand Group)

- Wens Foodstuff Group Co., Ltd.

- Guangdong Haid Group Co., Ltd.

- Muyuan Foods Co., Ltd.

- Beijing Dabeinong Technology Group Co., Ltd. (DBN Group)

- Tongwei Co., Ltd.

- Liaoning Wellhope Agri-Tech Co., Ltd.

- Cargill, Incorporated

- Archer-Daniels-Midland Company

- DSM-Firmenich AG

- Evonik Industries AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid consolidation of large-scale pig farms

- 4.2.2 African Swine Fever (ASF)-triggered surge in biosecure commercial feed

- 4.2.3 Government soybean-meal reduction mandate

- 4.2.4 Roll-out of precision-feeding IoT platforms

- 4.2.5 Adoption of recombinant thermostable phytase

- 4.2.6 Retailers carbon-neutral pork procurement targets

- 4.3 Market Restraints

- 4.3.1 Domestic corn-price volatility

- 4.3.2 Slow herd-rebuilding pace post-ASF

- 4.3.3 Stricter antibiotic-use regulations

- 4.3.4 Rising share of insect/fermented proteins in rations

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecast (Value)

- 5.1 By Product Type

- 5.1.1 Starter Feed

- 5.1.2 Grower Feed

- 5.1.3 Finisher Feed

- 5.1.4 Breeder Feed

- 5.2 By Form

- 5.2.1 Pellet

- 5.2.2 Mash

- 5.2.3 Crumbles

- 5.3 By Ingredient Type

- 5.3.1 Corn

- 5.3.2 Soybean Meal

- 5.3.3 Amino-Acid Additives

- 5.3.4 Vitamins and Minerals

- 5.3.5 Enzymes (e.g., Phytase)

- 5.3.6 Other Cereals and Fats

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 New Hope Liuhe Co., Ltd.

- 6.4.2 Chia Tai Investment Co., Ltd. (Charoen Pokphand Group)

- 6.4.3 Wens Foodstuff Group Co., Ltd.

- 6.4.4 Guangdong Haid Group Co., Ltd.

- 6.4.5 Muyuan Foods Co., Ltd.

- 6.4.6 Beijing Dabeinong Technology Group Co., Ltd. (DBN Group)

- 6.4.7 Tongwei Co., Ltd.

- 6.4.8 Liaoning Wellhope Agri-Tech Co., Ltd.

- 6.4.9 Cargill, Incorporated

- 6.4.10 Archer-Daniels-Midland Company

- 6.4.11 DSM-Firmenich AG

- 6.4.12 Evonik Industries AG