|

市場調查報告書

商品編碼

2063244

太陽能電池漿料:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Solar Cell Paste - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

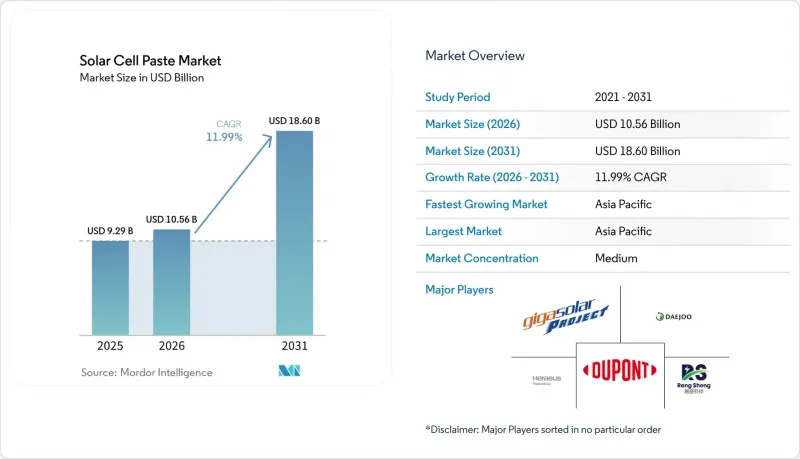

根據 Mordor Intelligence 預測,太陽能電池漿料的市場規模預計在 2025 年達到 92.9 億美元,在 2026 年達到 105.6 億美元,在 2031 年達到 186 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 11.99%。

本報告按類型(銀膠、鋁漿等)、應用(單晶矽電池、多晶矽電池、薄膜電池等)、最終用戶(住宅、商業/工業、公用事業規模、離網/微電網)和地區(北美、亞太、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球太陽能電池漿料市場趨勢與洞察

中國、印度和美國太陽能發電裝置容量的穩定成長正在推動對太陽能漿料的需求。

光是在中國,2024年至2025年間就將新增280吉瓦的電池產能,使累積產能超過800吉瓦。為攤銷固定成本,生產線運轉率的提高也導致了漿料消耗量的增加。印度24億美元的生產連結獎勵計畫計畫強制要求從國內採購漿料,促進了本地電池製造商與韓國供應商之間的合資企業。在美國,根據《通貨膨脹控制法案》(IRA)提供的45倍稅額扣抵,預計到2027年電池年產量將達到50吉瓦,而運作區域混合工廠的供應商已將漿料交貨週期縮短至30天。這種在基準需求。

快速向 PERC、TOPCon 和 HJT 電池的轉變,催生了對高性能焊膏的需求。

2025年底,拓普康(TOPCon)的季度產能成長將超過PERC,組件效率將超過24.5%。這證明了採用雙層金屬化和選擇性發射極結構的合理性,從而使正面漿料的接觸電阻低於1.5 mΩ*cm²,線寬低於25µm。 HJT電池需要低溫銀配方,可在200 度C以下燒結,以保護非晶質層。預計2026年底,REC Solar和華新(Huasun)的HJT總合將運作10GW。這些嚴格的規範將全球整體認證供應商的數量限制在10家以下,採購集中在賀利氏(Heraeus)、杜邦(DuPont)和兆輝(Giga Solar)等公司。隨著製造商的轉型,投資於流變控制和奈米銀分散技術的漿料供應商正在獲得溢價和長期契約,從而緩解銀價波動帶來的利潤壓力。

白銀價格波動增加了電池製造商的成本風險。

從2025年1月到2026年1月,白銀價格飆升76%,但隨後回落至2026年3月的每克2.65美元至2.90美元,導致通威、隆基和晶澳太陽能在2026年第一季因未對沖的白銀風險累計總合虧損11億美元。目前,漿料供應商提供與三個月期貨價格掛鉤的固定價格合約,這使得商品風險向上游轉移,並壓縮了供應商高達200個基點的毛利率。為了因應這個問題,從2023年到2025年,篩網的微型化將每片晶圓的平均白銀消耗量從110毫克降至92毫克。因此,價格波動將降低獲利的可預測性,並加速資源節約型技術的應用。

細分市場分析

銀膠因其高導電性和與PERC、TOPCon和HJT等多種太陽能電池的廣泛相容性,預計2025年將佔據太陽能電池漿料市場70.1%的佔有率。雖然這一細分市場的主導地位能夠保障短期利潤,但由於銀價波動和監管方面的阻力,其成長潛力有限。受歐盟REACH法規和中國GB/T 38597標準要求的推動,無鉛多金屬膏預計將達到14.1%的複合年成長率。 Sn-Ag-Cu混合材料雖然會使製造成本增加約10%,但可以消除合規風險。鋁漿料對於公用事業規模項目中的Al-BSF電池仍然十分重要,但隨著TOPCon的日益普及,其市場佔有率正在萎縮。如果能夠解決黏著性和遷移性問題,銅漿料和銀包銅漿料將具有很高的成長潛力。

供應商正在相應地調整產品系列。賀利氏和杜邦利用20-25%的價格溢價,將研發重點放在用於異質結變壓器(HJT)的低溫奈米銀分散液上。中國競爭對手如兆光科技則加大對鋁漿和傳統銀膠的投資,瞄準對價格敏感的吉瓦級太陽能電站。在日益嚴格的歐洲監管環境下,儘早獲得無鉛混合物的認證能夠帶來先發優勢,而銀包銅漿的先導計畫則可作為應對未來成本衝擊的替代方案。因此,競爭優勢在於同時投資於高效且成本最佳化的配方,而與燒結助劑和潤濕劑相關的智慧財產權則構成關鍵的競爭優勢。

區域分析

預計到2025年,亞太地區將佔據太陽能電池漿料市場62.7%的佔有率,並在2031年之前以13.4%的複合年成長率成長。這主要得益於中國計畫在2030年新增500吉瓦太陽能發電裝置容量,以及印度「國家太陽能計畫」的目標是280吉瓦。江蘇、浙江和安徽三省的電池產能佔全球總產能的60%以上,因此對漿料的需求高度集中,並具有規模經濟效益。印度的國內採購義務(DCR)已促成大州電子材料公司(Daejoo Electronic Materials)與吉加太陽能公司(Giga Solar)在古吉拉突邦和泰米爾納德邦成立合資企業,將物流交貨前置作業時間從90天縮短至30天。韓國和日本雖然產量較小,但憑藉其在半導體材料領域的深厚專業知識,在低溫異質結電晶體(HJT)漿料的創新方面處於領先地位。

預計到2028年,北美市場佔有率將快速成長。根據《通貨膨脹控制法案》(IRA)提供的稅額扣抵,美國電池產能預計將從2023年的8吉瓦增至2027年的50吉瓦,從而帶動當地對電解漿的需求相應成長。杜邦公司位於北卡羅來納州的生產線和賀利氏公司位於俄亥俄州的技術中心在這一復甦的市場中展現了其先鋒優勢。歐洲在REPowerEU計畫下,目標是每年新增30吉瓦產能,但目前面臨產能短缺的問題。因此,當地電解漿的消費量取決於歐盟內部電池計畫的成功,這些計畫主要由邁耶-伯格公司和義大利國家電力公司綠色能源公司主導。儘管如此,監管機構對無鉛配方的推動,正促使歐洲工廠率先採用錫銀銅(Sn-Ag-Cu)配方。

中東和非洲是新興的成長區域。沙烏地阿拉伯的「2030願景」目標是實現20吉瓦的太陽能發電裝置容量,為此,賀利氏計畫於2026年在利雅德開設服務基地。隨著阿拉伯聯合大公國5吉瓦的阿達夫拉太陽能發電廠的投產以及南非的採購,預計該地區的漿料進口量將會增加,儘管南非的國內生產仍處於起步階段。以巴西和智利為首的南美洲,其大部分太陽能電池嚴重依賴進口,但更嚴格的在地採購法規可能會在未來加速混合設施的建設。儘管這些地區共同促進了收入來源的多元化,但亞太地區仍將是太陽能電池漿料市場的基石,至少到2031年為止。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 中國、印度和美國太陽能發電設施的穩定擴張正在推動對太陽能漿料的需求。

- 快速過渡到 PERC、TOPCon 和 HJT 電池需要高性能雙面漿料。

- IRA、REPowerEU 和類似的在地化舉措正在推動亞洲以外地區新的糊狀物生產線的推出。

- 降低成本的競爭正在推動銀包銅和低溫焊膏的普及。

- 鈣鈦礦串聯系統的研究與開發正在蓬勃發展,對網版印刷導電油墨的需求也不斷成長。

- 市場限制因素

- 白銀價格波動增加了電池製造商的成本風險。

- 銀的節約和銅電鍍的加速發展正在威脅對銀漿的需求。

- 對含鉛玻璃料的更嚴格監管增加了配方變更的成本。

- 由於供應商高度集中,買方的議價能力有限。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 銀膠

- 鋁膏

- 銅膏

- 鍍銀銅漿

- 無鉛多金屬膏

- 透過使用

- 單晶胞

- 多晶矽電池

- 薄膜電池

- 雜合子(HJT)細胞

- 鈣鈦礦和串聯電池

- 最終用戶

- 住宅

- 商業和工業

- 公用事業規模

- 離網/微電網

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Heraeus Photovoltaics

- DuPont Microcircuit Materials

- Giga Solar Materials

- Rutech

- Daejoo Electronic Materials

- Samsung SDI

- Alpha Assembly(MacDermid Alpha)

- Dongjin Semichem

- InkTec

- Toyo Aluminium KK

- Monocrystal

- Ferro Corporation

- Targray

- Henkel AG & Co. KGaA

- Heraeus Noblelight(infra-red sintering)

- Pastetech GmbH

- Xi'an Hongxing Electronic Paste

- Jiangsu Hoyi Technology

- Hunan LEED Advanced Material

- Heraeus ShenZhen(local JV)

第7章 市場機會與未來展望

According to Mordor Intelligence, the solar cell paste market size is projected to be USD 9.29 billion in 2025, USD 10.56 billion in 2026, and reach USD 18.60 billion by 2031, growing at a CAGR of 11.99% from 2026 to 2031.

This report is Segmented by Type (Silver Paste, Aluminum Paste, and More), Application (Monocrystalline Cells, Polycrystalline Cells, Thin-Film Cells, and More), End-User (Residential, Commercial and Industrial, Utility-Scale, and Off-Grid/Micro-grid) and Geography (North America, Asia-Pacific, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Solar Cell Paste Market Trends and Insights

Relentless PV Capacity Additions in China, India & US Boosting Paste Demand

China alone added 280 GW of new cell capacity during 2024-2025, pushing cumulative capability beyond 800 GW and lifting past consumption as lines run at higher utilization to amortize fixed costs. India's USD 2.4 billion Production-Linked Incentive mandates domestic paste sourcing, catalyzing joint ventures between local cell makers and Korean suppliers. In the United States, the IRA's 45X credit is underwriting a projected climb to 50 GW of annual cell output by 2027, trimming lead times for paste deliveries to 30 days as suppliers commission regional blending plants. Regionalization reduces working capital tied up in inventory by up to 20%, freeing cash for further process upgrades. The driver's impact stays pronounced through 2028, underpinning baseline demand even as per-watt paste loadings decline.

Rapid Shift to PERC, TOPCon & HJT Cells Requiring Higher-Performance Pastes

TOPCon overtook PERC in quarterly capacity additions by late 2025, delivering module efficiencies above 24.5% that justify dual-layer metallization and selective-emitter architectures, which in turn require front-side pastes that achieve contact resistivity under 1.5 mΩ*cm2 and line widths under 25 µm. HJT cells demand low-temperature silver formulations that fire below 200 °C to preserve amorphous-silicon layers; REC Solar and Huasun expect 10 GW of combined HJT capacity online by end-2026. These tighter specs limit qualified suppliers to fewer than 10 globally, consolidating purchasing around Heraeus, DuPont, and Giga Solar. As manufacturers pivot, paste vendors investing in rheology control and nano-silver dispersion secure premium pricing and longer-term contracts, cushioning margin pressure from silver volatility.

Silver Price Volatility Enlarging Cost Risk for Cell Makers

Silver rallied 76% from January 2025 to January 2026, then retraced to USD 2.65-2.90 per g by March 2026, forcing Tongwei, LONGi, and JA Solar to book USD 1.1 billion in combined Q1 2026 losses tied to unhedged silver exposure. Paste suppliers now offer fixed-price contracts indexed to three-month forwards, but these shift commodity risk upstream, compressing supplier gross margins by up to 200 bps. To cope, average silver consumption dropped from 110 mg to 92 mg per wafer between 2023 and 2025 through finer screen meshes. Volatility, therefore, reduces revenue predictability and accelerates the uptake of thrifting technologies.

Other drivers and restraints analyzed in the detailed report include:

- IRA, REPowerEU & Localization Schemes Spurring New Paste Lines Outside Asia

- Cost-Down Race Driving Silver-Coated-Copper & Low-Temp Pastes Uptake

- Accelerated Silver-Thrifting & Copper Plating Threaten Paste Volumes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silver Paste captured 70.1% of the solar cell paste market share in 2025, underpinned by its high conductivity and broad qualification across PERC, TOPCon, and HJT. The segment's dominance shields near-term revenues, yet silver volatility and regulatory headwinds limit upside. Lead-Free Multi-Metal Paste is forecast to post a 14.1% CAGR, benefiting from EU REACH and China's GB/T 38597 mandates; Sn-Ag-Cu blends add roughly 10% to production cost but remove compliance risk. Aluminum Paste remains relevant for Al-BSF cells in utility-scale projects, though share erodes as TOPCon spreads. Copper and silver-coated copper pastes present high upside if adhesion and migration challenges are solved.

Suppliers are aligning portfolios accordingly. Heraeus and DuPont funnel R&D into low-temperature nano-silver dispersions for HJT, leveraging 20-25% price premiums. Chinese contenders like Giga Solar double down on aluminum and conventional silver pastes aimed at price-sensitive gigawatt farms. Early certification of lead-free blends offers first-mover advantage in Europe's tightening policy environment, while silver-coated-copper pilots act as an option on future cost shocks. Competitive positioning, therefore, hinges on parallel bets across premium-efficiency and cost-optimized formulations, with IP around sintering additives and wetting agents forming key moats.

Geography Analysis

Asia-Pacific controlled 62.7% of the solar cell paste market share in 2025 and is expanding at a 13.4% CAGR to 2031, fueled by China's plan for 500 GW of additional PV by 2030 and India's National Solar Mission target of 280 GW. Jiangsu, Zhejiang, and Anhui house over 60% of global cell capacity, concentrating paste demand and enabling economies of scale. India's domestic-content rules have already lured Daejoo Electronic Materials and Giga Solar into Gujarat and Tamil Nadu joint ventures, trimming logistics lead times from 90 days to 30 days. South Korea and Japan, though smaller in volume, drive innovation in low-temperature HJT pastes, supported by extensive semiconductor materials expertise.

North America's share is set to rise rapidly through 2028 as the IRA's 45X credit propels U.S. cell capacity from 8 GW in 2023 to a forecast 50 GW by 2027, bringing with it localized paste demand. DuPont's North Carolina line and Heraeus's Ohio tech center illustrate first-mover capture of this resurgent market. Europe, targeting 30 GW per annum under REPowerEU, faces a manufacturing gap; local paste consumption therefore hinges on the success of intra-EU cell projects led by Meyer Burger and Enel Green Power. Still, the regulatory push for lead-free formulations positions European plants at the forefront of Sn-Ag-Cu adoption.

The Middle East and Africa are emerging growth zones. Saudi Arabia's Vision 2030 aims for 20 GW of solar, prompting Heraeus to open a Riyadh service hub in 2026. The UAE's 5 GW Al Dhafra farm and South Africa's procurement rounds will lift regional paste imports, though domestic manufacturing remains nascent. South America, led by Brazil and Chile, imports most cells but could catalyze future blending facilities if local content rules tighten. Collectively, these geographies diversify revenue streams, but Asia-Pacific will remain the anchor of the solar cell paste market through at least 2031.

- Heraeus Photovoltaics

- DuPont Microcircuit Materials

- Giga Solar Materials

- Rutech

- Daejoo Electronic Materials

- Samsung SDI

- Alpha Assembly (MacDermid Alpha)

- Dongjin Semichem

- InkTec

- Toyo Aluminium K.K.

- Monocrystal

- Ferro Corporation

- Targray

- Henkel AG & Co. KGaA

- Heraeus Noblelight (infra-red sintering)

- Pastetech GmbH

- Xi'an Hongxing Electronic Paste

- Jiangsu Hoyi Technology

- Hunan LEED Advanced Material

- Heraeus ShenZhen (local JV)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Relentless PV capacity additions in China, India & US boosting paste demand

- 4.2.2 Rapid shift to PERC, TOPCon & HJT cells that require higher-performance front & rear pastes

- 4.2.3 IRA, REPowerEU & similar localisation schemes spurring new paste lines outside Asia

- 4.2.4 Cost-down race driving silver-coated-copper & low-temp pastes uptake

- 4.2.5 Surge in perovskite-tandem R&D demanding screen-printable conductive inks

- 4.3 Market Restraints

- 4.3.1 Silver price volatility enlarging cost risk for cell makers

- 4.3.2 Accelerated silver-thrifting & copper plating threaten paste volumes

- 4.3.3 Tighter lead-based frit regulations raising reformulation costs

- 4.3.4 High supplier concentration limits buyers' bargaining power

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Silver Paste

- 5.1.2 Aluminum Paste

- 5.1.3 Copper Paste

- 5.1.4 Silver-Coated-Copper Paste

- 5.1.5 Lead-Free Multi-Metal Paste

- 5.2 By Application

- 5.2.1 Monocrystalline Cells

- 5.2.2 Polycrystalline Cells

- 5.2.3 Thin-Film Cells

- 5.2.4 Heterojunction (HJT) Cells

- 5.2.5 Perovskite and Tandem Cells

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial and Industrial

- 5.3.3 Utility-Scale

- 5.3.4 Off-Grid/Micro-grid

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Heraeus Photovoltaics

- 6.4.2 DuPont Microcircuit Materials

- 6.4.3 Giga Solar Materials

- 6.4.4 Rutech

- 6.4.5 Daejoo Electronic Materials

- 6.4.6 Samsung SDI

- 6.4.7 Alpha Assembly (MacDermid Alpha)

- 6.4.8 Dongjin Semichem

- 6.4.9 InkTec

- 6.4.10 Toyo Aluminium K.K.

- 6.4.11 Monocrystal

- 6.4.12 Ferro Corporation

- 6.4.13 Targray

- 6.4.14 Henkel AG & Co. KGaA

- 6.4.15 Heraeus Noblelight (infra-red sintering)

- 6.4.16 Pastetech GmbH

- 6.4.17 Xi'an Hongxing Electronic Paste

- 6.4.18 Jiangsu Hoyi Technology

- 6.4.19 Hunan LEED Advanced Material

- 6.4.20 Heraeus ShenZhen (local JV)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

2026-2030年全球晶圓廠自動化市場

2026-2030年全球晶圓廠自動化市場 熔融石英鏡市場報告:趨勢、預測及競爭分析(至2035年)

熔融石英鏡市場報告:趨勢、預測及競爭分析(至2035年) 筆記型電腦組裝材料市場預測至2034年-按材料類型、應用和地區分類的全球分析

筆記型電腦組裝材料市場預測至2034年-按材料類型、應用和地區分類的全球分析 仿生半導體塗層市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、製程、最終用戶、功能、安裝類型、解決方案分類全球透明導電材料市場:預測(至2034年)-按材料類型、應用、最終用戶、技術和地區分類的分析

仿生半導體塗層市場分析及預測(至2035年):依類型、產品類型、技術、應用、材料類型、製程、最終用戶、功能、安裝類型、解決方案分類全球透明導電材料市場:預測(至2034年)-按材料類型、應用、最終用戶、技術和地區分類的分析 光伏漿料市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、應用、最終用戶、地區及競爭格局分類,2021-2031年)

光伏漿料市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、應用、最終用戶、地區及競爭格局分類,2021-2031年) FPD光阻劑市場按類型、抗蝕劑技術、銷售管道、應用和最終用途分類-2026-2032年全球預測半導體光阻劑市場:按光阻劑化學成分、光阻劑色調、裝置類型、應用領域和最終用途產業分類-2026-2032年全球市場預測半導體封裝用聚醯亞胺膠帶市場:按產品類型、黏合劑類型、厚度、應用和最終用戶分類的全球預測(2026-2032年)按類型、形態、工具、應用和最終用戶分類的CMP後清洗化學品市場—2026-2032年全球預測

FPD光阻劑市場按類型、抗蝕劑技術、銷售管道、應用和最終用途分類-2026-2032年全球預測半導體光阻劑市場:按光阻劑化學成分、光阻劑色調、裝置類型、應用領域和最終用途產業分類-2026-2032年全球市場預測半導體封裝用聚醯亞胺膠帶市場:按產品類型、黏合劑類型、厚度、應用和最終用戶分類的全球預測(2026-2032年)按類型、形態、工具、應用和最終用戶分類的CMP後清洗化學品市場—2026-2032年全球預測