|

市場調查報告書

商品編碼

2063238

Riser:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)Risers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

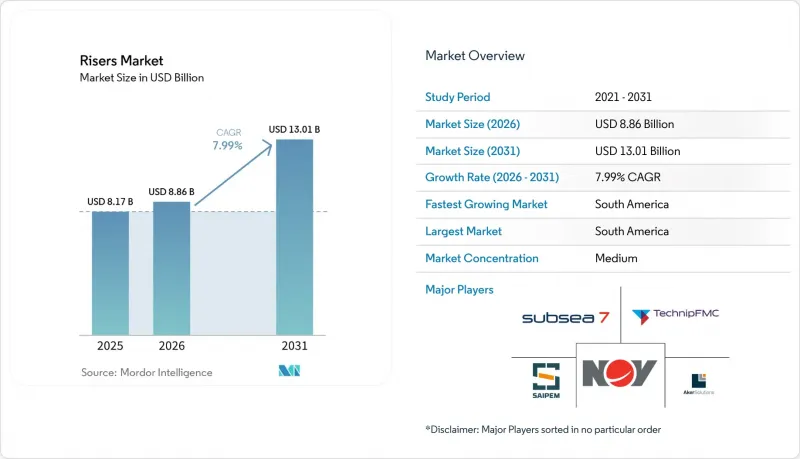

據 Mordor Intelligence 稱,2025 年立管市場價值為 81.7 億美元,預計到 2031 年將達到 130.1 億美元,而 2026 年為 88.6 億美元,預測期(2026-2031 年)的複合年成長率為 7.99%。

本報告按類型(軟性立管、剛性立管、混合立管)、材質(鋼、複合材料、熱塑性複合管、其他)、安裝深度(淺海、深海、超深海)、應用(鑽井、生產、修井、其他)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球立管市場趨勢及洞察

重啟深海和超深海計畫的最終投資決定(FID)

埃克森美孚已批准向圭亞那的「錘頭計畫投資68億美元,該計畫於2029年投產。本工程將採用比淺水標準長30%至40%的立管。同時,巴西石油公司(Petrobras)已批准SEAP II項目,該項目將使鹽層下油田的日產能增加12萬桶。這將需要24根鋼製懸索立管,以適應2200公尺的深度。到2028年,巴西和圭亞那的大規模最終投資決定(FID)將佔已批准深海油田產量的60%,這有利於擁有當地造船廠的綜合性海上油氣承包商。由於這些開發項目在鋼材價格穩定的情況下儘早簽署了EPC契約,因此不受近期金屬材料成本波動的影響,從而為立管市場需求提供了數年的支撐。

巴西和圭亞那衝浪套餐訂單激增

Subsea 7公司訂單了價值14億美元的Buzios 11項目,該項目包括18條軟性立管;而Technip FMC公司則獲得了價值2.5億至5億美元的錘頭項目,該項目結合了剛性立管供應和供應連系管。目前,SURF(海底管道、固定式管道和軟性管網)專案的平均合約價值超過8億美元。這是因為營運商將供應、安裝和健康管理服務整合到一個競標中,從而轉移了性能風險並縮短了製造前置作業時間。巴西石油公司(Petrobras)強制要求其專案60%的在地採購,這使得在巴西擁有製造能力的承包商獲得了競爭優勢,同時也為海外專業製造商設置了准入壁壘。

原油價格波動會影響外國投資決定(FID)的時間。

國際能源總署(IEA)預測,2026年全球原油供應將出現每日150萬至250萬桶的過剩,可能導致布蘭特原油價格跌破每桶70美元。巴西和圭亞那的深水項目受影響較小,因為它們的損益平衡點在每桶28至35美元之間,但西獲利能力較低的項目則面臨6至12個月的延期,導致立管市場短期訂單減少。

細分市場分析

預計剛性立管設計將在立管市場中呈現最高的成長率,複合年成長率將達到 8.7%。這是因為營運商正在縮短工程週期,並透過複製成熟的模板來實現批量採購。殼牌公司在墨西哥灣的棕地專案實現了三個油田設備 95% 的通用,從而減少了 40% 的前期工程工作。軟性立管憑藉其卓越的動態追蹤能力,預計到 2025 年仍將佔據 45.3% 的市場佔有率。 Technip FMC 的「錘頭」專案訂單訂單了電加熱軟性管線來防止蠟沉積。混合型立管目前仍處於小眾市場,但在頂部張力超過 1000 噸的超深水應用中至關重要,它將固定在海底的剛性段與抗疲勞複合複合材料頂部管柱相結合。向標準化剛性系統的轉變提高了採購計畫的確定性,並使擁有大容量管段的承包商獲得了更大的市場佔有率。

產業的模組化也促進了售後市場收入的成長。目錄化設計簡化了備件庫存管理,並最佳化了檢驗流程,從而降低了整體擁有成本。然而,在複雜的回接和延壽專案中,軟性管線仍然至關重要,因為現有基礎設施需要蜿蜒的管道路徑。隨著碳纖維拉伸增強材料最終通過認證,複合材料和鋼製產品預計將得到更廣泛的應用。這將減輕重量,拓寬立管市場可用的容器範圍,並縮短安裝時間。

複合材料替代品正以9.1%的複合年成長率快速成長,到2025年,它們將蠶食鋼管在立管市場69.5%的佔有率。 Strom公司的熱塑性管線已不再侷限於注水應用,預計2027年與巴西石油公司(Petrobras)合作,實現全面量產。 Magma World公司則瞄準西非高溫油井,這些油井的鋼管需要高成本的主動冷卻。現場數據顯示,複合材料管道重量減輕了77.7%,而抗張強度保持不變,這使得複合材料成為捲筒鋪設作業的理想選擇,因為鋼管無法承受甲板負載。

DNV對非金屬立管永久使用的批准掃清了最後一個障礙:監管批准。整合在層壓板中的光纖感測技術使每根複合材料立管都具備自我監測功能,無需外部測量儀器。然而,在壓力超過15,000 psi的超高壓酸性環境中,鋼材仍具有優勢,因為聚合物基體的氫脆問題仍然令人擔憂。儘管捲筒式船舶的供不應求和高昂的初始材料成本正在減緩複合材料的普及,但就生命週期成本而言,複合材料仍然具有吸引力,預計在預測期內,其在立管市場的佔有率將逐步成長。

區域分析

預計到2025年,南美洲將佔全球需求的35.7%,複合年成長率達8.4%,是所有地區中成長最快的。光是巴西石油公司(Petrobras)的SEAP II計畫就需要24根耐壓10,000磅/平方英吋(psi)的立管,而埃克森美孚公司在圭亞那的錘頭開發計畫預計到2029年將新增6根生產立管。在巴西,簡化的許可程序已將核准週期縮短至12個月;在圭亞那,一項300億美元的投資計畫預計將在2028年前新增40多根立管。立管市場受益於可預測的在地採購規則,這些規則有利於區域製造並縮短物流鏈。

在北美,重點在於最佳化現有設施。由於殼牌的凱基亞斯泛光項目以及墨西哥灣的多個維修項目,對服務的需求依然旺盛,而美國海洋能源管理局(BOEM)儲量製度的變更則加重了初始成本的負擔。在歐洲,以超級營運商為核心的北海一體化進程正在推進。殼牌和Equinor的Adura Venture公司在統一的監管計劃下管理相當於每日14萬桶原油的產量,該計劃充分利用了規模經濟。英國將於2026年生效的碳捕獲法規將強制要求對新的開發項目進行可行性研究,未來的最終投資決策(FID)將與綜合捕碳封存(CCS)理念掛鉤。

中東和亞太地區正在崛起為第二大樞紐。阿布達比國家石油公司(ADNOC)的SARB深層天然氣項目和Nasr-115擴建項目正在引入耐腐蝕合金立管用於酸性天然氣生產,而中海油(CNOOC)正在擴大其在南海的業務,並在開平18-1井採用剛性立管。東南亞由於價格不確定性和資金籌措而落後,但馬來西亞和印尼仍在持續做出穩定貢獻。這些發展將使收入的地域構成更加多元化,從而保護全球立管市場免受單一盆地衝擊的影響。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 恢復深海和超深海項目的最終投資決定(FID)。

- 巴西和圭亞那的SURF包裹訂單激增。

- 延長老舊淺水立管使用壽命的需求

- 熱塑性複合管(TCP)立管的快速普及

- 海上立管基礎設施碳捕獲與封存(CCS)維修的機會

- 人工智慧驅動的數位雙胞胎用於立管健康預測

- 市場限制因素

- 原油價格波動對最終投資決定時間的影響

- HSE和環境合規成本不斷上升

- 深海疲勞分析專家短缺

- 鍛造和冶金供應鏈交貨前置作業時間過長造成的瓶頸

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 軟性立管

- 剛性立管

- 混合升降台

- 材料

- 鋼

- 複合材料

- 熱塑性複合管

- 其他

- 按介紹的深度

- 淺水區(水深500公尺或以下)

- 深海(500-1500公尺)

- 超深海(深度1500公尺或以上)

- 透過使用

- 挖掘

- 生產

- 鍛鍊

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- TechnipFMC

- Aker Solutions

- Subsea 7

- NOV Inc.

- Saipem

- Baker Hughes(OneSubsea)

- McDermott International

- Oceaneering International

- Vallourec

- Oil States Industries

- Prysmian Group

- Airborne Oil & Gas

- Shawcor

- Trelleborg Offshore

- Ocyan

- MODEC

- Kongsberg Maritime

- DeepOcean

- Sapura Energy

- Bourbon Offshore

第7章 市場機會與未來展望

According to Mordor Intelligence, the risers market size was valued at USD 8.17 billion in 2025 and is estimated to grow from USD 8.86 billion in 2026 to reach USD 13.01 billion by 2031, at a CAGR of 7.99% during the forecast period (2026-2031).

This report is Segmented by Type (Flexible Risers, Rigid Risers, Hybrid Risers), Material (Steel, Composite, Thermoplastic Composite Pipe, Others), Deployment Depth (Shallow Water, Deepwater, Ultra-Deepwater), Application (Drilling, Production, Workover, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Risers Market Trends and Insights

Revival of Deep and Ultra-Deepwater Project FIDs

ExxonMobil sanctioned USD 6.8 billion for Hammerhead in Guyana, with start-up set for 2029 and riser lengths 30%-40% above shallow-water norms, while Petrobras approved SEAP II, adding 120,000 barrels per day of pre-salt capacity that requires 24 steel catenary risers rated for 2,200-meter depths . The clustering of large-scale FIDs in Brazil and Guyana, which together hold 60% of sanctioned deepwater barrels to 2028, benefits integrated SURF contractors owning local yards. Early locking of EPC contracts at stable steel prices has insulated these developments from recent metallurgy cost swings, anchoring a multiyear floor under risers market demand.

Surge in SURF Package Awards in Brazil and Guyana

Subsea7 won a USD 1.4 billion Buzios 11 award covering 18 flexible risers, whereas TechnipFMC secured a USD 250-500 million Hammerhead scope that bundles rigid-riser supply with umbilicals. Average SURF packages now exceed USD 800 million because operators consolidate supply, installation, and integrity services under single tenders, transferring performance risk and compressing fabrication lead times. Mandatory 60% local sourcing on Petrobras projects drives competitive advantage toward contractors with Brazilian fabrication capacity, creating barriers for foreign pure-play fabricators.

Crude-Oil Price Volatility Impacting FID Timing

The International Energy Agency foresees a 1.5-2.5 million-barrel-per-day supply surplus in 2026, which could pressure Brent below USD 70 per barrel . Deepwater projects in Brazil and Guyana remain insulated with breakevens at USD 28-35, but marginal West African prospects face deferrals of six to 12 months, trimming near-term order flow for the risers market.

Other drivers and restraints analyzed in the detailed report include:

- Life-Extension Demand for Aging Shallow-Water Risers

- Rapid Adoption of Thermoplastic Composite Pipe Risers

- Escalating HSE and Environmental Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rigid designs will post an 8.7% CAGR, the fastest growth in the risers market, as operators replicate proven templates that compress engineering cycles and enable bulk sourcing. Shell's Gulf of Mexico brownfield program achieved 95% equipment commonality across three fields, trimming front-end engineering by 40%. Flexible risers still hold 45.3% of 2025 demand thanks to superior motion compliance, with TechnipFMC's Hammerhead order featuring electrically heated flexible lines to combat wax deposition. Hybrid concepts remain niche but vital in ultra-deepwater where top tension exceeds 1,000 tons, blending a seabed-anchored rigid section with a fatigue-resistant composite top string. The shift toward standardized rigid systems underpins procurement predictability, tilting market share toward contractors with high-capacity spoolbases.

Industry modularization also boosts aftermarket revenue: cataloged designs simplify spares stocking and streamline inspection protocols, lowering total cost of ownership. Nonetheless, flexible lines remain indispensable for complex tiebacks and life-extension programs where existing infrastructure dictates serpentine routing. Composite-steel hybrids are likely to proliferate as carbon-fiber tensile armor clears final qualification hurdles, offering weight savings that widen vessel choice and shrink installation windows in the risers market.

Composite alternatives will advance at 9.1% CAGR, eroding steel's 69.5% 2025 hold on the risers market size. Strohm's thermoplastic pipe is already moving beyond water-injection service toward full production duty with Petrobras in 2027. Magma Global targets high-temperature West African wells where steel would need costly active cooling. Field data show 77.7% weight reduction and comparable tensile capability, making composites attractive for reel-lay campaigns that cannot tolerate the deck loads of steel.

Regulatory acceptance removed the last barrier when DNV endorsed non-metallic risers for permanent service. Integrated fiber-optic sensing baked into the laminate turns each composite riser into a self-monitoring asset, obviating external instrumentation. Yet steel retains primacy in ultra-high-pressure sour service above 15,000 psi, where hydrogen embrittlement of polymer matrices is still a concern. Limited availability of reel-lay vessels and high initial material cost temper adoption speed, but the lifecycle economics remain compelling, ensuring composites capture incremental risers market share through the forecast period.

Geography Analysis

South America accounted for 35.7% of global demand in 2025 and will expand at an 8.4% CAGR, the fastest among all regions. Petrobras's SEAP II alone requires 24 risers rated for 10,000-psi pressures, while ExxonMobil's Hammerhead development in Guyana adds six production risers by 2029. Streamlined Brazilian permitting now cuts approval times to 12 months, and Guyana's USD 30 billion investment pipeline promises more than 40 new risers through 2028. The risers market benefits from predictable local-content rules that encourage regional fabrication and generate shorter logistics chains.

North America centers on brownfield optimization. Shell's Kaikias waterflood and multiple Gulf of Mexico refurbishments keep service demand elevated, while U.S. BOEM bonding changes lift up-front cost burdens. In Europe, the North Sea consolidates around super-operators; Shell and Equinor's Adura venture manages 140,000 boe/d under unified inspection programs that harvest economies of scale. UK carbon-capture regulations, effective in 2026, compel feasibility studies on new developments, tying future FIDs to integrated CCS concepts.

The Middle East and Asia-Pacific emerge as secondary poles. ADNOC's SARB Deep Gas and Nasr-115 expansions add corrosion-resistant alloy risers for sour-gas production, while CNOOC ramps up South China Sea activity with rigid strings at Kaiping 18-1. Southeast Asia lags due to price uncertainty and financing constraints, but Malaysia and Indonesia remain incremental contributors. Combined, these trends diversify the geographic revenue mix and insulate the global risers market from single-basin shocks.

- TechnipFMC

- Aker Solutions

- Subsea 7

- NOV Inc.

- Saipem

- Baker Hughes (OneSubsea)

- McDermott International

- Oceaneering International

- Vallourec

- Oil States Industries

- Prysmian Group

- Airborne Oil & Gas

- Shawcor

- Trelleborg Offshore

- Ocyan

- MODEC

- Kongsberg Maritime

- DeepOcean

- Sapura Energy

- Bourbon Offshore

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Revival of deep- & ultra-deepwater project FIDs

- 4.2.2 Surge in SURF package awards in Brazil & Guyana

- 4.2.3 Life-extension demand for ageing shallow-water risers

- 4.2.4 Rapid adoption of thermoplastic composite pipe (TCP) risers

- 4.2.5 CCS retrofit opportunities for offshore riser infrastructure

- 4.2.6 AI-enabled digital twins for predictive riser integrity

- 4.3 Market Restraints

- 4.3.1 Crude-oil price volatility impacting FID timing

- 4.3.2 Escalating HSE & environmental compliance costs

- 4.3.3 Scarcity of deepwater fatigue-analysis specialists

- 4.3.4 Long-lead forgings & metallurgy supply-chain bottlenecks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Flexible Risers

- 5.1.2 Rigid Risers

- 5.1.3 Hybrid Risers

- 5.2 By Material

- 5.2.1 Steel

- 5.2.2 Composite

- 5.2.3 Thermoplastic Composite Pipe

- 5.2.4 Others

- 5.3 By Deployment Depth

- 5.3.1 Shallow Water (Up to 500 m)

- 5.3.2 Deepwater (500 to 1,500 m)

- 5.3.3 Ultra-Deepwater (Above 1,500 m)

- 5.4 By Application

- 5.4.1 Drilling

- 5.4.2 Production

- 5.4.3 Workover

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 TechnipFMC

- 6.4.2 Aker Solutions

- 6.4.3 Subsea 7

- 6.4.4 NOV Inc.

- 6.4.5 Saipem

- 6.4.6 Baker Hughes (OneSubsea)

- 6.4.7 McDermott International

- 6.4.8 Oceaneering International

- 6.4.9 Vallourec

- 6.4.10 Oil States Industries

- 6.4.11 Prysmian Group

- 6.4.12 Airborne Oil & Gas

- 6.4.13 Shawcor

- 6.4.14 Trelleborg Offshore

- 6.4.15 Ocyan

- 6.4.16 MODEC

- 6.4.17 Kongsberg Maritime

- 6.4.18 DeepOcean

- 6.4.19 Sapura Energy

- 6.4.20 Bourbon Offshore

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

立管市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、深度、地區和競爭格局分類,2021-2031年

立管市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、深度、地區和競爭格局分類,2021-2031年 淺層表面市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)深海臍帶供應連系管、立管及輸油管市場商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。

淺層表面市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)深海臍帶供應連系管、立管及輸油管市場商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。 水下供應連系管管輸液管(SURF)市場:依產品種類、水深及區域分類海底立管市場機會、成長要素、產業趨勢分析及2026年至2035年預測油氣海底臍帶供應連系管、立管及輸油管市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、類型、地區及競爭格局分類,2021-2031年)海底儲槽市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年海底生產和處理系統市場-全球產業規模、佔有率、趨勢、機會及預測(依生產系統元件組件、處理系統類型、水深、地區及競爭格局分類,2021-2031年)

水下供應連系管管輸液管(SURF)市場:依產品種類、水深及區域分類海底立管市場機會、成長要素、產業趨勢分析及2026年至2035年預測油氣海底臍帶供應連系管、立管及輸油管市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、類型、地區及競爭格局分類,2021-2031年)海底儲槽市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年海底生產和處理系統市場-全球產業規模、佔有率、趨勢、機會及預測(依生產系統元件組件、處理系統類型、水深、地區及競爭格局分類,2021-2031年) 全球深海臍帶供應連系管、立管及輸油管市場

全球深海臍帶供應連系管、立管及輸油管市場 海底生產與處理系統:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)

海底生產與處理系統:市場佔有率分析、產業趨勢與統計、成長預測(2025-2030 年)