|

市場調查報告書

商品編碼

2019102

淺層表面市場機會、成長促進因素、產業趨勢分析及預測(2026-2035年)Shallow Depth SURF Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

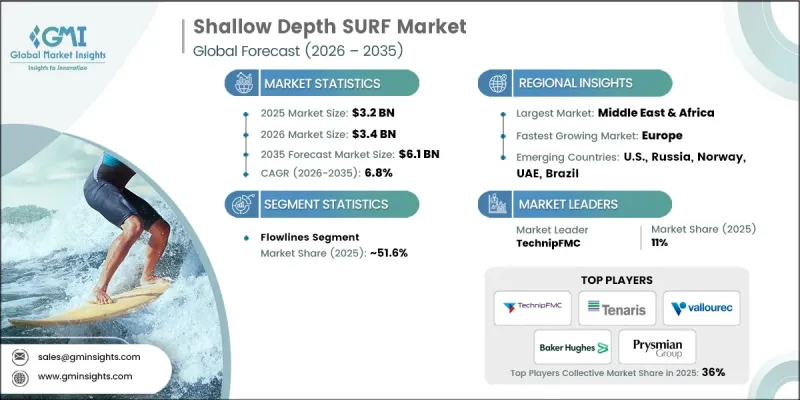

全球淺水衝浪市場預計到 2025 年將價值 32 億美元,預計到 2035 年將以 6.8% 的複合年成長率成長至 61 億美元。

市場擴張的驅動力來自海上油氣計畫投資的增加,以及產業為克服從不同地質構造中開採資源所面臨的技術和營運挑戰而做出的努力。浮體式鑽井平台數量的成長,以及將碳氫化合物從海底儲存高效地運輸到陸上加工設施的需求日益成長,進一步推動了該產業的發展。全球能源需求不斷成長而石油蘊藏量卻在下降,這促使企業採用先進的海底管道系統(SURF)材料和設計,以最大限度地降低故障風險。經濟高效的解決方案、創新的製造技術和更高的設計效率,使企業能夠在不影響安全性和性能的前提下降低SURF系統的成本。快速的工業化進程、新興市場和已開發國家的經濟成長,以及石油化工、發電和交通運輸等依賴碳氫化合物的行業的擴張,都在增強市場動力,並創造長期成長機會。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 32億美元 |

| 預測金額 | 61億美元 |

| 複合年成長率 | 6.8% |

預計到2025年,輸油管線產業將佔據51.6%的市場佔有率,並在2035年之前以6.2%的複合年成長率成長。輸油管線用於將油氣從海底油井輸送到陸上或海上加工設施,必須能夠承受極端壓力、零下低溫和惡劣的海底環境。正在進行的海上探勘和生產項目需要堅固耐用的設計,以確保安全可靠的運行,並延長海底生產系統的使用壽命。即時監測技術使營運商能夠評估輸油管線的狀況,識別潛在問題,並在不中斷作業的情況下更換受影響的管段,從而進一步加速這些系統的部署,並支援市場的持續擴張。

美國淺層地表探勘(SURF)市場佔52.9%的市場佔有率,預計到2025年市場規模將達到1.423億美元。這一區域成長主要得益於能源密集型產業投資的增加、豐富的海上油氣蘊藏量以及持續的探勘活動。政府對非傳統資源開發的支持,加上不斷成長的能源需求,共同創造了有利的市場環境。注重效率和成本最佳化的國內項目正在推動美國各地採用先進的SURF解決方案。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 原物料供應及採購分析

- 影響價值鏈的關鍵因素

- 中斷

- 影響產業的因素

- 成長促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 海底供應連系管、立管和輸油管的成本結構分析

- 價格趨勢分析,2022-2035年

- 依產品

- 按地區

- 新機會與趨勢

- 利用物聯網技術實現數位轉型

- 進入新興市場

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析:按地區分類

- 北美洲

- 歐洲

- 亞太地區

- 中東和非洲

- 拉丁美洲

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

第5章 市場規模及預測:依產品分類,2022-2035年

- 供應連系管

- 立管

- SCR

- 靈活的

- 其他

- 流線

第6章 市場規模及預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 挪威

- 荷蘭

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 印尼

- 馬來西亞

- 泰國

- 澳洲

- 中東和非洲

- 安哥拉

- 奈及利亞

- 埃及

- 卡達

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 拉丁美洲

- 巴西

第7章:公司簡介

- Alleima

- Baker Hughes

- DeRegt Cables

- Dril-Quip

- Halliburton

- Hohn Group

- JDR Cable Systems

- John Wood Group

- NOV

- Oceaneering International

- OneSubsea

- Prysmian Group

- Saipem

- Strohm

- Subsea7

- TechnipFMC

- Tenaris

- Tratos

- Vallourec

- Weatherford

The Global Shallow Depth SURF Market was valued at USD 3.2 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 6.1 billion by 2035.

The market expansion is driven by growing investments in offshore oil and gas projects and the industry's shift toward overcoming technical and operational challenges in extracting resources from diverse geological formations. Increasing floating rig counts, combined with the need for efficient hydrocarbon transport from subsea reservoirs to surface processing facilities, are further bolstering the industry. Rising global energy demand, coupled with depleting oil reserves, is encouraging the adoption of advanced SURF materials and designs to minimize failure risks. Cost-effective solutions, innovative manufacturing techniques, and improved design efficiency are enabling companies to reduce SURF system expenses without compromising safety or performance. Rapid industrialization, economic growth in emerging and developed regions, and the expansion of hydrocarbon-dependent sectors like petrochemicals, power generation, and transportation are reinforcing market momentum and creating long-term growth opportunities.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.2 Billion |

| Forecast Value | $6.1 Billion |

| CAGR | 6.8% |

The flowlines segment held 51.6% share in 2025 and is expected to grow at a CAGR of 6.2% through 2035. Flowlines are engineered to transport hydrocarbons from subsea wells to onshore or offshore processing facilities, enduring extreme pressures, subzero temperatures, and challenging seabed conditions. Ongoing offshore exploration and production projects require robust engineering to ensure safe and reliable operations while extending the lifespan of subsea production systems. Real-time monitoring technologies allow operators to assess flowline conditions, identify potential issues, and replace affected sections without interrupting operations, further accelerating the adoption of these systems and supporting continuous market expansion.

U.S. Shallow Depth SURF Market held 52.9% share, generating USD 142.3 million in 2025. The region's growth is supported by increasing investments in energy-intensive industries, abundant offshore oil and gas reserves, and ongoing exploration activities. Government initiatives supporting unconventional resource development, along with rising energy demand, are shaping a favorable market environment. Domestic projects focusing on efficiency and cost optimization are driving the deployment of advanced SURF solutions across the country.

Key players in the Global Shallow Depth SURF Market include Dril-Quip, TechnipFMC, Baker Hughes, NOV, Oceaneering International, Saipem, Alleima, Subsea7, Vallourec, Tratos, JDR Cable Systems, John Wood Group, Halliburton, Prysmian Group, Strohm, DeRegt Cables, Hohn Group, OneSubsea, and Weatherford. Companies operating in the Global Shallow Depth SURF Market are focusing on multiple strategies to strengthen their foothold. They invest heavily in R&D to develop durable, cost-efficient, and high-performance subsea solutions tailored to challenge offshore environments. Strategic partnerships with engineering, procurement, and construction firms expand their project capabilities and regional presence. Players also emphasize technological innovations such as real-time monitoring, predictive maintenance, and advanced material usage to improve system reliability and safety. Expanding manufacturing capacities and after-sales service networks ensure timely delivery and operational support. Additionally, companies are adopting sustainability initiatives, modular product designs, and digital integration to enhance competitiveness, meet client demands, and capture long-term market opportunities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid Sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Product trends

- 2.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of Subsea umbilicals, risers and flowlines

- 3.8 Price trend analysis, 2022-2035

- 3.8.1 By product

- 3.8.2 By region

- 3.9 Emerging opportunities & trends

- 3.9.1 Digital transformation with IoT technologies

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million, '000 Feet)

- 5.1 Key trends

- 5.2 Umbilicals

- 5.3 Risers

- 5.3.1 SCR

- 5.3.2 Flexible

- 5.3.3 Others

- 5.4 Flowlines

Chapter 6 Market Size and Forecast, By Region, 2022 - 2035, (USD Million, '000 Feet)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 UK

- 6.3.2 Norway

- 6.3.3 Netherlands

- 6.3.4 Russia

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Indonesia

- 6.4.4 Malaysia

- 6.4.5 Thailand

- 6.4.6 Australia

- 6.5 Middle East & Africa

- 6.5.1 Angola

- 6.5.2 Nigeria

- 6.5.3 Egypt

- 6.5.4 Qatar

- 6.5.5 Saudi Arabia

- 6.5.6 UAE

- 6.6 Latin America

- 6.6.1 Brazil

Chapter 7 Company Profiles

- 7.1 Alleima

- 7.2 Baker Hughes

- 7.3 DeRegt Cables

- 7.4 Dril-Quip

- 7.5 Halliburton

- 7.6 Hohn Group

- 7.7 JDR Cable Systems

- 7.8 John Wood Group

- 7.9 NOV

- 7.10 Oceaneering International

- 7.11 OneSubsea

- 7.12 Prysmian Group

- 7.13 Saipem

- 7.14 Strohm

- 7.15 Subsea7

- 7.16 TechnipFMC

- 7.17 Tenaris

- 7.18 Tratos

- 7.19 Vallourec

- 7.20 Weatherford

2026-2030年全球海底供應連系管、立管、輸油管(SURF)市場

2026-2030年全球海底供應連系管、立管、輸油管(SURF)市場 Riser:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)

Riser:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031) 立管市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、深度、地區和競爭格局分類,2021-2031年

立管市場 - 全球產業規模、佔有率、趨勢、機會、預測:按類型、深度、地區和競爭格局分類,2021-2031年 深海臍帶供應連系管、立管及輸油管市場商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。

深海臍帶供應連系管、立管及輸油管市場商業機會、成長要素、產業趨勢分析及 2026-2035 年預測。 水下供應連系管管輸液管(SURF)市場:依產品種類、水深及區域分類海底立管市場機會、成長要素、產業趨勢分析及2026年至2035年預測油氣海底臍帶供應連系管、立管及輸油管市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、類型、地區及競爭格局分類,2021-2031年)海底儲槽市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年海底生產和處理系統市場-全球產業規模、佔有率、趨勢、機會及預測(依生產系統元件組件、處理系統類型、水深、地區及競爭格局分類,2021-2031年)

水下供應連系管管輸液管(SURF)市場:依產品種類、水深及區域分類海底立管市場機會、成長要素、產業趨勢分析及2026年至2035年預測油氣海底臍帶供應連系管、立管及輸油管市場-全球產業規模、佔有率、趨勢、機會及預測(依產品、類型、地區及競爭格局分類,2021-2031年)海底儲槽市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年海底生產和處理系統市場-全球產業規模、佔有率、趨勢、機會及預測(依生產系統元件組件、處理系統類型、水深、地區及競爭格局分類,2021-2031年) 全球深海臍帶供應連系管、立管及輸油管市場

全球深海臍帶供應連系管、立管及輸油管市場